Automotive Airbag and Seatbelt Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Type (Chromatography, Spectroscopy, Molecular Analysis, Mass Spectrometry, Others), By Application (Life Science & Pharma, Environmental Testing, Food & Beverage, Petrochemicals, Others), By End-User (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Environmental Agencies, Industrial & Manufacturing Facilities) And Geography

2025-11-21

Automotive & Transportation (Mobility)

Ekta Chaurasia (Team Lead)

Description

Automotive Airbag and

Seatbelt Market Overview

The Automotive Airbag and Seatbelt Market is set

for a period of steady and progressive growth from 2025 to 2033, propelled by

stringent government safety regulations, rising consumer awareness, and the

rapid integration of advanced safety systems as a standard feature in vehicles.

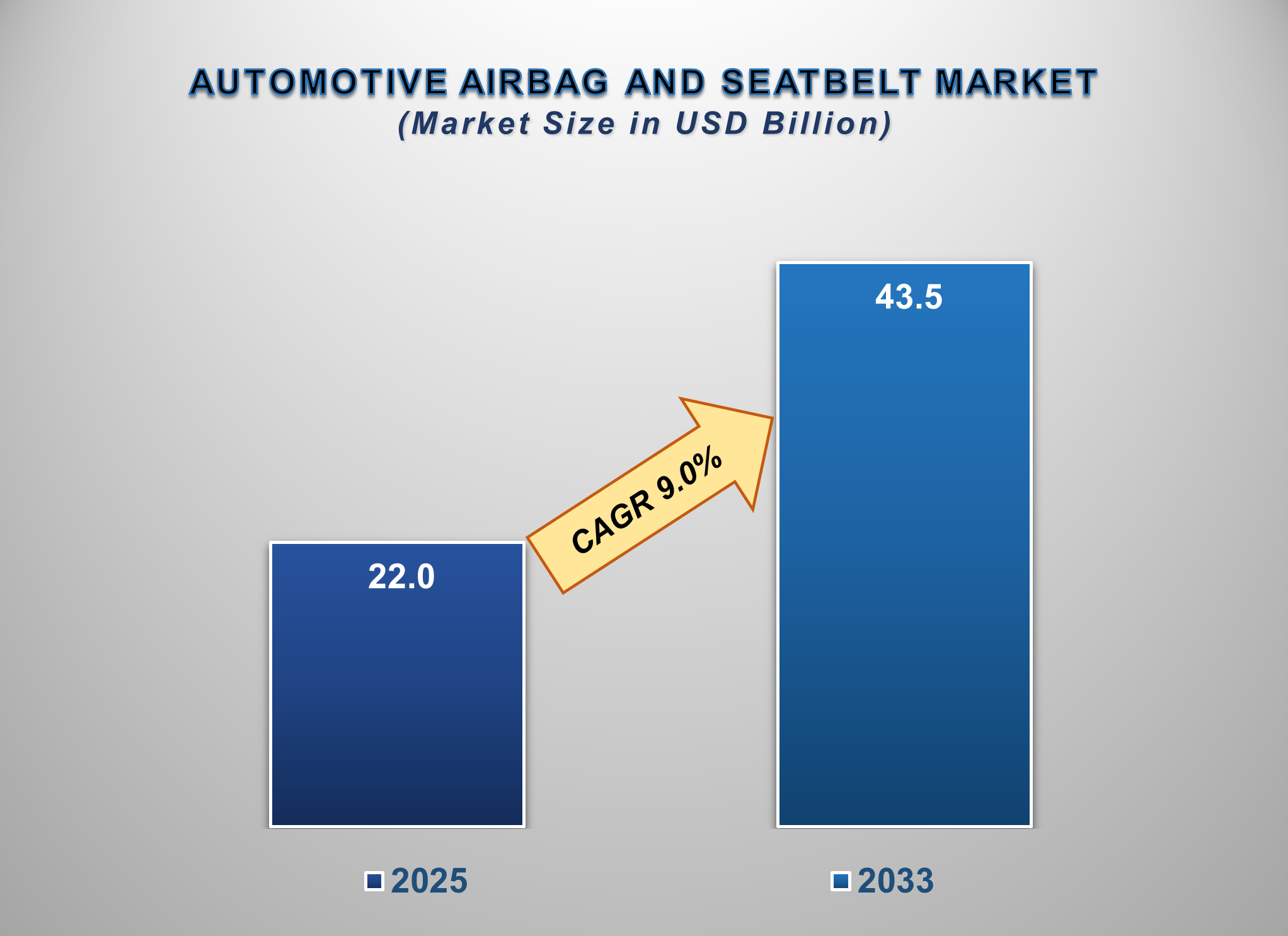

The market is projected to be valued at approximately USD 22.0 billion in 2025

and is forecasted to reach nearly USD 43.5 billion by 2033, exhibiting a

compound annual growth rate (CAGR) of 9.0% during this period.

Airbags and seatbelts are fundamental components of a vehicle's passive safety system, working in tandem to minimize occupant injury during a collision. The market growth is primarily fuelled by the mandatory adoption of safety norms across the globe, such as the inclusion of six airbags and three-point seatbelts for all seating positions. Furthermore, the development of New Car Assessment Programs (NCAP) in regions like Latin America and Southeast Asia, which incentivize manufacturers to offer better safety features, is a key market enabler. Technological advancements such as the development of adaptive airbags, inflatable seatbelts, and advanced sensor systems are creating new growth avenues. The Asia-Pacific region remains the largest and fastest-growing regional market due to its massive vehicle production and sales volume, coupled with increasingly strict safety regulations.

Automotive Airbag and Seatbelt Market

Drivers and Opportunities

Stringent Government Safety Regulations

and NCAP Protocols are Foundational Market Drivers

Governments worldwide are mandating stricter

vehicle safety standards to reduce road fatalities and injuries. Regulations

requiring dual-front airbags and three-point seatbelts are now commonplace,

with many developed economies moving towards mandates for side and curtain

airbags. Organizations like Global NCAP are pushing for higher safety ratings,

which directly encourages automakers to equip vehicles with more airbags and

advanced seatbelt pre-tensioners and load limiters as standard features. This regulatory

push creates a consistent, compliance-driven demand for these safety systems.

Rising Consumer Awareness and Demand for

Safety is a Primary Growth Engine

As safety becomes a significant differentiator

in the automotive market, consumers are increasingly prioritizing vehicles with

high safety ratings and advanced occupant protection systems. The proliferation

of online information and safety rating agencies has empowered buyers, making

the number of airbags and the presence of seatbelt reminders key purchase

decision factors. This shift in consumer preference is compelling automakers,

even in cost-sensitive markets, to offer enhanced safety packages, thereby driving

the penetration of airbags and advanced seatbelts across all vehicle segments.

Technological Advancements and the Shift

Towards Integrated Safety Systems Present Significant Opportunities

The market is evolving beyond basic restraint

systems towards intelligent, adaptive solutions. Key areas of opportunity

include the development of next-generation airbags (e.g., front-center airbags,

far-side airbags, and adaptive-output airbags that adjust deployment force

based on occupant size and crash severity) and smart seatbelts with motorized

pre-tensioning and haptic feedback. The integration of these systems with

active safety features like Autonomous Emergency Braking (AEB) through a

central electronic control unit is paving the way for holistic Integrated

Safety Systems. The rise of electric and autonomous vehicles also presents a

unique opportunity to redesign interior safety systems tailored to new cabin

layouts.

Automotive Airbag and Seatbelt Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 22.0 Billion |

|

Market Forecast in 2033 |

USD 43.5 Billion |

|

CAGR % 2025-2033 |

9.0% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio, Application Analysis, Company Market Share,

Company Heatmap, Regulatory Landscape, Growth Factors and more |

|

Segments Covered |

●

By Product Type ●

By Vehicle Type ●

By Material |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Automotive Airbag and Seatbelt Market Report Segmentation

Analysis

The global automotive airbag and

seatbelt market industry analysis is segmented by Product Type, by Vehicle

Type, by Material, and by region.

The Airbag segment is anticipated to command a significant

share of the global market during the forecast period.

Based on product type, the market is divided into

Airbag (Front, Side, Curtain, Knee) and Seatbelt (2-point, 3-point, Others). The Airbag segment is a major and rapidly

growing category. Its growth is driven by the increasing number of airbags per

vehicle, moving from standard dual-front airbags to include side, curtain, and

knee airbags as standard or optional features, especially in mid-range and

premium segments. The continuous innovation in airbag technology to improve

protection in various crash scenarios further solidifies its dominant position.

The airbag segment's commanding market share is

fueled by a global regulatory and consumer shift towards comprehensive vehicle

safety, moving beyond the minimum standard of dual-front airbags. This

expansion is characterized by the increasing adoption of side, curtain, and

knee airbags as standard equipment, even in mid-range vehicles, significantly

increasing the number of units per car. Continuous technological innovation

further propels this growth, with the development of advanced systems like

front-center airbags to prevent passenger collision and pedestrian airbags for

external safety. These innovations address a wider range of crash scenarios,

including side-impacts and rollovers, making them critical for achieving top

safety ratings.

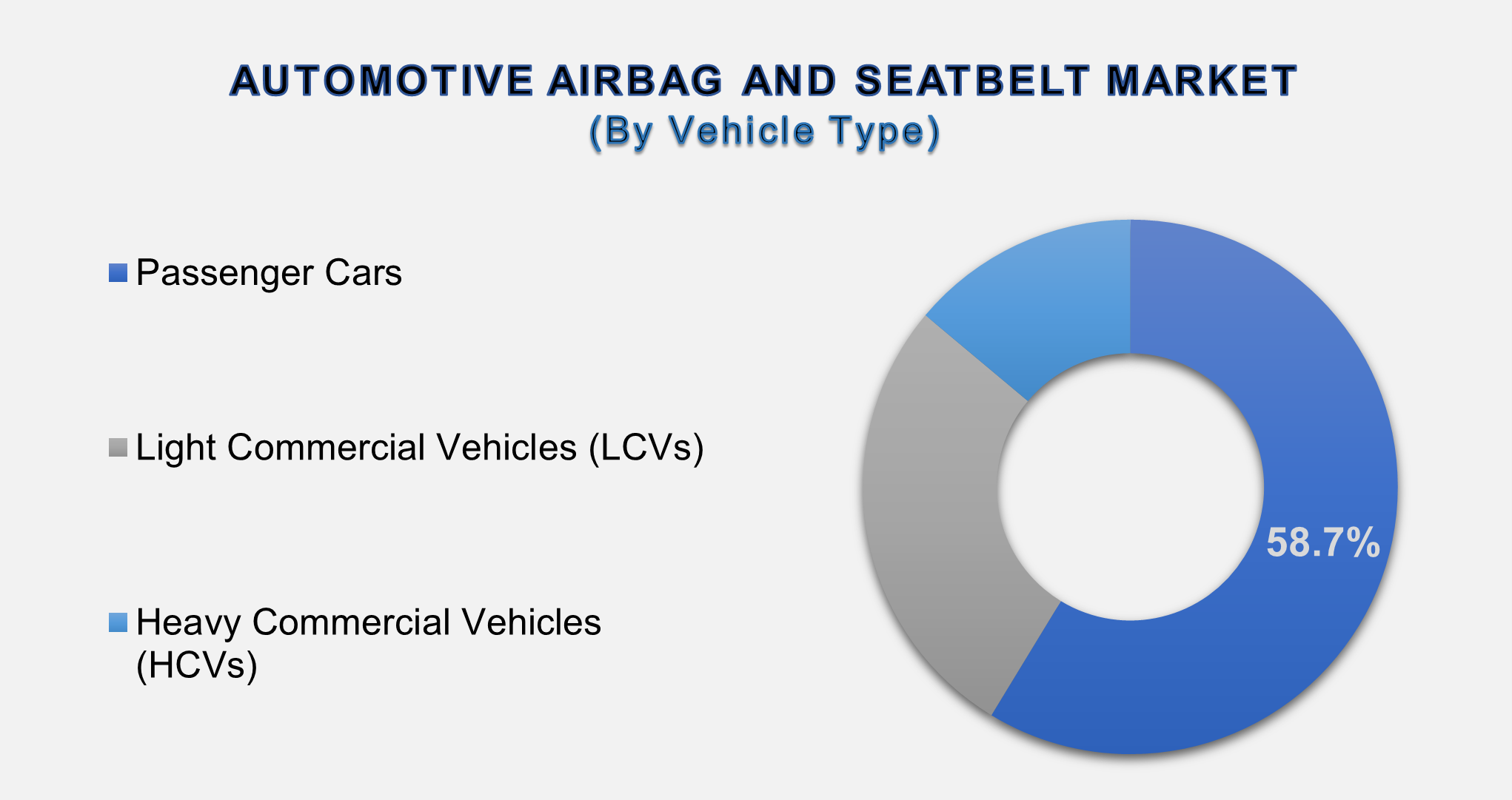

The Passenger Cars segment dominated the market in 2025 and

is projected to grow at a significant CAGR during the forecast period.

Based on vehicle type, the market is segmented

into Passenger Cars, Light Commercial Vehicles (LCVs), and Heavy Commercial

Vehicles (HCVs). The Passenger Cars segment holds the largest share by a

significant margin. This dominance is a direct result of the high global

production and sales volume of passenger cars, coupled with the widespread

application of safety regulations specifically targeting this vehicle category.

The intense competition among car manufacturers also drives the adoption of

advanced safety features as a key selling point.

Furthermore, stringent government safety

regulations and consumer-facing New Car Assessment Programs (NCAP) are most

aggressively applied to passenger vehicles, mandating advanced restraint

systems across all trims. Intense competition among automakers also plays a

crucial role; safety has become a key purchase driver, leading manufacturers to

offer features like six or more airbags and pre-tensioning seatbelts as

standard to enhance their brand appeal and meet five-star safety benchmarks.

This combination of high volume, strict regulation, and competitive pressure

solidifies passenger cars as the primary end-user for these safety components.

The Nylon segment is expected to hold the largest market

share in 2025.

By material, the market is divided into Nylon,

Polyester, and Others. The Nylon segment is the largest, as nylon 6-6 is the

predominant material used for airbag fabrics due to its excellent

strength-to-weight ratio, thermal stability, and energy absorption properties.

Its ability to withstand the high-force, high-temperature deployment of an

airbag makes it the material of choice for most manufacturers.

Most importantly, nylon's excellent energy

absorption and controlled elongation characteristics are vital for managing the

violent, high-force deployment; the fabric must inflate instantly yet cushion

the occupant effectively by absorbing kinetic energy. While polyester is a

competitor, nylon's proven track record, reliability, and optimal balance of

mechanical and thermal properties under extreme conditions continue to make it

the preferred and safest material for this life-saving application.

The following segments

are part of an in-depth analysis of the global Automotive Airbag and Seatbelt

Market:

|

Market Segments |

|

|

By Product Type |

●

Airbag o

Front Airbag o

Side Airbag o

Curtain Airbag o

Knee Airbag o

Other Airbags

(Front-Center, Pedestrian, etc.) ●

Seatbelt o

2-Point Seatbelt o

3-Point Seatbelt o

Other Seatbelts

(4-Point, 5-Point, Inflatable) |

|

By Material |

●

Nylon ●

Polyester ●

Other Materials |

|

By Vehicle Type |

●

Passenger Cars ●

Light Commercial

Vehicles (LCVs) ●

Heavy Commercial

Vehicles (HCVs) |

Automotive Airbag and Seatbelt Market Share Analysis by

Region

The Asia-Pacific region is anticipated to hold the largest

portion of the Automotive Airbag and Seatbelt Market globally throughout the

forecast period.

Asia-Pacific is the undisputed leader, holding a

dominant market share. This leadership is anchored by the region's status as

the world's largest automotive manufacturing hub, led by China, Japan, India,

and South Korea. Rapidly evolving safety regulations in high-growth markets

like India and ASEAN countries, increasing vehicle production, and rising

disposable incomes are the primary drivers of growth in this region.

In China, the world's largest

market, sales are projected to grow from 26.1 million vehicles in 2023 to 27.5

million in 2024. This growth is overwhelmingly fueled by a seismic shift toward

New Energy Vehicles (NEVs), which now constitute over 40% of all sales. This

trend is largely propelled by extensive government support, a mature charging

infrastructure, and intense competition among domestic manufacturers, making

China the epicenter of electric mobility innovation and adoption.

Conversely, the United States

market, the second-largest globally, shows a more modest recovery and growth,

with sales expected to rise from 15.5 million to 15.9 million. This uptick is

primarily driven by the normalization of inventory levels following years of

supply chain disruptions. The market continues to be dominated by consumer

preference for larger vehicles, with SUVs and pickup trucks accounting for the

vast majority of sales. While electric vehicle adoption is increasing, its pace

and penetration remain less aggressive than in China, reflecting different

consumer preferences, economic factors, and a less uniform policy push.

Automotive Airbag and Seatbelt Market Competition Landscape

Analysis

The global automotive airbag and seatbelt market is a

consolidated and highly competitive landscape, dominated by a few Tier-1 global

suppliers. Competition is intense and based on factors such as product

reliability, technological innovation, system integration capabilities, global

supply chain strength, and cost-effectiveness. Key strategies observed in the

market include heavy investment in R&D for next-generation safety products,

strategic partnerships and long-term contracts with automakers, and a focus on

vertical integration to control costs and ensure quality. The push for

lightweight materials and compact designs is also a key competitive

differentiator.

Global Automotive Airbag

and Seatbelt Market Recent Developments News:

- In March 2025, ZF Friedrichshafen AG launched a new

generation of side-airbag sensors with improved crash detection algorithms

for faster and more accurate deployment.

- In December 2024, Autoliv Inc. announced a major

supply agreement with a leading electric vehicle manufacturer for its

integrated interior safety system, including front-center airbags.

- In October 2024, Joyson Safety Systems acquired a specialist software

company to enhance its capabilities in sensor fusion and occupant

detection systems.

The Global Automotive

Airbag and Seatbelt Market Is Dominated by a Few Large Companies, such as

●

Autoliv Inc.

●

ZF Friedrichshafen AG

●

Joyson Safety Systems

●

Robert Bosch GmbH

●

Continental AG

●

Denso Corporation

●

Toyoda Gosei Co., Ltd.

●

Hyundai Mobis

●

Ashimori Industry Co.,

Ltd.

●

Toray Industries, Inc.

●

Takata Corporation

●

Jiangsu Huade

Automotive Engineering Co., Ltd.

●

Jinzhou Jinheng

Automotive Safety System Co., Ltd.

●

Beijing WKW Automotive

Parts Co., Ltd.

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Automotive Airbag

and Seatbelt Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Automotive Airbag and Seatbelt Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Automotive Airbag

and Seatbelt Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product Type of Global Automotive

Airbag and Seatbelt Market

1.3.2.Material of Global Automotive

Airbag and Seatbelt Market

1.3.3.Vehicle Type of Global Automotive

Airbag and Seatbelt Market

1.3.4.Region of Global Automotive

Airbag and Seatbelt Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5. Pricing Analysis

2.6.

Key

Developments

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Automotive Airbag and Seatbelt Market

Estimates & Historical Trend Analysis (2020 - 2024)

4. Global

Automotive Airbag and Seatbelt Market

Estimates & Forecast Trend Analysis, by Product

Type

4.1.

Global

Automotive Airbag and Seatbelt Market Revenue (US$ Bn) Estimates and Forecasts,

by Product Type, 2020 - 2033

4.1.1.

Airbag

4.1.1.1.

Front

Airbag

4.1.1.2.

Side

Airbag

4.1.1.3.

Curtain

Airbag

4.1.1.4.

Knee

Airbag

4.1.1.5.

Other

Airbags (Front-Center, Pedestrian, etc.)

4.1.2.

Seatbelt

4.1.2.1.

2-Point

Seatbelt

4.1.2.2.

3-Point

Seatbelt

4.1.2.3.

Other

Seatbelts (4-Point, 5-Point, Inflatable)

5. Global

Automotive Airbag and Seatbelt Market

Estimates & Forecast Trend Analysis, by Material

5.1.

Global

Automotive Airbag and Seatbelt Market Revenue (US$ Bn) Estimates and Forecasts,

by Material, 2020 - 2033

5.1.1.Nylon

5.1.2.Polyester

5.1.3.Other Materials

6. Global

Automotive Airbag and Seatbelt Market

Estimates & Forecast Trend Analysis, by Vehicle

Type

6.1.

Global

Automotive Airbag and Seatbelt Market Revenue (US$ Bn) Estimates and Forecasts,

by Vehicle Type, 2020 - 2033

6.1.1.Passenger Cars

6.1.2.Light Commercial Vehicles

(LCVs)

6.1.3.Heavy Commercial Vehicles

(HCVs)

7. Global

Automotive Airbag and Seatbelt Market

Estimates & Forecast Trend Analysis, by Region

7.1.

Global

Automotive Airbag and Seatbelt Market Revenue (US$ Bn) Estimates and Forecasts,

by Region, 2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Automotive

Airbag and Seatbelt Market: Estimates

& Forecast Trend Analysis

8.1. North America Automotive

Airbag and Seatbelt Market Assessments & Key Findings

8.1.1.North America Automotive

Airbag and Seatbelt Market Introduction

8.1.2.North America Automotive

Airbag and Seatbelt Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Product Type

8.1.2.2.

By Material

8.1.2.3.

By Vehicle Type

8.1.2.4. By Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Automotive

Airbag and Seatbelt Market: Estimates

& Forecast Trend Analysis

9.1. Europe Automotive Airbag

and Seatbelt Market Assessments & Key Findings

9.1.1.Europe Automotive Airbag

and Seatbelt Market Introduction

9.1.2.Europe Automotive Airbag

and Seatbelt Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Product Type

9.1.2.2.

By Material

9.1.2.3.

By Vehicle Type

9.1.2.4. By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Automotive

Airbag and Seatbelt Market: Estimates

& Forecast Trend Analysis

10.1. Asia Pacific Market

Assessments & Key Findings

10.1.1.

Asia

Pacific Automotive Airbag and Seatbelt Market Introduction

10.1.2.

Asia

Pacific Automotive Airbag and Seatbelt Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1.

By Product Type

10.1.2.2.

By Material

10.1.2.3.

By Vehicle Type

10.1.2.4. By Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Automotive

Airbag and Seatbelt Market: Estimates

& Forecast Trend Analysis

11.1. Middle East & Africa

Market Assessments & Key Findings

11.1.1. Middle

East & Africa

Automotive Airbag and Seatbelt Market Introduction

11.1.2. Middle

East & Africa

Automotive Airbag and Seatbelt Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

11.1.2.1.

By Product Type

11.1.2.2.

By Material

11.1.2.3.

By Vehicle Type

11.1.2.4. By Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Automotive Airbag and Seatbelt Market:

Estimates & Forecast Trend Analysis

12.1. Latin America Market

Assessments & Key Findings

12.1.1. Latin America Automotive

Airbag and Seatbelt Market Introduction

12.1.2. Latin America Automotive

Airbag and Seatbelt Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Product Type

12.1.2.2.

By Material

12.1.2.3.

By Vehicle Type

12.1.2.4. By Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13.

Country

Wise Market: Introduction

14.

Competition

Landscape

14.1. Global Automotive Airbag

and Seatbelt Market Product Mapping

14.2. Global Automotive Airbag

and Seatbelt Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3. Global Automotive Airbag

and Seatbelt Market Tier Structure Analysis

14.4. Global Automotive Airbag

and Seatbelt Market Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

Autoliv Inc.

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2.

ZF Friedrichshafen AG

15.3.

Joyson Safety Systems

15.4.

Robert Bosch GmbH

15.5.

Continental AG

15.6.

Denso Corporation

15.7.

Toyoda Gosei Co., Ltd.

15.8.

Hyundai Mobis

15.9.

Ashimori Industry Co., Ltd.

15.10.

Toray Industries, Inc.

15.11.

Takata Corporation

15.12.

Jiangsu Huade Automotive Engineering Co., Ltd.

15.13.

Jinzhou Jinheng Automotive Safety System Co., Ltd.

15.14.

Beijing WKW Automotive Parts Co., Ltd.

15.15.

Other Prominent Players

16. Research

Methodology

16.1. External Transportations /

Databases

16.2. Internal Proprietary

Database

16.3. Primary Research

16.4. Secondary Research

16.5. Assumptions

16.6. Limitations

16.7. Report FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables