Artificial Jewelry Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product Type (Necklaces, Earrings, Rings, Bracelets & Bangles, Others), By Material (Gold-Plated, Silver-Plated, Brass, Stainless Steel, Beaded, Others), By Distribution Channel (Offline [Hypermarkets/Supermarkets, Specialty Stores, Branded Outlets], Online) And Geography

2025-12-05

Consumer Products

Jaya Bundele (Research Analyst)

Description

Artificial Jewelry Market Overview

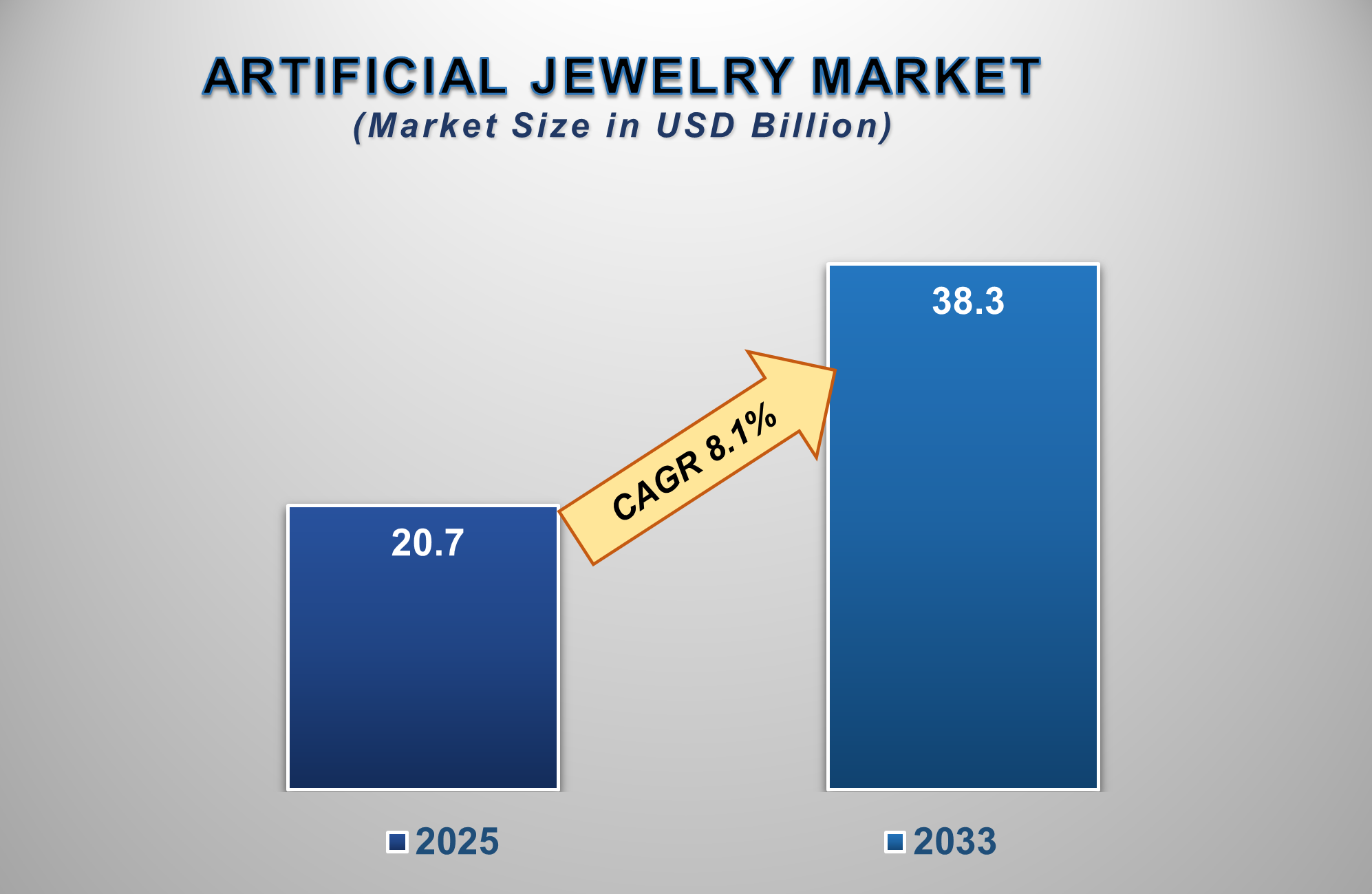

The Artificial Jewelry Market is poised for a period of robust and dynamic growth from 2025 to 2033, driven by rapidly changing fashion trends, rising disposable incomes in emerging economies, and the growing acceptance of fashion jewelry as a daily wear accessory. The market is projected to be valued at approximately USD 20.7 billion in 2025 and is forecasted to reach nearly USD 38.3 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 8.1% during this period.

Artificial jewelry, also known as fashion or

imitation jewelry, encompasses a wide range of non-precious accessory items designed for aesthetic appeal and affordability. The

market's expansion is underpinned by the influence of social media and fashion

influencers, which accelerates the adoption of new styles and encourages

frequent purchases. Furthermore, the increasing working-women population,

coupled with their desire for accessorizing different outfits for various

occasions, is a significant growth factor. Technological advancements in

manufacturing, such as electroplating and the use of high-quality alloys and

synthetic stones that closely mimic real jewelry, are also enhancing product

appeal and durability. North America and Europe currently hold significant

market shares due to high fashion consciousness, while the Asia-Pacific region

is anticipated to be the fastest-growing market, fueled by its large youth population, urbanization, and growing

middle class.

Artificial Jewelry Market Drivers and Opportunities

Rapid Fashion,

Cyclability, and Affordability are the Primary

Market Drivers

The fast-paced nature of the fashion industry is

the most significant driver of the artificial jewelry market. Unlike fine

jewelry, which is often considered a long-term investment, artificial jewelry

is purchased to complement transient fashion trends. The low cost per piece

allows consumers to experiment with styles, build extensive collections, and

frequently update their accessories without a significant financial burden. The

rise of "fast fashion" retailers, who quickly replicate runway trends

at affordable prices, creates a direct and continuous demand for complementary

fashion jewelry. This cyclical nature of fashion, combined with the economic

accessibility of these products, ensures a consistent and high-volume demand,

driving market growth.

Rising Disposable Income and Growing

Working-Women Population are Driving Widespread Adoption

The increasing disposable income, particularly

in developing nations across Asia-Pacific and Latin America, is a major

catalyst for market expansion. As consumers have more spending power, a larger

portion is allocated to non-essential and lifestyle products, including fashion

accessories. Concurrently, the global rise in the number of working women has

created a substantial consumer base that seeks stylish, professional, and

versatile jewelry for daily wear and corporate settings. These demographic groups'

view of artificial

jewelry is not just as an adornment but as an

integral component of their personal and professional identity, fueling repeated purchases and driving the market's growth

trajectory.

Product Innovation and the E-commerce Boom

Present Significant Opportunities

The development of innovative designs and the

explosive growth of online retail are creating significant growth frontiers for

the artificial jewelry market. Key opportunities lie in the use of new

materials like titanium plating, tungsten carbide, and high-quality resin,

which offer superior scratch resistance and longevity. The trend towards

personalized and customized jewelry, enabled by advanced manufacturing

techniques like 3D printing, represents a major opportunity. Furthermore, the

dominance of e-commerce platforms is revolutionizing the market. Online

channels offer a vast selection, competitive pricing, and the convenience of

home shopping, which is particularly appealing to the younger demographic. For

manufacturers, investing in an omnichannel presence, leveraging social media

marketing, and creating engaging online content are key strategies to capture

this rapidly expanding digital segment.

Artificial Jewelry Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 20.7 Billion |

|

Market Forecast in 2033 |

USD 38.3 Billion |

|

CAGR % 2025-2033 |

8.1% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Product Type ●

By Material ●

By Distribution

Channel |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Artificial Jewelry Market

Report Segmentation Analysis

The global Artificial Jewelry

Market industry analysis is segmented by Product Type, by Material, by

Distribution Channel, and by Region.

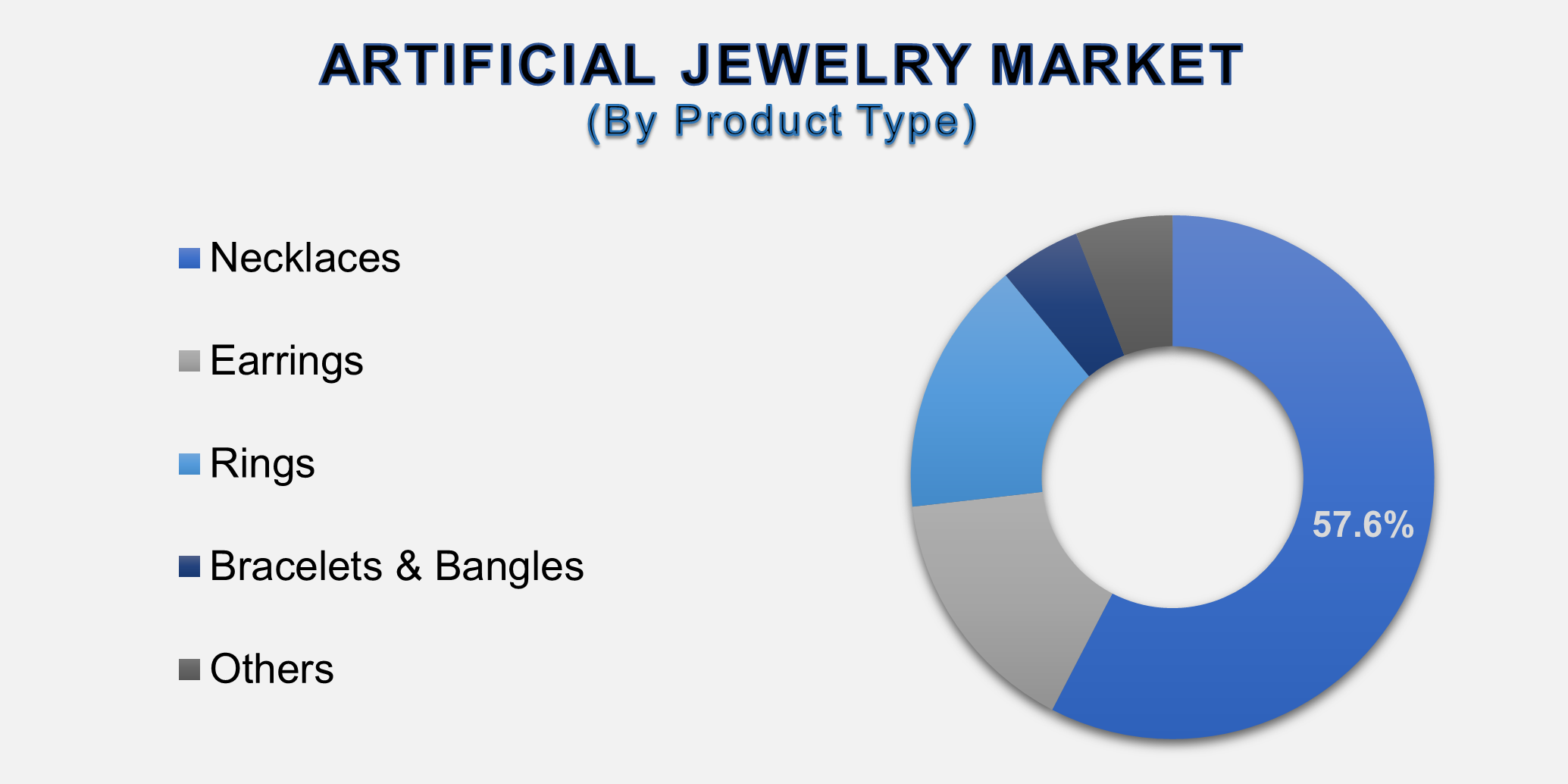

The Necklaces segment is

anticipated to command a significant market share in 2025.

The Product Type segment is categorized into

Necklaces, Earrings, Rings, Bracelets & Bangles, and Others. Necklaces

often serve as a statement piece in an ensemble, making them a highly

sought-after category. The versatility of necklaces, ranging from delicate

chains to bold, chunky designs, allows them to cater to a wide array of fashion

sensibilities and occasions. The constant innovation in pendants, chains, and

materials keeps this segment fresh and appealing. Its prominence on the upper

body, making it a focal point of any outfit, ensures that the necklace

segment captures a substantial portion of consumer spending and holds a leading

position in the market.

The Gold-Plated material segment is projected to

hold the largest market share.

The Material segment is divided into Gold-Plated,

Silver-Plated, Brass, Stainless Steel, Beaded, and Others. The dominance of

gold-plated jewelry is driven by its perennial appeal and its ability to offer

the luxurious look of real gold at a fraction of the cost. Gold is a timeless

metal associated with prestige and elegance across numerous cultures. Modern

electroplating techniques have improved the durability and tarnish resistance of gold-plated items, enhancing their value proposition.

As consumers seek affordable luxury and versatile pieces that can be worn daily

or on special occasions, gold-plated jewelry remains the most popular and

dominant material choice globally.

The Offline distribution channel segment is

projected to maintain its dominance, though Online is growing rapidly.

The Distribution Channel is split into Offline

(Hypermarkets/Supermarkets, Specialty Stores, Branded Outlets) and Online. The

Offline segment's leading position is attributed to the tactile nature of the

jewelry shopping experience. Consumers often prefer to see, touch, and try on

jewelry to assess its quality, finish, and how it looks on them before

purchasing. Specialty stores and branded outlets offer a curated experience,

expert advice, and immediate gratification. While the online

channel is experiencing explosive growth, the established network of physical

retail stores, malls, and kiosks continues to be the primary point of sale,

leveraging the sensory and instant aspects of the purchase decision.

The following segments are part of an in-depth analysis of

the global Artificial Jewelry Market:

|

Market

Segments |

|

|

By Product

Type |

●

Necklaces ●

Earrings ●

Rings ●

Bracelets &

Bangles ●

Others |

|

By Material |

●

Gold-Plated ●

Silver-Plated ●

Brass ●

Stainless Steel ●

Beaded ●

Others |

|

By Distribution Channel |

●

Offline Channel ●

Online Channel |

Artificial Jewelry Market

Share Analysis by Region

The Asia Pacific region is anticipated to hold

the largest portion of the Artificial Jewelry Market globally

throughout the forecast period.

Asia-Pacific's dominance is fuelled by its

massive population, deep-rooted cultural affinity for jewelry, and rapidly

growing economies. Countries like India and China have a long tradition of

adornment, and with rising disposable incomes, consumers are increasingly

purchasing jewelry for fashion rather than just for investment. The region is

also a global manufacturing hub, ensuring a steady and cost-effective supply.

The burgeoning e-commerce sector, combined with a young, fashion-conscious

demographic, makes Asia-Pacific the epicenter of current and future growth for

the artificial jewelry market.

The region benefits from a strong presence of

local artisans as well as large-scale manufacturers, creating a diverse product

range that caters to both traditional and contemporary tastes. Festivals,

weddings, and other cultural celebrations drive significant seasonal demand

spikes. Furthermore, the penetration of smartphones and internet connectivity

is bringing a vast rural consumer base into the market through online channels,

further accelerating regional market dominance.

Artificial Jewelry Market

Competition Landscape Analysis

The global artificial jewelry

market is highly fragmented and competitive, featuring a mix of international

brands, regional players, and numerous local artisans. Competition is intense

and based on design innovation, price, brand image, and distribution network

reach. Key strategies include frequent new collection launches to align with

fashion trends, celebrity endorsements and collaborations, investment in

marketing through social media influencers, and expansion of retail presence

both online and offline. The ability to quickly replicate high-end designer

trends at mass-market prices is a critical success factor in this dynamic

market.

Global Artificial Jewelry

Market Recent Developments News:

- In January

2025, Pandora announced a new collection of lab-created gemstone

fashion jewelry, aiming to capture the market for affordable, sustainable,

and sparkly accessories.

- In November 2024, a

major fast-fashion retailer, H&M, launched a collaboration with a

celebrity stylist for a limited-edition artificial jewelry line, which

sold out online within hours.

- In September

2024, Mia by Tanishq, a brand from the Tata Group, expanded its

retail footprint in India, focusing on trendy and affordable artificial

jewelry for young women.

- In July 2024, Amazon

India reported a significant surge in sales of artificial jewelry during

its Prime Day sale, highlighting the growing dominance of the online

channel in key markets.

The Global Artificial

Jewelry Market Is Dominated by a Few Large Companies, such as

●

Pandora A/S

●

Swarovski AG

●

H&M Group (Hennes & Mauritz AB)

●

Zara (Inditex)

●

Accessorize (Monsoon

Accessorize Ltd.)

●

Mia by Tanishq (Titan

Company Limited)

●

Stylophile

●

BaubleBar Inc.

●

Lovisa Holdings Ltd.

●

The Colibri Company

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Artificial Jewelry

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Artificial Jewelry Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Artificial Jewelry

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product Type of Global Artificial

Jewelry Market

1.3.2.Material Type of Global Artificial

Jewelry Market

1.3.3.Distribution Channel of Global

Artificial Jewelry Market

1.3.4.Region of Global Artificial

Jewelry Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Technological

Advancements

2.6.

Key

Developments

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Artificial Jewelry Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Artificial Jewelry Market Estimates

& Forecast Trend Analysis, by Product Type

4.1.

Global

Artificial Jewelry Market Revenue (US$ Bn) Estimates and Forecasts, by Product

Type, 2020 - 2033

4.1.1.Necklaces

4.1.2.Earrings

4.1.3.Rings

4.1.4.Bracelets & Bangles

4.1.5.Others

5. Global

Artificial Jewelry Market Estimates

& Forecast Trend Analysis, by Material Type

5.1.

Global

Artificial Jewelry Market Revenue (US$ Bn) Estimates and Forecasts, by Material

Type, 2020 - 2033

5.1.1.Gold-Plated

5.1.2.Silver-Plated

5.1.3.Brass

5.1.4.Stainless Steel

5.1.5.Beaded

5.1.6.Others

6. Global

Artificial Jewelry Market Estimates

& Forecast Trend Analysis, by Distribution Channel

6.1.

Global

Artificial Jewelry Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution

Channel 2020 - 2033

6.1.1.Offline Channel

6.1.2.Online Channel

7. Global

Artificial Jewelry Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Artificial Jewelry Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020

- 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Artificial

Jewelry Market: Estimates &

Forecast Trend Analysis

8.1. North America Artificial Jewelry

Market Assessments & Key Findings

8.1.1.North America Artificial Jewelry

Market Introduction

8.1.2.North America Artificial Jewelry

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Product Type

8.1.2.2.

By Material Type

8.1.2.3.

By Distribution Channel

8.1.2.4. By Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Artificial

Jewelry Market: Estimates &

Forecast Trend Analysis

9.1. Europe Artificial Jewelry

Market Assessments & Key Findings

9.1.1.Europe Artificial Jewelry

Market Introduction

9.1.2.Europe Artificial Jewelry

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Product Type

9.1.2.2.

By Material Type

9.1.2.3.

By Distribution Channel

9.1.2.4. By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Artificial

Jewelry Market: Estimates &

Forecast Trend Analysis

10.1. Asia Pacific Market

Assessments & Key Findings

10.1.1.

Asia

Pacific Artificial Jewelry Market Introduction

10.1.2.

Asia

Pacific Artificial Jewelry Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

10.1.2.1.

By Product Type

10.1.2.2.

By Material Type

10.1.2.3.

By Distribution Channel

10.1.2.4. By Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Artificial

Jewelry Market: Estimates &

Forecast Trend Analysis

11.1. Middle East & Africa

Market Assessments & Key Findings

11.1.1. Middle

East & Africa

Artificial Jewelry Market Introduction

11.1.2. Middle

East & Africa

Artificial Jewelry Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Product Type

11.1.2.2.

By Material Type

11.1.2.3.

By Distribution Channel

11.1.2.4. By Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Artificial Jewelry Market: Estimates

& Forecast Trend Analysis

12.1. Latin America Market

Assessments & Key Findings

12.1.1. Latin America Artificial Jewelry

Market Introduction

12.1.2. Latin America Artificial Jewelry

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Product Type

12.1.2.2.

By Material Type

12.1.2.3.

By Distribution Channel

12.1.2.4. By Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13.

Country

Wise Market: Introduction

14.

Competition

Landscape

14.1. Global Artificial Jewelry

Market Product Mapping

14.2. Global Artificial Jewelry

Market Concentration Analysis, by Leading Players / Innovators / Emerging

Players / New Entrants

14.3. Global Artificial Jewelry

Market Tier Structure Analysis

14.4. Global Artificial Jewelry

Market Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

Pandora A/S

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2.

Swarovski AG

15.3.

H&M Group (Hennes & Mauritz AB)

15.4.

Zara (Inditex)

15.5.

Accessorize (Monsoon Accessorize Ltd.)

15.6.

Mia by Tanishq (Titan Company Limited)

15.7.

Stylophile

15.8.

BaubleBar Inc.

15.9.

Lovisa Holdings Ltd.

15.10.

The Colibri Company

15.11.

Other Prominent Players

16. Research

Methodology

16.1. External Transportations /

Databases

16.2. Internal Proprietary

Database

16.3. Primary Research

16.4. Secondary Research

16.5. Assumptions

16.6. Limitations

16.7. Report FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables