Athletic Footwear Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Product Type (Running Shoes, Sports Shoes, Aerobic Shoes, Walking Shoes, and others); By Demographics (Men, Women, Kids); By Distribution Channel (Online, Offline) and Geography

2025-10-27

Consumer Products

Jaya Bundele (Research Analyst)

Description

Athletic Footwear Market Overview

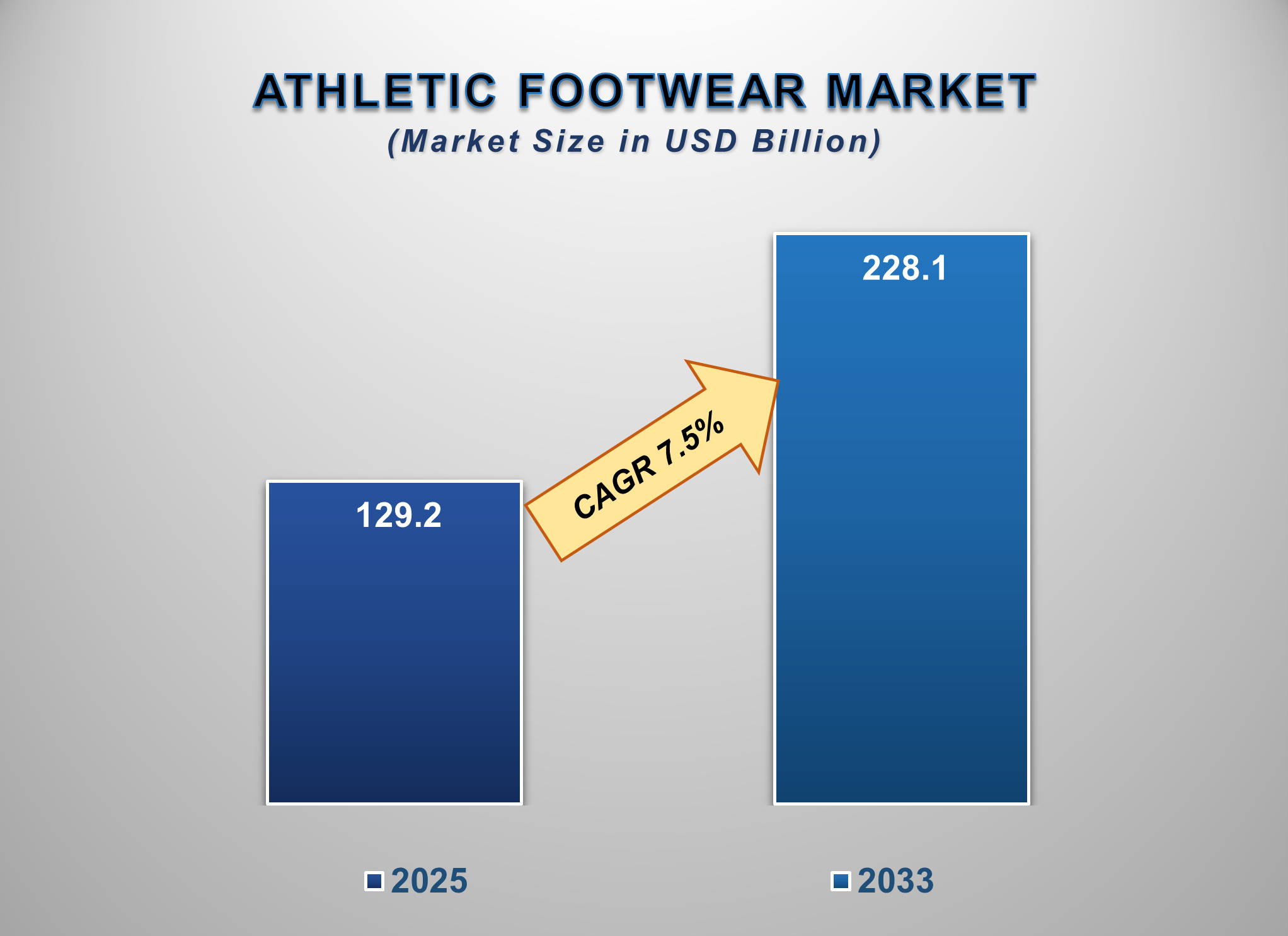

The athletic footwear market size is projected to witness substantial growth from 2025 to 2033, propelled by the rising global emphasis on health and fitness, the influence of athleisure fashion trends, and continuous innovation in material science and design. Valued at approximately USD 129.2 billion in 2025, the market is expected to surge to USD 228.1 billion by 2033, reflecting a steady compound annual growth rate (CAGR) of 7.5% over the forecast period.

The athletic footwear market is

undergoing a dynamic evolution, driven by the blurring lines between

performance sportswear and casual fashion. The "athleisure" trend has

become a dominant force, with consumers seeking footwear that offers both

comfort for all-day wear and technical performance for athletic activities. Key

growth areas include sustainable product lines, smart footwear with embedded

sensors, and shoes tailored for specific activities like hiking and

weightlifting.

The market is further benefiting

from the rapid expansion of e-commerce and digital marketing, which allows

brands to engage directly with consumers and offer personalized shopping

experiences. Continuous R&D investments are leading to advancements in

cushioning, energy return, and sustainability, thereby enhancing product appeal

and driving replacement cycles. North America and Asia-Pacific are pivotal

markets, with the latter exhibiting the highest growth rate due to a growing

middle class and increasing health consciousness.

Athletic Footwear Market

Drivers and Opportunities

The Pervasive Athleisure Trend and Fashion Convergence

The

integration of athletic footwear into everyday wardrobes is a primary driver

for the market. No longer confined to the gym, performance-inspired sneakers

have become a staple in casual and even business-casual attire. This shift is

fueled by consumer demand for comfort, versatility, and style. Collaborations

between major athletic brands and high-fashion designers or celebrities have

created cultural phenomena, driving hype, brand desirability, and premium

pricing. This trend is creating a sustained and diversified demand, encouraging

consumers to own multiple pairs of athletic shoes for different occasions.

Rising Health Consciousness and Participation in Sports &

Fitness

The

global post-pandemic focus on health and wellness is significantly driving the

adoption of athletic footwear. Increased participation in running, gym

workouts, hiking, and other recreational sports has created a robust demand for

specialized footwear that provides support, injury prevention, and performance

enhancement. Government initiatives promoting active lifestyles, coupled with

the growing popularity of fitness challenges and events, are providing a strong

impetus for the market. Consumers are increasingly knowledgeable and seek

technical features, making innovation in biomechanics and material science a

key competitive differentiator.

Opportunity for the

Athletic Footwear Market

Expansion of Sustainable and Direct-to-Consumer (DTC) Models

A

significant opportunity lies in the growing consumer demand for sustainable

products and the efficiency of DTC channels. Brands are investing heavily in

developing footwear using recycled materials (e.g., polyester, rubber),

bio-based alternatives, and circular business models that include repair and

recycling programs. This resonates strongly with environmentally conscious

consumers. Simultaneously, the DTC model, through brand-owned websites and

apps, allows companies to capture higher margins, control brand narrative, and

gather valuable first-party data on consumer preferences. Brands that can

successfully integrate sustainability into their core identity and leverage DTC

engagement are poised to capture a substantial share of the evolving market.

Athletic Footwear Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 129.2 Billion |

|

Market Forecast in 2033 |

USD 228.1 Billion |

|

CAGR % 2025-2033 |

7.2% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production, growth factors, and more |

|

Segments Covered |

●

By Product Type ●

By Demographics ●

By Distribution Channel |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Netherland 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19)

Egypt 20) South Africa |

Athletic Footwear Market

Report Segmentation Analysis

The global Athletic Footwear

Market industry analysis is segmented by product type, by demographics, by

distribution channel, and by region.

The Dominance of the Running Shoes Segment

The running shoes segment is a foundational pillar and revenue leader of the athletic footwear market because running is one of the most accessible and popular forms of exercise worldwide. Its dominance is secured by two key factors. First, it caters to a massive and diverse user base, from casual joggers to competitive marathoners, each requiring specific features like cushioning, stability, and lightweight construction. This creates a high-volume, continuous demand. Second, running shoes serve as the primary platform for technological innovation. Brands consistently debut their latest advancements in midsole foam (e.g., Nike Air, Adidas Boost), carbon-fiber plating, and sustainable materials in this segment. The high rate of innovation drives frequent replacement cycles as consumers seek the latest performance benefits, ensuring this segment's continued profitability and major market share.

The Commanding Share of the Men's Demographics Segment

The men's demographic segment commands a major market share due to

historically higher participation rates in sports and a long-standing cultural

association with sneakerhead culture and collecting. This dominance is driven

by established spending power and a deep engagement with both performance and

lifestyle aspects of athletic footwear. Men have been the primary target for

flagship basketball, running, and training shoe launches for decades, creating

strong brand loyalty. Furthermore, the resale market for limited-edition

sneakers is largely driven by male consumers, which amplifies hype and primary

market demand. While the women's segment is growing rapidly, the men's segment

continues to lead in overall volume and value due to its entrenched position and

diverse consumption drivers.

The Leadership of the Offline Distribution Channel Segment

The offline distribution channel segment, which includes specialty

sportswear stores, department stores, and brand-owned retail outlets, remains

the largest channel for athletic footwear. This dominance is attributed to the

critical importance of the tactile shopping experience. Consumers highly value

the ability to try on shoes for fit, comfort, and feel—factors that are

difficult to assess online. Brand-owned flagship stores and experience centers

also serve as powerful marketing tools, building brand equity and allowing for

direct consumer engagement. While online growth is explosive, the offline

channel's role in providing expert advice, instant gratification, and an

immersive brand experience secures its leadership position, especially for

high-consideration purchases.

The following segments are part of an in-depth analysis of the global

Athletic Footwear Market:

|

Market Segments |

|

|

By Product Type |

●

Running Shoes ●

Sports Shoes

(Basketball, Soccer, etc.) ●

Aerobic & Gym

Training Shoes ●

Walking Shoes ●

Others (Hiking,

etc.) |

|

By Demographics

|

●

Men ●

Women ●

Kids |

|

By Distribution Channel |

●

Online Channel ●

Offline Channel |

Athletic Footwear Market

Share Analysis by Region

The Asia-Pacific Region is Expected to

Dominate the Global Athletic Footwear Market During the Forecast Period

Asia-Pacific is anticipated to be the dominant and

fastest-growing region in the global Athletic Footwear Market. This leadership

is driven by a massive population, a rapidly expanding middle class with

increasing disposable income, and a growing cultural emphasis on health and

fitness. Countries like China, India, and Vietnam are both major consumption

hubs and production centers, hosting the manufacturing bases for nearly all

global brands. The deep penetration of e-commerce and mobile payment systems

further facilitates market growth. The region's young demographic, which is

highly influenced by global fashion and sport trends, creates a sustained and

powerful demand pull, securing Asia-Pacific's leading position.

The Chinese

athletic footwear market experienced a volatile but ultimately growth-positive

trajectory from 2021 to 2023, defined by a post-pandemic surge, a COVID-induced

contraction, and a strong recovery.

In 2021, the

market saw a robust rebound with unit sales increasing by an estimated 15-18%.

This growth was fueled by a national health and wellness boom, where a newfound

emphasis on fitness post-lockdowns drove demand for running and training shoes.

Concurrently, an "outdoor craze" for activities like camping and

hiking surged, boosting sales of specialized footwear. The powerful

"Guochao" (national trend) movement also propelled domestic brands

like Li-Ning and Anta to new heights, as consumers increasingly favored local

brands over international ones.

This momentum

was interrupted in 2022, when strict "zero-COVID" policies triggered

widespread lockdowns, causing an estimated 5-8% decline in unit sales. The

physical retail sector, a critical sales channel, was severely hampered. While

consumer demand remained, the ability to fulfill it was crippled by shuttered

stores and major supply chain disruptions, delaying product launches and

creating inventory imbalances.

By 2023, the market staged a strong recovery with unit sales growing approximately 10-12%. The full reopening of the economy unleashed significant pent-up demand. A renewed focus on sports participation, supported by government initiatives and marquee events, further accelerated growth. Domestic brands continued to solidify their gains, capitalizing on strong national sentiment and deep consumer connections. This three-year period cemented China's status as a dynamic and resilient engine for the global athletic footwear industry.

Global Athletic Footwear Market Recent

Developments News:

- In January 2025, Nike, Inc. launched its

next-generation Alphafly 3 racing shoe featuring a new, more responsive

ZoomX foam formulation and a refined carbon fiber plate for elite

marathoners.

- In February 2025, Adidas AG announced a new

sustainability target to use 100% recycled polyester in all its products

by 2026, starting with its bestselling Ultraboost and Stan Smith lines.

- In March 2025, On Running (On Holding AG) opened

its new flagship "CloudHQ" experience store in New York City,

featuring a running treadmill lab for gait analysis and product

personalization.

- In April 2025, A consortium led by L Catterton

acquired a significant minority stake in Hoka One One (Deckers Brands),

highlighting the strong investor confidence in the performance running

category.

The Global Athletic Footwear Market is

dominated by a few large companies, such as

●

Nike, Inc.

●

Adidas AG

●

PUMA SE

●

ASICS Corporation

●

Skechers USA, Inc.

●

Under Armour, Inc.

●

New Balance Athletics,

Inc.

●

VF Corporation (Vans,

The North Face)

●

On Holding AG

●

Anta Sports Products

Ltd.

●

Li Ning Company

Limited

●

Deckers Brands (Hoka

One One, UGG)

●

Mizuno Corporation

●

Wolverine World Wide,

Inc. (Saucony, Merrell)

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

- Global Athletic Footwear Market Introduction and Market Overview

- Objectives of the Study

- Global Athletic Footwear Market Scope and Market Estimation

- Global Athletic Footwear Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Athletic Footwear Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

- Market Segmentation

- Product Type of Global Athletic Footwear Market

- Demographic of Global Athletic Footwear Market

- Distribution Channel of Global Athletic Footwear Market

- Region of Global Athletic Footwear Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Athletic Footwear Market

- Key Product/Brand Analysis

- Pricing Analysis

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Athletic Footwear Market Estimates & Historical Trend Analysis (2020 - 2024)

- Global Athletic Footwear Market Estimates & Forecast Trend Analysis, by Product Type

- Global Athletic Footwear Market Revenue (US$ Bn) Estimates and Forecasts, by Product Type, 2020 - 2033

- Running Shoes

- Sports Shoes (Basketball, Soccer, etc.)

- Aerobic & Gym Training Shoes

- Walking Shoes

- Others (Hiking, etc.)

- Global Athletic Footwear Market Revenue (US$ Bn) Estimates and Forecasts, by Product Type, 2020 - 2033

- Global Athletic Footwear Market Estimates & Forecast Trend Analysis, by Demographic

- Global Athletic Footwear Market Revenue (US$ Bn) Estimates and Forecasts, by Demographic, 2020 - 2033

- Men

- Women

- Kids

- Global Athletic Footwear Market Revenue (US$ Bn) Estimates and Forecasts, by Demographic, 2020 - 2033

- Global Athletic Footwear Market Estimates & Forecast Trend Analysis, by Distribution Channel

- Global Athletic Footwear Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution Channel, 2020 - 2033

- Online Channel

- Offline Channel

- Global Athletic Footwear Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution Channel, 2020 - 2033

- Global Athletic Footwear Market Estimates & Forecast Trend Analysis, by region

- Global Athletic Footwear Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Athletic Footwear Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020 - 2033

- North America Athletic Footwear Market: Estimates & Forecast Trend Analysis

- North America Athletic Footwear Market Assessments & Key Findings

- North America Athletic Footwear Market Introduction

- North America Athletic Footwear Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product Type

- By Demographic

- By Distribution Channel

- By Country

- The U.S.

- Canada

- North America Athletic Footwear Market Assessments & Key Findings

- Europe Athletic Footwear Market: Estimates & Forecast Trend Analysis

- Europe Athletic Footwear Market Assessments & Key Findings

- Europe Athletic Footwear Market Introduction

- Europe Athletic Footwear Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product Type

- By Demographic

- By Distribution Channel

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Netherland

- Rest of Europe

- Europe Athletic Footwear Market Assessments & Key Findings

- Asia Pacific Athletic Footwear Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Athletic Footwear Market Introduction

- Asia Pacific Athletic Footwear Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product Type

- By Demographic

- By Distribution Channel

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Athletic Footwear Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Athletic Footwear Market Introduction

- Middle East & Africa Athletic Footwear Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product Type

- By Demographic

- By Distribution Channel

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Athletic Footwear Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Athletic Footwear Market Introduction

- Latin America Athletic Footwear Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product Type

- By Demographic

- By Distribution Channel

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Athletic Footwear Market Product Type Mapping

- Global Athletic Footwear Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Athletic Footwear Market Tier Structure Analysis

- Global Athletic Footwear Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

- Nike, Inc.

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Type Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Nike, Inc.

* Similar details would be provided for all the players mentioned below

- Adidas AG

- PUMA SE

- ASICS Corporation

- Skechers USA, Inc.

- Under Armour, Inc.

- New Balance Athletics, Inc.

- VF Corporation (Vans, The North Face)

- On Holding AG

- Anta Sports Products Ltd.

- Li Ning Company Limited

- Deckers Brands (Hoka One One, UGG)

- Mizuno Corporation

- Wolverine World Wide, Inc. (Saucony, Merrell)

- Other Prominent Players

- Research Methodology

- External Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables