Agricultural Adjuvants Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Type (Activator Adjuvants, Utility Adjuvants), By Application (Herbicides, Insecticides, Fungicides, Others), By Crop (Cereals, Oilseeds, Fruits & Vegetables, Other Crops), and Geography

2026-01-02

Agriculture Industry

Jaya Bundele (Research Analyst)

Description

Agricultural

Adjuvants Market Overview

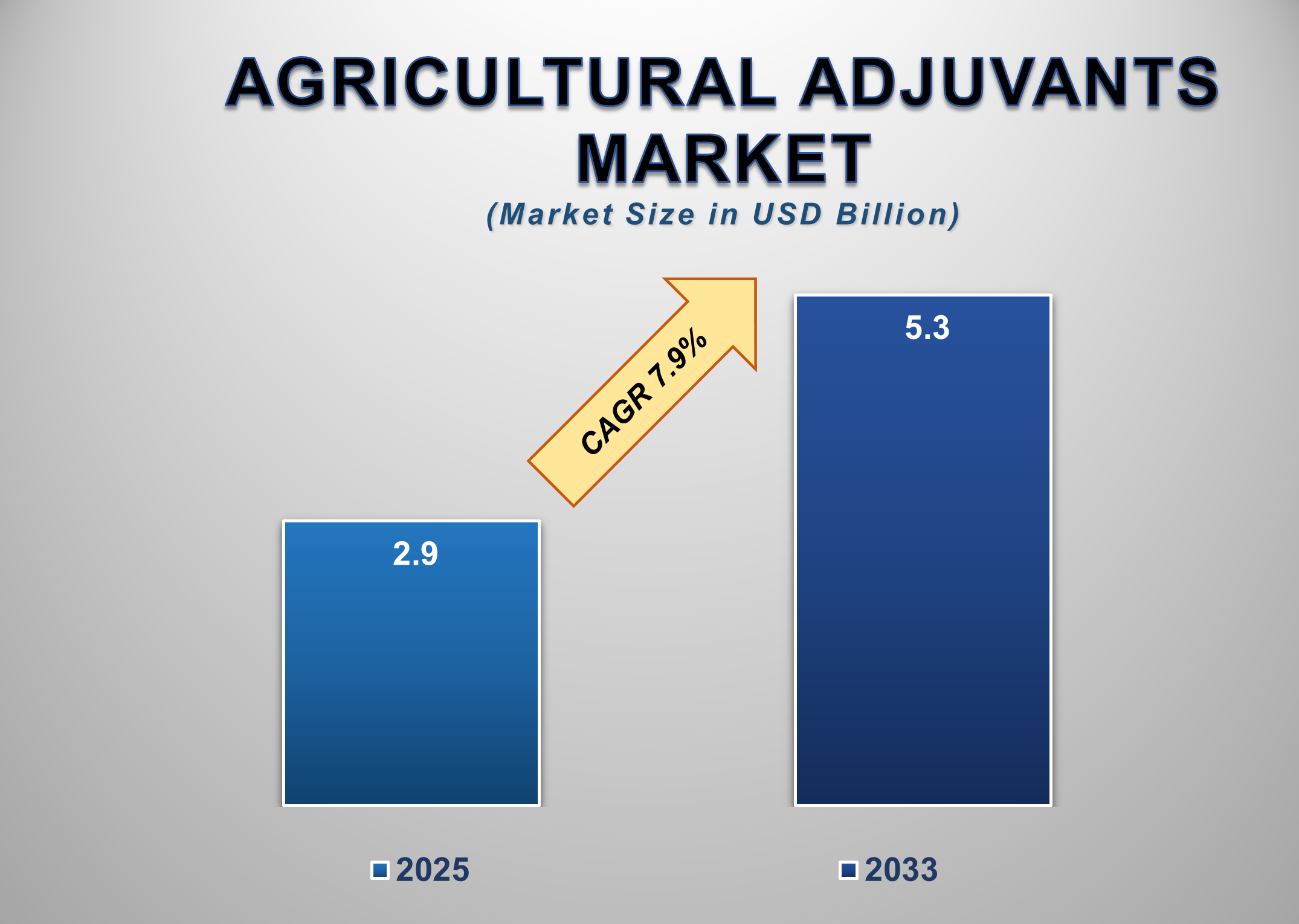

The global Agricultural Adjuvants Market is gaining significant momentum as modern farming practices place greater emphasis on crop protection efficiency, superior product performance, and precision agriculture. Estimated at USD 2.9 billion in 2025, the market is projected to reach USD 5.3 billion by 2033, expanding at a robust CAGR of 7.9%. Agricultural adjuvant substances added to pesticides, herbicides, fungicides, or other crop protection formulations play a critical role in enhancing spray effectiveness, improving chemical stability, boosting adhesion, and ensuring better penetration into plant tissues. Their rising adoption aligns with global pressure to increase crop yields while minimizing agrochemical usage and environmental impact. As farmers transition toward data-driven and sustainable farming practices, the need to optimize every spray application is fueling widespread usage of adjuvants across all major crop categories.

Rapid industrialization of

agriculture, especially in emerging economies, is creating strong demand for

efficient agrochemical formulations capable of delivering high performance

under diverse climatic and soil conditions. Adjuvants are increasingly seen not

just as product enhancers but as essential complements to crop protection

solutions in precision farming, enabling better droplet formation, reduced

spray drift, and maximized bioavailability. Markets in Asia-Pacific, Latin

America, and North America are experiencing significant growth due to

large-scale farming operations, rising pest resistance, and expanded

application of advanced chemistries.

Rapid industrialization of

agriculture, especially in emerging economies, is creating strong demand for

efficient agrochemical formulations capable of delivering high performance

under diverse climatic and soil conditions. Adjuvants are increasingly seen not

just as product enhancers but as essential complements to crop protection

solutions in precision farming, enabling better droplet formation, reduced

spray drift, and maximized bioavailability. Markets in Asia-Pacific, Latin

America, and North America are experiencing significant growth due to

large-scale farming operations, rising pest resistance, and expanded

application of advanced chemistries.

Agricultural Adjuvants Market Drivers and

Opportunities

Rising Use of Herbicides

and Improved Formulation Efficiency Is Driving the Agricultural Adjuvants

Market Growth

The growing reliance on

herbicides across global agricultural systems is a central force driving the

Agricultural Adjuvants Market. Herbicides remain essential for weed control,

which has become increasingly challenging due to climate change, expanded cropping

intensity, and rising herbicide-resistant weed populations. As new resistant

strains continue to emerge, farmers are under pressure to maximize the

efficiency of every herbicide application. Adjuvants significantly improve

spray uniformity, leaf surface coverage, and penetration, enabling optimal

herbicide efficacy even in complex environments. Because herbicides represent

the highest share of crop protection chemicals globally, the increased need for

supporting technologies to enhance their performance directly strengthens

demand for adjuvants. At the same time, agrochemical manufacturers are

reformulating products to comply with stricter environmental and safety

regulations. Many modern chemistries require adjuvants for effective

dispersion, solubilization, and surfactant action. This has accelerated the

adoption of activator adjuvants, multifunctional surfactants, and advanced

penetration enhancers. Moreover, the rapid expansion of precision agriculture,

such as GPS-guided spraying, controlled droplet application, and variable-rate

technology, further amplifies the need for adjuvants that ensure stable spray

patterns and reliability under varying droplet sizes. Together, these factors

are reshaping crop protection strategies, making adjuvants indispensable for

achieving consistent, high-yield outcomes across large-scale cropping systems

worldwide.

Growing Adoption of

Cereals and Oilseed Farming Is Fueling Large-Scale Demand for Agricultural

Adjuvants Worldwide

The increasing global demand for

cereals such as wheat, rice, corn, and barley is creating strong momentum for

adjuvant adoption. Cereals remain the most widely cultivated crops across the

world, driven by population growth, industrial food processing needs, livestock

feed production, and rising consumption in developing regions. Large-scale

cereal farming involves extensive use of agrochemicals to mitigate pests,

diseases, and weeds that can drastically reduce yields. Adjuvants play a vital

role in ensuring that these crop protection inputs perform consistently, even

under challenging environmental conditions such as high temperatures, heavy

rainfall, or dry climates. High-volume cereal production operations, especially

in Asia-Pacific, Europe, and North America, depend heavily on effective spray

applications, making adjuvants essential for enhancing herbicide, fungicide,

and insecticide efficiency.

Additionally, the expansion of

oilseed crops such as soybean, canola, and sunflower is further boosting the

market. These crops require targeted protection against fungal pathogens and

insect infestations that can significantly affect oil extraction quality and

yields. Adjuvants ensure better droplet adhesion and cuticular penetration,

particularly important for oilseeds where waxy leaf surfaces hinder pesticide

absorption. As global food security initiatives focus on improving per-acre

productivity, and as farming in developing regions transitions to more

mechanized and chemical-intensive systems, the demand for agricultural

adjuvants continues to rise sharply. This increasing crop dependency

underscores the essential nature of adjuvants as part of modern agricultural

input portfolios.

Growing Focus on

Sustainable and Bio-Based Crop Protection Solutions Is Creating Significant

Opportunities in the Agricultural Adjuvants Market Worldwide

The global transition toward

environmentally sustainable agriculture is opening new growth avenues for the

Agricultural Adjuvants Market. Governments and regulatory bodies across regions

are implementing stricter measures to reduce pesticide residues, minimize

environmental contamination, and encourage biodegradable crop inputs. This

regulatory shift is compelling manufacturers to develop bio-based,

low-toxicity, and eco-friendly adjuvant formulations derived from natural oils,

plant extracts, and renewable surfactants. Bio-based adjuvants not only reduce

the environmental footprint but also improve compatibility with organic and

reduced-chemical farming systems segments which are expanding rapidly

worldwide. Farmers are increasingly adopting these solutions to meet

certification standards and consumer demand for cleaner, residue-free food

products. Furthermore, the rise of regenerative agriculture, sustainable

intensification, and carbon-smart farming is creating long-term structural

demand for adjuvants that enhance application precision and reduce chemical

wastage. Many farmers are turning to adjuvants that allow lower chemical

dosages without compromising efficacy, helping them comply with evolving

environmental guidelines. Technological advancements such as nano-emulsion

adjuvants, biodegradable surfactants, and multifunctional additives are giving

manufacturers new opportunities to differentiate their products. As

sustainability continues to guide global agricultural policies and consumer

preferences, bio-based and advanced adjuvants are positioned to become a major

growth engine for the market throughout the forecast period.

Agricultural Adjuvants

Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 2.9 Billion |

|

Market Forecast in 2033 |

USD 5.3 Billion |

|

CAGR % 2025-2033 |

7.9% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, Company

Share, Company Heatmap, Company Production Capacity, Growth Factors and more |

|

Segments Covered |

●

By Type, By

Application, By Crop |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Agricultural Adjuvants

Market Report Segmentation Analysis

The global Agricultural Adjuvants

market is segmented by Type, by Application, by Crop, and by Geography.

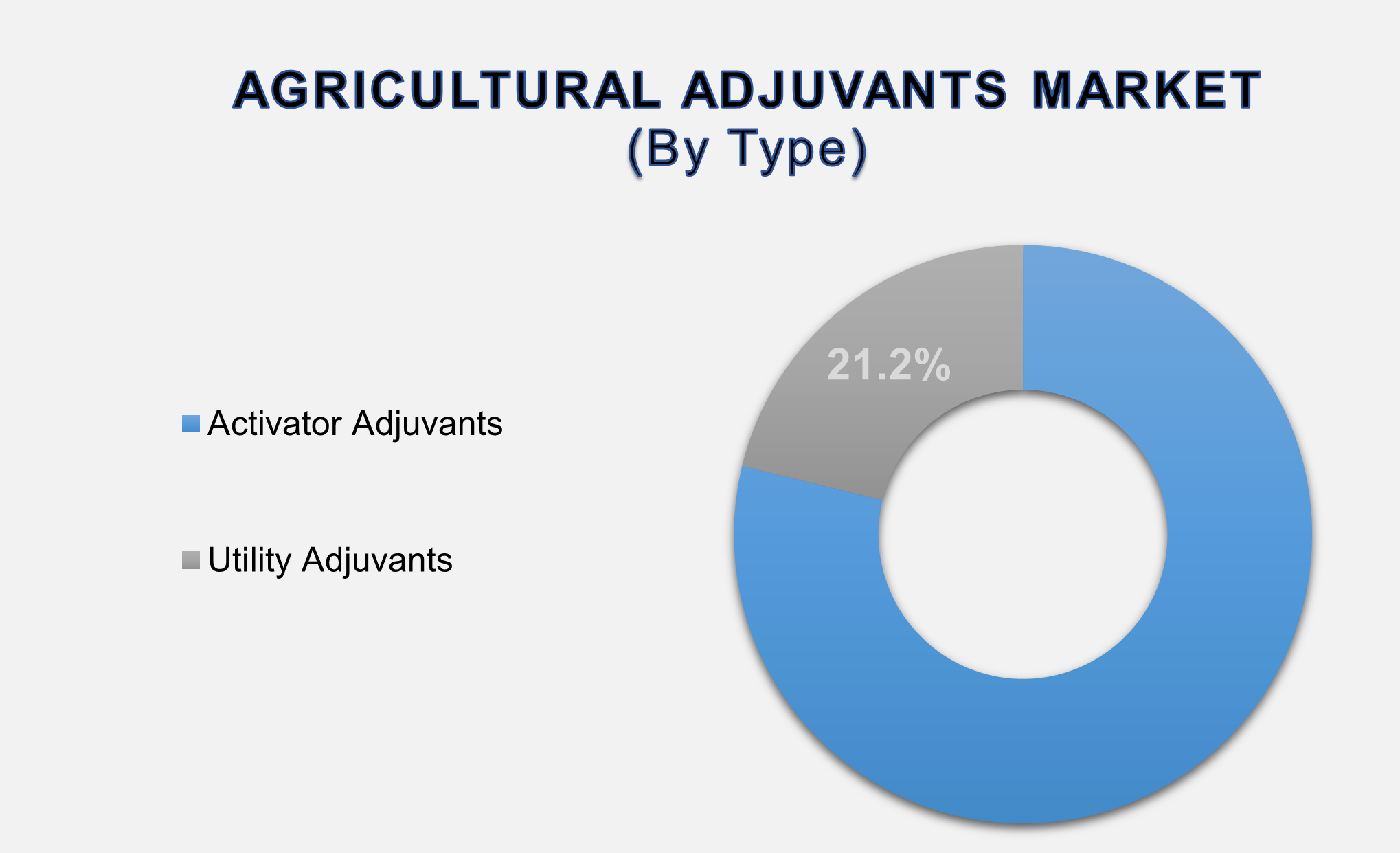

Activator Adjuvants

Segment Accounted for the Largest Market Share in the Global Agricultural

Adjuvants Market

The Activator Adjuvants segment dominates the market with a 78.8% share, underscoring their essential role in improving agrochemical performance across multiple crop types. These adjuvants include surfactants, wetting agents, spreaders, and penetrants designed to enhance the absorption of herbicides, insecticides, and fungicides. Their widespread adoption is driven by the increasing use of systemic pesticides that require effective penetration into plant tissues for optimal functionality. Farmers prefer activator adjuvants because they improve droplet retention, reduce surface tension, and enhance product distribution across leaves and stems. Additionally, they allow for better performance under challenging field conditions such as high humidity, extreme temperatures, and variable spray pressures. The growing prevalence of herbicide-resistant weeds and the expansion of high-value crops globally are further boosting demand for activator adjuvants. Newer pesticide formulations are also increasingly dependent on these additives to achieve desired efficacy, making activator adjuvants indispensable for modern agriculture. Precision agriculture technologies such as automated spraying systems, controlled droplet applications, and drone-assisted spraying also rely heavily on activator adjuvants to maintain uniform spray patterns and absorption.

Herbicides Segment Accounted for the Largest Market Share in the Global Agricultural Adjuvants Market by Application

The Herbicides segment holds the

largest share in the Application category, reflecting the growing need for

effective weed control to maintain high crop productivity. Herbicides account

for the majority of all crop protection chemicals used globally, and their

performance is heavily influenced by the use of adjuvants. Agricultural

adjuvants improve herbicide uptake by enabling superior spray coverage, reducing

droplet bounce, and enhancing penetration into tough weed cuticles. These

performance improvements are particularly critical for managing resistant weed

species, which have become increasingly widespread due to excessive use of

similar modes of action over time. Farmers cultivating large-scale cereal,

oilseed, and fiber crops rely extensively on herbicides to maintain clean

fields and maximize yields. Adjuvants ensure that herbicides remain effective

even under adverse environmental conditions such as wind drift, high

temperatures, and inconsistent moisture levels.

The Cereals Segment

Accounted for the Largest Market Share in the Global Agricultural Adjuvants

Market by Crop Type

The Cereals segment, comprising

crops such as wheat, rice, maize, and barley, commands the largest share in the

Crop category. Cereals form the backbone of global food supply, animal feed

industries, and industrial applications, making efficient crop protection

essential for sustaining global food security. The high pest and disease

pressure associated with cereal farming drives strong adoption of adjuvants to

enhance pesticide performance. Adjuvants help improve spray adherence,

retention, and penetration on cereal leaves, which often have waxy surfaces

that reduce chemical absorption. As large-acreage cereal farming expands across

Asia-Pacific, North America, and Europe, the demand for adjuvants will continue

to scale proportionally. Environmental challenges such as unpredictable

rainfall patterns, soil degradation, and rising temperatures underscore the

need for reliable crop protection methods. Adjuvants support improved spray

outcomes under such conditions, ensuring reduced pesticide wastage and enhanced

effectiveness.

The following segments are

part of an in-depth analysis of the global Agricultural Adjuvants Market:

|

Market

Segments |

|

|

By Type |

●

Activator Adjuvants ●

Utility Adjuvants |

|

By Material |

●

Herbicides ●

Insecticides ●

Fungicides ●

Others |

|

By

Distribution Channel |

●

Cereals ●

Oilseeds ●

Fruits &

Vegetables ●

Other Crops |

Agricultural Adjuvants Market Share Analysis by

Region

The Asia Pacific region

is projected to hold the largest share of the global Agricultural Adjuvants

Market over the forecast period.

Asia-Pacific accounted for the

largest share of the Agricultural Adjuvants Market at 46.7%, supported by its

massive agricultural base, extensive cereal crop cultivation, and increasing

adoption of modern farming technologies. Countries such as India, China,

Indonesia, and Vietnam are experiencing rapid transitions toward mechanized and

chemical-intensive farming practices, creating strong demand for adjuvants that

enhance spray efficiency. Favorable government policies promoting improved crop

productivity and reduced chemical usage also encourage farmers to adopt

advanced adjuvant formulations. The region’s high population density and

growing food security pressures further accelerate the need for optimized crop

protection inputs.

North America is expected to

exhibit the highest CAGR during the forecast period, driven by technological

advancements, precision agriculture adoption, and strong penetration of

specialty adjuvants. The region benefits from well-established agricultural infrastructure,

advanced R&D capabilities, and widespread use of herbicides, fungicides,

and insecticides in large-scale commercial farming. Europe also represents a

significant market with strong regulatory support for sustainable agriculture,

driving demand for bio-based and environmentally friendly adjuvants. Meanwhile,

Latin America, especially Brazil and Argentina, is experiencing rising demand

for utility and activator adjuvants due to the rapid expansion of soybean,

corn, and sugarcane cultivation. Together, these regional dynamics position the

Agricultural Adjuvants Market for continued global expansion through 2033.

Agricultural Adjuvants Market Competition

Landscape Analysis

The

Agricultural Adjuvants Market is moderately consolidated, with leading players

such as BASF, Dow Chemical, Solvay, Evonik, Croda, Clariant, and Huntsman

shaping the competitive environment. These companies invest heavily in product

innovation, particularly bio-based and multifunctional adjuvant formulations

that comply with evolving environmental regulations.

Global Agricultural Adjuvants Market Recent

Developments News:

- In April 2022,

Lamberti SPA acquired Turftech International, a UK-based producer of

specialty surfactants for horticulture and turf management. The

acquisition strengthens Lamberti’s product portfolio and expands its

regional market presence in Europe.

- In June 2021,

Evonik and Tropfen commercialized BREAK-THRU MSO MAX adjuvants in

Argentina. This partnership supports the needs of South American growers

by providing advanced agricultural solutions designed to improve

application efficiency and crop performance.

The Global Agricultural Adjuvants Market is

dominated by a few large companies, such as

●

BASF

●

Dow Chemical Company

●

Evonik Industries

●

Solvay

●

Clariant

●

Croda International

●

Huntsman Corporation

●

Helena

Agri-Enterprises

●

WinField United

●

Nufarm

●

Brandt Consolidated

●

Loveland Products

●

Wilbur-Ellis

●

Precision Laboratories

●

Innvictis Crop Care

●

Kalo

●

SinoHarvest

●

Adjuvant Plus

●

Tanchem

●

GarrCo Products

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Agricultural

Adjuvants Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Agricultural Adjuvants Market Scope and Market Estimation

1.2.1.Global Agricultural

Adjuvants Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast

(2025 - 2033)

1.2.2.Global Agricultural

Adjuvants Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Type of Global Agricultural

Adjuvants Market

1.3.2.Application of Global Agricultural

Adjuvants Market

1.3.3.Crop of Global Agricultural

Adjuvants Market

1.3.4.Region of Global Agricultural

Adjuvants Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Agricultural Adjuvants Market

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

2.10.

Key

Regulation

3. Global

Agricultural Adjuvants Market Estimates

& Historical Trend Analysis (2020 - 2024)

4.

Global Agricultural

Adjuvants Market Estimates

& Forecast Trend Analysis, by Type

4.1.

Global

Agricultural Adjuvants Market Revenue (US$ Bn) Estimates and Forecasts, by Type,

2020 - 2033

4.1.1.Activator Adjuvants

4.1.2.Utility Adjuvants

5.

Global Agricultural

Adjuvants Market Estimates

& Forecast Trend Analysis, by Application

5.1.

Global

Agricultural Adjuvants Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

5.1.1.Herbicides

5.1.2.Insecticides

5.1.3.Fungicides

5.1.4.Others

6.

Global Agricultural

Adjuvants Market Estimates

& Forecast Trend Analysis, by Crop

6.1.

Global

Agricultural Adjuvants Market Revenue (US$ Bn) Estimates and Forecasts, by Crop,

2020 - 2033

6.1.1.Cereals

6.1.2.Oilseeds

6.1.3.Fruits & Vegetables

6.1.4.Other Crops

7. Global

Agricultural Adjuvants Market Estimates

& Forecast Trend Analysis, by region

1.1.

Global

Agricultural Adjuvants Market Revenue (US$ Bn) Estimates and Forecasts, by

region, 2020 - 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East & Africa

1.1.5.Latin America

8. North America Agricultural

Adjuvants Market: Estimates &

Forecast Trend Analysis

8.1.

North

America Agricultural Adjuvants Market Assessments & Key Findings

8.1.1.North America Agricultural

Adjuvants Market Introduction

8.1.2.North America Agricultural

Adjuvants Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Type

8.1.2.2. By Application

8.1.2.3. By Crop

8.1.2.4.

By

Country

8.1.2.4.1.

The

U.S.

8.1.2.4.2.

Canada

9. Europe Agricultural

Adjuvants Market: Estimates &

Forecast Trend Analysis

9.1.

Europe

Agricultural Adjuvants Market Assessments & Key Findings

9.1.1.Europe Agricultural

Adjuvants Market Introduction

9.1.2.Europe Agricultural

Adjuvants Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Type

9.1.2.2. By Application

9.1.2.3. By Crop

9.1.2.4.

By

Country

9.1.2.4.1. Germany

9.1.2.4.2. Italy

9.1.2.4.3. U.K.

9.1.2.4.4. France

9.1.2.4.5. Spain

9.1.2.4.6. Switzerland

9.1.2.4.7.

Rest of Europe

10. Asia Pacific Agricultural

Adjuvants Market: Estimates &

Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Agricultural Adjuvants Market Introduction

10.1.2.

Asia

Pacific Agricultural Adjuvants Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1. By Type

10.1.2.2. By Application

10.1.2.3. By Crop

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6.

Rest

of Asia Pacific

11. Middle East & Africa Agricultural

Adjuvants Market: Estimates &

Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Agricultural Adjuvants Market

Introduction

11.1.2.

Middle East & Africa Agricultural Adjuvants Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Type

11.1.2.2. By Application

11.1.2.3. By Crop

11.1.2.4.

By

Country

11.1.2.4.1. South

Africa

11.1.2.4.2. UAE

11.1.2.4.3. Saudi

Arabia

11.1.2.4.4.

Rest of MEA

12. Latin America

Agricultural Adjuvants Market:

Estimates & Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Agricultural Adjuvants Market Introduction

12.1.2.

Latin

America Agricultural Adjuvants Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

12.1.2.1. By Type

12.1.2.2. By Application

12.1.2.3. By Crop

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Mexico

12.1.2.4.3. Argentina

12.1.2.4.4.

Rest of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Agricultural Adjuvants Market Product Mapping

14.2.

Global

Agricultural Adjuvants Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3.

Global

Agricultural Adjuvants Market Tier Structure Analysis

14.4.

Global

Agricultural Adjuvants Market Concentration & Company Market Shares (%)

Analysis, 2023

15.

Company

Profiles

15.1. BASF

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all

the players mentioned below

15.2. Dow Chemical

Company

15.3. Evonik

Industries

15.4. Solvay

15.5. Clariant

15.6. Croda

International

15.7. Huntsman

Corporation

15.8. Helena

Agri-Enterprises

15.9. WinField

United

15.10. Nufarm

15.11. Brandt

Consolidated

15.12. Loveland

Products

15.13. Wilbur-Ellis

15.14. Precision

Laboratories

15.15. Innvictis

Crop Care

15.16. Kalo

15.17. SinoHarvest

15.18. Adjuvant Plus

15.19. Tanchem

15.20. GarrCo

Products

15.21. Other

Prominent Players

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables