Medical Device Packaging Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Material (Plastic, Paper & Paperboard, Metal, Others); By Product (Pouches & Bags, Trays, Boxes, Clamshells, Others); By Application (Disposable Consumables, Therapeutic Equipment, Monitoring & Diagnostic Equipment); and Geography

2025-07-25

Packaging Industry

Jaya Bundele (Research Analyst)

Description

Medical Device Packaging Market Overview

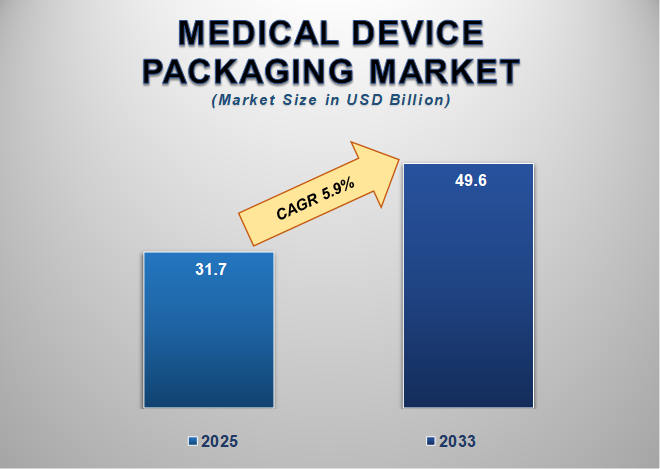

The Global Medical Device Packaging Market size is witnessing steady growth, driven by the increasing demand for advanced healthcare solutions, rising regulatory standards, and the growing need for sterile, safe, and reliable packaging formats. Valued at USD 31.7 billion in 2025, the market is forecasted to reach USD 49.6 billion by 2033, expanding at a CAGR of 5.9% during the forecast period. Medical device packaging plays a crucial role in ensuring the integrity, safety, and functionality of a wide range of medical instruments, consumables, implants, and diagnostic equipment. It must comply with stringent regulatory and sterilization standards while supporting efficient distribution and shelf-life preservation.

One of the key market growth

drivers is the surge in demand for minimally invasive surgical instruments and

disposable medical devices. As the global population ages and chronic diseases

become more prevalent, the production of medical devices is rising, thereby

boosting the demand for effective packaging solutions. The trend toward home

healthcare and the increasing adoption of wearable medical technologies also

contribute to the expansion of this market, as these products require robust

and user-friendly packaging. Moreover, the market analysis highlights growing

investments in packaging innovation, including sustainable materials,

tamper-evident designs, and smart labeling technologies that enhance

traceability and patient safety. Manufacturers are increasingly focused on

meeting regulatory compliance from organizations like the FDA and ISO, further

pushing advancements in medical-grade packaging.

Medical Device Packaging Market Drivers and Opportunities

Increasing demand for sterile and safe packaging solutions is anticipated to lift the medical device packaging market during the forecast period

The global medical device

packaging market is largely driven by the need for sterile, contamination-free

packaging. Devices must stay safe from germs, physical damage, and chemical

changes throughout their shelf life and transport. As health care systems get

more advanced and patient safety remains a top goal, manufacturers are

investing in better packaging methods that keep items sterile. Critical tools

like surgical tools, implants, catheters, and test kits require special

protection. Regulatory agencies such as the U.S. FDA, the European Medicines

Agency (EMA), and ISO have strict rules on packaging materials and processes.

These rules, along with rising awareness of hospital-acquired infections and

their costs, boost the use of tamper-proof, barrier, and sterilizable packaging

options. Innovations like multi-layer films, coatings that kill bacteria, and

high-barrier blister packs are becoming more popular. This shows how important

sterile packaging is for the industry. As demand for single-use and disposable

medical devices grows, especially in developing countries and outpatient

clinics, the need for reliable sterile packaging rises. This trend plays a big

role in driving market growth.

Stringent regulatory standards for medical packaging drive the global medical device packaging market

Stringent regulatory standards

are a key factor shaping the global medical device packaging market. Agencies

like the U.S. FDA, ISO, and EU MDR set strict rules for how medical devices

should be packaged, especially those that need to stay sterile. These rules

cover labeling, barrier qualities, seal strength, biocompatibility, and

resistance to sterilization methods like gamma rays or ethylene oxide. Meeting

these detailed standards is crucial to ensure devices work properly, remain

safe for patients, and stay intact during storage and shipping. Because of

this, manufacturers and packaging firms are working together more often to

create high-quality, compliant solutions. The push for harmonized regulations,

such as ISO 11607 for sterilized packaging systems, pushes companies to update

their packaging. This shift has increased demand for precise materials and

testing services to validate packaging. The rise in traceability,

anti-counterfeit measures, and serialization, aligned with global device ID

rules, also adds complexity. These regulations drive innovation and influence

the overall direction of the market.

Opportunity for the Medical Device Packaging Market

Growth of home healthcare and point-of-care devices is a significant opportunity in the global medical device packaging market

The move toward home healthcare

and the rise of point-of-care (PoC) medical devices offer a major opportunity

for the packaging industry. As remote monitoring, telehealth, and wearable

diagnostic tools become more common, more patients are managing chronic

conditions like diabetes, hypertension, and heart disease at home. This shift

calls for packaging that is safe, sterile, and easy for patients to use, open,

and dispose of. It must also be designed with those who have limited mobility

or cognitive issues in mind, while still meeting all regulatory rules. Devices

used in pharmacies and clinics need packaging that allows quick setup, safe

storage, and clear labels. This growing trend creates a strong market for

packaging that is smart, simple, and accessible. Adding features like QR codes,

temperature indicators, and authentication tags can create value-added

solutions suited for home and mobile care. As healthcare moves away from

hospitals and clinics toward more decentralized care, demand for specialized packaging

will increase. This shift will open new revenue streams for companies that

develop innovative packaging solutions for this sector.

Medical Device Packaging Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 31.7 Billion |

|

Market Forecast in 2033 |

USD 49.6 Billion |

|

CAGR % 2025-2033 |

5.9% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production Capacity, growth factors and more |

|

Segments Covered |

●

By Material ●

By Product ●

By Application |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Medical Device Packaging Market Report Segmentation Analysis

The global Medical Device

Packaging industry analysis is segmented by Material, by Product, by

Application, and by region.

The plastic segment accounted for the largest market share in the global medical device packaging market

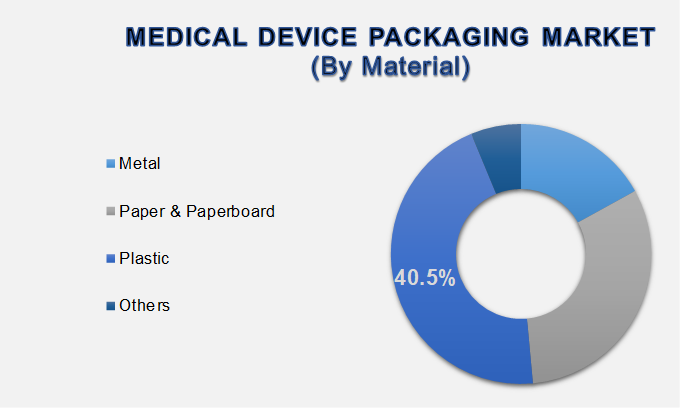

By Material, the Market is Segmented into Plastic, Paper & Paperboard, Metal, and Others. The plastic segment accounted for the largest market share, over 40.5% in the global medical device packaging market. Plastics are widely used in medical packaging due to their versatility, durability, lightweight properties, and ability to form airtight and sterile barriers. Materials such as polyethylene (PE), polypropylene (PP), and polyvinyl chloride (PVC) are commonly utilized for creating flexible and rigid packaging solutions that meet the stringent safety and sterilization requirements of medical devices. The segment's dominance is driven by the increasing production of disposable medical supplies, the rising demand for cost-effective materials, and the compatibility of plastics with various sterilization techniques. Moreover, plastic’s adaptability for high-speed production and its suitability for creating tamper-evident and transparent packaging further contribute to its widespread use across the healthcare sector.

The pouches & bags segment holds a major share in the medical

device packaging market

By Product, the Market is

Segmented into Pouches & Bags, Trays, Boxes, Clamshells, and Others. The

pouches & bags segment holds the major share in the medical device

packaging market. Pouches and bags offer a flexible, sterile, and

cost-efficient packaging solution, making them ideal for disposable devices,

diagnostic kits, catheters, and surgical instruments. The segment is primarily

driven by the growing demand for single-use medical consumables and the

expanding use of minimally invasive surgical tools that require compact, secure

packaging. Additionally, the trend toward portable and home-use medical devices

has further boosted the demand for pouches and bags due to their lightweight

and user-friendly design.

The disposable consumables segment dominates in medical device packaging market

By Application, the Market is

Segmented into Disposable Consumables, Therapeutic Equipment, and Monitoring

& Diagnostic Equipment. The disposable consumables segment dominates the

global medical device packaging market. This category includes products such as

syringes, surgical gloves, IV kits, and catheters that are designed for single

use to minimize infection risk and ensure patient safety. The increasing

emphasis on infection control, particularly in the wake of global health crises

like COVID-19, has significantly amplified the consumption of disposable

medical supplies. As a result, the demand for secure, sterile, and convenient

packaging solutions for these consumables has surged.

The following segments are part of an in-depth analysis of the global Medical Device Packaging Market:

|

Market Segments |

|

|

By Material |

●

Plastic ●

Paper &

Paperboard ●

Metal ●

Others |

|

By Product |

●

Pouches & Bags ●

Trays ●

Boxes ●

Clamshells ●

Others |

|

By Application |

●

Disposable

Consumables ●

Therapeutic

Equipment ●

Monitoring &

Diagnostic Equipment |

Medical Device Packaging Market Share Analysis by Region

The North America region is projected to hold the largest share of the global medical device packaging market over the forecast period.

North America accounted for the

largest share of 36.5% in the global medical device packaging market in 2025.

It continues to lead because of its advanced healthcare system, strict

regulations, and many top medical device makers. The region benefits from high

healthcare spending, quick adoption of new technologies, and a large elderly

population. These factors increase the need for medical devices and reliable

packaging that meets all standards. U.S. FDA rules and ISO standards push

companies to use high-quality, tamper-proof, and sterilizable packages. A focus

on patient safety and the rise of disposable medical products has sparked new

packaging ideas for hospitals, clinics, and home care. North America also needs

strong packaging for exports, which often travel long distances and face

different environments. This need helps keep the region a leader in the global

market.

Meanwhile, the Asia Pacific area

is set to see the fastest growth rate over the coming years. Rapid city growth,

better healthcare systems, and a bigger demand for affordable medical devices

are major reasons. Countries such as China, India, and Japan are producing and

using more local medical devices. This boosts the need for cost-efficient and

effective packaging options.

Medical Device Packaging Market Competition Landscape Analysis

The market is

competitive, with several established players and new entrants offering a range

of products. Some of the key players are Amcor plc, Berry Global Group, Inc.,

AVERY DENNISON CORPORATION, Sonoco Products Company, and others.

Global Medical Device Packaging Market Recent Developments News:

- In February 2024, Berry Global Inc. revealed plans

to spin off its Health, Hygiene, and Specialties Global Nonwovens and

Films (HHNF) segment and merge it with Glatfelter Corporation. This

strategic move aims to streamline operations and enhance market positioning

in the specialty materials sector.

- In January 2024, Amcor Plc announced an expansion of its

thermoforming production capabilities in North America to address rising

demand from the medical, pharmaceutical, and consumer health industries.

The investment strengthens Amcor's ability to deliver high-performance

packaging solutions for critical healthcare applications.

The Global Medical Device Packaging Market is dominated by a few large companies, such as

●

Amcor PLC

●

DuPont

●

SteriPack

●

Wipak Walothen GmbH

●

Sonoco Products

Company

●

Sealed Air

●

Tekni-Plex, Inc.

●

Nelipak

●

Oliver

●

Berry Global Inc.

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

- Global Medical Device Packaging Market Introduction and Market Overview

- Objectives of the Study

- Global Medical Device Packaging Market Scope and Market Estimation

- Global Medical Device Packaging Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Medical Device Packaging Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2033

- Market Segmentation

- Material of Global Medical Device Packaging Market

- Product of Global Medical Device Packaging Market

- Application of Global Medical Device Packaging Market

- Region of Global Medical Device Packaging Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Medical Device Packaging Market

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Medical Device Packaging Market Estimates & Historical Trend Analysis (2021 - 2024)

- Global Medical Device Packaging Market Estimates & Forecast Trend Analysis, by Material

- Global Medical Device Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Material, 2021 - 2033

- Plastic

- Paper & Paperboard

- Metal

- Others

- Global Medical Device Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Material, 2021 - 2033

- Global Medical Device Packaging Market Estimates & Forecast Trend Analysis, by Product

- Global Medical Device Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Product, 2021 - 2033

- Pouches & Bags

- Trays

- Boxes

- Clamshells

- Others

- Global Medical Device Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Product, 2021 - 2033

- Global Medical Device Packaging Market Estimates & Forecast Trend Analysis, by Application

- Global Medical Device Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2033

- Disposable Consumables

- Therapeutic Equipment

- Monitoring & Diagnostic Equipment

- Global Medical Device Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2033

- Global Medical Device Packaging Market Estimates & Forecast Trend Analysis, by region

- Global Medical Device Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Medical Device Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America Medical Device Packaging Market: Estimates & Forecast Trend Analysis

- North America Medical Device Packaging Market Assessments & Key Findings

- North America Medical Device Packaging Market Introduction

- North America Medical Device Packaging Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Material

- By Product

- By Application

- By Country

- The U.S.

- Canada

- North America Medical Device Packaging Market Assessments & Key Findings

- Europe Medical Device Packaging Market: Estimates & Forecast Trend Analysis

- Europe Medical Device Packaging Market Assessments & Key Findings

- Europe Medical Device Packaging Market Introduction

- Europe Medical Device Packaging Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Material

- By Product

- By Application

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Switzerland

- Rest of Europe

- Europe Medical Device Packaging Market Assessments & Key Findings

- Asia Pacific Medical Device Packaging Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Medical Device Packaging Market Introduction

- Asia Pacific Medical Device Packaging Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Material

- By Product

- By Application

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Medical Device Packaging Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Medical Device Packaging Market Introduction

- Middle East & Africa Medical Device Packaging Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Material

- By Product

- By Application

- By Country

- South Africa

- UAE

- Saudi Arabia

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Medical Device Packaging Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Medical Device Packaging Market Introduction

- Latin America Medical Device Packaging Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Material

- By Product

- By Application

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Medical Device Packaging Market Product Mapping

- Global Medical Device Packaging Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Medical Device Packaging Market Tier Structure Analysis

- Global Medical Device Packaging Market Concentration & Company Market Shares (%) Analysis, 2023

- Company Profiles

- Amcor PLC

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Amcor PLC

* Similar details would be provided for all the players mentioned below

- DuPont

- SteriPack

- Wipak Walothen GmbH

- Sonoco Products Company

- Sealed Air

- Tekni-Plex, Inc.

- Nelipak

- Oliver

- Berry Global Inc.

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables