Belt Loader Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Ownership (New Delivery, Resale, Lease/Rent), By System (Self-Propelled, Electric, Towable, Diesel, Others), By Weight (0–1000 Kg, 1000–5000 Kg, >5000 Kg), and Geography

2026-02-25

Automotive & Transportation (Mobility)

Ekta Chaurasia (Team Lead)

Description

Belt Loader Market Overview

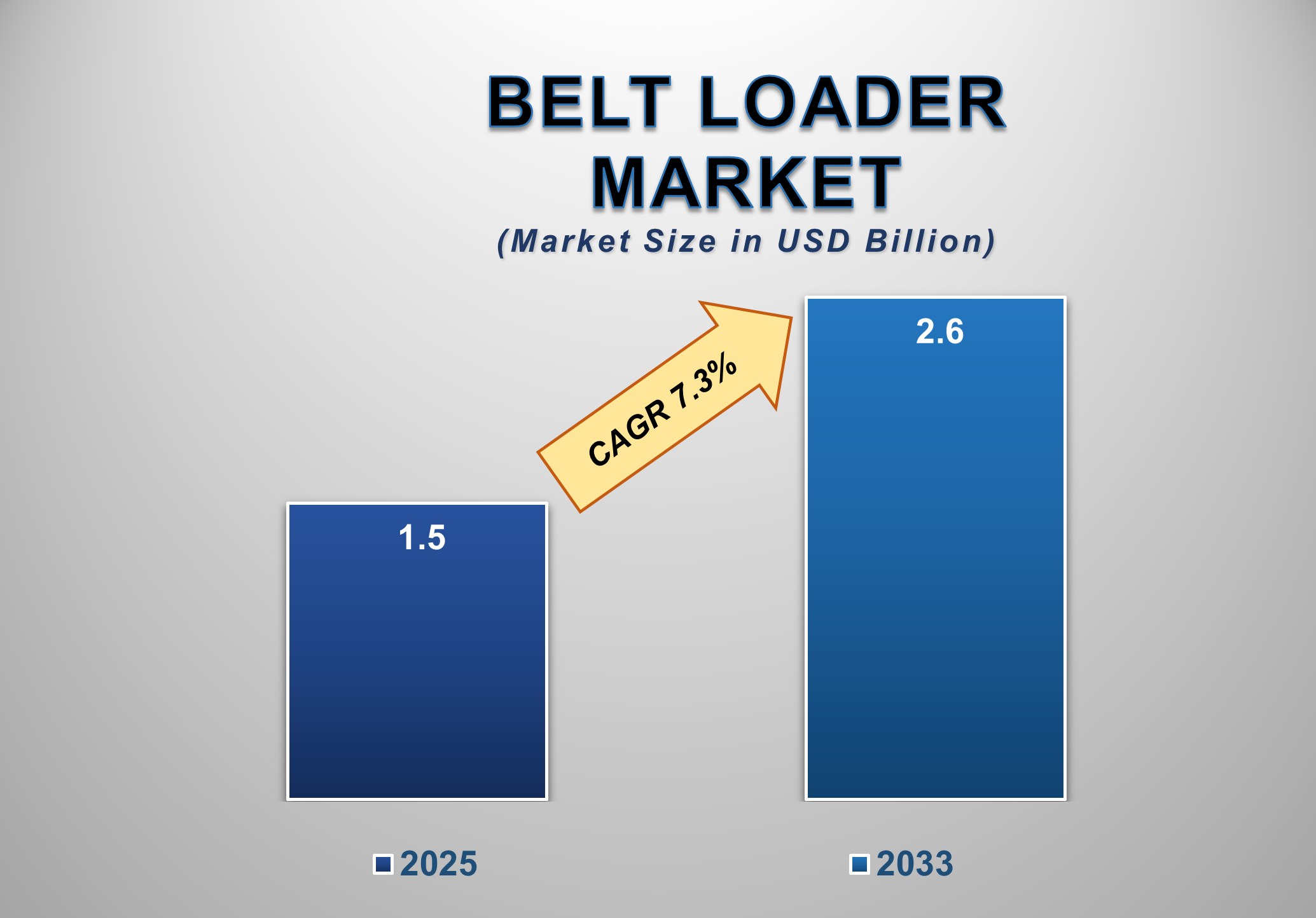

The global Belt Loader Market was valued at USD 1.5 billion in 2025 and is projected to reach USD 2.6 billion by 2033, expanding at a CAGR of 7.3% during the forecast period. This steady growth is primarily driven by rising global air passenger traffic, continuous airport infrastructure expansion, and increasing demand for efficient ground support equipment (GSE) to reduce aircraft turnaround time. Belt loaders play a critical role in airport ground operations by enabling the safe and efficient loading and unloading of baggage, cargo, and mail into aircraft holds, making them indispensable assets for airlines, airports, and ground handling service providers.

The market is witnessing strong

demand from both commercial aviation and cargo operations, supported by

increasing aircraft fleet sizes and the rapid growth of low-cost carriers

worldwide. Additionally, airport operators are increasingly prioritizing operational

efficiency, worker safety, and compliance with stringent aviation regulations,

which has led to higher adoption of technologically advanced and ergonomically

designed belt loaders. The growing shift toward electric and low-emission

ground support equipment is also reshaping the market, as airports seek to meet

sustainability targets and reduce carbon footprints.

Belt Loader Market

Drivers and Opportunities

Rising Air Passenger

Traffic and Aircraft Fleet Expansion Are Driving the Belt Loader Market Growth

The continuous increase in global air passenger traffic remains

one of the primary drivers of the belt loader market. Rising disposable

incomes, urbanization, and increasing affordability of air travel, particularly

through low-cost carriers, have significantly boosted passenger volumes

worldwide. According to aviation authorities, global passenger traffic is

expected to surpass pre-pandemic levels, leading to higher aircraft movements

and increased demand for efficient ground handling operations. Belt loaders are

essential equipment in ensuring fast and safe baggage handling, directly

impacting aircraft turnaround times and airline operational efficiency. In

parallel, the expansion of commercial aircraft fleets is further accelerating

market growth. Airlines across North America, Europe, and the Asia Pacific are

investing heavily in fleet modernization and expansion to meet growing travel

demand and improve fuel efficiency. Each additional aircraft introduced into

service increases the requirement for ground support equipment, including belt

loaders, across airports and airline hubs. Moreover, the growth of air cargo

operations, driven by e-commerce and express logistics, has further increased

the utilization of belt loaders for handling cargo aircraft and freighters.

Airports are also under pressure to improve on-time performance

and reduce congestion, which has resulted in increased procurement of advanced

belt loaders capable of handling higher loads with improved reliability. As

airlines and ground handling companies focus on operational optimization, the

demand for modern belt loaders is expected to remain strong, reinforcing market

growth throughout the forecast period.

Airport Infrastructure Modernization and Automation Is

Accelerating Market Adoption

Another significant driver fueling the belt loader market is the

ongoing modernization and expansion of airport infrastructure globally.

Governments and airport authorities are investing heavily in new terminal

construction, runway expansions, and apron upgrades to accommodate rising air

traffic. These infrastructure development projects often include large-scale

procurement of ground support equipment, including belt loaders, to support

increased operational capacity. Modern airports are increasingly adopting

automated and semi-automated ground handling systems to enhance efficiency and

minimize manual labor. Advanced belt loaders equipped with ergonomic controls,

adjustable heights, and enhanced safety features are being preferred over

conventional models. Additionally, airports are increasingly emphasizing

equipment standardization to streamline maintenance and reduce operational

complexity, further supporting demand for new belt loader deliveries.

Sustainability initiatives are also influencing procurement

decisions. Many airports have committed to achieving carbon neutrality,

prompting a shift toward electric and low-emission belt loaders. Electric belt

loaders not only reduce greenhouse gas emissions but also lower noise levels

and maintenance costs, making them attractive alternatives to diesel-powered

equipment. This transition toward environmentally friendly GSE solutions is

expected to significantly contribute to market growth, particularly in developed

regions and large international airports.

Electrification of Ground Support Equipment Is Creating

Significant Opportunities in the Belt Loader Market

The growing emphasis on sustainability and decarbonization within the aviation industry presents a major opportunity for the belt loader market. Airports and airlines are increasingly adopting electric ground support equipment as part of their environmental strategies to reduce emissions and comply with stringent regulatory standards. Electric belt loaders offer several advantages, including zero tailpipe emissions, lower operating costs, reduced maintenance requirements, and quieter operation compared to traditional diesel-powered units. This transition is particularly pronounced in developed markets such as North America and Europe, where regulatory pressure and sustainability commitments are stronger. However, emerging economies in the Asia Pacific are also rapidly adopting electric GSE solutions as part of new airport development projects. Manufacturers that focus on developing advanced electric belt loaders with longer battery life, faster charging capabilities, and improved load handling are well-positioned to capitalize on this growing opportunity. Additionally, the increasing adoption of leasing and rental models for ground support equipment is creating new growth avenues for manufacturers and service providers. Airlines and ground handlers are increasingly opting for flexible ownership models to reduce capital expenditure, further expanding the addressable market for belt loader suppliers. As sustainability and operational efficiency continue to dominate procurement decisions, electrification is expected to remain a key opportunity area in the belt loader market

Belt Loader Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 1.5 Billion |

|

Market Forecast in 2035 |

USD 2.6 Billion |

|

CAGR % 2025-2035 |

7.3% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2035 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Ownership, By

System, By Weight |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Belt Loader Market Report

Segmentation Analysis

The Global Belt Loader Market

Industry Analysis Is Segmented By Ownership, By System, By Weight, By

Geography, and By Region.

New Delivery Segment Accounted for the Largest Market Share

in the Global Belt Loader Market

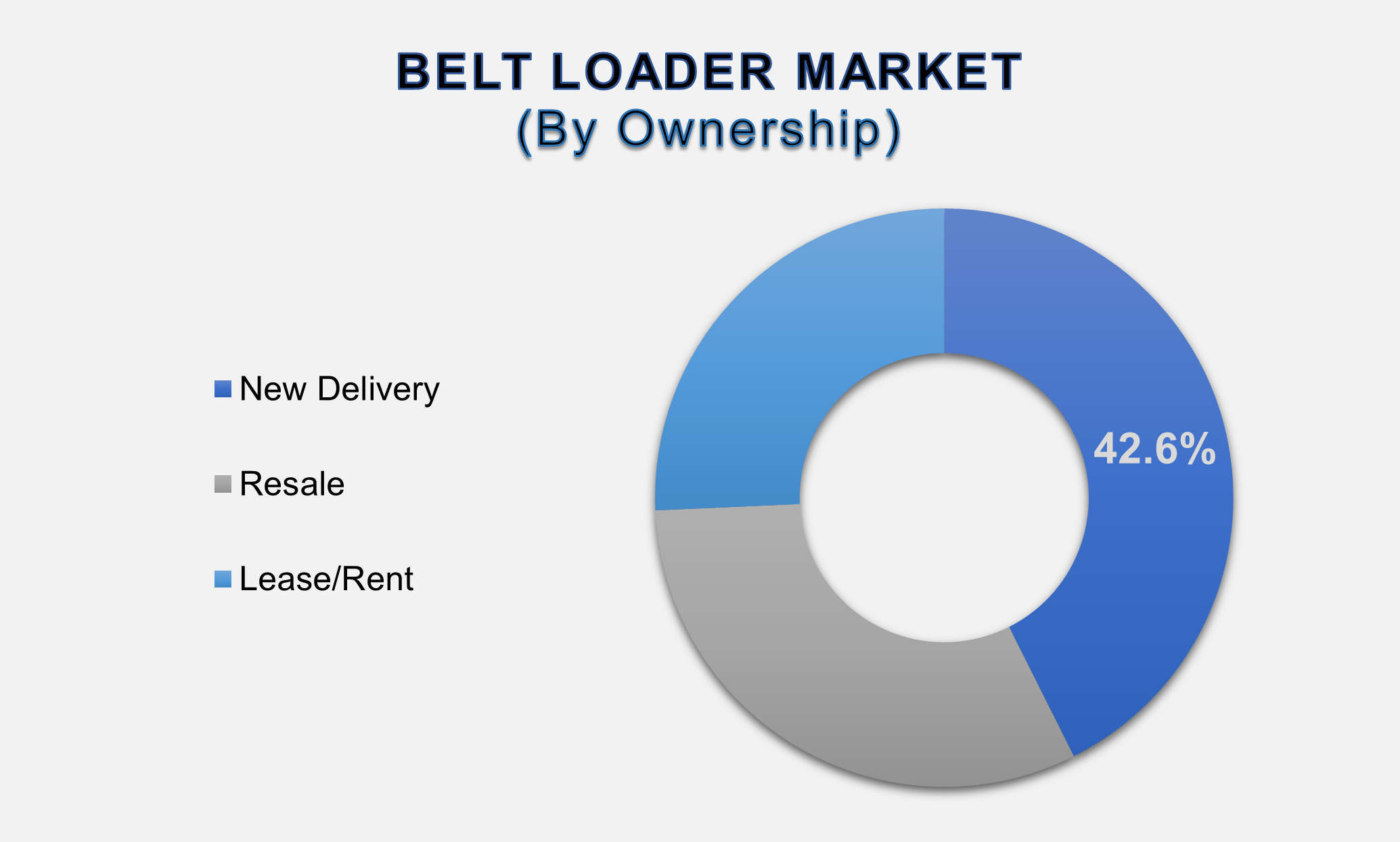

The new delivery segment accounted for the largest market share of 42.6% in 2025 and continues to dominate the global belt loader market. This dominance is primarily attributed to ongoing airport expansion projects, fleet modernization initiatives, and the replacement of aging ground support equipment. Airports and airlines increasingly prefer new belt loaders equipped with advanced safety features, improved ergonomics, and enhanced reliability to meet modern operational standards. Newly delivered belt loaders also comply with the latest emission regulations and sustainability requirements, making them more attractive than refurbished or resale equipment. Additionally, manufacturers are offering customized solutions tailored to specific aircraft types and airport layouts, further driving demand for new equipment. As airports continue to invest in long-term infrastructure development, the new delivery segment is expected to maintain its leading position throughout the forecast period.

Self-Propelled

System Segment Held the Leading Share Owing to Operational Efficiency

The

self-propelled system segment holds a significant share of the global belt

loader market, driven by its superior maneuverability, operational flexibility,

and reduced dependency on towing vehicles. Self-propelled belt loaders enable

faster positioning and repositioning during aircraft turnaround operations,

contributing to improved ground handling efficiency. These systems are

particularly favored at large and busy airports where minimizing ground time is

critical. Additionally, self-propelled belt loaders are increasingly being

integrated with electric powertrains, aligning with sustainability goals and

reducing operating costs. The combination of performance efficiency and

environmental benefits is expected to sustain strong demand for self-propelled

belt loaders in the coming years.

0–1000

Kg Weight Segment Dominated Due to High Usage in Narrow-Body Aircraft

Operations

The

0–1000 kg weight segment accounted for a substantial share of the market in

2025, primarily due to its widespread use in narrow-body and regional aircraft

operations. These belt loaders are ideal for handling passenger baggage and

light cargo, making them suitable for most commercial flights operated by

low-cost and regional carriers. Their compact size, ease of operation, and

lower acquisition costs make them a preferred choice for airports with

high-frequency short-haul flights. As narrow-body aircraft continue to dominate

airline fleets globally, the demand for belt loaders in the 0–1000 kg capacity

range is expected to remain strong during the forecast period.

The following segments are

part of an in-depth analysis of the global Belt Loader market:

|

Market Segments |

|

|

By Ownership |

●

New Delivery ●

Resale ●

Lease/Rent |

|

By System |

●

Self-Propelled ●

Electric ●

Towable ●

Diesel ●

Others |

|

By Weight |

●

0-1000 Kg ●

1000–5000 kg ●

<5000 Kg |

Belt Loader Market Share

Analysis by Region

North America is

anticipated to hold the biggest portion of the Belt Loader Market globally

throughout the forecast period.

North America accounted for the

largest share of 45.9% of the global belt loader market in 2025, driven by high

air traffic volumes, a well-established aviation infrastructure, and early

adoption of advanced ground support equipment. The presence of major

international airports, extensive airline networks, and strong investment in

airport modernization projects has significantly contributed to market growth

in the region. Additionally, stringent safety regulations and sustainability

initiatives have accelerated the replacement of legacy equipment with modern

belt loaders, further supporting regional dominance.

The Asia Pacific region is

expected to witness the highest CAGR during the forecast period, fueled by

rapid growth in air passenger traffic, expanding airline fleets, and

large-scale airport construction projects across countries such as China,

India, and Southeast Asian nations. Governments in the region are investing

heavily in aviation infrastructure to support economic growth and tourism,

leading to increased procurement of ground support equipment. The rising

adoption of electric belt loaders and flexible ownership models is further

expected to boost market growth across the Asia Pacific.

Belt Loader Market

Competition Landscape Analysis

The global belt loader market is

moderately consolidated, with key players focusing on product innovation,

geographic expansion, and strategic partnerships. Leading companies are

investing in electric and hybrid belt loaders to align with sustainability trends

while expanding their service networks to strengthen customer relationships.

Competitive strategies include mergers, acquisitions, and long-term contracts

with airports and ground handling companies.

Global Belt Loader Market

Recent Developments News:

- In September 2024 – Wollard International unveiled

its new M100e belt loader at the Europe GSE Expo. Designed for heavy-duty

operations, it has a drawbar rating of 8,000–12,000 pounds and can

function for two full shifts on a single charge.

- In September 2024 – Power Stow introduced a new

tail loader, a specialized belt loader designed to bridge the gap between

baggage carts and belt loaders. It improves operational efficiency by

handling heavy lifting and complex maneuvering during baggage handling.

- In July 2024 – CVC DIF, a subsidiary of CVC Capital

Partners, acquired HiSERV, a leading Germany-based aviation ground support

equipment (GSE) leasing company. HiSERV provides GSE leasing, maintenance,

and repair services across European airports.

- In March 2024 – Mallaghan partnered with Delta Air

Lines to supply the airline with its advanced SkyBelt belt loaders,

designed for higher operational efficiency.

- In April 2023 – Delta Air Lines announced that

nearly all ground support equipment (tugs, belt loaders, tractors) at its

major hub in Boston Logan International Airport is now electric, marking a

significant step toward achieving net-zero ground operations.

The Global Belt Loader Market Is

Dominated by a Few Large Companies, such as

●

TLD Group

●

Mallaghan Engineering

●

Mulag

●

Tug Technologies

●

Charlatte America

●

Fast Global Solutions

●

JBT AeroTech

●

Tronair

●

Aircraft GSE

●

Weihai Guangtai

●

Sovam

●

NMC-Wollard

●

LAS-1 Company

●

Aviaco GSE

●

Nepean

●

TBD

●

TREPEL

●

Power Force

●

SMI

●

SACI

● Others

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Belt Loader Market

Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Belt Loader Market Scope and Market Estimation

1.2.1.Global Belt Loader Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Belt Loader Market

Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Ownership of Global Belt

Loader Market

1.3.2.System of Global Belt

Loader Market

1.3.3.Weight of Global Belt

Loader Market

1.3.4.Region of Global Belt

Loader Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Belt Loader Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Belt Loader Market Estimates

& Forecast Trend Analysis, by Ownership

4.1.

Global

Belt Loader Market Revenue (US$ Bn) Estimates and Forecasts, by Ownership, 2020

- 2033

4.1.1.New Delivery

4.1.2.Resale

4.1.3.Lease/Rent

5. Global

Belt Loader Market Estimates

& Forecast Trend Analysis, by System

5.1.

Global

Belt Loader Market Revenue (US$ Bn) Estimates and Forecasts, by System, 2020 - 2033

5.1.1.Self-Propelled

5.1.2.Electric

5.1.3.Towable

5.1.4.Diesel

5.1.5.Others

6. Global

Belt Loader Market Estimates

& Forecast Trend Analysis, by Weight

6.1.

Global

Belt Loader Market Revenue (US$ Bn) Estimates and Forecasts, by Weight, 2020 -

2033

6.1.1.0-1000 Kg

6.1.2.1000 – 5000 Kg

6.1.3.<5000 Kg

7. Global

Belt Loader Market Estimates

& Forecast Trend Analysis, by Region

7.1.

Global

Belt Loader Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Belt

Loader Market: Estimates & Forecast

Trend Analysis

8.1.

North

America Belt Loader Market Assessments & Key Findings

8.1.1.North America Belt Loader

Market Introduction

8.1.2.North America Belt Loader

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Ownership

8.1.2.2. By System

8.1.2.3. By Weight

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Belt

Loader Market: Estimates & Forecast

Trend Analysis

9.1.

Europe

Belt Loader Market Assessments & Key Findings

9.1.1.Europe Belt Loader Market

Introduction

9.1.2.Europe Belt Loader Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Ownership

9.1.2.2. By System

9.1.2.3. By Weight

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Belt

Loader Market: Estimates & Forecast

Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Belt Loader Market Introduction

10.1.2.

Asia

Pacific Belt Loader Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Ownership

10.1.2.2. By System

10.1.2.3. By Weight

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Belt

Loader Market: Estimates & Forecast

Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Belt Loader Market Introduction

11.1.2.

Middle East & Africa Belt Loader Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Ownership

11.1.2.2. By System

11.1.2.3. By Weight

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Belt Loader Market: Estimates &

Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Belt Loader Market Introduction

12.1.2.

Latin

America Belt Loader Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1. By Ownership

12.1.2.2. By System

12.1.2.3. By Weight

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Belt Loader Market Product Mapping

14.2.

Global

Belt Loader Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3.

Global

Belt Loader Market Tier Structure Analysis

14.4.

Global

Belt Loader Market Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

TLD Group

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. Mallaghan

Engineering

15.3. Mulag

15.4. Tug

Technologies

15.5. Charlatte

America

15.6. Fast

Global Solutions

15.7. JBT

AeroTech

15.8. Tronair

15.9. Aircraft

GSE

15.10. Weihai

Guangtai

15.11. Sovam

15.12. NMC-Wollard

15.13. LAS-1

Company

15.14. Aviaco

GSE

15.15. Nepean

15.16. TBD

15.17. TREPEL

15.18. Power

Force

15.19. SMI

15.20. SACI

15.21. Others

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables