Barley Tea Market Size and Forecast (2025–2033), Global and Regional Share, Trends, and Industry Analysis Report Coverage: By Flavor (Original, Flavored), By Form (Instant, Ready-to-Drink), By Distribution Channel (Offline, Online), and Geography

2026-01-30

Consumer Products

Jaya Bundele (Research Analyst)

Description

Barley Tea Market Overview

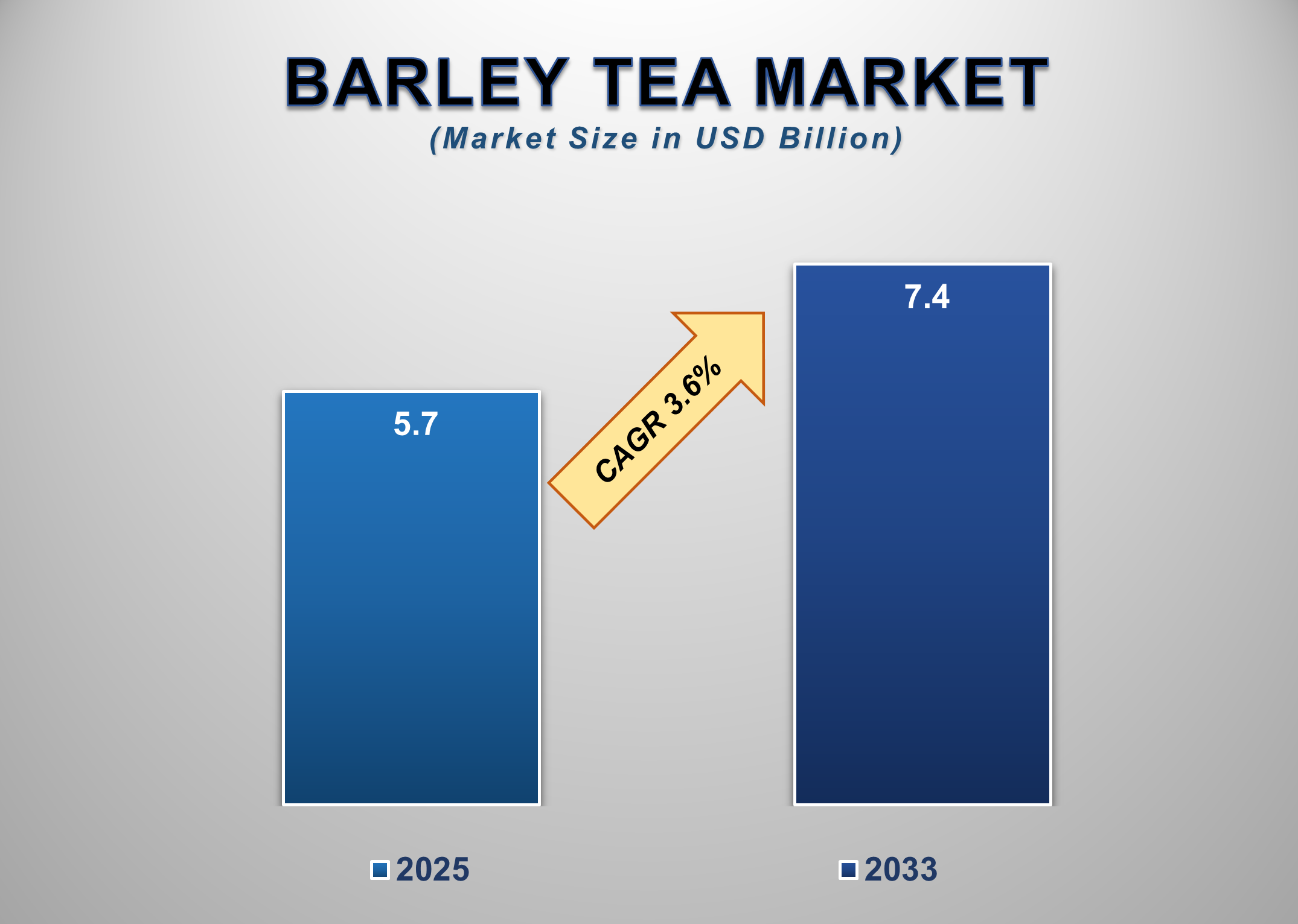

The global Barley Tea Market is experiencing steady growth as consumers increasingly shift toward caffeine-free, plant-based, and digestive-friendly beverage alternatives. Valued at USD 5.7 billion in 2025, the market is projected to reach USD 7.4 billion by 2033, expanding at a CAGR of 3.6% during the forecast period. Barley tea, traditionally consumed in East Asian countries such as Japan, South Korea, and China, is gaining international traction due to its mild flavor, zero caffeine content, and perceived health benefits, including improved digestion and hydration support.

The beverage is typically

produced by roasting barley grains and infusing them in hot or cold water,

resulting in a naturally aromatic drink with no added sugars or artificial

ingredients. This clean-label profile aligns well with rising global demand for

functional and wellness beverages. The growing popularity of herbal and

grain-based teas among health-conscious consumers, athletes, and individuals

seeking caffeine alternatives has significantly contributed to market

expansion.

Barley Tea Market Drivers

and Opportunities

Rising Demand for

Caffeine-Free and Digestive-Friendly Beverages Is Driving Market Growth

The growing consumer shift away from caffeinated beverages toward

natural, caffeine-free alternatives is a key driver fueling the Barley Tea

Market. Increasing awareness of the adverse effects of excessive caffeine

intake, such as sleep disturbances, anxiety, and digestive discomfort, has

encouraged consumers to explore healthier beverage options. Barley tea,

naturally free from caffeine and calories, has positioned itself as a preferred

everyday drink suitable for all age groups, including children and elderly

populations. Digestive health has become a major focus area within the global

wellness movement. Barley tea is traditionally associated with supporting

digestion, reducing bloating, and promoting hydration, making it attractive to

consumers seeking functional beverages without medicinal claims. The drink’s

mild taste and versatility for hot and cold consumption further enhance its

adoption across climates and seasons. In addition, increasing consumption of

herbal and grain-based teas in Western markets has expanded retail shelf space

for barley tea products. Supermarkets, health food stores, and specialty tea

retailers are actively promoting caffeine-free tea alternatives, driving higher

visibility and consumer trials. This sustained demand for clean-label,

functional hydration solutions continues to support steady market growth.

Expansion of Ready-to-Drink Formats and Premium Tea

Consumption Is Strengthening Market Adoption

The rapid growth of ready-to-drink (RTD) beverage consumption is

another significant driver supporting the Barley Tea Market. Modern consumers

increasingly prioritize convenience, portability, and on-the-go hydration,

leading to rising demand for bottled and canned tea products. RTD barley tea

has gained strong traction in urban markets due to its refreshing profile, long

shelf life, and suitability as a daily hydration beverage. Premiumization

trends within the global tea industry are also positively influencing market

growth. Consumers are showing greater willingness to pay for high-quality,

authentic, and traditionally inspired beverages. Japanese and Korean barley tea

brands, known for their heritage and brewing techniques, are gaining popularity

in international markets, particularly in North America and Europe.

Additionally, innovation in packaging, such as eco-friendly bottles and

minimalist branding, is helping manufacturers appeal to

sustainability-conscious consumers. As functional hydration continues to

replace sugary soft drinks, RTD barley tea is well-positioned to benefit from

evolving beverage consumption habits.

Growing Popularity of Asian Functional Beverages Creates

Significant Market Opportunities

The rising global influence of Asian food and beverage culture

presents a major opportunity for the Barley Tea Market. Increased exposure

through travel, digital media, and international cuisine has driven curiosity

and acceptance of traditional Asian beverages among Western consumers. Barley

tea, already deeply embedded in Japanese and Korean daily consumption, is

increasingly perceived as an authentic and healthy lifestyle drink globally.

Manufacturers have opportunities to expand product portfolios through flavored

variants, organic certifications, and functional positioning such as digestive

wellness and hydration support. Growth in e-commerce and direct-to-consumer

channels further enables brands to reach niche health-focused audiences without

heavy reliance on traditional retail infrastructure. Emerging markets in

Southeast Asia, the Middle East, and Latin America also present untapped

potential due to rising disposable incomes and increasing adoption of herbal

beverages. Strategic marketing, localized flavors, and partnerships with

wellness-focused retailers can significantly enhance market penetration in

these regions.

Barley Tea Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 5.7 Billion |

|

Market Forecast in 2033 |

USD 7.4 Billion |

|

CAGR % 2025-2033 |

3.6% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Flavor, By

Form, By Distribution Channel |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Barley Tea Market Report

Segmentation Analysis

The Barley Tea Market is segmented by flavor, form, distribution

channel, and geography.

Original

Flavor Segment Accounted for the Largest Market Share in the Global Barley Tea

Market

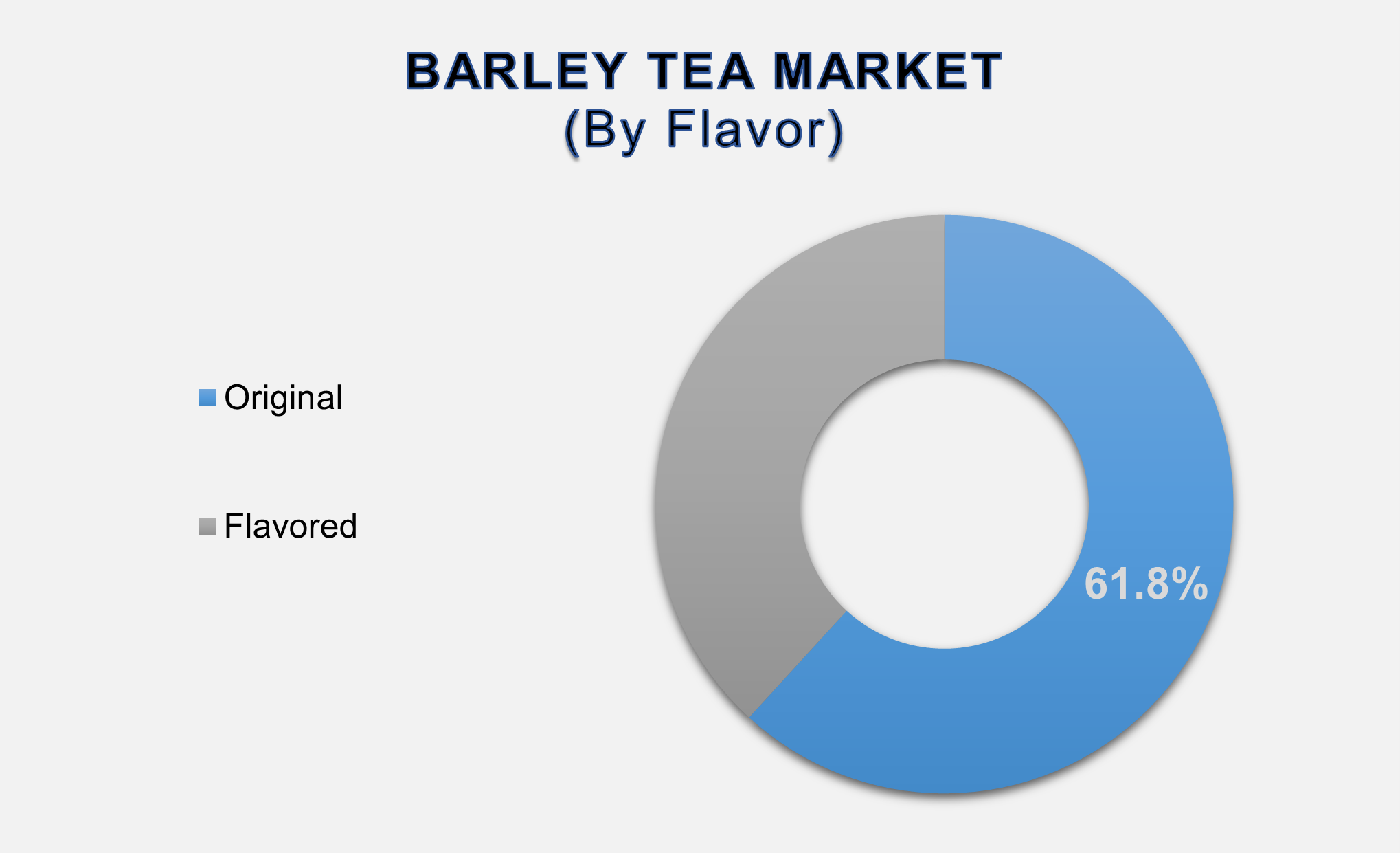

The original flavor segment accounted for the largest market share, holding 61.8% of the global Barley Tea Market, driven by strong consumer preference for traditional, unflavored barley tea. Original barley tea is widely consumed in Japan and South Korea as a daily hydration beverage and is valued for its roasted aroma, mild taste, and digestive benefits. Consumers seeking clean-label and minimally processed beverages prefer original variants over flavored options, particularly in health-conscious demographics. The absence of added sweeteners or artificial flavors aligns with rising demand for natural beverages. This segment also benefits from strong cultural familiarity in Asia-Pacific and increasing adoption in Western markets through specialty tea retailers and Asian grocery chains.

Ready-to-Drink Segment Holds a Significant Share

Due to Convenience and Urban Demand

The ready-to-drink barley tea

segment holds a significant share of the global market, supported by rising

demand for convenient and portable beverage options. RTD formats are widely

consumed in urban areas, workplaces, schools, and fitness environments where

quick hydration is essential. Bottled barley tea products are particularly

popular in North America and Asia-Pacific due to their extended shelf life and

ease of consumption. Manufacturers are increasingly investing in premium

packaging, organic positioning, and functional claims to differentiate RTD

offerings. As on-the-go consumption continues to rise, the RTD segment is

expected to maintain strong momentum.

Offline Distribution Channel Dominates Due to

Strong Retail Presence

The offline distribution channel

accounts for the largest share of the Barley Tea Market, driven by widespread

availability in supermarkets, hypermarkets, convenience stores, and specialty

tea outlets. Consumers often prefer purchasing tea beverages through physical

retail due to brand familiarity, promotional visibility, and immediate

availability. Offline channels also play a key role in introducing new

consumers to barley tea through sampling and in-store marketing. While online

sales are growing, particularly for premium and imported brands, traditional

retail remains the dominant purchasing channel globally.

The following segments are

part of an in-depth analysis of the global Barley Tea market:

|

Market Segments |

|

|

By Flavor |

●

Original ●

Flavored |

|

By Barley Tea

Form |

●

Instant ●

Ready-to-drink |

|

By

Distribution Channel |

●

Offline ●

Online |

Barley Tea Market Share

Analysis by Region

North America is anticipated to hold the biggest

portion of the Barley Tea Market globally throughout the forecast period.

North America dominates the

global Barley Tea Market with 49.9% market share, supported by rising health

awareness, growing demand for caffeine-free beverages, and increasing

popularity of Asian-origin functional drinks. The presence of specialty tea brands

and expanding ethnic food retail networks has strengthened market penetration

across the U.S. and Canada.

Asia-Pacific is expected to grow

at the highest CAGR, driven by strong cultural consumption, expanding RTD

product launches, and increasing urbanization. Countries such as Japan, South

Korea, and China remain core markets, while Southeast Asia is emerging as a

high-growth region due to rising disposable incomes and modern retail

expansion.

Barley Tea Market

Competition Landscape Analysis

The Barley Tea Market is

moderately fragmented, with a mix of established Asian beverage companies and

emerging specialty tea brands. Key players focus on brand heritage, product

authenticity, packaging innovation, and geographic expansion. Strategic partnerships,

RTD product launches, and expansion into online channels are common competitive

strategies.

Global Barley Tea Market

Recent Developments News:

- In August 2022,

Deer Creek Malthouse, a U.S. specialty malt company, launched

nitro-dosed canned barley tea made from organic sprouted whole grains,

available in multiple flavors.

- In April 2022,

The Canadian Barley Tea Company introduced mo’mugi roasted barley tea,

offering convenient preparation and availability on Amazon in Canada and

the U.S.

- In January 2020,

National Foods and Beverages (India) launched the

House brand barley tea, packaged in boxes of 16 individual 20-gram

pouches, distributed through Indian retail channels.

The Global Barley Tea Market Is

Dominated by a Few Large Companies, such as

●

ITO En

●

Suntory Beverage &

Food

●

Kirin Holdings

●

Otsuka Pharmaceutical

●

Jinjja Barley Tea

●

Haitai

●

The Republic of Tea

●

Lotte

●

New Mexico Tea Company

●

The Canadian Barley

Tea Company

● Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Barley Tea Market

Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Barley Tea Market Scope and Market Estimation

1.2.1.Global Barley Tea Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Barley Tea Market

Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Flavor of Global Barley

Tea Market

1.3.2.Barley Tea Form of Global Barley

Tea Market

1.3.3.Distribution Channel of

Global Barley Tea Market

1.3.4.Region of Global Barley

Tea Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Barley Tea Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Barley Tea Market Estimates

& Forecast Trend Analysis, by Flavor

4.1.

Global

Barley Tea Market Revenue (US$ Bn) Estimates and Forecasts, by Flavor, 2020 - 2033

4.1.1.Original

4.1.2.Flavored

5. Global

Barley Tea Market Estimates

& Forecast Trend Analysis, by Barley Tea Form

5.1.

Global

Barley Tea Market Revenue (US$ Bn) Estimates and Forecasts, by Barley Tea Form,

2020 - 2033

5.1.1.Instant

5.1.2.Ready-to-drink

6. Global

Barley Tea Market Estimates

& Forecast Trend Analysis, by Distribution Channel

6.1.

Global

Barley Tea Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution

Channel, 2020 - 2033

6.1.1.Offline

6.1.2.Online

7. Global

Barley Tea Market Estimates

& Forecast Trend Analysis, by Region

7.1.

Global

Barley Tea Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Barley

Tea Market: Estimates & Forecast

Trend Analysis

8.1.

North

America Barley Tea Market Assessments & Key Findings

8.1.1.North America Barley Tea

Market Introduction

8.1.2.North America Barley Tea

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Flavor

8.1.2.2. By Barley Tea

Form

8.1.2.3. By Distribution

Channel

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Barley

Tea Market: Estimates & Forecast

Trend Analysis

9.1.

Europe

Barley Tea Market Assessments & Key Findings

9.1.1.Europe Barley Tea Market

Introduction

9.1.2.Europe Barley Tea Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Flavor

9.1.2.2. By Barley Tea

Form

9.1.2.3. By Distribution

Channel

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Barley

Tea Market: Estimates & Forecast

Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Barley Tea Market Introduction

10.1.2.

Asia

Pacific Barley Tea Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Flavor

10.1.2.2. By Barley Tea

Form

10.1.2.3. By Distribution

Channel

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Barley

Tea Market: Estimates & Forecast

Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Barley Tea Market Introduction

11.1.2.

Middle East & Africa Barley Tea Market Size Estimates and

Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Flavor

11.1.2.2. By Barley Tea

Form

11.1.2.3. By Distribution

Channel

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Barley Tea Market: Estimates &

Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Barley Tea Market Introduction

12.1.2.

Latin

America Barley Tea Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1. By Flavor

12.1.2.2. By Barley Tea

Form

12.1.2.3. By Distribution

Channel

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Barley Tea Market Product Mapping

14.2.

Global

Barley Tea Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3.

Global

Barley Tea Market Tier Structure Analysis

14.4.

Global

Barley Tea Market Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

ITO En

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. SIG

Combibloc

15.3. Suntory

Beverage & Food

15.4. Kirin

Holdings

15.5. Otsuka

Pharmaceutical

15.6. Jinjja

Barley Tea

15.7. Haitai

15.8. The

Republic of Tea

15.9. Lotte

15.10. New

Mexico Tea Company

15.11. The

Canadian Barley Tea Company

15.12. Others

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables