Aerostructures Market Size and Forecast (2026–2034), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Component (Fuselage, Wings, Empennage, Nacelles & Pylons, Flight Control Surfaces, Doors & Interiors, Others); By Material (Aluminum Alloys, Titanium Alloys, Composite Materials, Steel Alloys, Others); By Platform (Commercial Aircraft, Military Aircraft, Business Jets, Helicopters, Unmanned Aerial Vehicles, Urban Air Mobility Aircraft); By End User (OEMs, MRO Providers, Defense Organizations, Aircraft Leasing Companies), and Geography

2026-06-22

Aerospace & Defense

Ekta Chaurasia (Team Lead)

Description

Aerostructures Market Overview

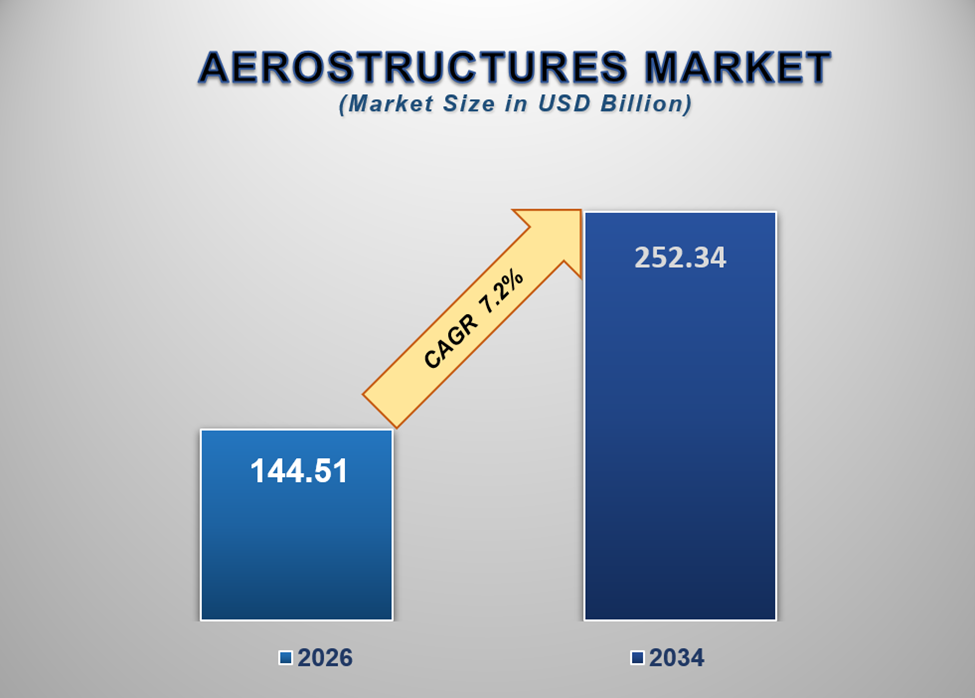

The global Aerostructures

Market was valued at USD 144.51 billion in 2026 and is projected to

reach USD 252.34 billion by 2034, growing at a CAGR of 7.2% during

the forecast period. The market is witnessing robust expansion due to

increasing aircraft production, rising global passenger traffic, growing

defense modernization programs, and continuous technological advancements in

lightweight structural materials and manufacturing technologies.

Aerostructures

form the backbone of every aircraft and include critical structural components

such as fuselages, wings, empennages, nacelles, pylons, flight control

surfaces, and structural assemblies. These components are engineered to

withstand extreme operational conditions while ensuring safety, performance,

fuel efficiency, and structural integrity throughout the aircraft lifecycle.

The

aerostructures market plays a fundamental role in the global aerospace industry

because structural systems account for a significant portion of aircraft

manufacturing costs and directly influence aircraft weight, operational

efficiency, payload capacity, and maintenance requirements. As airlines seek

more fuel-efficient aircraft and governments invest in advanced military

platforms, demand for innovative aerostructure solutions continues to rise.

The increasing

recovery and expansion of commercial aviation is creating substantial demand

for new-generation narrow-body and wide-body aircraft. Growing passenger

volumes, expanding airline fleets, and rising air travel demand across emerging

economies are encouraging aircraft manufacturers to increase production rates,

thereby driving aerostructure demand globally.

Simultaneously,

military modernization initiatives are accelerating procurement of fighter

jets, transport aircraft, surveillance platforms, rotorcraft, and unmanned

aerial systems. Defense agencies are increasingly prioritizing lightweight,

durable, and technologically advanced structural components capable of

enhancing aircraft performance and mission effectiveness.

One of the most

transformative trends shaping the market is the growing adoption of composite

materials. Aerospace manufacturers are increasingly replacing traditional

metallic structures with advanced composites to reduce weight, improve

corrosion resistance, enhance fatigue performance, and increase fuel

efficiency. Modern aircraft platforms incorporate significantly higher

proportions of composite materials than previous generations, creating

substantial opportunities for aerostructure suppliers.

Additionally,

advanced manufacturing technologies such as additive manufacturing, robotic

assembly systems, digital twins, automated fiber placement, and artificial

intelligence-assisted quality inspection are transforming aerostructure

production processes. These innovations improve manufacturing precision, reduce

production costs, shorten development timelines, and enhance product

consistency.

As the aerospace sector continues prioritizing operational efficiency, sustainability, lightweight design, and advanced manufacturing capabilities, the aerostructures market is expected to maintain strong growth momentum throughout the forecast period.

Aerostructures Market Drivers and

Opportunities

Expanding

Commercial Aircraft Production Is Driving Market Growth

The rapid

expansion of global commercial aviation remains one of the most significant

drivers of the aerostructures market.

Air passenger

traffic continues to increase due to economic development, urbanization,

tourism growth, rising disposable incomes, and expanding connectivity across

both developed and emerging economies. Airlines are actively expanding and

modernizing their fleets to accommodate growing travel demand, creating

substantial opportunities for aerostructure manufacturers.

Aircraft

manufacturers are experiencing significant order backlogs as airlines place

long-term orders for fuel-efficient aircraft capable of reducing operating

costs and meeting environmental objectives. Every new aircraft produced

requires a wide range of aerostructural components, directly supporting market

growth.

The increasing

popularity of low-cost carriers is also contributing to aircraft demand. Budget

airlines are expanding operations globally, particularly in Asia-Pacific, the

Middle East, and Latin America, leading to increased procurement of narrow-body

aircraft and associated structural systems.

Furthermore,

fleet replacement programs are creating additional demand. Many airlines are

retiring older aircraft and replacing them with advanced platforms featuring

lightweight structures, improved aerodynamics, and enhanced fuel efficiency.

As commercial aviation continues its long-term growth trajectory, aerostructure manufacturers are expected to benefit from increasing production volumes and expanding global aircraft fleets.

Rising

Adoption of Composite Materials Is Transforming Aircraft Manufacturing

The growing use

of advanced composite materials is revolutionizing aerostructure design and

manufacturing.

Aircraft

manufacturers are increasingly incorporating carbon fiber-reinforced polymers,

glass fiber composites, and hybrid composite materials into structural

assemblies. These materials offer substantial advantages over conventional

metals, including reduced weight, improved corrosion resistance, enhanced

fatigue performance, and greater design flexibility.

Weight reduction

remains a critical objective within the aerospace industry because lighter

aircraft consume less fuel, generate lower emissions, and provide improved

operational efficiency. Even modest weight reductions can translate into

significant fuel savings over an aircraft's operational lifespan.

Composite

structures also enable manufacturers to create more aerodynamically optimized

designs while reducing the number of individual components required during

assembly. This contributes to improved structural efficiency and lower

maintenance requirements.

Advanced

military aircraft programs are similarly increasing reliance on composite

materials due to their strength-to-weight advantages and ability to support

stealth technologies.

As material

science continues advancing and manufacturing costs gradually decline,

composite adoption is expected to expand across commercial, military, and

emerging aviation platforms.

Urban Air

Mobility and Advanced Air Mobility Platforms Present Significant Opportunities

The emergence of

urban air mobility (UAM) and advanced air mobility (AAM) ecosystems represents

a major opportunity for the aerostructures industry.

Electric

vertical takeoff and landing (eVTOL) aircraft, air taxis, autonomous aerial

vehicles, and next-generation regional mobility platforms require innovative

structural designs optimized for lightweight performance, battery integration,

safety, and operational efficiency.

Many of these

aircraft rely heavily on advanced composite materials and novel structural

architectures that differ substantially from traditional aircraft designs.

Governments,

aviation regulators, technology firms, and aerospace manufacturers are

investing heavily in urban mobility programs aimed at transforming future

transportation systems. As these initiatives progress toward commercialization,

demand for specialized aerostructure solutions is expected to increase

significantly.

In addition, the

growth of unmanned aerial systems across commercial, military, logistics,

agricultural, and surveillance applications is creating new opportunities for

structural component manufacturers.

Manufacturers

capable of developing lightweight, durable, and highly efficient aerostructures

tailored to emerging aviation platforms are expected to benefit from

substantial long-term growth opportunities.

Aerostructures Market Scope

|

Report Attributes |

Description |

|

Market Size in 2026 |

USD

144.51 Billion |

|

Market Forecast in 2034 |

USD 252.34 Billion |

|

CAGR % 2026-2034 |

7.2% |

|

Base Year |

2025 |

|

Historic Data |

2021-2025 |

|

Forecast Period |

2026-2034 |

|

Report USP |

Production, Consumption, Company

Share, Company Heatmap, Company Production, Service Type, Growth Factors and

more |

|

Segments Covered |

∙ By Component |

|

Regional Scope |

● North

America ● Europe ● APAC ● Latin

America ● Middle

East and Africa |

|

Country Scope |

U.S. Canada U.K. Germany France Italy Spain Switzerland China India Japan South Korea Australia Mexico Brazil Argentina Saudi Arabia UAE South Africa |

Aerostructures

Market Report Segmentation Analysis

The global aerostructures market industry analysis is segmented by component, by material, by platform, by end user, and by region.

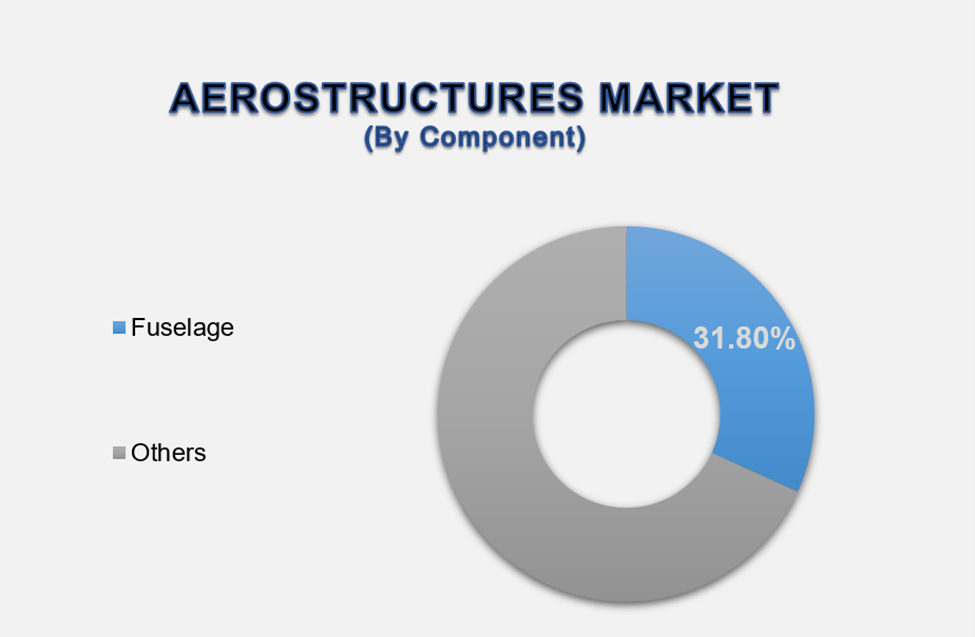

Fuselage

Segment Is Expected to Dominate the Market During the Forecast Period

The fuselage

segment accounted for approximately 31.8% of the global market, making

it the largest component category.

The fuselage

serves as the primary structural body of an aircraft and represents one of the

most complex, material-intensive, and high-value aerostructural assemblies. It

houses passengers, cargo, avionics systems, fuel systems, cockpit modules, and

numerous operational subsystems.

The dominance of

this segment is primarily attributed to the extensive engineering,

manufacturing complexity, and material requirements associated with fuselage

production. Modern fuselage structures require advanced design approaches to

balance strength, weight, durability, safety, and aerodynamic performance.

Increasing

production rates of commercial aircraft are significantly driving demand for

fuselage structures. As airlines expand fleets and aircraft manufacturers ramp

up deliveries, fuselage suppliers continue experiencing strong order volumes.

The segment is

also benefiting from increasing use of composite materials, which help reduce

aircraft weight while improving operational performance. New-generation

aircraft incorporate larger composite fuselage sections than previous models,

creating opportunities for advanced materials manufacturers.

Furthermore,

military aviation programs continue investing in next-generation airframes

featuring enhanced survivability, mission adaptability, and lightweight

structural architectures.

Given its central role in aircraft design and its substantial contribution to overall aircraft value, the fuselage segment is expected to maintain market leadership throughout the forecast period.

The Composite

Materials Segment Is Expected to Lead the Market by Material

Composite

materials represent the fastest-growing and most influential material segment

within the aerostructures market.

The aerospace

industry's relentless pursuit of fuel efficiency has significantly accelerated

the adoption of lightweight composite structures. Carbon fiber-reinforced

composites offer exceptional strength-to-weight ratios, enabling manufacturers

to reduce aircraft weight without compromising structural integrity.

Unlike

traditional metallic materials, composites provide superior resistance to

corrosion, fatigue, and environmental degradation. This translates into lower

maintenance requirements and longer service life for aircraft operators.

Commercial

aircraft manufacturers increasingly utilize composite materials in wings,

fuselages, empennages, nacelles, and flight control surfaces. Modern aircraft

programs have demonstrated the substantial economic and operational benefits

associated with composite-intensive designs.

The military

sector is also increasing adoption due to the ability of composites to support

advanced performance requirements, including stealth capabilities and enhanced

maneuverability.

As manufacturing

technologies mature and production scalability improves, composite materials

are expected to capture an increasingly larger share of future aerostructure

production.

Commercial

Aircraft Segment Is Expected to Dominate the Market by Platform

Commercial

aircraft account for the largest share of the aerostructures market due to

their high production volumes, large structural content, and extensive global

demand.

The continued

growth of international air travel is creating strong demand for both

narrow-body and wide-body aircraft. Airlines are expanding capacity, opening

new routes, and replacing aging fleets with fuel-efficient aircraft equipped

with advanced structural technologies.

Aircraft

manufacturers maintain substantial order backlogs spanning several years,

providing long-term visibility and demand stability for aerostructure

suppliers.

Additionally,

sustainability initiatives are encouraging the adoption of lighter and more

efficient aircraft platforms, further supporting structural innovation and

market growth.

Emerging markets

across Asia-Pacific, the Middle East, and Africa are expected to contribute

significantly to future commercial aircraft demand, creating additional

opportunities for aerostructure manufacturers.

The combination of rising passenger traffic, fleet modernization initiatives, and increasing aircraft production rates ensures the continued dominance of the commercial aircraft segment.

OEM Segment

Is Expected to Lead the Market by End User

Original

Equipment Manufacturers (OEMs) represent the largest end-user segment within

the aerostructures market.

OEMs are

responsible for integrating structural assemblies into new aircraft production

programs and therefore account for the majority of aerostructure procurement

activities.

Aircraft

manufacturers increasingly collaborate with specialized aerostructure suppliers

to improve production efficiency, reduce development costs, and access advanced

manufacturing capabilities.

The growing

complexity of modern aircraft programs has encouraged greater outsourcing of

structural manufacturing activities, creating substantial opportunities for

tier-one and tier-two suppliers.

Furthermore,

rising aircraft production rates and long-term delivery backlogs continue

supporting strong demand from OEM customers globally.

As aerospace

manufacturing expands and aircraft development programs accelerate, OEM demand

for advanced aerostructures is expected to remain robust throughout the

forecast period.

The following

segments are part of an in-depth analysis of the global Aerostructures market:

|

Market Segments |

|

|

By Component |

∙ Fuselage |

|

By

Material |

∙ Aluminum Alloys |

|

By

Platform |

∙ Commercial Aircraft |

|

By End User |

∙ OEMs |

Aerostructures

Market Share Analysis By Region

North America is

projected to hold the largest share of the global aerostructures market

throughout the forecast period, accounting for approximately 39.4% of global

revenue in 2026.

The region

benefits from the presence of major aircraft manufacturers, advanced aerospace

supply chains, extensive defense spending, and strong investments in aerospace

research and development. The United States remains the dominant market due to

its leadership in commercial aviation, military aerospace programs, and

advanced manufacturing technologies.

Europe

represents the second-largest market, supported by strong aerospace

manufacturing capabilities, advanced engineering expertise, and significant

aircraft production activities. Countries such as France, Germany, the United

Kingdom, and Spain play important roles within the global aerospace ecosystem.

Asia-Pacific is

expected to register the fastest growth throughout the forecast period. Rising

passenger traffic, increasing aircraft procurement, growing domestic aerospace

industries, and expanding defense budgets are driving regional demand.

China and India

are emerging as major aerospace growth centers due to expanding aviation

infrastructure, increasing air travel demand, and government support for

indigenous aerospace manufacturing capabilities.

The Middle East

continues investing heavily in commercial aviation expansion, while Latin

America is experiencing gradual growth supported by regional fleet

modernization initiatives.

As global aviation demand continues to increase, regional investments in aerospace manufacturing and aircraft procurement are expected to drive sustained market expansion.

Aerostructures

Market Competition Landscape Analysis

The

aerostructures market is characterized by intense competition, technological

innovation, and extensive collaboration between aircraft manufacturers and

component suppliers.

Leading

companies are investing heavily in advanced composites, automated manufacturing

systems, additive manufacturing technologies, digital engineering solutions,

and sustainable production processes.

Manufacturers

are focusing on improving production efficiency, reducing structural weight,

enhancing product quality, and supporting next-generation aircraft development

programs.

Strategic

partnerships, mergers, acquisitions, and long-term supply agreements continue

shaping the competitive landscape as companies seek to strengthen technological

capabilities and global market presence.

The increasing complexity of aircraft programs and growing demand for lightweight structures are expected to further intensify competition and innovation throughout the forecast period.

Global

Aerostructures Market Recent Developments News:

∙ In April 2026,

major aerospace manufacturers expanded investments in advanced composite

aerostructure production facilities.

∙ In February

2026, aircraft suppliers introduced automated robotic assembly systems to

improve structural manufacturing efficiency.

∙ In November

2025, several commercial aircraft programs increased production targets to

address growing airline order backlogs.

∙ In August

2025, aerospace companies accelerated the development of lightweight structural

technologies for sustainable aviation applications.

∙ In June 2025, multiple defense modernization initiatives generated increased demand for advanced military aircraft structures.

The Global

Aerostructures Market is Dominated by a Few Large Companies, Such As

∙ Spirit AeroSystems Holdings, Inc.

∙ Leonardo S.p.A.

∙ Airbus Atlantic

∙ Triumph Group, Inc.

∙ GKN Aerospace

∙ Safran S.A.

∙ Collins Aerospace

∙ ST Engineering Aerospace

∙ Korean Aerospace Industries Ltd.

∙ Mitsubishi Heavy Industries, Ltd.

∙ Kawasaki Heavy Industries, Ltd.

∙ Daher Group

∙ Saab AB

∙ FACC AG

∙ Premium AEROTEC GmbH

∙ Others

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Aerostructures Market

Introduction and Market Overview

1.1. Objectives of the Study

1.2. Global Aerostructures Market Scope

and Market Estimation

1.2.1. Global Aerostructures Overall Market

Size (US$ Million), Market CAGR (%), Market Forecast (2026 - 2034)

1.2.2. Global Aerostructures Market Revenue

Share (%) and Growth Rate (Y-o-Y) from 2021 - 2034

1.3. Market Segmentation

1.3.1. Component of Global Aerostructures

Market

1.3.2. Material of Global Aerostructures

Market

1.3.3. Platform of Global Aerostructures

Market

1.3.4. End User of Global Aerostructures

Market

1.3.5. Region of Global Aerostructures

Market

2. Executive Summary

2.1. Demand Side Trends

2.2. Key Market Trends

2.3. Market Demand (US$ Million) Analysis

2021 – 2025 and Forecast, 2026 – 2034

2.4. Demand and Opportunity Assessment

2.5. Key Developments

2.6. Overview of Tariff, Regulatory

Landscape and Standards

2.7. Market Entry Strategies

2.8. Market Dynamics

2.8.1. Drivers

2.8.2. Limitations

2.8.3. Opportunities

2.8.4. Impact Analysis of Drivers and

Restraints

2.9. Porter’s Five Forces Analysis

2.10.

PEST

Analysis

3. Global Aerostructures Market

Estimates & Historical Trend Analysis (2021 - 2025)

4. Global Aerostructures Market

Estimates & Forecast Trend Analysis, by Component

4.1. Global Aerostructures Market Revenue

(US$ Million) Estimates and Forecasts, by Component, 2021 - 2034

4.1.1. Fuselage

4.1.2. Wings

4.1.3. Empennage

4.1.4. Nacelles & Pylons

4.1.5. Flight Control Surfaces

4.1.6. Doors & Interiors

4.1.7. Others

5. Global Aerostructures Market

Estimates & Forecast Trend Analysis, by Material

5.1. Global Aerostructures Market Revenue

(US$ Million) Estimates and Forecasts, by Material, 2021 - 2034

5.1.1. Aluminum Alloys

5.1.2. Titanium Alloys

5.1.3. Composite Materials

5.1.4. Steel Alloys

5.1.5. Others

6. Global Aerostructures Market

Estimates & Forecast Trend Analysis, by Platform

6.1. Global Aerostructures Market Revenue

(US$ Million) Estimates and Forecasts, by Platform, 2021 - 2034

6.1.1. Commercial Aircraft

6.1.2. Military Aircraft

6.1.3. Business Jets

6.1.4. Helicopters

6.1.5. Unmanned Aerial Vehicles

6.1.6. Urban Air Mobility Aircraft

7. Global Aerostructures Market

Estimates & Forecast Trend Analysis, by End User

7.1. Global Aerostructures Market Revenue

(US$ Million) Estimates and Forecasts, by End User, 2021 - 2034

7.1.1. OEMs

7.1.2. MRO Providers

7.1.3. Defense Organizations

7.1.4. Aircraft Leasing Companies

8. Global Aerostructures Market

Estimates & Forecast Trend Analysis, by Region

8.1. Global Aerostructures Market Revenue

(US$ Million) Estimates and Forecasts, by Region, 2021 - 2034

8.1.1. North America

8.1.2. Europe

8.1.3. Asia Pacific

8.1.4. Middle East & Africa

8.1.5. Latin America

9. North America Aerostructures Market:

Estimates & Forecast Trend Analysis

9.1. North America Aerostructures Market

Assessments & Key Findings

9.1.1. North America Aerostructures Market

Introduction

9.1.2. North America Aerostructures Market

Size Estimates and Forecast (US$ Million) (2021 - 2034)

9.1.2.1.

By

Component

9.1.2.2.

By

Material

9.1.2.3.

By

Platform

9.1.2.4.

By

End User

9.1.2.5.

By

Country

9.1.2.5.1.

The

U.S.

9.1.2.5.2.

Canada

10. Europe Aerostructures Market:

Estimates & Forecast Trend Analysis

10.1.

Europe

Aerostructures Market Assessments & Key Findings

10.1.1. Europe Aerostructures Market

Introduction

10.1.2. Europe Aerostructures Market Size

Estimates and Forecast (US$ Million) (2021 - 2034)

10.1.2.1.

By

Component

10.1.2.2.

By

Material

10.1.2.3.

By

Platform

10.1.2.4.

By

End User

10.1.2.5.

By

Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7.

Rest

of Europe

11. Asia Pacific Aerostructures Market:

Estimates & Forecast Trend Analysis

11.1.

Asia

Pacific Market Assessments & Key Findings

11.1.1. Asia Pacific Aerostructures Market

Introduction

11.1.2. Asia Pacific Aerostructures Market

Size Estimates and Forecast (US$ Million) (2021 - 2034)

11.1.2.1.

By

Component

11.1.2.2.

By

Material

11.1.2.3.

By

Platform

11.1.2.4.

By

End User

11.1.2.5.

By

Country

11.1.2.5.1.

China

11.1.2.5.2.

Japan

11.1.2.5.3.

India

11.1.2.5.4.

Australia

11.1.2.5.5.

South

Korea

11.1.2.5.6.

Rest

of Asia Pacific

12. Middle East & Africa

Aerostructures Market: Estimates & Forecast Trend Analysis

12.1.

Middle

East & Africa Market Assessments & Key Findings

12.1.1. Middle East & Africa

Aerostructures Market Introduction

12.1.2. Middle East & Africa

Aerostructures Market Size Estimates and Forecast (US$ Million) (2021 - 2034)

12.1.2.1.

By

Component

12.1.2.2.

By

Material

12.1.2.3.

By

Platform

12.1.2.4.

By

End User

12.1.2.5.

By

Country

12.1.2.5.1.

UAE

12.1.2.5.2.

Saudi

Arabia

12.1.2.5.3.

South

Africa

12.1.2.5.4.

Rest

of MEA

13. Latin America Aerostructures Market:

Estimates & Forecast Trend Analysis

13.1.

Latin

America Market Assessments & Key Findings

13.1.1. Latin America Aerostructures Market Introduction

13.1.2. Latin America Aerostructures Market

Size Estimates and Forecast (US$ Million) (2021 - 2034)

13.1.2.1.

By

Component

13.1.2.2.

By

Material

13.1.2.3.

By

Platform

13.1.2.4.

By

End User

13.1.2.5.

By

Country

13.1.2.5.1.

Brazil

13.1.2.5.2.

Mexico

13.1.2.5.3.

Argentina

13.1.2.5.4.

Rest

of LATAM

14. Competition Landscape

14.1.

Global

Aerostructures Market Product Mapping

14.2.

Global

Aerostructures Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3.

Global

Aerostructures Market Tier Structure Analysis

14.4.

Global

Aerostructures Market Concentration & Company Market Shares (%) Analysis,

2025

15. Company Profiles

15.1.

Spirit

AeroSystems Holdings, Inc.

15.1.1. Company Overview & Key Stats

15.1.2. Financial Performance & KPIs

15.1.3. Product Portfolio

15.1.4. SWOT Analysis

15.1.5. Business Strategy & Recent

Developments

*Similar details would be provided for all the players

mentioned below

15.2.

Leonardo

S.p.A.

15.3.

Airbus

Atlantic

15.4.

Triumph

Group, Inc.

15.5.

GKN

Aerospace

15.6.

Safran

S.A.

15.7.

Collins

Aerospace

15.8.

ST

Engineering Aerospace

15.9.

Korean

Aerospace Industries Ltd.

15.10.

Mitsubishi

Heavy Industries, Ltd.

15.11.

Kawasaki

Heavy Industries, Ltd.

15.12.

Daher

Group

15.13.

Saab

AB

15.14.

FACC

AG

15.15.

Premium

AEROTEC GmbH

15.16.

Others

16. Research Findings & Conclusion

17. Assumption & Acronyms Used

18. Research Methodology

18.1.

External

Databases

18.2.

Internal

Proprietary Database

18.3.

Primary

Research

18.4.

Secondary

Research

18.5.

Assumptions

18.6.

Limitations

18.7.

Report

FAQs

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables