Global 3D Metrology Market Size and Forecast (2026–2034), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage; Offering (Hardware, Software, and Services), Technology (Coordinate Measuring Machines, Optical Digitizers and Scanners, Video Measuring Machines, and Others), End Use (Automotive, Aerospace & Defense, Electronics, Industrial Manufacturing, and Others), and Geography

2026-03-10

Semiconductor and Electronics

Ekta Chaurasia (Team Lead)

Description

Global 3D Metrology Market Overview

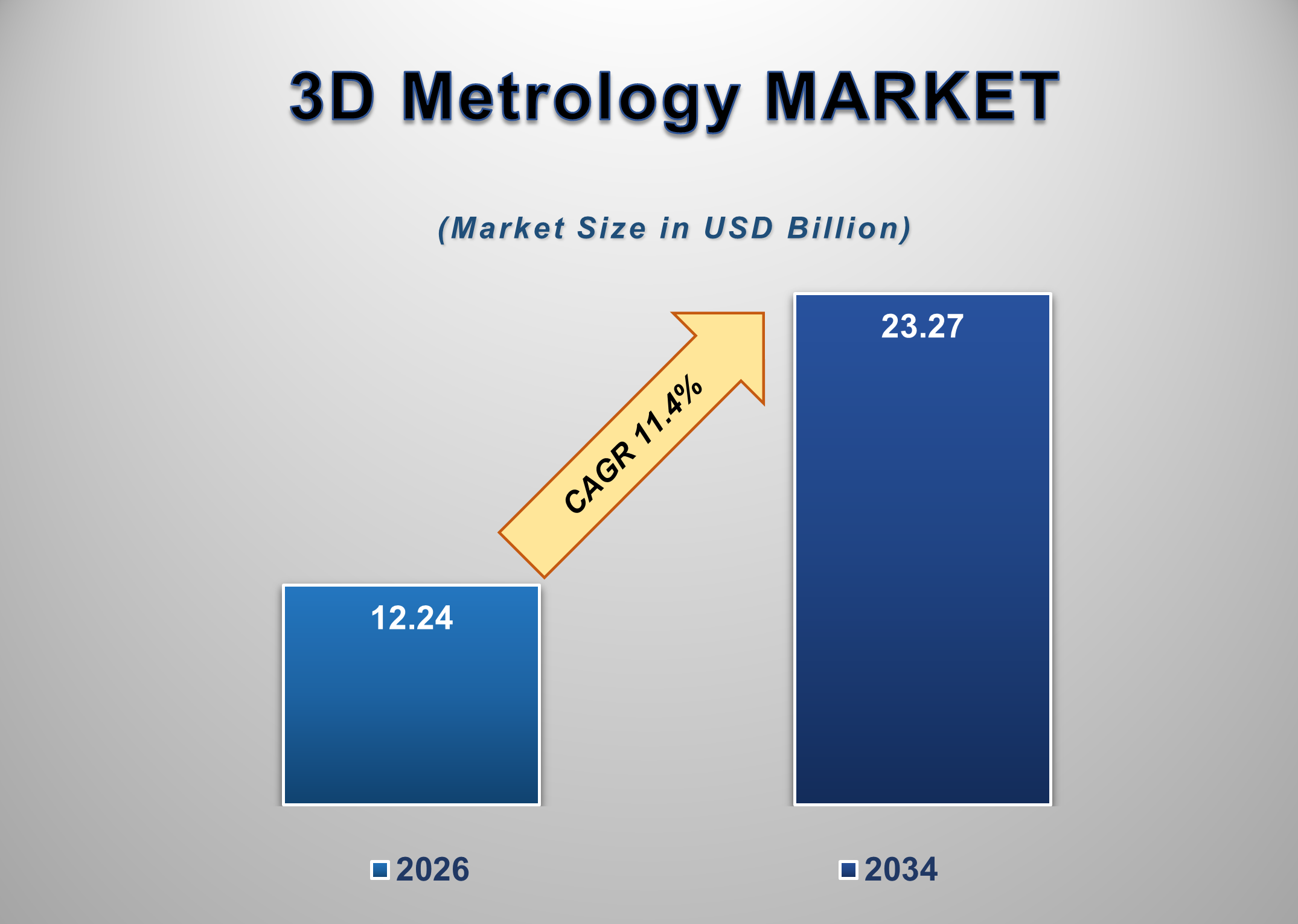

The global 3D metrology market is witnessing robust growth, driven by the increasing demand for high-precision measurement and quality inspection across manufacturing industries. Valued at USD 12.24 billion in 2026, the market is projected to reach USD 23.27 billion by 2034, expanding at a CAGR of 8.2% during the forecast period.

3D metrology refers to advanced measurement technologies used to inspect, analyze, and verify the physical dimensions and geometrical characteristics of components and assemblies. These systems play a critical role in ensuring product quality, reducing manufacturing errors, and supporting compliance with stringent industry standards. Technologies such as coordinate measuring machines (CMMs), optical scanners, laser trackers, and structured-light systems enable manufacturers to achieve micron-level accuracy across complex geometries.

The rising adoption of automation, smart manufacturing, and Industry 4.0 initiatives is significantly accelerating market growth. Industries such as automotive and aerospace increasingly rely on 3D metrology solutions for dimensional inspection, reverse engineering, and in-line quality control. Additionally, the growing complexity of manufactured components, lightweight materials, and tighter tolerances is driving the need for advanced non-contact measurement systems.

Technological advancements in sensors, imaging, and software analytics have enhanced the speed, accuracy, and ease of use of 3D metrology solutions. The integration of artificial intelligence, cloud computing, and digital twin technologies is further expanding application capabilities, enabling real-time inspection and predictive quality management.

Despite strong growth prospects, the market faces challenges such as high initial investment costs, skilled labor requirements, and integration complexities within existing production lines. However, the long-term benefits of reduced rework, improved productivity, and enhanced product reliability outweigh these constraints.

The global 3D metrology market is expected to grow steadily as manufacturers prioritize precision engineering, digital transformation, and zero-defect production strategies. Increasing adoption across emerging economies and continuous innovation in measurement technologies position 3D metrology as a cornerstone of modern manufacturing ecosystems.

Global 3D Metrology Market Drivers and Opportunities

Quality Assurance Imperatives in Precision-Critical Industries

The increasing complexity of manufactured parts, especially in sectors like aerospace, medical devices, and EV powertrains, has elevated quality assurance from a compliance task to a strategic priority. Traditional measurement techniques fail to detect micro-level deviations in free-form, multi-axis components, while 3D metrology systems can generate dense point-cloud data, enabling manufacturers to validate tolerances with micron-level precision. For example, aerospace OEMs use high-resolution optical scanners to inspect turbine blades and structural airframe components, where even slight dimensional errors compromise aerodynamic performance and safety certifications. Similarly, in electric vehicle (EV) battery assemblies, 3D metrology tools are crucial for verifying electrode alignment and weld quality, factors directly impacting battery life and thermal performance. This requirement for precision has driven capital investment into 3D CMMs, laser trackers, and non-contact scanning systems, making quality assurance a core revenue driver for the market.

Integration with Digital Engineering and Real-Time Process Control

Three-dimensional metrology is no longer a standalone inspection activity, it’s increasingly embedded into smart manufacturing workflows. The integration of metrology systems with digital engineering platforms (e.g., CAD, PLM, and digital twin environments) enables in-process measurement and automated feedback loops. This integration allows manufacturers to detect deviations during production rather than at final inspection, reducing rework, scrap, and throughput delays. For instance, automotive OEMs have integrated laser trackers with real-time PLC systems on final assembly lines, enabling instantaneous corrective adjustments to robotic weld paths. The rise of cloud-based metrology software also permits remote analysis of measurement data, facilitating global quality governance across distributed manufacturing sites. This convergence of 3D metrology and digital manufacturing ecosystems is a structural driver, not a trend, because it fundamentally shifts quality validation from batch inspection to continuous, data-driven process control.

Expansion of Non-Contact Metrology in Automated & Large-Volume Production

A major opportunity for market expansion lies in non-contact 3D metrology technologies, including structured-light scanning, photogrammetry, and laser triangulation, particularly within large-volume and automated environments where traditional contact methods are impractical. Non-contact systems can rapidly capture millions of data points with minimal impact on cycle time, enabling inspection of complex surface textures and thin-wall components without physical contact or fixturing.

Industrial manufacturers are increasingly adopting non-contact metrology at scale for several reasons:

Ultra-fast throughput: Structured-light scanners can measure entire automotive body panels in seconds, supporting real-time quality decisions within high-speed production lines.

Complex geometry capability: Curved, free-form shapes common in aerospace and consumer electronics are better quantified through dense point clouds that non-contact systems capture.

Automation readiness: These systems interface more easily with robotic manipulators and automated conveyors, enabling unattended inspection and data logging.

Advanced analytics enablement: The rich data sets produced by non-contact metrology feed AI-powered defect prediction models, allowing manufacturers to trend quality deviations and forecast failure risks before they occur.

As automation and Industry 4.0 initiatives deepen globally, especially in Asia-Pacific and North America, the deployment of non-contact 3D metrology within smart factories offers a significant growth opportunity. Strategic investments in scalable, high-speed inspection systems are expected to unlock demand in sectors that were previously constrained by cost, speed, or technology limitations.

Global 3D Metrology Market Scope

Market Segment

Global 3D Metrology Market Report Segmentation Analysis

The global 3D metrology market analysis is segmented by Offering, Technology, End Use, and Region. The Optical Digitizers and Scanners segment dominated the market in 2025 and is expected to register the highest CAGR during the forecast period.

By technology, the market includes coordinate measuring machines, optical digitizers and scanners, video measuring machines, and others. Optical digitizers and scanners account for the largest share due to their non-contact measurement capabilities, high speed, and ability to capture complex geometries. These systems use laser or structured-light technology to generate accurate 3D representations of components. Their application in reverse engineering, quality inspection, and rapid prototyping makes them highly valuable across industries. The portability, ease of integration, and declining costs of optical systems further support their widespread adoption.

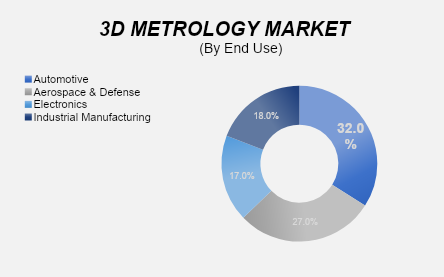

End Use Segment Analysis

The Automotive segment holds the largest share of the end-use segment over the forecast period.

The automotive industry extensively utilizes 3D metrology solutions for dimensional inspection, body-in-white analysis, powertrain measurement, and quality assurance. With the rise of electric vehicles and lightweight materials, manufacturers require precise measurement tools to ensure component compatibility and structural integrity. 3D metrology enables faster inspection cycles, reduced rework, and improved production efficiency. Automotive manufacturers also integrate metrology systems into automated production lines to support high-volume manufacturing and maintain consistent quality standards.

Global 3D Metrology Market Share Analysis by Region

North America is projected to hold a significant share of the global 3D metrology market over the forecast period.

North America’s dominance is attributed to the presence of advanced manufacturing industries, strong adoption of automation technologies, and early implementation of Industry 4.0 practices. The United States leads the regional market due to high investments in aerospace, automotive, and electronics manufacturing. The presence of major metrology solution providers, continuous technological innovation, and a strong focus on quality assurance further support market growth. Increasing adoption of digital inspection solutions and smart manufacturing initiatives is expected to sustain regional leadership.

Global 3D Metrology Market Recent Developments News

In March 2024, Hexagon AB launched an advanced optical scanning solution integrated with AI-driven analytics to enhance real-time quality inspection in automotive manufacturing.

In July 2025, FARO Technologies expanded its portable 3D metrology product portfolio to support large-scale industrial inspection and aerospace applications.

In October 2025, ZEISS Industrial Metrology introduced a cloud-enabled metrology software platform to improve data integration and digital workflow efficiency across manufacturing operations.

Competitive Landscape

The Global 3D Metrology Market is dominated by a few large companies, such as

Hexagon AB

Carl Zeiss AG

FARO Technologies, Inc.

Nikon Metrology NV

Mitutoyo Corporation

Keyence Corporation

Renishaw plc

Creaform Inc. (a TECNALIA company)

Leica Geosystems (Hexagon Group)

ZEISS Industrial Metrology (Carl Zeiss group)

Perceptron, Inc.

KLA Corporation (including CV Group / LMI Technologies)

Trimble Inc.

Topcon Positioning Systems, Inc.

GOM GmbH (a ZEISS company)

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

3D Metrology Market

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables