Automotive Air Compressor Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product Type (Reciprocating, Rotary Screw, Centrifugal), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Electric Vehicles (EVs)), By Application (Air Suspension, Braking Systems, HVAC, Engine Cooling, Others), and Geography

2025-12-19

Automotive & Transportation (Mobility)

Ekta Chaurasia (Team Lead)

Description

Automotive

Air Compressor Market Overview

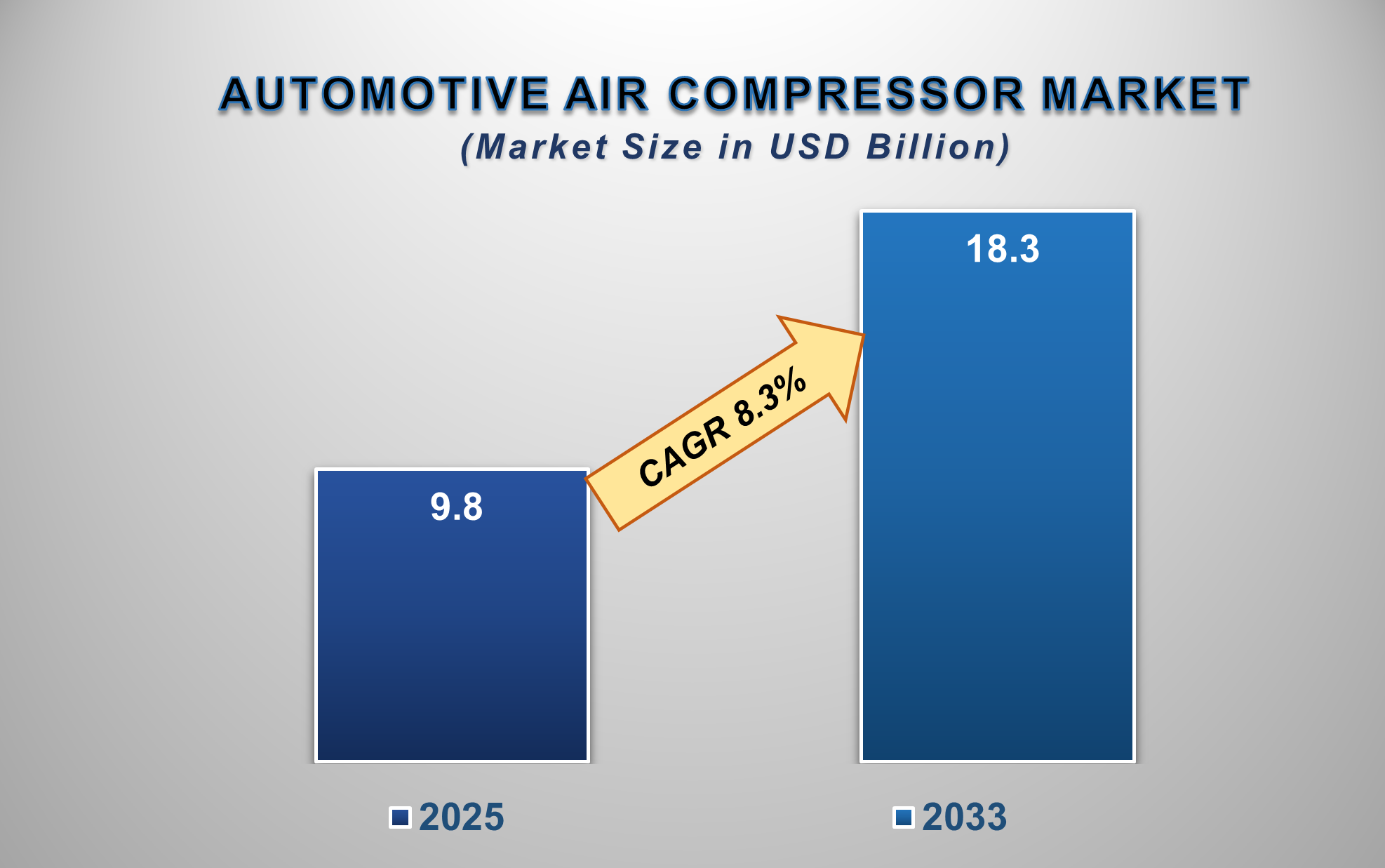

The Automotive Air Compressor Market is set for significant and steady growth from 2025 to 2033, driven by the rising demand for advanced comfort and safety systems, the rapid electrification of vehicle fleets, and the increasing adoption of air suspension in premium and commercial vehicles. The market is projected to be valued at approximately USD 9.8 billion in 2025 and is forecasted to reach nearly USD 18.3 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 8.3% during this period.

An automotive air compressor is a device that converts

power into pressurized air, which is essential for operating various critical

systems in a vehicle, including air brakes, suspension, HVAC, and engine

thermal management. The market's expansion is primarily fueled by the

automotive industry's shift towards enhanced passenger comfort, vehicle

electrification, and stringent safety standards. The growing popularity of air

suspension systems in SUVs and luxury passenger cars for their superior ride

quality and adjustability is a major growth driver.

Furthermore, the transition to electric vehicles (EVs)

necessitates efficient electric-driven compressors for cabin HVAC and battery

thermal management, creating a new, high-value segment. North America and

Europe are significant markets due to the high

penetration of luxury vehicles and advanced commercial fleets, while

Asia-Pacific is the fastest-growing region, propelled by rising vehicle

production and increasing adoption of premium features.

Automotive Air Compressor Market Drivers and

Opportunities

Rising Demand for Vehicle Comfort and Advanced Suspension

Systems:

The pursuit of superior ride quality is fundamentally

reshaping vehicle architectures and directly fueling the air compressor market.

Air suspension systems, which rely on a compressor to inflate and adjust air

springs, offer transformative benefits over traditional steel springs. They

provide a dynamic, adjustable ride height

useful for both aerodynamic efficiency on highways and ground clearance on

rough terrain, along with adaptive damping

that improves handling stability. Crucially, these systems automatically level

the vehicle under varying loads, enhancing safety and comfort. Once exclusive

to luxury sedans and flagship SUVs, this technology is now a key differentiator

in the competitive premium mid-market segment. Consumers increasingly expect a

quiet, smooth, and adaptable ride, making air suspension a sought-after

feature. This rapid democratization of premium comfort features across millions

of new vehicles annually creates sustained, high-volume demand for the

reliable, compact, and efficient air compressors that serve as the heart of

these systems.

Vehicle Electrification and Specialized Thermal Management:

The shift to electric vehicles represents a paradigm shift

for air compressor technology, creating a critical and high-value new

application. Unlike internal combustion engines, EVs lack a significant source

of waste heat for cabin warming, making a dedicated, high-performance electric

compressor essential for efficient heat pump-based HVAC systems. This is vital

for preserving driving range in cold climates. Simultaneously, the sensitive

lithium-ion battery packs require precise thermal management to operate within

an optimal temperature window for maximum performance, fast charging, and

long-term health. Electrically driven scroll or screw compressors are central

to active battery cooling and heating circuits. These EV-specific compressors

are engineering challenges in themselves, demanding exceptional efficiency to

minimize energy draw, high reliability, and quiet operation, all while

integrating with 800V electrical architectures. As EV production scales, the

demand for these advanced thermal management compressors grows proportionally,

making this the market's most dynamic growth frontier.

Stringent Safety Regulations and Commercial Vehicle

Proliferation:

In the commercial vehicle sector, air compressor demand is

underpinned by non-negotiable safety mandates and robust industrial growth. Air

brake systems are legally required on medium-

and heavy-duty trucks and buses globally because of their superior reliability

and stopping power. The compressor is the core component that generates and

maintains the pressurized air for these critical braking systems. Therefore,

every new commercial vehicle produced mandates a heavy-duty air compressor. The

ongoing expansion of global logistics, e-commerce, and infrastructure

development continues to drive the production of freight and construction

vehicles, creating a direct and stable OEM demand. Furthermore, this vast

installed base of commercial vehicles generates a predictable and lucrative

aftermarket. Compressors, as wear items, require periodic maintenance, repair,

and replacement over a vehicle's long service life. This creates a resilient,

recurring revenue stream for manufacturers and distributors, insulating this

segment from cyclical downturns in new vehicle sales.

Automotive Air Compressor Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 9.8 Billion |

|

Market Forecast in 2033 |

USD 18.3 Billion |

|

CAGR % 2025-2033 |

8.3% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Product Type ●

By Vehicle Type ●

By Application |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Automotive Air Compressor Market Report

Segmentation Analysis

The global Automotive Air

Compressor Market industry analysis is segmented by Product Type, Drive Type,

Vehicle Type, Application, and Region.

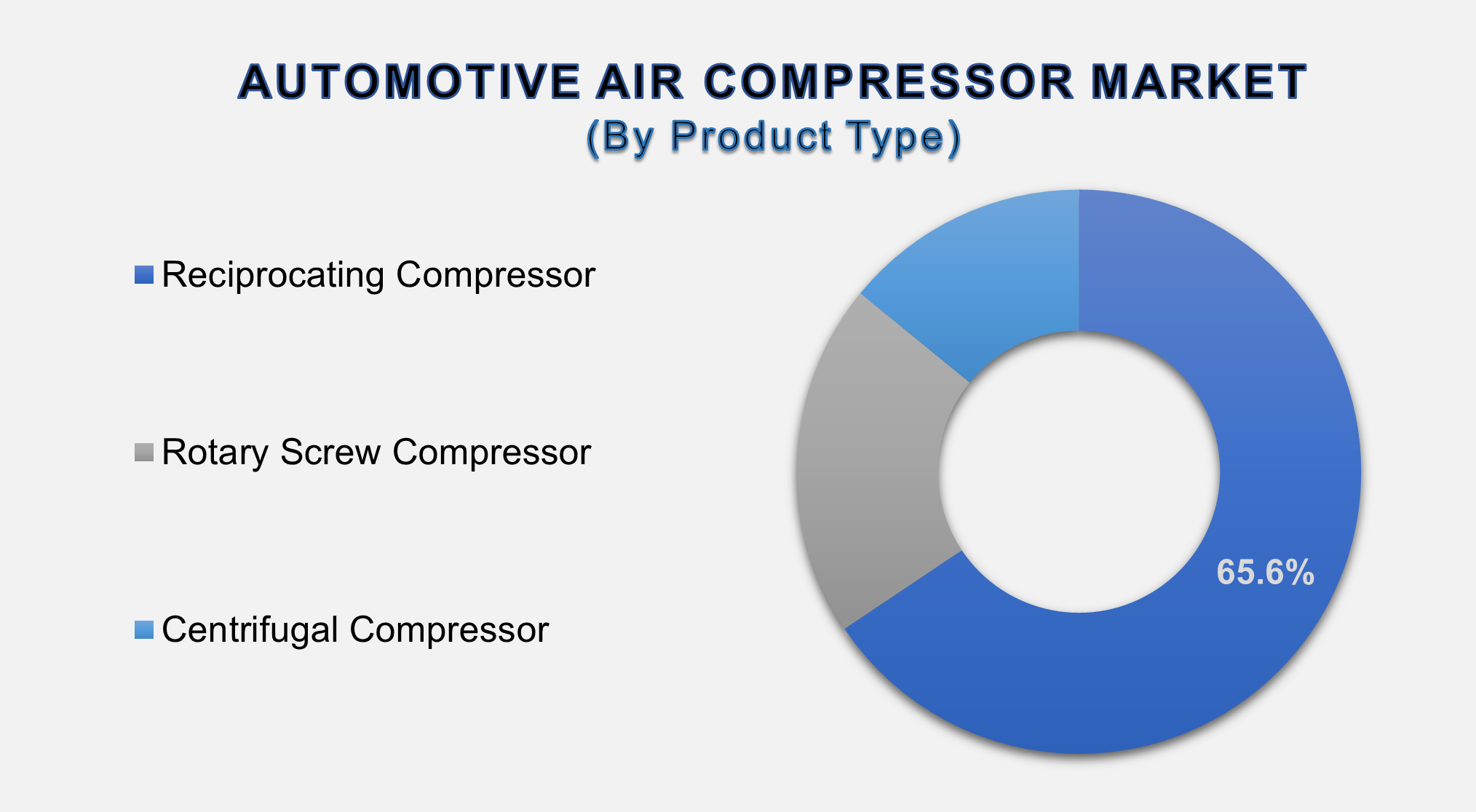

The Reciprocating

Compressor segment is anticipated to hold the largest market share in 2025.

The Product Type segment is categorized into Reciprocating, Rotary Screw, and Centrifugal. Reciprocating compressors dominate due to their robustness, cost-effectiveness, and proven reliability in demanding applications like air brake systems for commercial vehicles. Their simple design and ability to deliver high pressure make them the industry standard for heavy-duty braking and auxiliary air functions. However, rotary screw compressors are gaining traction in air suspension applications for passenger vehicles due to their quieter operation, continuous airflow, and compact size.

The Electric Drive Type

segment is projected to witness the highest growth rate during the forecast

period.

The

Drive Type segment is divided into Electric and Engine-driven. The electric

drive segment is experiencing explosive growth, driven almost entirely by the

electric vehicle revolution. Electric compressors are essential for EV HVAC and

battery cooling, operating independently of the engine. Their growth is further

supported by the trend towards 48V mild-hybrid architectures in conventional

vehicles, which use electric compressors for efficient climate control during

engine start-stop phases.

The Passenger Cars

vehicle type segment holds a dominant market share, while the EV segment shows

phenomenal growth.

The

Vehicle Type segment includes Passenger Cars, LCVs, HCVs, and Electric

Vehicles. Passenger cars lead in volume, attributed to the widespread adoption

of air suspension and advanced HVAC systems. However, the Electric Vehicles

segment, though smaller in absolute volume, is the fastest-growing. Every new

EV platform requires at least one high-voltage electric compressor, creating a

premium, technology-intensive market with significant value addition.

The following segments are

part of an in-depth analysis of the global Automotive Air Compressor Market:

|

Market

Segments |

|

|

By Product

Type |

●

Reciprocating

Compressor ●

Rotary Screw

Compressor ●

Centrifugal

Compressor |

|

By Application |

●

Air Suspension ●

Braking Systems ●

HVAC ●

Engine/Battery

Cooling ●

Others (Tire

Inflation, Pneumatic Tools) |

|

By Vehicle Type |

●

Passenger Cars ●

Light Commercial

Vehicles (LCVs) ●

Heavy Commercial

Vehicles (HCVs) ●

Electric Vehicles

(EVs) |

Automotive

Air Compressor Market Share Analysis by Region

The Asia-Pacific region

is anticipated to hold the largest portion of the Automotive Air Compressor

Market globally throughout the forecast period.

Asia-Pacific's

dominance stems from its undisputed position as the epicenter of global

automotive manufacturing and sales, led by China, Japan, and India. The

region's massive vehicle production volume provides a foundational demand.

China's rapid adoption of electric vehicles, the

largest EV market in the world, directly fuels

demand for advanced electric compressors. Furthermore, the increasing affluence

in the region is driving the uptake of premium features like air suspension in

passenger vehicles. The presence of leading global automotive suppliers and

compressor manufacturers with localized production further solidifies APAC's

leadership.

North

America and Europe remain critical high-value markets. North America's large

commercial vehicle fleet and high penetration of luxury pickups and SUVs with

air suspension drive significant demand. Europe's stringent emissions and

safety regulations, coupled with a strong premium automotive segment and rapid

EV adoption, make it a key region for technological innovation and advanced

compressor adoption.

Automotive Air Compressor Market Competition

Landscape Analysis

The global automotive air

compressor market is moderately consolidated, with a mix of large, diversified

automotive suppliers and specialized compressor manufacturers. Competition is

based on technological innovation (especially in e-compressors), system

integration capabilities, reliability, global supply chain presence, and cost

competitiveness. Key strategies include forming strategic partnerships with EV

manufacturers, investing heavily in R&D for efficient and quiet compressor

technologies, and expanding product portfolios to cover both conventional and

electric vehicle segments. The aftermarket for brake system compressors in

commercial vehicles is also a competitive and fragmented space.

Global Automotive Air Compressor Market Recent Developments

News:

- In February 2025, Hanon Systems launched a new ultra-quiet and

high-efficiency scroll compressor specifically designed for 800V EV

architectures.

- In December 2024, Continental AG secured a major contract to supply

integrated air supply units (compressors + dryers) for a North American

OEM's next-generation full-size SUV platform.

- In October 2024, Valeo and Mahle announced a joint venture to develop

next-generation thermal management systems for EVs, focusing on heat pump

technology that relies on advanced compressors.

- In August 2024, Knorr-Bremse introduced a new generation of

energy-efficient air compressors for commercial vehicles, targeting a 10%

reduction in power consumption.

The Global Automotive Air Compressor Market Is Dominated by a

Few Large Companies, such as

●

Continental AG

●

Knorr-Bremse AG

●

Valeo SA

●

Hanon Systems

●

MAHLE GmbH

●

Toyota Industries

Corporation

●

Hitachi Automotive

Systems, Ltd.

●

WABCO (ZF

Friedrichshafen AG)

●

VIAIR Corporation

●

Denso Corporation

●

Garrett Motion Inc.

●

SPX FLOW, Inc.

●

Bendix Commercial

Vehicle Systems LLC

●

Mitsubishi Heavy

Industries Machinery Systems, Ltd.

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Automotive Air

Compressor Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Automotive Air Compressor Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Automotive Air

Compressor Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product Type of Global Automotive

Air Compressor Market

1.3.2.Application of Global Automotive

Air Compressor Market

1.3.3.Vehicle Type of Global Automotive

Air Compressor Market

1.3.4.Region of Global Automotive

Air Compressor Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Overview

of Global IVF Treatment and Access

2.6.

Key

Developments

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Automotive Air Compressor Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Automotive Air Compressor Market Estimates

& Forecast Trend Analysis, by Product Type

4.1.

Global

Automotive Air Compressor Market Revenue (US$ Bn) Estimates and Forecasts, by Product

Type, 2020 - 2033

4.1.1.Reciprocating Compressor

4.1.2.Rotary Screw Compressor

4.1.3.Centrifugal Compressor

5. Global

Automotive Air Compressor Market Estimates

& Forecast Trend Analysis, by Application

5.1.

Global

Automotive Air Compressor Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

5.1.1.Air Suspension

5.1.2.Braking Systems

5.1.3.HVAC

5.1.4.Engine/Battery Cooling

5.1.5.Others (Tire Inflation,

Pneumatic Tools)

6. Global

Automotive Air Compressor Market Estimates

& Forecast Trend Analysis, by Vehicle Type

6.1.

Global

Automotive Air Compressor Market Revenue (US$ Bn) Estimates and Forecasts, by Vehicle

Type 2020 - 2033

6.1.1.Passenger Cars

6.1.2.Light Commercial Vehicles

(LCVs)

6.1.3.Heavy Commercial Vehicles

(HCVs)

6.1.4.Electric Vehicles (EVs)

7. Global

Automotive Air Compressor Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Automotive Air Compressor Market Revenue (US$ Bn) Estimates and Forecasts, by region,

2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Automotive

Air Compressor Market: Estimates &

Forecast Trend Analysis

8.1.

North

America Automotive Air Compressor Market Assessments & Key Findings

8.1.1.North America Automotive

Air Compressor Market Introduction

8.1.2.North America Automotive

Air Compressor Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Product

Type

8.1.2.2. By Application

8.1.2.3. By Vehicle

Type

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Automotive

Air Compressor Market: Estimates &

Forecast Trend Analysis

9.1.

Europe

Automotive Air Compressor Market Assessments & Key Findings

9.1.1.Europe Automotive Air

Compressor Market Introduction

9.1.2.Europe Automotive Air

Compressor Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product

Type

9.1.2.2. By Application

9.1.2.3. By Vehicle

Type

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Automotive

Air Compressor Market: Estimates &

Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Automotive Air Compressor Market Introduction

10.1.2.

Asia

Pacific Automotive Air Compressor Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1. By Product

Type

10.1.2.2. By Application

10.1.2.3. By Vehicle

Type

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Automotive

Air Compressor Market: Estimates &

Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Automotive Air Compressor Market

Introduction

11.1.2.

Middle East & Africa Automotive Air Compressor Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Product

Type

11.1.2.2. By Application

11.1.2.3. By Vehicle

Type

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Automotive Air Compressor Market:

Estimates & Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Automotive Air Compressor Market Introduction

12.1.2.

Latin

America Automotive Air Compressor Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

12.1.2.1. By Product

Type

12.1.2.2. By Application

12.1.2.3. By Vehicle

Type

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Automotive Air Compressor Market Product Mapping

14.2.

Global

Automotive Air Compressor Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3.

Global

Automotive Air Compressor Market Tier Structure Analysis

14.4.

Global

Automotive Air Compressor Market Concentration & Company Market Shares (%)

Analysis, 2024

15.

Company

Profiles

15.1.

Continental AG

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. Knorr-Bremse

AG

15.3. Valeo SA

15.4. Hanon Systems

15.5. MAHLE GmbH

15.6. Toyota

Industries Corporation

15.7. Hitachi

Automotive Systems, Ltd.

15.8. WABCO (ZF

Friedrichshafen AG)

15.9. VIAIR

Corporation

15.10. Denso

Corporation

15.11. Garrett

Motion Inc.

15.12. SPX FLOW,

Inc.

15.13. Bendix

Commercial Vehicle Systems LLC

15.14. Mitsubishi

Heavy Industries Machinery Systems, Ltd.

15.15. Other

Prominent Players

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables