Analytical Instruments Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Type (Chromatography, Spectroscopy, Molecular Analysis, Mass Spectrometry, Others), By Application (Life Science & Pharma, Environmental Testing, Food & Beverage, Petrochemicals, Others), By End-User (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Environmental Agencies, Industrial & Manufacturing Facilities) And Geography

2025-11-14

Healthcare

Swetal (Research Analyst)

Description

Analytical Instruments

Market Overview

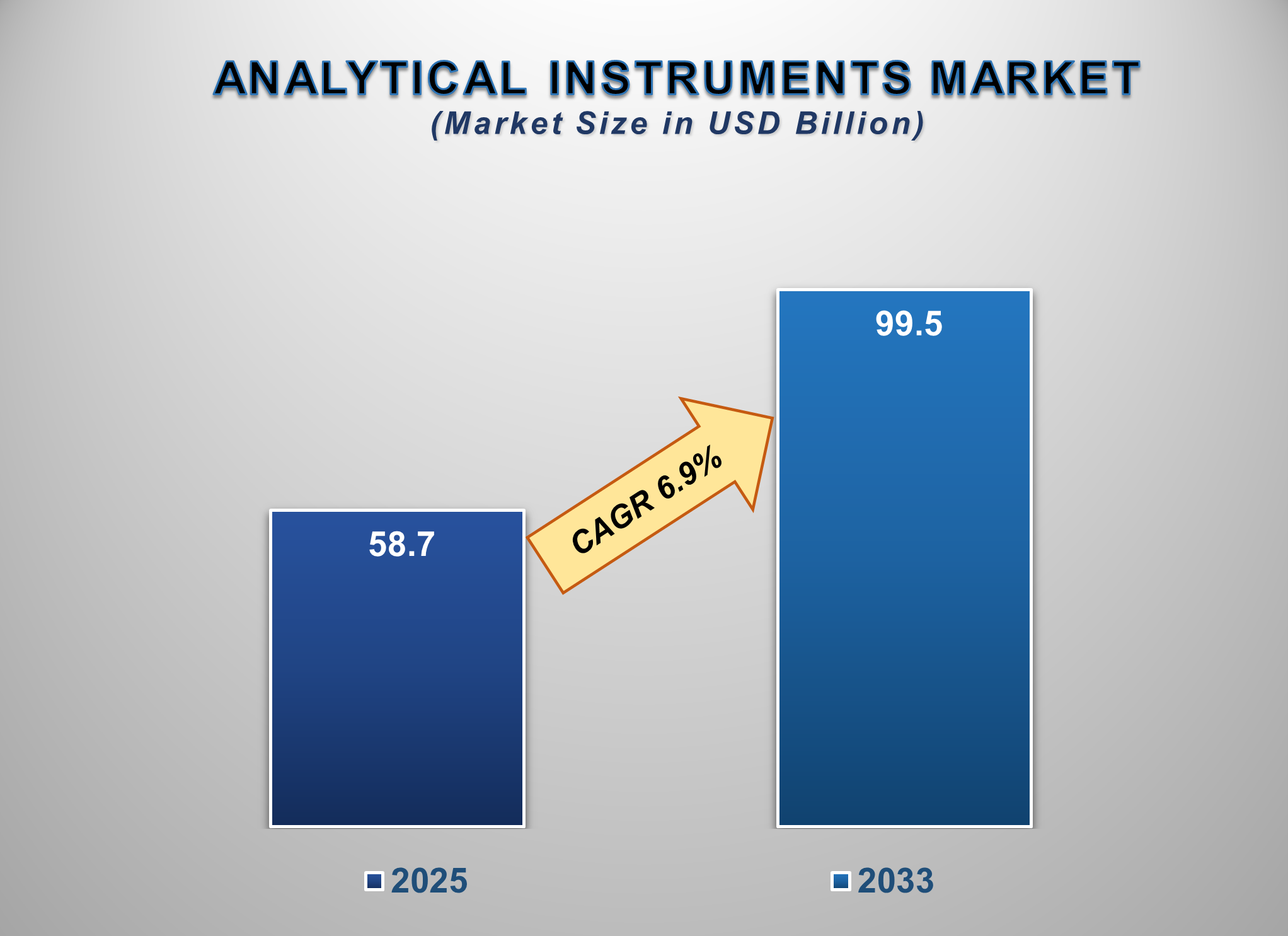

The Analytical Instruments Market is poised for a period of robust and sustained growth from 2025 to 2033, driven by technological advancements, stringent regulatory requirements, and increasing investment in quality control and R&D across diverse industries. The market is projected to be valued at approximately USD 58.7 billion in 2025 and is forecasted to reach nearly USD 99.5 billion by 2033, exhibiting a steady compound annual growth rate (CAGR) of 6.9% during this period.

Analytical instruments are sophisticated devices

used to identify, quantify, and analyze the chemical composition, structure,

and physical properties of substances. They are the backbone of scientific

research, quality assurance, and diagnostic processes. The market growth is

primarily fuelled by the expanding pharmaceutical and biotechnology sector,

where these instruments are critical for drug discovery, development, and

quality control.

Furthermore, increasing government regulations

regarding environmental monitoring, food safety, and product quality, coupled

with a growing emphasis on precision medicine and personalized diagnostics, are

creating sustained demand. Technological innovations such as the integration of

artificial intelligence (AI) and IoT for data analysis and instrument control,

the development of portable and handheld devices for on-site testing, and the

push for higher sensitivity, resolution, and throughput are key market

enablers. North America remains the dominant regional market due to high

R&D expenditure and a strong industrial base, while the Asia-Pacific region

is expected to witness the fastest growth, driven by industrialization and

increasing investment in healthcare and infrastructure.

Analytical Instruments Market Drivers and

Opportunities

Stringent Regulatory Standards and Quality

Control Demands are Foundational Market Drivers

Across the globe, regulatory bodies like the FDA

(Food and Drug Administration), EMA (European Medicines Agency), and EPA

(Environmental Protection Agency) are enforcing increasingly strict guidelines

for product safety and quality. In the pharmaceutical industry, adherence to

Good Manufacturing Practices (GMP) and the need for rigorous characterization

of biologics and complex drugs necessitate advanced analytical techniques like

HPLC, Mass Spectrometry, and Capillary Electrophoresis. Similarly, in the

food and beverage and environmental sectors,

regulations concerning contaminants, pollutants, and composition drive the

continuous demand for reliable analytical instrumentation for compliance

testing and monitoring. This regulatory pressure ensures a consistent,

non-discretionary market for analytical instruments.

The Biotechnology and Pharmaceutical Boom

is a Primary Growth Engine

The rapid growth of the biopharmaceutical

sector, including the development of complex modalities like monoclonal

antibodies, cell and gene therapies, and mRNA vaccines, has created an

unprecedented need for sophisticated analytical tools. These instruments are

indispensable for characterizing biomolecules, ensuring product purity and

potency, and monitoring manufacturing processes through Process Analytical

Technology (PAT). The rise of biopharmaceuticals, which are larger and more

complex than traditional small-molecule drugs, requires more advanced

analytical techniques for full characterization, thereby driving the adoption

of high-end mass spectrometers, chromatographic systems, and molecular analysis

instruments. The expanding pipeline of biologics and the increasing outsourcing

of analytical testing to CROs (Contract Research Organizations) further amplify

this demand.

Technological Advancements and the Shift

to Lab Automation Present Significant Opportunities

The market is undergoing a transformation driven

by technological innovation. Key areas of opportunity include the development

of hyphenated techniques (e.g., GC-MS, LC-MS) that combine separation and

detection for superior analysis, the miniaturization of instruments for field

deployment, and the integration of AI and machine learning for predictive

maintenance and automated data interpretation. Furthermore, the push for lab

automation and the "connected lab" is creating a strong demand for integrated,

high-throughput analytical systems that can enhance efficiency, reduce human

error, and streamline workflows. The emergence of portable and handheld

spectrometers and chromatographs is also opening new application areas in

environmental monitoring, food safety inspection, and point-of-care

diagnostics, representing a high-growth niche within the broader market.

Analytical Instruments Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 58.7 Billion |

|

Market Forecast in 2033 |

USD 99.5 Billion |

|

CAGR % 2025-2033 |

6.9% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio, Application Analysis, Company Market Share,

Company Heatmap, Regulatory Landscape, Growth Factors and more |

|

Segments Covered |

●

By Type ●

By Application ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Analytical Instruments Market Report Segmentation Analysis

The global analytical instruments

market industry analysis is segmented by Type, by Application, by End-User, and

by region.

The Spectroscopy segment is anticipated to command a

significant share in the global Analytical Instruments Market during the

forecast period.

Based on type, the market is divided into

Chromatography, Spectroscopy, Molecular Analysis, Mass Spectrometry, and Others

(e.g., microscopy, electrophoresis). The Spectroscopy segment, which includes

techniques like NMR, UV-Vis, and Atomic Absorption, is a major and consistently

growing category. Its dominance is attributed to its versatility, wide range of

applications from material science to pharmaceutical analysis, and its role as

a fundamental tool in both research and quality control laboratories. Mass

Spectrometry is also a high-growth sub-segment due to its unparalleled

sensitivity and specificity in identifying and quantifying compounds.

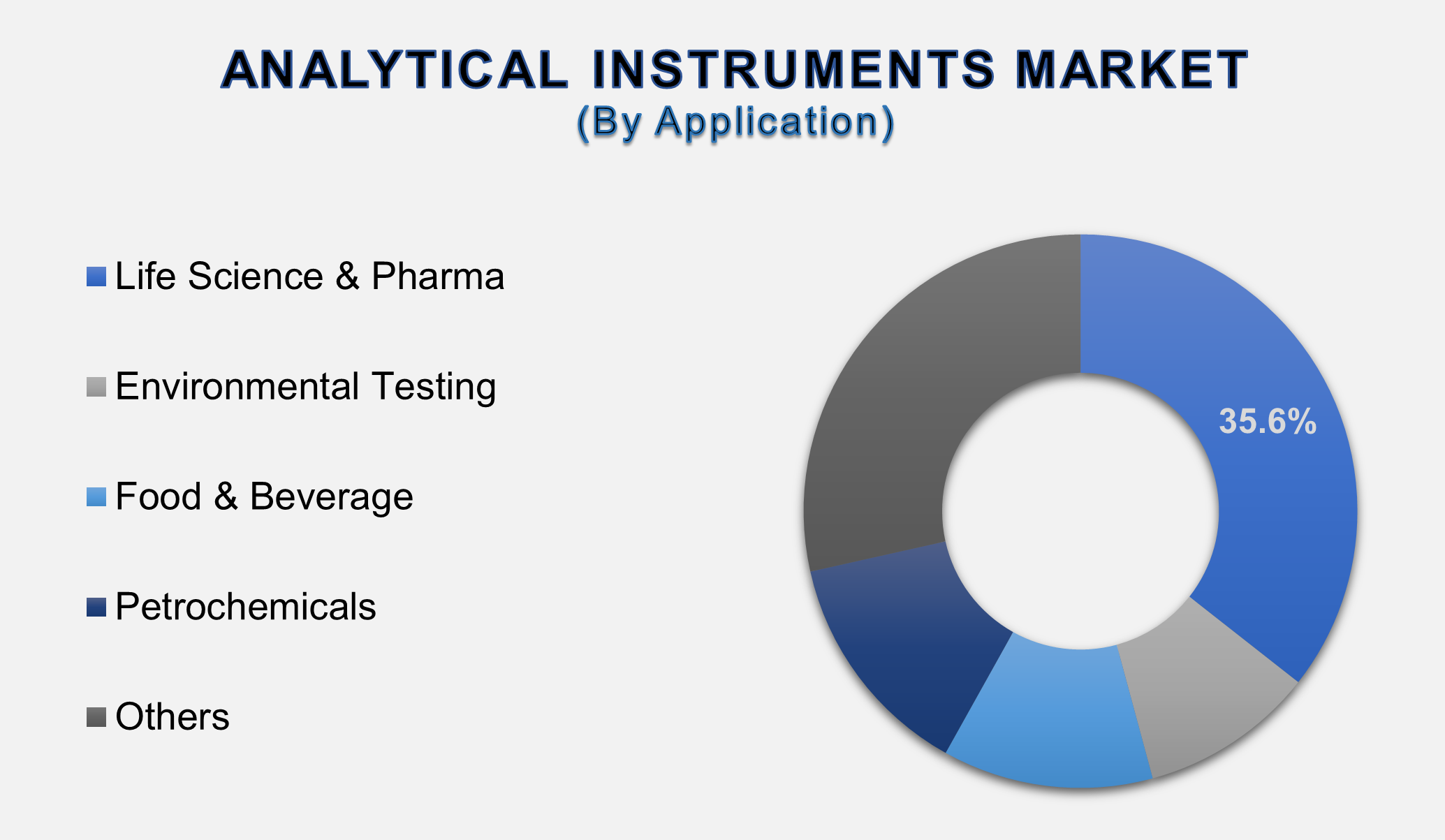

The Life Science & Pharma segment dominated the market in

2025 and is projected to grow at a significant CAGR during the forecast period.

Based on application, the market is segmented

into Life Science & Pharma, Environmental Testing, Food & Beverage,

Petrochemicals, and Others. The Life Science & Pharma segment holds the

largest share. This dominance is driven by the extensive use of analytical

instruments across the entire drug development lifecycle, from early-stage

research and target identification to clinical trials, quality control, and

batch release of finished products. The high cost of advanced instruments used

in this sector and the critical nature of their application contribute

significantly to the segment's revenue.

The Life Science & Pharma segment is a direct

consequence of the sector's high R&D expenditure and the critical role of

analytical data in regulatory submissions. The complexity of modern

therapeutics, particularly biologics, requires a multi-attribute analytical

approach that leverages a suite of instruments to characterize size variants,

post-translational modifications, and higher-order structure. This

"analytical toolbox" approach, combined with the stringent

requirement for data integrity and compliance with regulatory standards (e.g.,

FDA 21 CFR Part 11), makes the pharmaceutical industry the most demanding and

high-value customer for analytical instrument manufacturers. The continuous

innovation in drug modalities ensures that the demand for more sophisticated

analytical solutions will persist.

The Pharmaceutical & Biotechnology Companies segment is

expected to hold the largest market share in 2025.

By end-user, the market is divided into

Pharmaceutical & Biotechnology Companies, Academic & Research

Institutes, Environmental Agencies, and Industrial & Manufacturing

Facilities. The Pharmaceutical & Biotechnology Companies segment is the

largest end-user. This is due to their substantial capital investment in

laboratory infrastructure, the continuous need for instruments in both R&D

and production environments, and the high throughput requirements of commercial

manufacturing.

The following segments

are part of an in-depth analysis of the global Analytical Instruments Market:

|

Market Segments |

|

|

By Type |

●

Chromatography ●

Spectroscopy ●

Molecular Analysis ●

Mass Spectrometry ●

Others |

|

By Application |

●

Life Science &

Pharma ●

Environmental

Testing ●

Food & Beverage ●

Petrochemicals ●

Others |

|

By End-user |

●

Pharmaceutical &

Biotechnology Companies ●

Academic &

Research Institutes ●

Environmental

Agencies ●

Industrial &

Manufacturing Facilities ●

Others |

Analytical Instruments Market Share Analysis by Region

The North America region is anticipated to hold the largest

portion of the Analytical Instruments Market globally throughout the forecast

period.

North America is the leading segment, holding a

dominant share. This leadership is anchored by the strong presence of major

pharmaceutical and biotechnology companies, world-renowned academic

and research institutions, and robust regulatory agencies like the FDA and EPA.

High healthcare and R&D spending, early adoption of advanced technologies,

and a mature industrial base collectively contribute to the region's market

supremacy.

The dominance of North America, particularly the

United States, in the analytical instruments market is underpinned by a

powerful innovation ecosystem. The region is home to the headquarters of most

leading instrument manufacturers and a dense network of biopharma giants and

agile startups. The NIH's substantial funding for basic and clinical research

fuels demand in academic and government labs, while the FDA's rigorous

regulatory framework mandates the use of high-quality analytical data for drug

and device approval, creating a non-negotiable market demand. Furthermore, high

awareness and investment in environmental monitoring and food safety standards

ensure a steady demand from public and private sectors outside of life

sciences, creating a diversified and resilient market base.

Analytical Instruments Market Competition Landscape Analysis

The global analytical instruments market is highly

competitive and fragmented, featuring a mix of well-established multinational

corporations and specialized niche players. Competition is intense and based on

factors such as technological innovation, product performance (sensitivity,

resolution, speed), reliability, service support, and price. Key strategies

observed in the market include continuous investment in R&D to launch

next-generation products with enhanced capabilities, strategic acquisitions to

broaden product portfolios and geographic reach, and a strong focus on

developing integrated software solutions and services to enhance the customer

value proposition. The trend towards laboratory automation and digitalization

is also pushing companies to form partnerships and develop compatible systems.

Global Analytical Instruments Market Recent Developments

News:

- In January 2025, Thermo Fisher Scientific Inc.

launched a new high-resolution mass spectrometer with integrated AI-driven

software for automated data analysis in proteomics research.

- In November 2024, Agilent Technologies Inc.

acquired a specialized company in the field of process analytical

technology (PAT) to strengthen its offerings for real-time monitoring in

pharmaceutical manufacturing.

- In September 2024, Shimadzu Corporation introduced

a new series of compact, portable gas chromatographs aimed at the

environmental monitoring and field testing market.

- In July 2024, Waters Corporation announced a long-term partnership

with a major pharmaceutical company to provide integrated chromatography

and mass spectrometry solutions for their global quality control labs.

The Global Analytical

Instruments Market Is Dominated by a Few Large Companies, such as

●

Thermo Fisher

Scientific Inc.

●

Agilent Technologies,

Inc.

●

Danaher Corporation

●

Waters Corporation

●

Shimadzu Corporation

●

PerkinElmer, Inc.

●

Bruker Corporation

●

Merck KGaA

●

JEOL Ltd.

●

Hitachi High-Tech

Corporation

●

Mettler-Toledo

International Inc.

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global Analytical

Instruments Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Analytical Instruments Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Analytical

Instruments Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Type of Global Analytical

Instruments Market

1.3.2.Application of Global Analytical

Instruments Market

1.3.3.End-user of Global Analytical

Instruments Market

1.3.4.Region of Global Analytical

Instruments Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5. Pricing Analysis

2.6.

Key

Developments

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Analytical Instruments Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Analytical Instruments Market Estimates

& Forecast Trend Analysis, by Type

4.1.

Global

Analytical Instruments Market Revenue (US$ Bn) Estimates and Forecasts, by Type,

2020 - 2033

4.1.1.Chromatography

4.1.2.Spectroscopy

4.1.3.Molecular Analysis

4.1.4.Mass Spectrometry

4.1.5.Others

5. Global

Analytical Instruments Market Estimates

& Forecast Trend Analysis, by Application

5.1.

Global

Analytical Instruments Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

5.1.1.Life Science & Pharma

5.1.2.Environmental Testing

5.1.3.Food & Beverage

5.1.4.Petrochemicals

5.1.5.Others

6. Global

Analytical Instruments Market Estimates

& Forecast Trend Analysis, by End-user

6.1.

Global

Analytical Instruments Market Revenue (US$ Bn) Estimates and Forecasts, by End-user,

2020 - 2033

6.1.1.Pharmaceutical &

Biotechnology Companies

6.1.2.Academic & Research

Institutes

6.1.3.Environmental Agencies

6.1.4.Industrial &

Manufacturing Facilities

6.1.5.Others

7. Global

Analytical Instruments Market Estimates

& Forecast Trend Analysis, by Region

7.1.

Global

Analytical Instruments Market Revenue (US$ Bn) Estimates and Forecasts, by Region,

2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Analytical

Instruments Market: Estimates &

Forecast Trend Analysis

8.1. North America Analytical

Instruments Market Assessments & Key Findings

8.1.1.North America Analytical

Instruments Market Introduction

8.1.2.North America Analytical

Instruments Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Type

8.1.2.2.

By Application

8.1.2.3.

By End-user

8.1.2.4. By Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Analytical

Instruments Market: Estimates &

Forecast Trend Analysis

9.1. Europe Analytical

Instruments Market Assessments & Key Findings

9.1.1.Europe Analytical

Instruments Market Introduction

9.1.2.Europe Analytical

Instruments Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Type

9.1.2.2.

By Application

9.1.2.3.

By End-user

9.1.2.4. By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Analytical

Instruments Market: Estimates &

Forecast Trend Analysis

10.1. Asia Pacific Market

Assessments & Key Findings

10.1.1.

Asia

Pacific Analytical Instruments Market Introduction

10.1.2.

Asia

Pacific Analytical Instruments Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1.

By Type

10.1.2.2.

By Application

10.1.2.3.

By End-user

10.1.2.4. By Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Analytical

Instruments Market: Estimates &

Forecast Trend Analysis

11.1. Middle East & Africa

Market Assessments & Key Findings

11.1.1. Middle

East & Africa

Analytical Instruments Market Introduction

11.1.2. Middle

East & Africa

Analytical Instruments Market Size Estimates and Forecast (US$ Billion) (2020 -

2033)

11.1.2.1.

By Type

11.1.2.2.

By Application

11.1.2.3.

By End-user

11.1.2.4. By Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Analytical Instruments Market:

Estimates & Forecast Trend Analysis

12.1. Latin America Market

Assessments & Key Findings

12.1.1. Latin America Analytical

Instruments Market Introduction

12.1.2. Latin America Analytical

Instruments Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Type

12.1.2.2.

By Application

12.1.2.3.

By End-user

12.1.2.4. By Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13.

Country

Wise Market: Introduction

14.

Competition

Landscape

14.1. Global Analytical

Instruments Market Product Mapping

14.2. Global Analytical

Instruments Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3. Global Analytical

Instruments Market Tier Structure Analysis

14.4. Global Analytical

Instruments Market Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

Thermo Fisher Scientific Inc.

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2.

Agilent Technologies, Inc.

15.3.

Danaher Corporation

15.4.

Waters Corporation

15.5.

Shimadzu Corporation

15.6.

PerkinElmer, Inc.

15.7.

Bruker Corporation

15.8.

Merck KGaA

15.9.

JEOL Ltd.

15.10.

Hitachi High-Tech Corporation

15.11.

Mettler-Toledo International Inc.

15.12.

Other Prominent Players

16. Research

Methodology

16.1. External Transportations /

Databases

16.2. Internal Proprietary

Database

16.3. Primary Research

16.4. Secondary Research

16.5. Assumptions

16.6. Limitations

16.7. Report FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables