AI Agents in Financial Services Market Size and Forecast (2025–2033), Global and Regional Trends, Share, and Industry Analysis Report Coverage: By Type (Risk Management Agents, Compliance & Regulatory Agents, Fraud Detection Agents, Customer Service Agents, Credit Scoring Agents, Others), By Institutional Type (Traditional Banks, InsurTech Firms, FinTech Companies, Others), By Technology (Machine Learning & Deep Learning, Large Language Models, Robotic Process Automation, Cloud Computing & APIs, Others), and Geography

2026-01-02

Business & Financial Services

Ekta Chaurasia (Team Lead)

Description

AI Agents in the Financial Services Market Overview

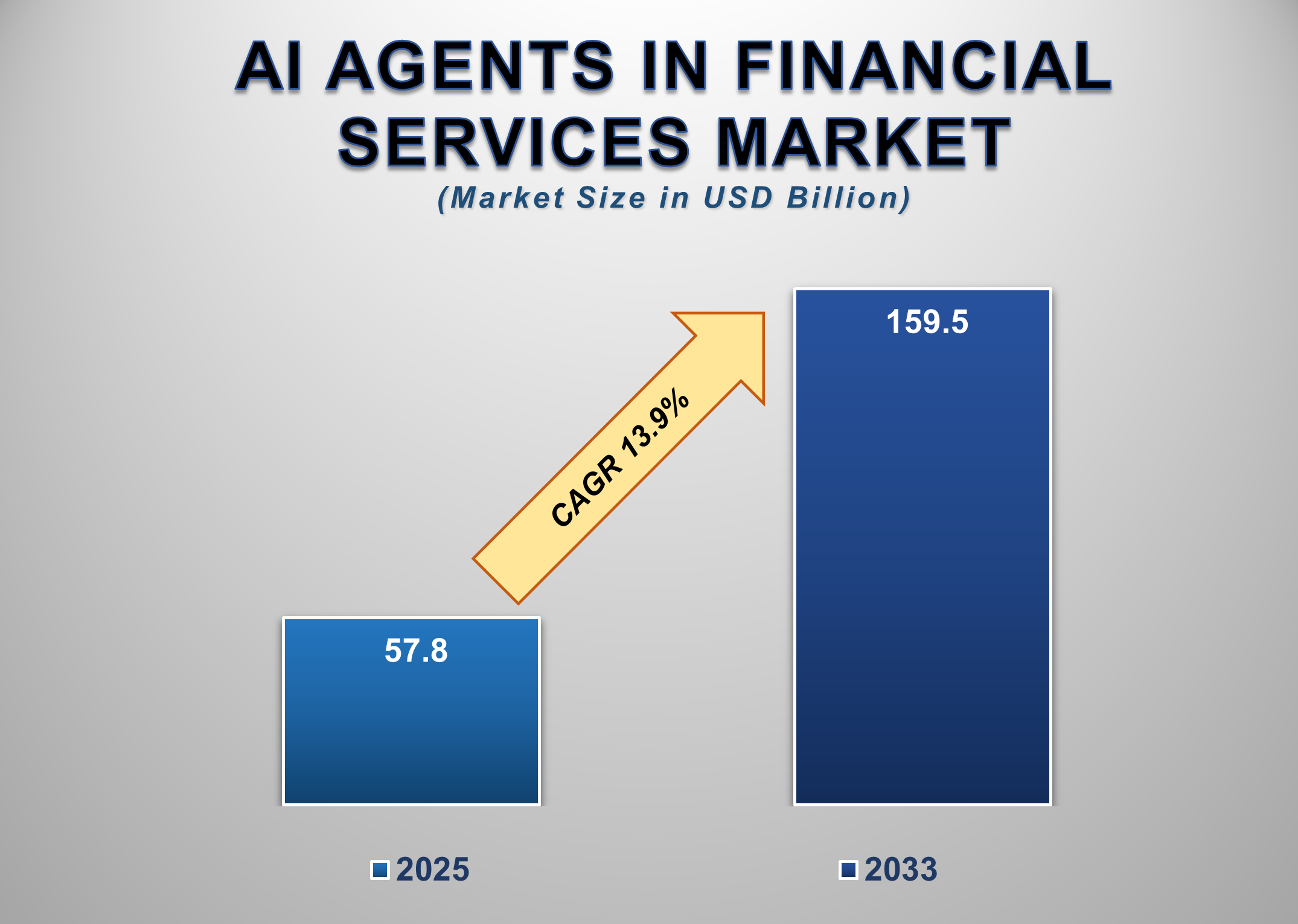

The Global AI Agents in Financial Services Market is witnessing strong growth as financial institutions adopt intelligent automation to enhance decision-making, operational efficiency, and customer experience. AI agents, autonomous or semi-autonomous systems powered by machine learning, LLMs, analytics, and predictive algorithms, are increasingly integrated across banking, insurance, payments, and capital markets. The market reached USD 57.8 billion in 2025 and is projected to reach USD 159.5 billion by 2033, expanding at a CAGR of 13.9%. This growth is propelled by the rapid shift toward digital banking, escalating fraud incidents, and regulatory pressures requiring more advanced compliance technologies. AI agents now handle tasks such as transaction monitoring, credit scoring, risk assessment, underwriting, customer onboarding, and advisory services, significantly reducing human workload and error rates.

Financial institutions are also

deploying generative AI-driven agents for conversational banking, anomaly

detection, underwriting automation, and investment analytics. North America

currently leads the market with a 41.2% share, supported by high adoption rates

among major banks and established regulatory frameworks.

AI Agents in Financial

Services Market Drivers and Opportunities

Rising Financial Fraud

and Cyberthreats Are Driving the Adoption of AI Agents Across Banks and FinTech

Platforms

Rising fraud incidents,

cyberattacks, and financial crimes are among the strongest drivers accelerating

the adoption of AI agents in the global financial services sector. Traditional

rule-based fraud detection systems are no longer sufficient due to increasingly

sophisticated cyberthreats, identity theft, phishing, synthetic fraud, and

account takeover (ATO) techniques. AI agents equipped with machine learning,

deep learning, natural language processing, and anomaly detection models can

analyze millions of transactions in real time, identify suspicious patterns,

and autonomously block high-risk activities. This significantly enhances fraud

prevention accuracy while reducing false positives, a key challenge faced by

financial institutions. Banks and fintech companies are leveraging AI agents

for behavioral biometrics, transaction scoring, digital identity verification,

and AML monitoring. These agents continuously learn from new data, making them

more effective against emerging fraud typologies. With the exponential rise in

digital transactions, open banking ecosystems, and cross-border payments, the

threat landscape has expanded, making automated risk mitigation a necessity.

Regulators globally are enforcing stricter compliance standards, further

encouraging institutions to adopt AI-powered fraud detection and AML agents. As

security threats grow more complex, AI agents offer the scalable, 24/7

monitoring capabilities required to safeguard digital financial systems, making

fraud prevention one of the most critical growth drivers in this market.

Growing Regulatory Pressure and Complexity in Compliance

Workflows Are Fueling the Demand for AI-Driven Compliance Agents

The increasing stringency of compliance regulations worldwide is

creating substantial demand for AI agents that streamline regulatory reporting,

risk monitoring, and policy adherence. Financial institutions face complex

requirements related to anti-money laundering (AML), know-your-customer (KYC),

customer due diligence (CDD), Basel III rules, IFRS standards, GDPR, and

country-specific banking regulations. Managing compliance manually is

time-consuming, error-prone, and costly. AI-powered compliance and regulatory

agents automate document verification, risk scoring, sanctions screening,

transaction auditing, suspicious activity report (SAR) generation, and

regulatory document interpretation using ML and LLM-based models.

These agents can analyze vast regulatory datasets, detect

discrepancies in real-time, and ensure timely reporting, reducing compliance

breaches and associated penalties. The emergence of regulatory technology

(RegTech) has further accelerated AI adoption, enabling institutions to achieve

continuous compliance with minimal manual intervention. Generative AI agents

capable of interpreting evolving regulatory guidelines, summarizing updates,

and recommending required actions are transforming compliance departments into

AI-augmented units. As global regulatory frameworks become more dynamic,

particularly around digital banking, crypto-assets, ESG reporting, and

cybersecurity, institutions increasingly rely on intelligent agents to maintain

operational integrity. The shift from manual compliance to AI-driven regulatory

intelligence remains a powerful market growth driver for financial institutions

worldwide.

Expanding AI Adoption in Emerging Markets and SME Financial

Services Is Creating Significant Growth Opportunities Worldwide

The accelerating adoption of AI agents in emerging economies

presents major opportunities for market players. Countries across Asia-Pacific,

Latin America, the Middle East, and Africa are modernizing their banking

infrastructures, promoting digital finance, and strengthening financial

inclusion initiatives. Small and mid-sized financial institutions,

traditionally limited by cost and expertise constraints, are increasingly

embracing cloud-based AI agents for fraud monitoring, risk scoring,

underwriting assistance, and customer engagement. The availability of

subscription-based AI solutions and API-driven deployment models is making

advanced financial automation accessible to a broader market. AI agents also

support microfinance, rural banking, and digital lending ecosystems, which are

expanding rapidly in developing regions. These agents enable real-time

creditworthiness assessment for underbanked populations using alternative data

such as mobile usage, transaction history, and digital behavioral patterns. Governments

in several emerging markets are encouraging AI adoption through national AI

strategies, sandboxes, and digitization programs. FinTech startups are

integrating AI agents into payment systems, mobile banking apps, and InsurTech

platforms, further fueling innovation. As emerging economies digitize financial

operations and expand financial inclusion, AI agents offer scalable,

cost-effective, and high-impact solutions, positioning developing regions as

high-growth opportunity hubs for global AI technology vendors.

AI Agents in the

Financial Services Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 57.8 Billion |

|

Market Forecast in 2033 |

USD 159.5 Billion |

|

CAGR % 2025-2033 |

13.9% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Type,

Institutional Type, Technology |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

AI Agents in Financial

Services Market Report Segmentation Analysis

The AI Agents in the Financial Services Market are segmented by

type, institutional type, technology, and geography.

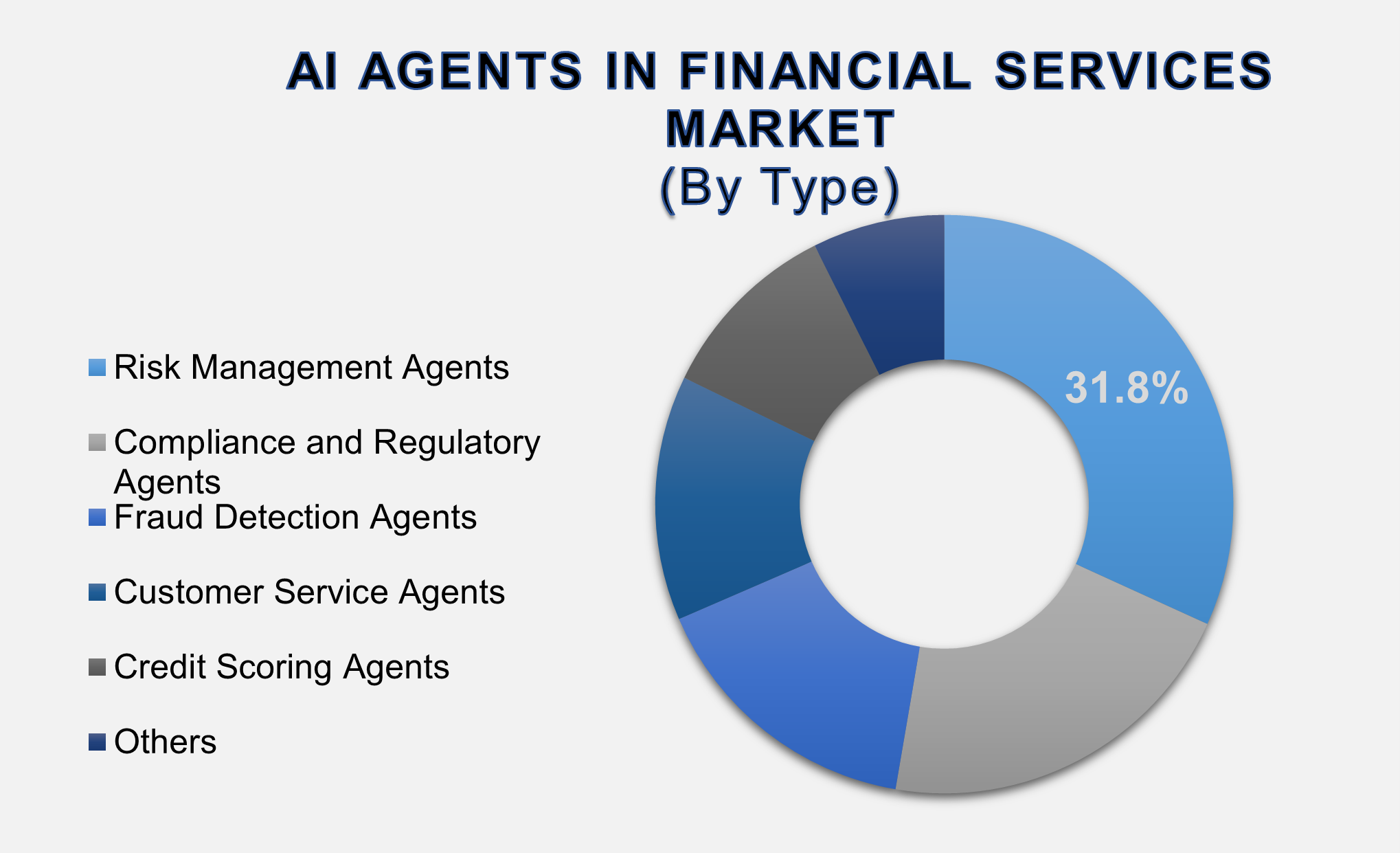

Risk Management Agents

Accounted for the Largest Market Share in the Global AI Agents in Financial

Services Market

Risk Management Agents accounted for the largest market share in the global AI Agents in Financial Services market, driven by the critical need for accurate, real-time risk profiling and decision support across banking and insurance ecosystems. These agents utilize machine learning models, predictive analytics, and generative AI capabilities to evaluate credit risks, market volatility, liquidity exposure, portfolio risks, and operational vulnerabilities. Financial institutions increasingly rely on AI-driven risk agents to improve forecasting accuracy, automate risk scoring, and optimize capital allocation processes. With rising market instability, fluctuating interest rates, and stricter regulatory frameworks, risk management functions require rapid data analysis and scenario simulation capabilities that AI agents deliver far more efficiently than traditional tools. Adoption is also supported by the growth of algorithmic trading, digital lending, and decentralized finance platforms, where real-time risk insights are crucial. As risk evaluation becomes more data-intensive and complex, the dominance of AI-enabled risk agents is expected to strengthen further.

The Traditional Banks

Segment Accounted for the Largest Market Share in the Global AI Agents in

Financial Services Market

The Traditional Banks segment

accounted for the largest market share in the global AI Agents in Financial

Services market, as large financial institutions continue to lead investments

in AI-driven modernization. Traditional banks manage vast customer bases, high

transaction volumes, and complex regulatory obligations, making AI agents

essential for automating workflows such as KYC verification, customer

onboarding, risk assessment, fraud detection, and portfolio management. With

heightened competition from fintech disruptors, banks are adopting AI agents to

deliver personalized customer experiences, reduce operational costs, and

enhance digital service delivery. Generative AI agents are increasingly

deployed for conversational banking, automated advisory services, and

transaction insights. Additionally, banks face regulatory pressure to maintain

compliance accuracy and improve financial crime surveillance, further

reinforcing AI adoption. Their robust IT infrastructure, access to extensive

historical data, and financial resources enable large-scale integration of

machine learning, LLMs, and cloud-based AI models, solidifying traditional

banks' leadership in market share.

Machine Learning &

Deep Learning Segment Accounted for the Largest Market Share in the Global AI

Agents in Financial Services Market

The Machine Learning (ML) &

Deep Learning segment accounted for the largest market share in the global AI

Agents in Financial Services market, supported by widespread use of predictive

modeling, behavioral analytics, and real-time data processing across financial

workflows. These technologies form the foundation for most AI agent

functionalities, including fraud detection, customer segmentation, credit

scoring, risk modeling, and personalized product recommendations. ML and deep

learning models continuously learn from new datasets, improving accuracy and

adaptability, making them ideal for dynamic financial environments. Their

integration with advanced neural networks enables superior pattern recognition,

anomaly detection, and autonomous decision-making compared with rule-based

systems. Financial institutions also use deep learning to power chatbots,

underwriting automation, sentiment analytics, and high-frequency trading

algorithms. As data volumes grow exponentially and digital financial

interactions increase, ML and deep learning remain the most widely adopted

technologies underlying AI agents, sustaining their dominance in the technology

segment.

The following segments are

part of an in-depth analysis of the global AI Agents in Financial Services

market:

|

Market Segments |

|

|

By Type |

●

Risk Management

Agents ●

Compliance and

Regulatory Agents ●

Fraud Detection

Agents ●

Customer Service

Agents ●

Credit Scoring

Agents ●

Others |

|

By

Institutional Type |

●

Traditional Banks ●

InsurTech Firms ●

FinTech Companies ●

Others |

|

By Technology |

●

Machine Learning

(ML) & Deep Learning ●

Large Language

Models (LLMs) ●

Robotic Process

Automation (RPA) ●

Cloud Computing

& APIs ●

Others |

AI Agents in Financial

Services Market Share Analysis by Region

North America is

anticipated to hold the largest portion of the AI Agents in the Financial

Services Market globally throughout the forecast period.

North America held the largest

share of the global AI Agents in Financial Services market at 41.2% in 2025,

driven by early adoption of AI technologies, a strong presence of major

financial institutions, and advancements in cloud infrastructure. U.S. banks,

fintech companies, and insurance firms have been at the forefront of deploying

AI-driven agents for fraud prevention, risk modeling, automated compliance, and

digital customer engagement. Favorable regulatory frameworks, high digital

banking penetration, and ongoing investments in generative AI and machine

learning platforms further strengthen the region’s leadership.

Asia-Pacific, however, is

projected to witness the highest CAGR through 2033, supported by the rapid

expansion of fintech ecosystems, government-led digital transformation

programs, and strong mobile banking adoption. Countries such as China, India,

Singapore, and Japan are integrating AI agents into digital lending, InsurTech

services, payment gateways, and neobanking platforms. Growing financial

inclusion initiatives and the rise of SME lending are accelerating demand for

intelligent automation. Europe continues to adopt AI agents to enhance

regulatory compliance, cybersecurity resilience, and open banking services

under PSD2 guidelines. Meanwhile, the Middle East and Latin America are

emerging as fast-developing markets due to investments in digital banking

infrastructure and AI-driven financial modernization. Overall, global adoption

is expected to rise significantly across all regions.

AI Agents in Financial

Services Market Competition Landscape Analysis

The competitive landscape of the

AI Agents in the Financial Services market is characterized by strong

participation from global technology companies, cloud service providers, AI

software vendors, fintech firms, and industry-focused solution providers. Key

players are expanding capabilities in generative AI, LLM-based automation,

predictive analytics, and API-driven integration to meet the growing demand for

intelligent financial services.

Global AI Agents in

Financial Services Market Recent Developments News:

- In March 2025,

Oracle Financial Services launched agentic AI capabilities within its

Investigation Hub Cloud Service, enabling financial institutions to

automate complex fraud investigations. The AI agents identify

sophisticated crime patterns, generate detailed narratives, and prioritize

high-value leads, reducing manual

effort and improving investigation efficiency and accuracy globally.

- In March 2025,

Auquan introduced its industry-first risk agent, an autonomous AI

solution for financial risk monitoring. The agent continuously scans over

two million multilingual data sources to detect emerging investment,

credit, and operational risks, automating entire risk workflows and

delivering early warnings to enhance institutional decision-making.

The Global AI Agents in Financial Services Market Is Dominated by a Few Large Companies, such as

●

IBM

●

Google

●

Microsoft

●

Amazon Web Services

●

Oracle

●

SAP

●

Accenture

●

Infosys

●

Capgemini

●

FIS Global

●

Fiserv

●

SS&C Technologies

●

Bloomberg

●

Refinitiv

●

Salesforce

●

NICE Actimize

●

Compliance.ai

●

Kensho

●

AlphaSense

●

Ayasdi

● Others

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global AI Agents in

Financial Services Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

AI Agents in Financial Services Market Scope and Market Estimation

1.2.1.Global AI Agents in

Financial Services Overall Market Size (US$ Bn), Market CAGR (%), Market

forecast (2025 - 2033)

1.2.2.Global AI Agents in

Financial Services Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 -

2033

1.3.

Market

Segmentation

1.3.1.Type of Global AI Agents

in Financial Services Market

1.3.2.Institutional Type of

Global AI Agents in Financial Services Market

1.3.3.Technology of Global AI

Agents in Financial Services Market

1.3.4.Region of Global AI Agents

in Financial Services Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

AI Agents in Financial Services Market

Estimates & Historical Trend Analysis (2020 - 2024)

4. Global

AI Agents in Financial Services Market

Estimates & Forecast Trend Analysis, by Type

4.1.

Global

AI Agents in Financial Services Market Revenue (US$ Bn) Estimates and

Forecasts, by Type, 2020 - 2033

4.1.1.Risk Management Agents

4.1.2.Compliance and Regulatory

Agents

4.1.3.Fraud Detection Agents

4.1.4.Customer Service Agents

4.1.5.Credit Scoring Agents

4.1.6.Others

5. Global

AI Agents in Financial Services Market

Estimates & Forecast Trend Analysis, by Institutional

Type

5.1.

Global

AI Agents in Financial Services Market Revenue (US$ Bn) Estimates and

Forecasts, by Institutional Type, 2020 - 2033

5.1.1.Traditional Banks

5.1.2.InsurTech Firms

5.1.3.FinTech Companies

5.1.4.Others

6. Global

AI Agents in Financial Services Market

Estimates & Forecast Trend Analysis, by Technology

6.1.

Global

AI Agents in Financial Services Market Revenue (US$ Bn) Estimates and

Forecasts, by Technology, 2020 - 2033

6.1.1.Machine Learning (ML)

& Deep Learning

6.1.2.Large Language Models

(LLMs)

6.1.3.Robotic Process Automation

(RPA)

6.1.4.Cloud Computing & APIs

6.1.5.Others

7. Global

AI Agents in Financial Services Market

Estimates & Forecast Trend Analysis, by Region

7.1.

Global

AI Agents in Financial Services Market Revenue (US$ Bn) Estimates and

Forecasts, by Region, 2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America AI

Agents in Financial Services Market:

Estimates & Forecast Trend Analysis

8.1.

North

America AI Agents in Financial Services Market Assessments & Key Findings

8.1.1.North America AI Agents in

Financial Services Market Introduction

8.1.2.North America AI Agents in

Financial Services Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Type

8.1.2.2. By Institutional

Type

8.1.2.3. By Technology

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe AI

Agents in Financial Services Market:

Estimates & Forecast Trend Analysis

9.1.

Europe

AI Agents in Financial Services Market Assessments & Key Findings

9.1.1.Europe AI Agents in

Financial Services Market Introduction

9.1.2.Europe AI Agents in

Financial Services Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Type

9.1.2.2. By Institutional

Type

9.1.2.3. By Technology

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific AI

Agents in Financial Services Market:

Estimates & Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific AI Agents in Financial Services Market Introduction

10.1.2.

Asia

Pacific AI Agents in Financial Services Market Size Estimates and Forecast (US$

Billion) (2020 - 2033)

10.1.2.1. By Type

10.1.2.2. By Institutional

Type

10.1.2.3. By Technology

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa AI

Agents in Financial Services Market:

Estimates & Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa AI Agents in Financial Services

Market Introduction

11.1.2.

Middle East & Africa AI Agents in Financial Services

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Type

11.1.2.2. By Institutional

Type

11.1.2.3. By Technology

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

AI Agents in Financial Services Market:

Estimates & Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America AI Agents in Financial Services Market Introduction

12.1.2.

Latin

America AI Agents in Financial Services Market Size Estimates and Forecast (US$

Billion) (2020 - 2033)

12.1.2.1. By Type

12.1.2.2. By Institutional

Type

12.1.2.3. By Technology

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

AI Agents in Financial Services Market Product Mapping

14.2.

Global

AI Agents in Financial Services Market Concentration Analysis, by Leading

Players / Innovators / Emerging Players / New Entrants

14.3.

Global

AI Agents in Financial Services Market Tier Structure Analysis

14.4.

Global

AI Agents in Financial Services Market Concentration & Company Market

Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

IBM

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. Google

15.3. Microsoft

15.4. Amazon

Web Services

15.5. Oracle

15.6. SAP

15.7. Accenture

15.8. Infosys

15.9. Capgemini

15.10. FIS

Global

15.11. Fiserv

15.12. SS&C

Technologies

15.13. Bloomberg

15.14. Refinitiv

15.15. Salesforce

15.16. NICE

Actimize

15.17. Compliance.ai

15.18. Kensho

15.19. AlphaSense

15.20. Ayasdi

15.21. Others

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables