Alfalfa Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Animal Type (Cattle, Horses, Others), By Feed Type (Hay, Cubes, Pellets), and Geography

2026-02-25

Agriculture Industry

Jaya Bundele (Research Analyst)

Description

Alfalfa Market Overview

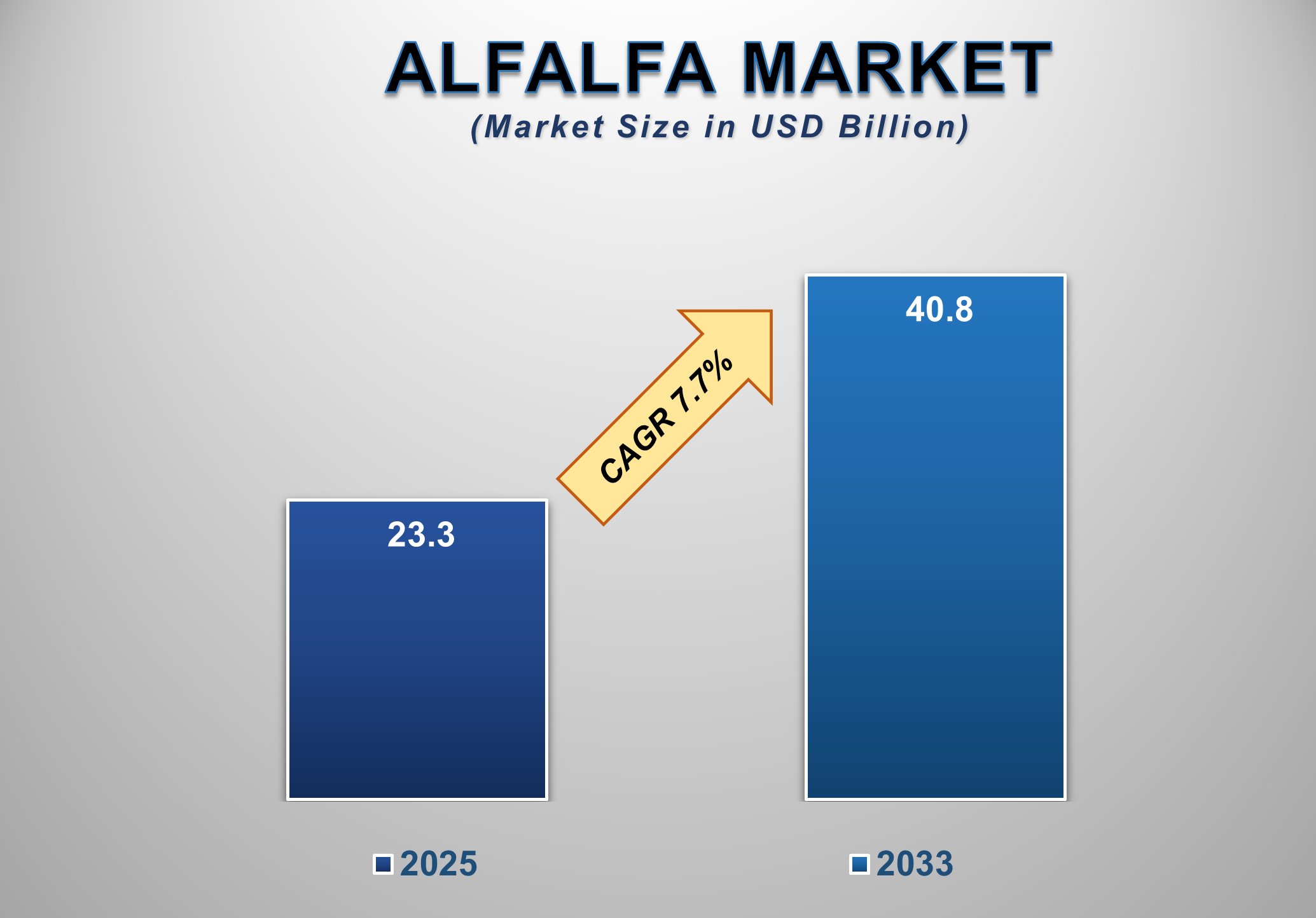

The global alfalfa market was valued at USD 23.3 billion in 2025 and is projected to reach USD 40.8 billion by 2033, growing at a CAGR of 7.7% during the forecast period. Market expansion is primarily driven by rising demand for high-protein forage crops, increasing livestock population, growing commercial dairy and beef production, and heightened focus on animal nutrition efficiency. Alfalfa remains one of the most widely cultivated and consumed forage crops globally due to its superior nutritional profile, digestibility, and role in improving livestock productivity.

Alfalfa is extensively used as a

primary feed ingredient for cattle, horses, and other ruminants, owing to its

high protein content, essential amino acids, vitamins, and minerals. The crop

plays a critical role in enhancing milk yield, meat quality, and overall animal

health. As global demand for dairy products, beef, and animal-derived proteins

continues to rise, the importance of nutritionally dense feed crops such as

alfalfa has increased substantially. Additionally, advancements in agricultural

practices, improved alfalfa seed varieties, mechanized harvesting, and better

storage solutions have enhanced crop yield and feed quality. Export-oriented

alfalfa production, particularly from North America, is further strengthening

global trade flows. As sustainable livestock farming and feed efficiency gain

prominence, the alfalfa market is expected to witness steady and sustained

growth through 2033.

Alfalfa Market Drivers

and Opportunities

Rising Livestock Population and Dairy Consumption Are Driving

Market Growth

The increasing global livestock population, particularly cattle,

is a major driver of the alfalfa market. Growing consumption of milk, cheese,

yogurt, and other dairy products has intensified demand for high-quality forage

that supports higher milk yield and consistent production. Alfalfa, with its

high crude protein content and digestibility, is widely preferred in dairy

rations to enhance lactation performance. Expanding commercial dairy farming in

both developed and emerging economies has further accelerated alfalfa demand.

Countries with large-scale dairy operations increasingly rely on alfalfa hay,

pellets, and cubes to maintain feed consistency throughout the year. Moreover,

rising urbanization and changing dietary habits are increasing per capita consumption

of animal protein, indirectly boosting alfalfa usage. Government support

programs aimed at improving livestock productivity and farmer incomes also

contribute to market growth. Subsidies for fodder cultivation, improved

irrigation infrastructure, and extension services promoting high-yield forage

crops have encouraged wider alfalfa adoption. As livestock farming becomes more

intensive and efficiency-driven, alfalfa demand is expected to grow steadily.

Nutritional Advantages and Feed Efficiency Are Strengthening

Market Expansion

Alfalfa’s superior nutritional characteristics are another key

driver of market growth. It offers a balanced combination of protein, fiber,

calcium, and vitamins, making it an essential component of ruminant diets.

Compared to other forage crops, alfalfa provides higher feed conversion

efficiency, enabling farmers to achieve better productivity with lower feed

volumes. The crop’s role in improving rumen function and reducing digestive

disorders has made it a preferred feed option among livestock producers. Alfalfa

also contributes to better weight gain in beef cattle and improved reproductive

performance in breeding animals. These benefits are particularly valuable in

intensive farming systems where productivity optimization is critical.

Additionally, alfalfa’s nitrogen-fixing properties enhance soil

fertility, reducing reliance on synthetic fertilizers and supporting

sustainable agricultural practices. As environmental sustainability becomes a

priority across agricultural value chains, alfalfa’s dual role as a feed crop

and soil enhancer is expected to further boost its adoption.

Expanding Export Demand and Value-Added Feed Products Present

Key Opportunities

The growing international trade of alfalfa represents a significant opportunity for market expansion. Rising demand from regions with limited arable land or water resources has increased imports of alfalfa hay and processed feed products. North America, in particular, has emerged as a major exporter, supplying alfalfa to Asia Pacific and Middle Eastern markets. Value-added feed products such as alfalfa pellets and cubes are gaining popularity due to their ease of storage, transportation, and standardized nutritional content. These formats reduce spoilage risks and allow precise ration formulation, making them attractive for large-scale livestock operations. Technological advancements in processing and packaging are further enhancing product quality and shelf life. As global livestock supply chains become more interconnected, opportunities for premium alfalfa products and export-oriented production are expected to grow. Investments in logistics infrastructure and quality certification systems will play a crucial role in unlocking these opportunities

Alfalfa Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 23.3 Billion |

|

Market Forecast in 2035 |

USD 40.8 Billion |

|

CAGR % 2025-2035 |

7.7% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2035 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Animal Type ●

By Feed Type |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Alfalfa Market Report

Segmentation Analysis

The Global Alfalfa Market

Industry Analysis Is Segmented By Animal Type, By Feed Type, and By Region.

Cattle Segment Is Expected to Dominate the Alfalfa Market

During the Forecast Period

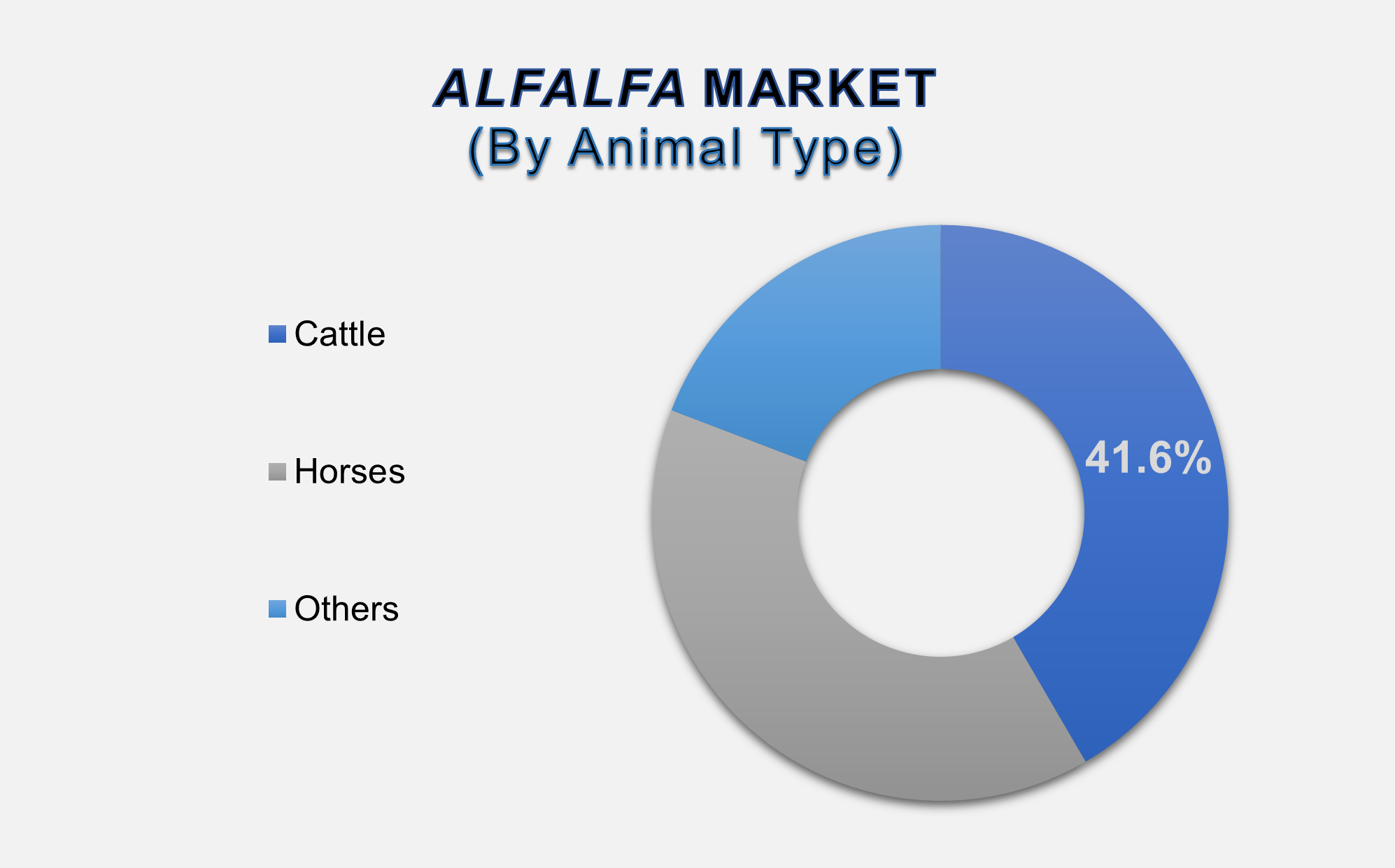

The cattle segment accounted for approximately 41.6% of the global alfalfa market, making it the dominant animal type segment. This leadership is driven by the extensive use of alfalfa in dairy and beef cattle diets due to its high protein content and positive impact on milk yield and weight gain. Dairy cattle operations rely heavily on alfalfa to support consistent lactation performance, particularly in high-producing herds. Beef cattle producers use alfalfa to enhance feed efficiency and improve carcass quality. The crop’s adaptability to different feeding systems, including total mixed rations, further supports its widespread adoption. As global demand for dairy and beef products continues to rise, the cattle segment is expected to maintain its dominant position in the alfalfa market throughout the forecast period.

Hay

Feed Type Is Expected to Lead Market Demand Through 2033

The hay

segment is expected to hold the largest share of the alfalfa market, driven by

its widespread availability, cost-effectiveness, and suitability for both

small-scale and commercial livestock operations. Alfalfa hay is widely used due

to its natural form, ease of feeding, and minimal processing requirements. Hay

remains the preferred feed type in regions with strong domestic alfalfa

production and established storage infrastructure. Its flexibility in feeding

schedules and compatibility with traditional livestock practices further

support its dominance. Despite growing adoption of processed feed formats,

alfalfa hay is expected to remain the primary feed type due to its economic and

practical advantages.

The following segments are

part of an in-depth analysis of the global Alfalfa market:

|

Market Segments |

|

|

By Animal Type |

●

Cattle ●

Horses ●

Others |

|

By Feed Type |

●

Hay ●

Cubes ●

Pellets |

Alfalfa Market Share

Analysis by Region

North America is

anticipated to hold the biggest portion of the Alfalfa Market globally

throughout the forecast period.

North America accounted for

approximately 37.9% of the global alfalfa market in 2025, making it the largest

regional market. The region benefits from favorable climatic conditions,

advanced farming practices, and strong mechanization levels that support high-yield

alfalfa cultivation. The United States dominates regional production and

exports, supported by large dairy and beef industries. Well-established

logistics infrastructure and access to international markets further reinforce

North America’s leadership. Additionally, continuous investment in seed

technology, irrigation efficiency, and harvesting equipment enhances

productivity and feed quality across the region.

Asia Pacific is expected to

register the highest CAGR during the forecast period, driven by rapid growth in

livestock farming, rising demand for animal protein, and increasing reliance on

imported feed. Countries such as China, Japan, and South Korea are major

importers of alfalfa due to limited domestic production capacity and water

constraints. Expanding dairy consumption, modernization of livestock

operations, and government initiatives to improve feed quality are accelerating

market growth. As livestock industries in Asia Pacific continue to scale up,

the region is poised to become the fastest-growing market for alfalfa globally.

Alfalfa Market

Competition Landscape Analysis

The alfalfa market is moderately

fragmented, with the presence of regional producers, export-oriented suppliers,

and specialized feed companies. Competition is based on feed quality,

consistency, pricing, processing capabilities, and export reach. Companies

focus on expanding production capacity, improving feed processing technologies,

and strengthening distribution networks to enhance market presence.

Global Alfalfa Market

Recent Developments News:

- In June 2025 – Cibus and S&W Seed Company

received FDA regulatory clearance to commercialize their gene-edited,

low-lignin alfalfa. This innovation enables higher digestibility forage,

directly addressing the demand for sustainable and efficient animal-feed

solutions. It strengthens their position in the advanced forage genetics

market, which is increasingly critical for large-scale dairy operations.

- In May 2025 – A research collaboration in Quebec,

led by INRS (Institut National de la Recherche Scientifique) , developed a

system using satellite imaging and machine learning to monitor alfalfa

crop height and health. This precision agriculture tool provides real-time

insights for irrigation, fertilization, and harvest planning, helping

producers mitigate risks from rising production costs and climate

volatility.

- In September 2023 – DLF acquired Corteva

Agriscience’s alfalfa breeding program, including key germplasm,

trademarks (such as Alforex Seeds), and hybrid trait technologies. This

acquisition significantly expanded DLF's portfolio of high-performance

forage genetics and solidified its market footprint in North America,

positioning it to better serve the export demands of the Asia-Pacific

region.

The Global Alfalfa Market Is

Dominated by a Few Large Companies, such as

●

Alfalfa Monegros, S.L.

●

Anderson Hay &

Grain Inc.

●

Standlee Premium

Products, LLC

●

Green Prairie

International Inc

●

SL Follen Company

●

Bailey Farms

●

Haykingdom Inc.

●

Cubeit Hay Company

●

Old Manor Farm Ltd.

●

Barr-Ag Ltd.

● Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Medical Tourism

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Medical Tourism Market Scope and Market Estimation

1.2.1.Global Medical Tourism Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Medical Tourism

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Healthcare Services of

Global Medical Tourism Market

1.3.2.Service Provider of Global

Medical Tourism Market

1.3.3.Region of Global Medical

Tourism Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Medical Tourism Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Medical Tourism Market Estimates

& Forecast Trend Analysis, by Healthcare Services

4.1.

Global

Medical Tourism Market Revenue (US$ Bn) Estimates and Forecasts, by Healthcare

Services, 2020 - 2033

4.1.1.Medical Treatment

4.1.1.1.

Cardiac

Procedures

4.1.1.2.

Oncology

Procedures

4.1.1.3.

Orthopedic

& Spine Procedures

4.1.1.4.

Dental

Procedures

4.1.1.5.

Others

4.1.2.Wellness Treatment

4.1.2.1.

Cosmetic

Procedures

4.1.2.2.

Rejuvenation

Procedures

4.1.2.3.

Others

4.1.3.Alternative Treatment

5. Global

Medical Tourism Market Estimates

& Forecast Trend Analysis, by Service Provider

5.1.

Global

Medical Tourism Market Revenue (US$ Bn) Estimates and Forecasts, by Service

Provider, 2020 - 2033

5.1.1.Public

5.1.2.Private

6. Global

Medical Tourism Market Estimates

& Forecast Trend Analysis, by Region

6.1.

Global

Medical Tourism Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020

- 2033

6.1.1.North America

6.1.2.Europe

6.1.3.Asia Pacific

6.1.4.Middle East & Africa

6.1.5.Latin America

7. North America Medical

Tourism Market: Estimates &

Forecast Trend Analysis

7.1.

North

America Medical Tourism Market Assessments & Key Findings

7.1.1.North America Medical

Tourism Market Introduction

7.1.2.North America Medical

Tourism Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

7.1.2.1. By Healthcare

Services

7.1.2.2. By Service

Provider

7.1.2.3.

By

Country

7.1.2.3.1. The U.S.

7.1.2.3.2. Canada

8. Europe Medical

Tourism Market: Estimates &

Forecast Trend Analysis

8.1.

Europe

Medical Tourism Market Assessments & Key Findings

8.1.1.Europe Medical Tourism

Market Introduction

8.1.2.Europe Medical Tourism

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Healthcare

Services

8.1.2.2. By Service

Provider

8.1.2.3.

By

Country

8.1.2.3.1.

Germany

8.1.2.3.2.

Italy

8.1.2.3.3.

U.K.

8.1.2.3.4.

France

8.1.2.3.5.

Spain

8.1.2.3.6.

Switzerland

8.1.2.3.7. Rest

of Europe

9. Asia Pacific Medical

Tourism Market: Estimates &

Forecast Trend Analysis

9.1.

Asia

Pacific Market Assessments & Key Findings

9.1.1.Asia Pacific Medical

Tourism Market Introduction

9.1.2.Asia Pacific Medical

Tourism Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Healthcare

Services

9.1.2.2. By Service

Provider

9.1.2.3.

By

Country

9.1.2.3.1.

China

9.1.2.3.2.

Japan

9.1.2.3.3.

India

9.1.2.3.4.

Australia

9.1.2.3.5.

South

Korea

9.1.2.3.6. Rest of Asia Pacific

10. Middle East & Africa Medical

Tourism Market: Estimates &

Forecast Trend Analysis

10.1.

Middle

East & Africa Market Assessments & Key Findings

10.1.1.

Middle East & Africa Medical Tourism Market Introduction

10.1.2.

Middle East & Africa Medical Tourism Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Healthcare

Services

10.1.2.2. By Service

Provider

10.1.2.3.

By

Country

10.1.2.3.1. UAE

10.1.2.3.2. Saudi

Arabia

10.1.2.3.3. South

Africa

10.1.2.3.4. Rest

of MEA

11. Latin America

Medical Tourism Market: Estimates &

Forecast Trend Analysis

11.1.

Latin

America Market Assessments & Key Findings

11.1.1.

Latin

America Medical Tourism Market Introduction

11.1.2.

Latin

America Medical Tourism Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

11.1.2.1. By Healthcare

Services

11.1.2.2. By Service

Provider

11.1.2.3.

By

Country

11.1.2.3.1. Brazil

11.1.2.3.2. Argentina

11.1.2.3.3. Mexico

11.1.2.3.4. Rest

of LATAM

12. Country Wise Market:

Introduction

13.

Competition

Landscape

13.1.

Global

Medical Tourism Market Product Mapping

13.2.

Global

Medical Tourism Market Concentration Analysis, by Leading Players / Innovators

/ Emerging Players / New Entrants

13.3.

Global

Medical Tourism Market Tier Structure Analysis

13.4.

Global

Medical Tourism Market Concentration & Company Market Shares (%) Analysis,

2024

14.

Company

Profiles

14.1.

Bumrungrad International Hospital

14.1.1.

Company

Overview & Key Stats

14.1.2.

Financial

Performance & KPIs

14.1.3.

Product

Portfolio

14.1.4.

SWOT

Analysis

14.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

14.2. Apollo

Hospitals Enterprise

14.3. Bangkok

Hospital

14.4. Anadolu

Medical Center

14.5. Fortis

Healthcare

14.6. Prince

Court Medical Centre

14.7. Asklepios

Kliniken

14.8. Shouldice

Hospital

14.9. Samitivej

Hospital

14.10. Gleneagles

Hospital

14.11. Raffles

Medical Group

14.12. KPJ

Healthcare Berhad

14.13. Clemenceau

Medical Center

14.14. Asian

Heart Institute

14.15. Burjeel

Hospital

14.16. Christus

Muguerza

14.17. Hospital

Clínic de Barcelona

14.18. UZ

Leuven

14.19. Johns

Hopkins Medicine International

14.20. Mayo

Clinic

14.21. Others

15. Research

Methodology

15.1.

External

Transportations / Databases

15.2.

Internal

Proprietary Database

15.3.

Primary

Research

15.4.

Secondary

Research

15.5.

Assumptions

15.6.

Limitations

15.7.

Report

FAQs

16. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables