Agricultural Biologicals Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Product Type (Biopesticides, Biofertilizers, Biostimulants) By Mode of Application (Soil Treatment, Seed Treatment, Foliar Spray), By Application (Cereals & Grains, Oilseed & Pulses, Fruits & Vegetables, Others) and Geography

2025-10-30

Agriculture Industry

Jaya Bundele (Research Analyst)

Description

Agricultural Biologicals Market Overview

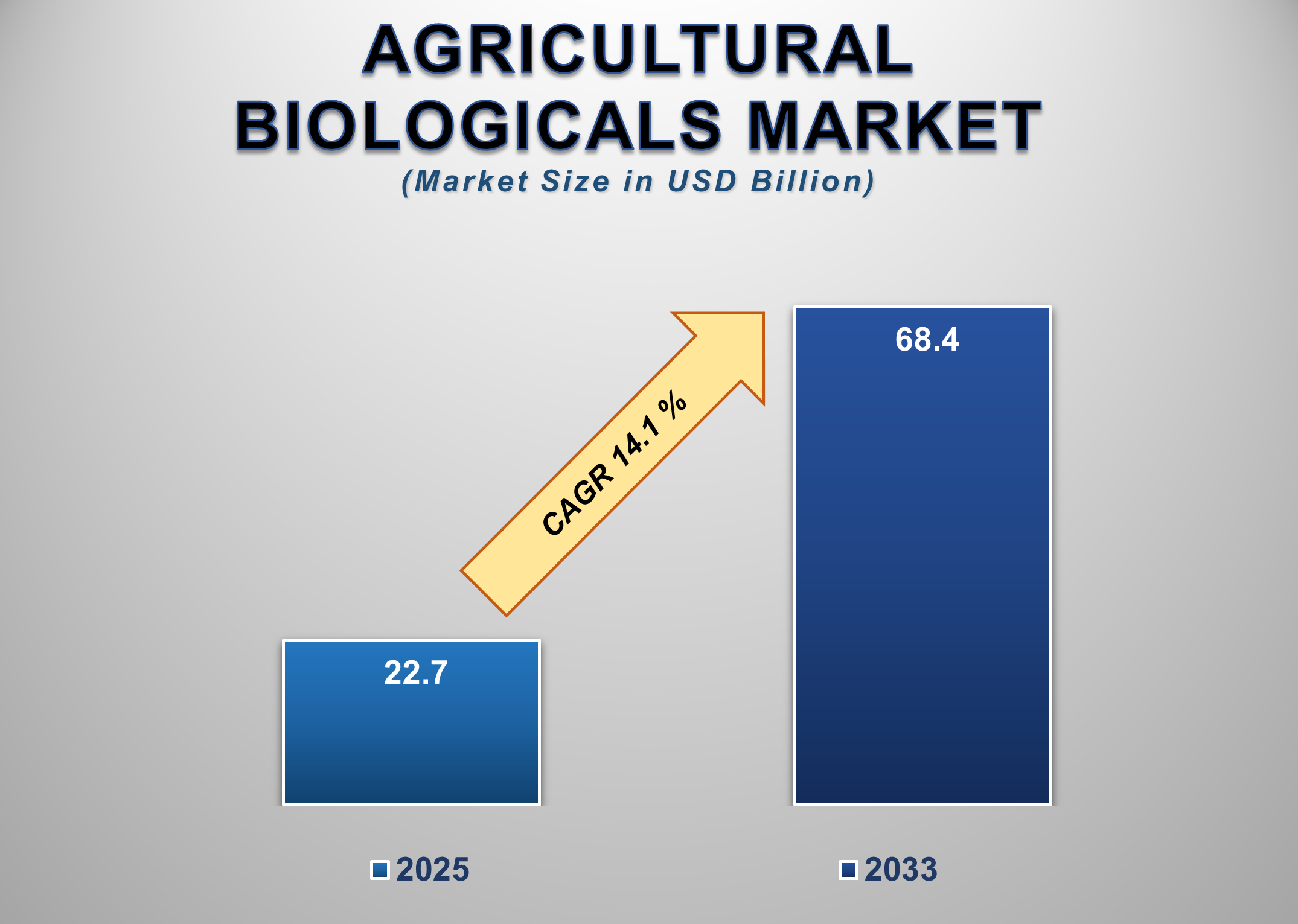

The global Agricultural Biologicals Market is projected to grow from USD 22.7 billion in 2025 to USD 68.4 billion by 2033, registering a robust CAGR of 14.1% during the forecast period. Growth in this market is largely driven by the increasing demand for sustainable and environmentally friendly agricultural solutions, as farmers and policymakers alike shift toward reducing chemical dependency in food production.

Agricultural biologicals, including biopesticides, biofertilizers, and biostimulants, are derived from natural sources such as beneficial insects, microorganisms, and plant extracts. These products are gaining rapid acceptance as effective alternatives to synthetic chemicals, aligning with the rising adoption of organic farming practices and the global movement toward sustainable crop protection and soil management. Regulatory authorities worldwide are also imposing stringent restrictions on chemical pesticide use, further accelerating demand for biological inputs. At the same time, consumer preference for organic and residue-free food products is fueling strong adoption across both developed and emerging economies.

Agricultural

Biologicals Market Drivers and Opportunities

Rising Incidences Of Pest Resistance To Chemical Crop

Protection Are Anticipated To Lift The Agricultural Biologicals Market During

The Forecast Period

The significant driver of the

market in agricultural biologicals is the growing incidence of resistance of

pests to chemical pesticides. Inappropriate use and overuse of chemical

pesticides have triggered the evolution of resistant pest populations,

degrading the effectiveness of conventional crop protectants. This has

compelled the industry to look towards innovative and integrated pest

management techniques, where the role of farming biologicals becomes pivotal.

Biopesticides from natural organisms exhibit a unique mode of action that can

safely target resistant pest strains. Biologicals also pose less risk to target

species and the environment, and fit well with IPM schemes. Farmers see the

long-term ecological and financial benefits of converting to biological

alternatives and supplementing with them. Agrochemical firms also remain

heavily committed to R&D and acquisitions to increase biological product

offerings in their pipelines, which indicates market optimism and growth

prospects in the future. As word spreads and regulation compels less chemical

use, the use of biologicals is projected to increase gradually. This is not

only combating current crop protectant issues but also creating a more robust

and diverse farming practice.

Favorable Regulatory Environment And Government Initiatives

Is A Vital Driver For Influencing The Growth Of The Global Agricultural

Biologicals Market

Supportive policies and

proactive government measures have been instrumental in increasing the size and

growth of the agricultural biological market. Governments across the globe are

accepting the merits of biologicals in resolving food security, sustainability

of the environment, and rural growth. Organic farming subsidies, public-private

collaborations in research on biologicals, and efficient approval protocols for

biological products are being increasingly observed. For example, the European

Union's Farm to Fork and Green Deal strategy emphasizes aggressively curbing

chemical pesticide use, thereby providing significant growth opportunities to

biological solutions. Emerging economies in countries such as India, Brazil,

and China, too, are embracing biological products in the national agriculture

plans to enhance productivity and health of the land and minimize input costs.

These are complemented by international agencies such as FAO and UNEP in

propagating biologicals in agriculture to promote sustainability. These

regulatory authorities, too, are revising product registration protocols to

include the distinctive properties of biologicals, which vary from conventional

agrochemicals largely in their risk profile owing to their biological origin

and complex interactions with the plant and pest organisms. This regulatory

readiness has promoted innovation and market entry of fresh players and

increased product diversity in the market. Such government support and

favorable policies during the past few years are expected to be instrumental in

scaling up the use of agricultural biologicals in developed and developing

regions.

Technological Advancements In Biological R&D and

Formulation Are Poised to Create Significant Opportunities In The Global

Agricultural Biologicals Market

Development of next-generation

biological products through technological innovation is a significant

opportunity in the market for agricultural biologicals. Improvements in

microbiology, genomics, fermentation technology, and methods of precise

application are making it possible to deliver more potent, stable, and targeted

biologicals. In contrast to previous generations of biologicals that had

limitations of shelf life and effectiveness in extreme weather conditions,

current formulations are much more resistant and reliable in performance. Firms

are investing more in R&D to create tailored bio-based products that tackle

particular crops, climates, and pest pressure. Digital agriculture solutions

such as AI-based diagnostic tools, IoT sensors, and remote monitoring platforms

are also being infused to enhance the timing and application of biologicals to

enhance their effectiveness and ROI for farmers. These innovations also allow

real-time tracking of biological performance to build trust and encourage

increased adoption among end-users. With existing participation by

biotechnology firms and agriculture startups in the market space, the pipeline

of innovation is rich and dynamic. These technologies increasing commercial

viability and broad-scale adoption will be expected to drive a significant

growth enhancement in the market and unlock fresh chances in developed and

emerging agricultural economies.

Agricultural Biologicals Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 22.7 Billion |

|

Market Forecast in 2033 |

USD 68.4 Billion |

|

CAGR % 2025-2033 |

14.1% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production capacity, growth factors and more |

|

Segments Covered |

●

By Product Type ●

By Mode of Application ●

By Application |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

China 9)

India 10)

Japan 11)

South Korea 12)

Australia 13)

Mexico 14)

Brazil 15)

Argentina 16)

Saudi Arabia 17)

UAE 18) South Africa |

Agricultural Biologicals Market Report Segmentation Analysis

The Global Agricultural

Biologicals Market Industry Analysis Is Segmented by Product Type, by Mode of

Application, by Application and by Region.

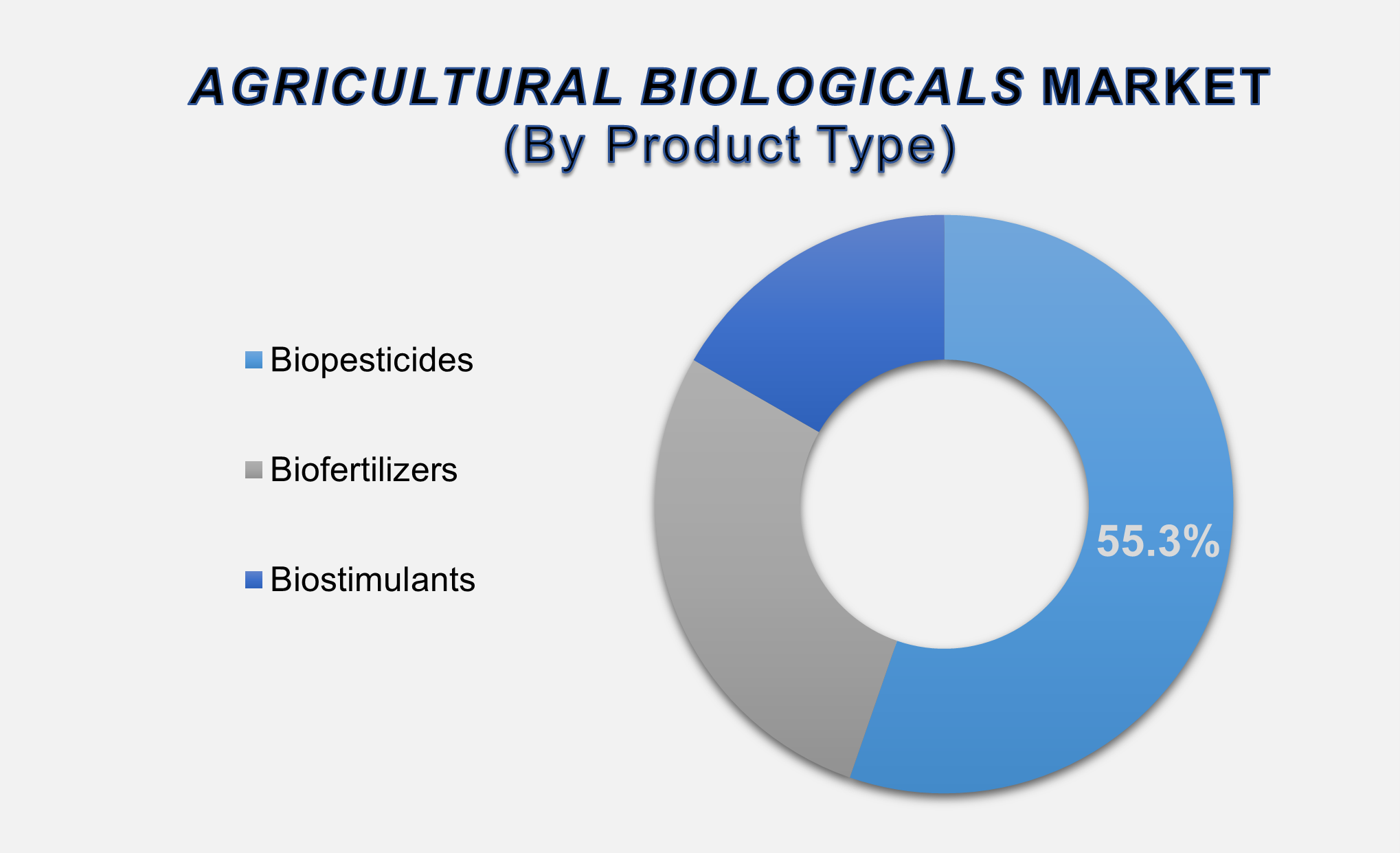

The Biopesticides Segment Is Anticipated To Hold The Highest

Share Of The Global Agricultural Biologicals Market During The Projected

Timeframe

By product type, the market is segmented into Biopesticides, Biofertilizers, and Biostimulants. Among these, the Biopesticides segment is anticipated to hold the highest share of 55.3% in the global agricultural biologicals market. The dominance of biopesticides is largely attributed to the growing global push to reduce the usage of chemical pesticides, which are associated with harmful environmental and health effects. Biopesticides are derived from natural materials such as bacteria, fungi, and plant extracts, making them environmentally friendly and safe for non-target organisms, including beneficial insects and pollinators. Increasing regulatory support for biopesticides and the rising occurrence of pesticide-resistant pests are further accelerating their adoption in integrated pest management (IPM) practices.

The Seed Treatment segment is anticipated to hold the highest

share of the market over the forecast period

By mode of application, the

market is segmented into Soil Treatment, Seed Treatment, and Foliar Spray. The

Seed Treatment segment is anticipated to hold the highest share of the market

over the forecast period. This growth is due to the efficiency and accuracy in

treating seeds before planting, which ensures protection against pests and

pathogens from the early stages in the soil. Biological seed treatment

increases germination percentages of the seeds, plant vigor, and root strength.

In addition to that, the cost savings and ease of use mean that seed treatment

is the most favored among farmers in large-scale production. This method also

finds good use in support of sustainable agriculture since it minimizes the use

of multiple applications of agrochemicals throughout the cropping cycle.

The Cereals & Grains Segment Dominated The Market In 2024

And Is Predicted To Grow At The Highest CAGR Over The Forecast Period

By application, the market is

segmented into Cereals & Grains, Oilseed & Pulses, Fruits &

Vegetables, and Others. The Cereals & Grains segment dominated the market

in 2024 and is predicted to grow at the highest CAGR over the forecast period.

The growth is driven by vast cultivation areas and demand in the international

market for staple crops of grains and cereal crops such as wheat, maize, and

rice. These crops are highly vulnerable to pest and disease pressure and are

hence good targets for biological crop enhancement and protection products.

Farmers also use biologicals in increasing proportions to improve the production

of grains and cereals in order to achieve sustainability and meet regulatory

requirements for pesticide residues in food exports.

The following segments are part of an in-depth analysis of the global

agricultural biologicals market:

|

Market Segments |

|

|

By Product Type |

●

Biopesticides ●

Biofertilizers ●

Biostimulants |

|

By Mode of Application |

●

Soil Treatment ●

Seed Treatment ●

Foliar Spray |

|

By Application |

●

Cereals & Grains ●

Oilseed & Pulses ●

Fruits &

Vegetables ●

Others |

Agricultural Biologicals

Market Share Analysis by Region

North America Is

Projected To Hold The Largest Share Of The Global Agricultural Biologicals

Market Over The Forecast Period.

In 2024, North America accounts

for the largest share of over 36.5% in the global Agricultural Biologicals

Market. This is attributed to a highly developed agri-infrastructure base in

the region, robust R&D capacity, and rising demand for sustainable

agriculture practices. Strong demand from agriculture in the region is fueled

by stringent regulations against chemical agrochemicals and a growing demand

among consumers for organic and chemical residue-free food products. Both the

U.S. and Canada together power the market growth of the region with government

support towards applying sustainability to agriculture and enhanced market

awareness among farmers and scientists towards biological products and

technologies. The strong presence of major industry players disrupting product

offerings with innovation is also contributing to market growth in the region.

Investments in cutting-edge biological solutions in pest management, soil

health improvement, and crop growth enhancement, and the increasing practice of

regenerative agriculture also increased the adoption level among large farms

and specialty crop growers in the region.

Furthermore, the Asia-Pacific is

likely to experience the most significant CAGR over the forecast period due to

the dynamic growth of the agriculture industry in emerging nations such as

China, India, and Southeast Asia. Driving growth in the region is a cluster of

factors that include rising demand for food, expanding interest in

sustainability in farming and agriculture, and incentives from the government

in favor of adopting bio-inputs. Abundant arable land in the region and a large

and expanding population of farmers offer huge opportunities for farm

biological producers seeking to expand their market footprint in high-growth

regions.

Agricultural Biologicals

Market Competition Landscape Analysis

The Global Agricultural

Biologicals Market is marked by robust competition among key players focusing

on innovation, strategic expansion, and sustainability. Continuous research and

development efforts lead to the introduction of advanced Agricultural Biologicals

formulations with improved performance characteristics, catering to evolving

industry demands.

Global Agricultural

Biologicals Market Recent Developments News:

●

In December 2024,

Koppert, a global leader in biological crop solutions, partnered with Greentech

innovator Amoéba to launch AXPERA, a groundbreaking biofungicide powered by

Amoéba's proprietary amoeba lysate technology. This collaboration combines

Amoéba's cutting-edge microbiological research with Koppert's extensive

agricultural expertise and global distribution channels to deliver a

sustainable alternative for fungal disease control.

●

In January 2024,

Certis Biologicals launched Convergence Biofungicide, a breakthrough

dual-action crop protection solution specifically formulated for corn,

soybeans, and peanuts. This innovative product delivers superior disease

control while enhancing overall plant health—all in a cost-effective,

easy-to-use formulation.

The Global Agricultural Biologicals Market is dominated by

a few large companies, such as

●

BASF SE

●

Bayer CropScience Company

●

Biomax

●

CBF China Bio-Fertilizer AG

●

Isagro Company

●

Kiwa Bio-Tech Products Group Corporation

●

Koppert Biological Systems

●

Lallemand Inc

●

Mapleton Agri Biotec

●

Marrone Bio Innovation Inc

●

National Fertilizers Ltd

●

Novozymes AS

●

Rizobacter Argentina SA

●

Sigma Agri-Science LLC

●

Symborg SL

●

Syngenta AG

●

The Dow Chemical Company

●

Valent BioSciences Corporation

●

Zebra Medical Vision Inc

●

Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Agricultural

Biologicals Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Agricultural Biologicals Market Scope and Market Estimation

1.2.1.Global Agricultural

Biologicals Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Agricultural

Biologicals Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product Type of Global Agricultural

Biologicals Market

1.3.2.Mode of Application of

Global Agricultural Biologicals Market

1.3.3.Application of Global Agricultural

Biologicals Market

1.3.4.Region of Global Agricultural

Biologicals Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Market

Dynamics

2.5.1.Drivers

2.5.2.Limitations

2.5.3.Opportunities

2.5.4.Impact Analysis of Drivers

and Restraints

2.6.

Key

Product/Brand Analysis

2.7.

Technological

Advancements

2.8.

Key

Developments

2.9.

Porter’s

Five Forces Analysis

2.9.1.Bargaining Power of

Suppliers

2.9.2.Bargaining Power of Buyers

2.9.3.Threat of Substitutes

2.9.4.Threat of New Entrants

2.9.5.Competitive Rivalry

2.10.

PEST

Analysis

2.10.1.

Political

Factors

2.10.2.

Economic

Factors

2.10.3.

Social

Factors

2.10.4.

Technology

Factors

2.11.

Insights

on Cost-effectiveness of Agricultural Biologicals

2.12.

Key

Regulation

3. Global

Agricultural Biologicals Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Agricultural Biologicals Market Estimates

& Forecast Trend Analysis, by Product Type

4.1.

Global

Agricultural Biologicals Market Revenue (US$ Bn) Estimates and Forecasts, by Product

Type, 2020 - 2033

4.1.1.Biopesticides

4.1.2.Biofertilizers

4.1.3.Biostimulants

5. Global

Agricultural Biologicals Market Estimates

& Forecast Trend Analysis, by Mode of Application

5.1.

Global

Agricultural Biologicals Market Revenue (US$ Bn) Estimates and Forecasts, by Mode

of Application, 2020 - 2033

5.1.1.Soil Treatment

5.1.2.Seed Treatment

5.1.3.Foliar Spray

6. Global

Agricultural Biologicals Market Estimates

& Forecast Trend Analysis, by Application

6.1.

Global

Agricultural Biologicals Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

6.1.1.Cereals & Grains

6.1.2.Oilseed & Pulses

6.1.3.Fruits & Vegetables

6.1.4.Others

7. Global

Agricultural Biologicals Market Estimates

& Forecast Trend Analysis, by Region

7.1.

Global

Agricultural Biologicals Market Revenue (US$ Bn) Estimates and Forecasts, by Region,

2020 - 2033

7.1.1.North America

7.1.2.Western Europe

7.1.3.Eastern Europe

7.1.4.Asia Pacific

7.1.5.Middle East & Africa

7.1.6.Latin America

8. North America Agricultural

Biologicals Market: Estimates &

Forecast Trend Analysis

8.1. North America Agricultural

Biologicals Market Assessments & Key Findings

8.1.1.North America Agricultural

Biologicals Market Introduction

8.1.2.North America Agricultural

Biologicals Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Product

Type

8.1.2.2. By Mode of

Application

8.1.2.3. By Application

8.1.2.4.

By

Country

8.1.2.4.1.

The

U.S.

8.1.2.4.2.

Canada

9. Europe Agricultural

Biologicals Market: Estimates &

Forecast Trend Analysis

9.1.

Europe

Agricultural Biologicals Market Assessments & Key Findings

9.1.1.Europe Agricultural

Biologicals Market Introduction

9.1.2.Europe Agricultural

Biologicals Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product

Type

9.1.2.2. By Mode of

Application

9.1.2.3. By Application

9.1.2.4.

By

Country

9.1.2.4.1. Germany

9.1.2.4.2. Italy

9.1.2.4.3. U.K.

9.1.2.4.4. France

9.1.2.4.5. Spain

9.1.2.4.6.

Rest of Europe

10. Asia Pacific Agricultural

Biologicals Market: Estimates &

Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Agricultural Biologicals Market Introduction

10.1.2.

Asia

Pacific Agricultural Biologicals Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1. By Product

Type

10.1.2.2. By Mode of

Application

10.1.2.3. By Application

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6.

Rest

of Asia Pacific

11. Middle East & Africa Agricultural

Biologicals Market: Estimates &

Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Agricultural Biologicals Market

Introduction

11.1.2.

Middle East & Africa Agricultural Biologicals Market Size

Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Product

Type

11.1.2.2. By Mode of

Application

11.1.2.3. By Application

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4.

Rest of MEA

12. Latin America

Agricultural Biologicals Market:

Estimates & Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Agricultural Biologicals Market Introduction

12.1.2.

Latin

America Agricultural Biologicals Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

12.1.2.1. By Product

Type

12.1.2.2. By Mode of

Application

12.1.2.3. By Application

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Colombia

12.1.2.4.4.

Rest of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Agricultural Biologicals Market Product Mapping

14.2.

Global

Agricultural Biologicals Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3.

Global

Agricultural Biologicals Market Tier Structure Analysis

14.4.

Global

Agricultural Biologicals Market Concentration & Company Market Shares (%)

Analysis, 2024

15.

Company

Profiles

15.1.

BASF SE

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

*

Similar details would be provided for all the players mentioned below

15.2. Bayer

CropScience Company

15.3. Biomax

15.4. CBF

China Bio-Fertilizer AG

15.5. Isagro

Company

15.6. Kiwa

Bio-Tech Products Group Corporation

15.7. Koppert

Biological Systems

15.8. Lallemand

Inc

15.9. Mapleton

Agri Biotec

15.10. Marrone

Bio Innovation Inc

15.11. National

Fertilizers Ltd

15.12. Novozymes

AS

15.13. Rizobacter

Argentina SA

15.14. Sigma

Agri-Science LLC

15.15. Symborg

SL

15.16. Syngenta

AG

15.17. The Dow

Chemical Company

15.18. Valent

BioSciences Corporation

15.19. Zebra

Medical Vision Inc

15.20. Others

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables