Agriculture Pumps Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Pump Type (Rotodynamic Pump and Positive Displacement Pumps); By Power Source (Electric (Grid-Connected), Diesel/Petrol and Solar-Powered); By Power Range (0.5–3 HP, 4–15 HP, 16–30 HP, 31–40 HP and Above 40 HP); By Distribution Channel (Direct Sales, Distributors / Dealers, Retail Outlets, Online / E-commerce, Agri‑tradeshows and Expos) and Geography

2025-08-12

Agriculture Industry

Jaya Bundele (Research Analyst)

Description

Agriculture Pumps Market Overview

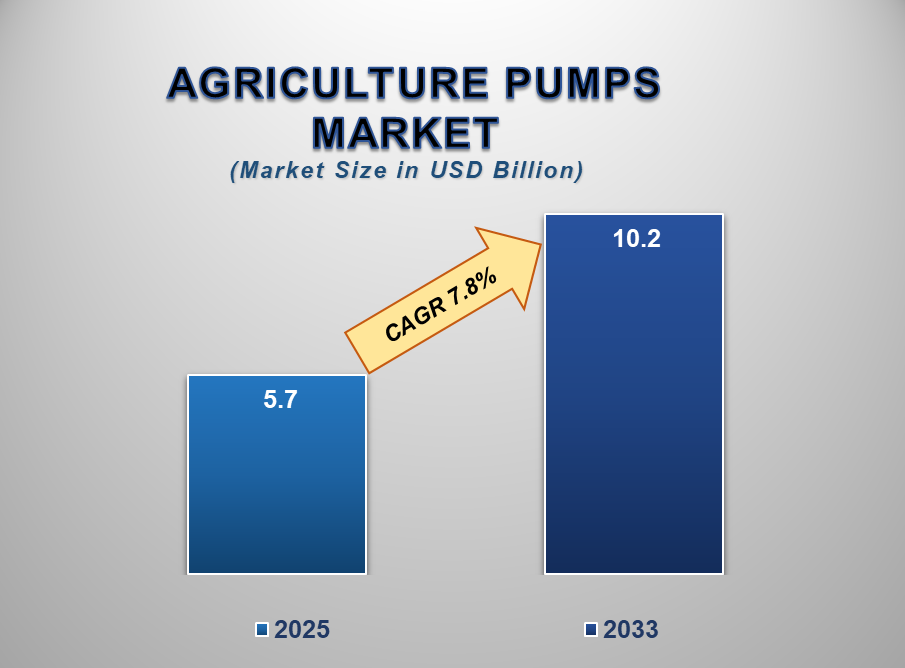

The Agriculture Pumps Market size is projected to witness significant growth from 2025 to 2033, driven by technological advancements in pump manufacturing. Valued at approximately USD 5.7 billion in 2025, the market is expected to surge to USD 10.2 billion by 2033, reflecting a strong compound annual growth rate (CAGR) of 7.8% over the forecast period.

The agricultural pumps market plays a critical role in ensuring a reliable water supply for irrigation, livestock, fertigation, and other farming activities. These pumps are essential for improving agricultural productivity, especially in regions where rainfall is inconsistent or inadequate. The market encompasses a wide range of pump types—including centrifugal and positive displacement pumps—operating across various power ranges to meet the needs of smallholder farmers and large-scale commercial operations alike. Demand is driven by rising global food requirements, increasing adoption of mechanized farming, and government support programs, particularly in developing countries.

Solar-powered pumps are gaining traction due to sustainability concerns and rural electrification challenges. Asia-Pacific dominates the market, led by countries like India and China, while growth is also notable in Africa and Latin America. As climate change intensifies pressure on water resources, efficient and energy-saving agricultural pumps will be crucial in enabling sustainable farming and improving water management in the agricultural sector.

Agriculture Pumps Market Drivers and Opportunities

Rising Demand for Efficient Irrigation Systems to Drive Agriculture Pumps Market Growth

The growing global need to improve agricultural output with limited water resources is significantly driving the adoption of efficient irrigation systems, thereby boosting demand for agricultural pumps. As traditional flood irrigation methods become increasingly unsustainable due to water scarcity, farmers are turning to modern solutions such as drip and sprinkler systems, which require reliable and high-performing pumps. These pumps enable precise water delivery, reduce wastage, and support the cultivation of high-value crops.

In regions like Asia-Pacific and Africa—where agriculture heavily depends on timely irrigation—governments are promoting pump adoption through subsidies and rural development programs. Furthermore, technological innovations such as smart and solar-powered pumps are enhancing irrigation efficiency and accessibility. As a result, the agricultural pumps market is expected to grow steadily in tandem with the rising emphasis on sustainable irrigation practices and precision farming, both of which are essential to meet global food demand amid changing climate conditions.

Government Initiatives and Subsidy Programs

Government initiatives aimed at improving agricultural productivity are a major driver for the agricultural pumps market. Many developing countries, particularly in the Asia-Pacific and Africa, are investing in rural infrastructure and supporting farmers through subsidies for irrigation equipment, including pumps. For instance, India's PM-KUSUM scheme promotes the adoption of solar-powered pumps by offering financial assistance to farmers, thus reducing dependency on diesel or grid electricity. These initiatives not only help smallholder farmers access reliable irrigation but also contribute to reducing greenhouse gas emissions and operational costs.

In addition, several governments partner with private entities and NGOs to implement community-based irrigation projects that require efficient pump systems. This institutional support is vital in regions facing frequent droughts or erratic rainfall. As global food security becomes a priority, government policies encouraging sustainable water use and energy efficiency in agriculture will continue to fuel the adoption of agricultural pumps across various power ranges and applications.

Opportunity for the Agriculture Pumps Market

Technological Advancements in Solar-Powered Pumps

The rapid advancement of solar-powered pump technology presents a significant opportunity for the agricultural pumps market, especially in regions with unreliable electricity access. With falling costs of solar panels and improvements in photovoltaic efficiency, solar-powered pumps have become an economically viable and environmentally friendly alternative to diesel and electric pumps. These pumps offer benefits such as low operating costs, minimal maintenance, and independence from grid connectivity—making them ideal for small and remote farms.

Governments and international agencies are increasingly funding solar pump deployment as part of climate-resilient agriculture programs. Moreover, the integration of IoT and smart controllers in solar pump systems enables real-time monitoring and optimized water usage, enhancing their appeal among tech-savvy and sustainability-focused farmers. As the world pushes toward decarbonization and water conservation, the adoption of solar-powered agricultural pumps is expected to surge, opening new avenues for manufacturers, installers, and financing institutions in emerging and underserved markets.

Agriculture Pumps Market Scope

Agriculture Pumps Market Report Segmentation Analysis

The global Agriculture Pumps Market industry analysis is segmented by Pump Type, by Power Source, by Power Range, by Distribution Channel, and by region.

The Rotodynamic Pump Type segment is anticipated to hold the major share of the global Agriculture Pumps Market during the projected timeframe.

The rotodynamic pump type segment is expected to dominate the global agricultural pumps market during the forecast period due to its high efficiency, ease of use, and broad applicability in various irrigation practices. This category includes centrifugal, axial-flow, and mixed-flow pumps, which are widely preferred for their ability to handle large volumes of water with relatively low energy input. Among them, centrifugal pumps are the most commonly used in agriculture for surface and sub-surface water movement, especially in flood irrigation and sprinkler systems. These pumps are also relatively simple in design, cost-effective, and require less maintenance compared to other types. Their compatibility with multiple power sources—including electric motors and solar panels—further enhances their flexibility and appeal among farmers. As global agricultural operations scale up and seek more energy-efficient irrigation solutions, the demand for rotodynamic pumps is projected to increase steadily, ensuring their leading market position throughout the forecast timeline.

The Electric (Grid-Connected) Power Source segment is fastest-growing segment for the Agriculture Pumps Market

The electric (grid-connected) power source segment is anticipated to be the fastest-growing category in the agricultural pumps market due to expanding rural electrification and growing awareness of clean energy alternatives. Farmers are increasingly shifting from diesel-powered pumps to electric variants as electricity becomes more accessible and affordable, particularly in developing countries. Grid-connected pumps offer lower operational costs, reduced emissions, and consistent performance, making them highly suitable for modern irrigation systems like drip and sprinkler setups. Additionally, government initiatives aimed at electrifying rural areas and subsidizing electric irrigation equipment are accelerating this transition. Countries such as India and China are witnessing a rapid uptake of electric pumps due to strong policy support. Furthermore, as smart farming technologies advance, grid-connected electric pumps are easier to integrate with automation tools and IoT-based control systems. These advantages make them an attractive choice, contributing to their fast-paced growth in both smallholder and commercial agricultural applications.

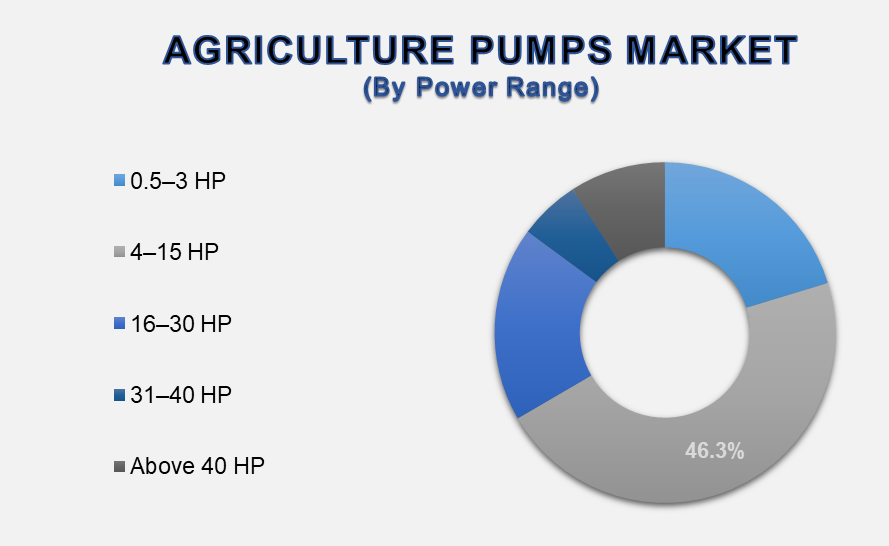

The 4-15 HP power range segment is anticipated to hold the highest share of the market over the forecast period

The 4–15 HP power range segment is expected to hold the largest share of the global agricultural pumps market over the forecast period. This power range strikes an ideal balance between energy efficiency and water delivery capacity, making it highly suitable for small to medium-sized farms. Pumps in this category are versatile enough to handle various irrigation methods—such as drip, sprinkler, and flood systems—across diverse crops and field sizes.

They are powerful enough to deliver substantial water flow while remaining cost-effective in terms of fuel or electricity consumption. This range is especially popular in emerging markets like India, China, and parts of Africa, where fragmented land holdings require moderately powered yet reliable pump solutions. Governments and NGOs also tend to promote pumps in this category through subsidy and support programs aimed at smallholder farmers. As mechanization and irrigation modernization grow across developing regions, the 4–15 HP segment will remain the most in-demand across the global market.

The Distributors / Dealers distribution channel segment is anticipated to hold the highest share of the market over the forecast period.

The distributors and dealers segment is projected to hold the highest share of the agricultural pumps market distribution channel over the forecast period. This dominance is largely due to the segment’s deep-rooted presence in rural and semi-urban regions where most agricultural activity occurs. Distributors and dealers serve as critical intermediaries between manufacturers and end-users, offering product availability, installation services, and after-sales support. They also provide guidance to farmers on pump selection based on specific irrigation needs and farm size. Local dealers often build long-term trust with farming communities, making them the preferred channel for pump purchases. Moreover, manufacturers rely on these networks for market penetration, warranty servicing, and localized promotions. As the agricultural pumps market becomes more competitive and fragmented, the role of well-established distribution networks becomes even more vital in maintaining brand presence and ensuring timely delivery and support. Consequently, this channel is expected to continue dominating pump sales globally.

The following segments are part of an in-depth analysis of the global Agriculture Pumps Market:

Agriculture Pumps Market Share Analysis by Region

The Asia Pacific region is expected to dominate the Global Agriculture Pumps Market during the Forecast Period

The Asia Pacific region is anticipated to dominate the global agricultural pumps market throughout the forecast period, driven by its large agricultural base, expanding population, and increasing focus on improving irrigation infrastructure. Countries like India, China, and Indonesia are among the world’s top agricultural producers, and they rely heavily on efficient water management systems to sustain crop yields. In India, for instance, a vast proportion of farmland depends on pumped irrigation systems, supported by strong government initiatives such as the PM-KUSUM scheme that subsidizes solar-powered pumps. Additionally, rising rural electrification, increasing awareness of energy-efficient solutions, and growing adoption of precision agriculture are all contributing to pump demand. The region also benefits from a strong presence of local pump manufacturers offering cost-effective and tailored solutions for diverse farm sizes. With continued investment in sustainable irrigation technologies and favorable government policies, the Asia Pacific is well-positioned to lead the global market in both pump volume and value.

Global Agriculture Pumps Market Recent Developments News:

In March 2025, Futurepump received a $2.3 million grant from the Gates Foundation to scale up manufacturing and expand access to affordable solar irrigation for smallholder farmers. The funding will support production capacity in India and bolster rural distribution networks.

In July 2024, Rivulis, a major provider of drip and micro-irrigation systems, entered a strategic partnership with Israeli ag-tech firm Phytech. Rivulis merged its precision ag subsidiary Manna into Phytech and became a shareholder, enhancing analytics-driven irrigation management.

In July 2025, Chamundeshwari Electricity Supply Corporation (CESC) launched a 172.8 MW solar generation project across Mysuru to directly power irrigation pumps under PM-KUSUM, involving agency land leases and government cost-sharing.

The Global Agriculture Pumps Market is dominated by a few large companies, such as

Grundfos Holding A/S

Xylem Inc.

Flowserve Corporation

KSB SE & Co. KGaA

Sulzer Ltd.

The Gorman-Rupp Company

Franklin Electric Co., Inc.

Wilo SE

Ebara Corporation

Bucher Industries AG (Rosenbauer Pumps)

Lubi Industries LLP

Texmo Industries

CRI Pumps Pvt. Ltd.

Shakti Pumps (India) Ltd.

Tsurumi Manufacturing Co., Ltd.

Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

- Global Agriculture Pumps Market Introduction and Market Overview

- Objectives of the Study

- Global Agriculture Pumps Market Scope and Market Estimation

- Global Agriculture Pumps Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Agriculture Pumps Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

- Market Segmentation

- Pump Type of Global Agriculture Pumps Market

- Power Source of Global Agriculture Pumps Market

- Power Range of Global Agriculture Pumps Market

- Distribution Channel of Global Agriculture Pumps Market

- Region of Global Agriculture Pumps Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Agriculture Pumps Market

- Key Products/Brand Analysis

- Pricing Analysis

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Agriculture Pumps Market Estimates & Historical Trend Analysis (2020 - 2024)

- Global Agriculture Pumps Market Estimates & Forecast Trend Analysis, by Pump Type

- Global Agriculture Pumps Market Revenue (US$ Bn) Estimates and Forecasts, by Pump Type, 2020 - 2033

- Rotodynamic Pump

- Positive Displacement Pumps

- Global Agriculture Pumps Market Estimates & Forecast Trend Analysis, by Power Source

- Global Agriculture Pumps Market Revenue (US$ Bn) Estimates and Forecasts, by Power Source, 2020 - 2033

- Electric (Grid-Connected)

- Diesel/Petrol

- Solar-Powered

- Global Agriculture Pumps Market Estimates & Forecast Trend Analysis, by Power Range

- Global Agriculture Pumps Market Revenue (US$ Bn) Estimates and Forecasts, by Power Range, 2020 - 2033

- 0.5–3 HP

- 4–15 HP

- 16–30 HP

- 31–40 HP

- Above 40 HP

- Global Agriculture Pumps Market Estimates & Forecast Trend Analysis, by Distribution Channel

- Global Agriculture Pumps Market Revenue (US$ Bn) Estimates and Forecasts, by Power Range, 2020 - 2033

- Direct Sales

- Distributors / Dealers

- Retail Outlets

- Online / E-commerce

- Agri‑tradeshows and Expos

- Global Agriculture Pumps Market Estimates & Forecast Trend Analysis, by region

- Global Agriculture Pumps Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- North America Agriculture Pumps Market: Estimates & Forecast Trend Analysis

- North America Agriculture Pumps Market Assessments & Key Findings

- North America Agriculture Pumps Market Introduction

- North America Agriculture Pumps Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Pump Type

- By Power Source

- By Power Range

- By Distribution Channel

- By Country

- The U.S.

- Canada

- Europe Agriculture Pumps Market: Estimates & Forecast Trend Analysis

- Europe Agriculture Pumps Market Assessments & Key Findings

- Europe Agriculture Pumps Market Introduction

- Europe Agriculture Pumps Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Pump Type

- By Power Source

- By Power Range

- By Distribution Channel

- By Country

- Germany

- Italy

- U.K.

- France

- Spain

- Netherland

- Rest of Europe

- Asia Pacific Agriculture Pumps Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Agriculture Pumps Market Introduction

- Asia Pacific Agriculture Pumps Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Pump Type

- By Power Source

- By Power Range

- By Distribution Channel

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East & Africa Agriculture Pumps Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Agriculture Pumps Market Introduction

- Middle East & Africa Agriculture Pumps Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Pump Type

- By Power Source

- By Power Range

- By Distribution Channel

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Latin America Agriculture Pumps Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Agriculture Pumps Market Introduction

- Latin America Agriculture Pumps Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Pump Type

- By Power Source

- By Power Range

- By Distribution Channel

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Country Wise Market: Introduction

- Competition Landscape

- Global Agriculture Pumps Market Product Mapping

- Global Agriculture Pumps Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Agriculture Pumps Market Tier Structure Analysis

- Global Agriculture Pumps Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

- Grundfos Holding A/S

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

* Similar details would be provided for all the players mentioned below

- Xylem Inc.

- Flowserve Corporation

- KSB SE & Co. KGaA

- Sulzer Ltd.

- The Gorman-Rupp Company

- Franklin Electric Co., Inc.

- Wilo SE

- Ebara Corporation

- Bucher Industries AG (Rosenbauer Pumps)

- Lubi Industries LLP

- Texmo Industries

- CRI Pumps Pvt. Ltd.

- Shakti Pumps (India) Ltd.

- Tsurumi Manufacturing Co., Ltd.

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables