Biodegradable Cups Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Product Type (Hot Beverage Cups, Cold Beverage Cups, Soups & Broths Cups and Others); By Material (Polylactic Acid (PLA) & Blends, Paper & Paperboard, Bagasse and Others (PHA, Starch Blends)); By End-User (Foodservice Outlets, Institutional Catering, Households and Others) and Geography

2025-11-04

Consumer Products

Jaya Bundele (Research Analyst)

Description

Biodegradable Cups Market Overview

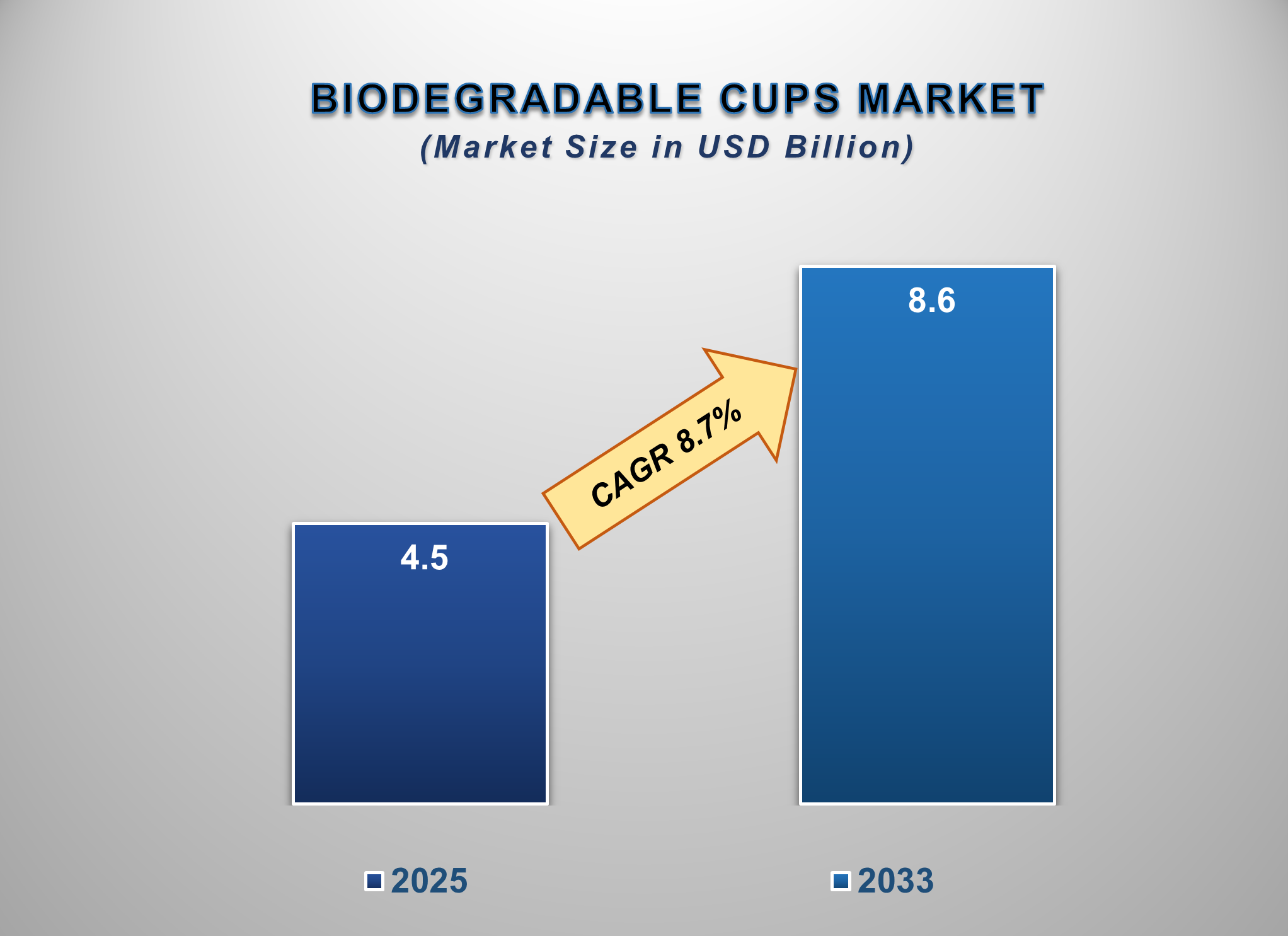

The global biodegradable cups market is poised for substantial growth from 2025 to 2033, driven by escalating consumer environmental awareness, stringent government regulations against single-use plastics, and a corporate shift towards sustainable packaging. Valued at approximately USD 4.5 billion in 2025, the market is projected to surge to USD 8.6 billion by 2033, reflecting a robust compound annual growth rate (CAGR) of 8.7% during the forecast period.

The market is expanding rapidly

as biodegradable cups become a mainstream solution for the foodservice

industry. These cups, made from materials like polylactic acid (PLA), paper

with PLA linings, bagasse, and other plant-based polymers, offer a reduced environmental

footprint compared to conventional plastic. Growth is primarily fueled by the

global movement to phase out single-use plastics, with bans and taxes being

implemented in numerous countries. The proliferation of coffee chains,

quick-service restaurants (QSRs), and the online food delivery ecosystem are

key end-users adopting these sustainable alternatives.

While North America and Europe

lead the market due to early regulatory action and high consumer consciousness,

the Asia-Pacific region is expected to be the fastest-growing market, fueled by

rapid urbanization, a growing middle class, and increasing government focus on

waste management. The market is characterized by the presence of global

packaging giants and specialized sustainable manufacturers, with competition

centering on material innovation, cost-effectiveness, supply chain reliability,

and certifications for compostability.

Biodegradable Cups Market

Drivers and Opportunities

Stringent Government Regulations and Plastic Bans

The most significant driver for the biodegradable

cups market is the increasing number of government mandates aimed at reducing

plastic pollution. Bans on single-use plastics, including conventional

polystyrene and polypropylene cups, in regions like Europe, Canada, and parts

of the US and Asia, are compelling foodservice operators to seek compliant

alternatives. Legislation such as the EU's Single-Use Plastics Directive

directly creates a massive, regulated demand for biodegradable and compostable

products, ensuring market growth.

Rising Consumer Environmental Awareness and Demand

A profound shift in consumer preferences towards

eco-friendly brands and products is a powerful market force. Environmentally

conscious consumers are actively choosing brands that demonstrate a commitment

to sustainability, pressuring major corporations in the beverage and food

industry to switch to biodegradable packaging. This consumer-driven demand is

no longer a niche trend but a mainstream expectation, making sustainable cups a

key element of brand image and corporate social responsibility (CSR) strategies.

Opportunity for the Biodegradable Cups Market

Material

Innovation and Expansion in Emerging Economies

A significant opportunity lies in the development

of next-generation biodegradable materials that offer better performance, such

as higher heat resistance for hot beverages and improved barrier properties to

prevent leakage, at a lower cost. Furthermore, the burgeoning foodservice

markets in emerging economies across Asia-Pacific, Latin America, and Africa

present a substantial growth frontier. As these regions grapple with plastic

waste and their middle-class populations expand, there is immense potential for

market penetration. Companies that can establish local manufacturing

partnerships and offer cost-competitive, certified compostable solutions

tailored to regional preferences are well-positioned to capture this

high-growth potential.

Biodegradable Cups Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 4.5 Billion |

|

Market Forecast in 2033 |

USD 8.6 Billion |

|

CAGR % 2025-2033 |

8.7% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, Company Share, Company Heatmap, Company

Production, Service Type, Growth Factors, and more |

|

Segments Covered |

●

By Product Type ●

By Material ●

By End-user |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Netherlands 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19)

Egypt 20) South Africa |

Biodegradable Cups Market

Report Segmentation Analysis

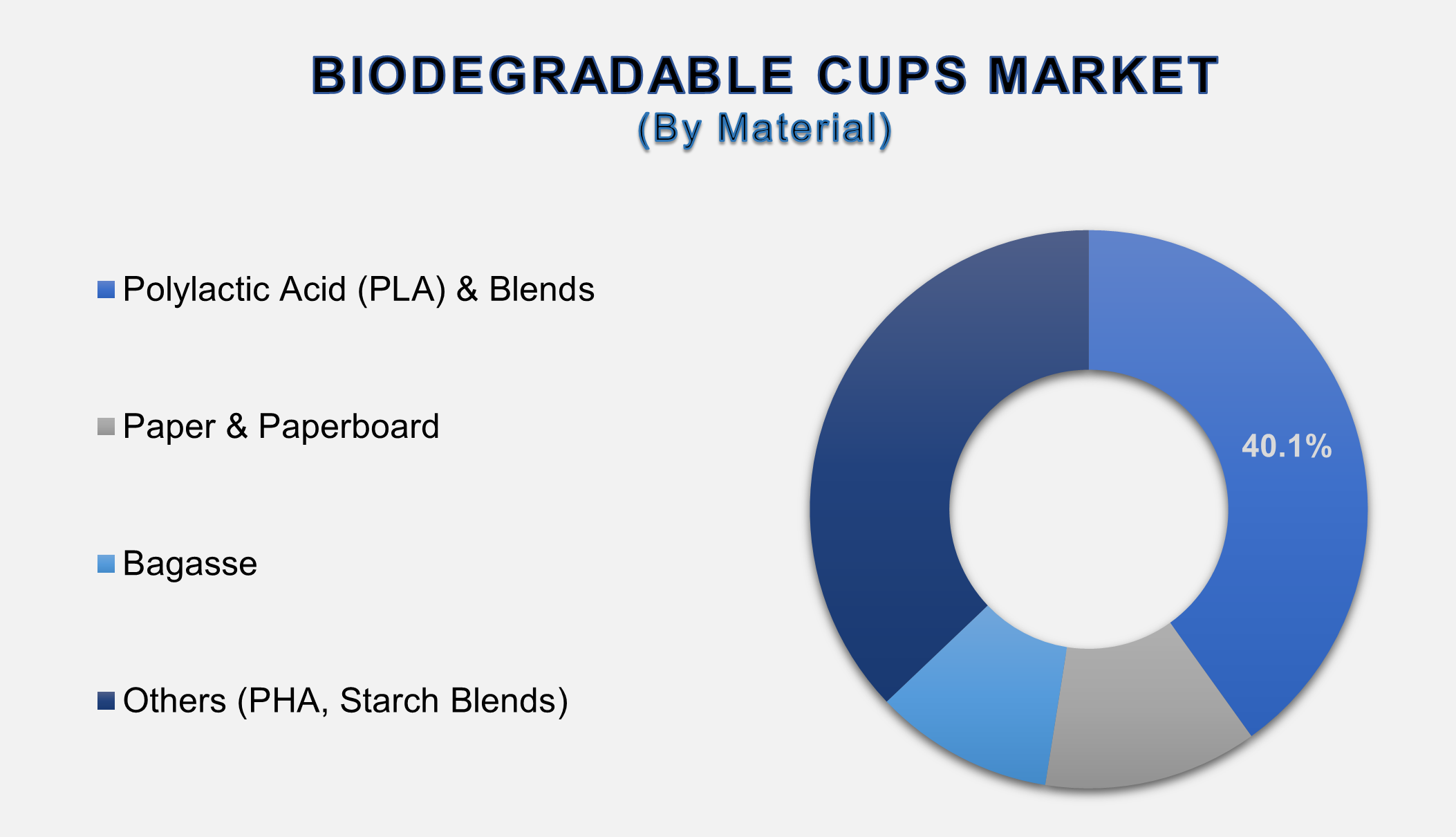

The

global Biodegradable Cups Market industry analysis is segmented by Material, by

Product Type, by End-user, and by region.

Polylactic Acid (PLA) & Blends Segment Dominance

The dominance of the Polylactic Acid (PLA) and

blends segment is rooted in its unique combination of functionality,

sustainability, and processability. As a biopolymer derived from fermented

plant sugars, typically cornstarch, PLA offers a compelling environmental narrative of being

bio-based and industrially compostable. Functionally, its clarity and rigidity

make it the premier material for clear cold cups, mimicking the appearance of

conventional petroleum-based plastics like PET, while its application as a

thin, effective lining inside paper cups makes it indispensable for hot

beverages. This versatility allows it to serve a dual market. Crucially, PLA

can be processed on standard plastic manufacturing equipment like thermoformers

and injection molders, enabling converters to pivot to sustainable production

with minimal capital investment. This blend of consumer appeal, a strong

sustainability profile, and seamless integration into existing supply chains

solidifies PLA's position as the market-leading material, bridging the gap

between traditional plastic performance and eco-friendly objectives.

Hot Beverage Cups Segment Contribution

The hot beverage cups segment is a major market

contributor, propelled by the immense global scale of coffee and tea

consumption. The daily ritual of buying a hot drink from cafes, quick-service

restaurants, and convenience stores generates a consistent, high-volume demand

that forms the backbone of the single-use cup industry. The primary technical

challenge for biodegradable options in this segment has been creating a product

that can withstand high temperatures, prevent leakage, and provide adequate insulation

for the user. Innovation has successfully addressed this through the widespread

adoption of paper cups lined with a thin layer of PLA. This combination

leverages the structural integrity and heat-insulating properties of paper with

the moisture-resistant, biodegradable barrier of PLA. As global coffee culture

continues to flourish and major chains actively phase out conventional

polyethylene-lined cups, the demand for these high-performance, compostable hot

cup solutions is set for sustained growth.

Foodservice End-User Segment Dominance

The foodservice end-user segment's dominance is a

direct consequence of its position at the epicenter of consumer demand,

regulatory pressure, and industry transformation. This segment, encompassing

coffee shops, quick-service restaurants, hotels, and delivery services, is the

primary point of consumption for single-use cups. These businesses face intense

and direct pressure from two fronts: environmentally conscious consumers who

prefer brands with sustainable practices and increasingly stringent government

regulations banning conventional single-use plastics.

Adopting biodegradable cups has become a critical

business imperative for brand image, regulatory compliance, and customer

retention. Furthermore, the explosive growth of online food delivery platforms

has exponentially increased this segment's reliance on single-use packaging.

These platforms often promote "green" packaging as a feature, pushing

their restaurant partners to adopt biodegradable options. This convergence of

social, regulatory, and commercial drivers makes the foodservice industry the

undisputed largest and most dynamic consumer of biodegradable cups.

The following segments are part of an in-depth analysis of the global

Biodegradable Cups Market:

|

Market Segments |

|

|

By Product Type |

●

Hot Beverage Cups ●

Cold Beverage Cups ●

Soups & Broths

Cups ●

Others |

|

By Material |

●

Polylactic Acid

(PLA) & Blends ●

Paper &

Paperboard ●

Bagasse ●

Others (PHA, Starch

Blends) |

|

By End-user |

●

Foodservice Outlets ●

Institutional

Catering ●

Households ●

Others |

Biodegradable Cups Market

Share Analysis by Region

The North America region is expected to

dominate the Global Biodegradable Cups Market during the forecast period.

North America is anticipated to lead the

global market, driven by early and widespread municipal bans on single-use

plastics, high consumer awareness, and the presence of major global coffee

chains and QSRs that have proactively committed to sustainable packaging. For

instance, several states in the U.S. and cities in Canada have implemented

strict regulations, creating a compliance-driven market. The region's strong packaging industry and focus

on technological innovation in bioplastics further consolidate its dominant

position.

Global Biodegradable Cups

Market Recent Developments News:

- In January 2025, a major consortium of coffee

chains announced a joint initiative to standardize the collection and

industrial composting of their PLA-based cups in key North American and

European cities.

- In February 2025, Dart Container Corporation (a

Novolex brand) launched a new line of biodegradable cold cups made from a

novel PHA blend, offering enhanced marine biodegradability.

- In March 2025, Huhtamaki partnered with a leading

chemical company to develop a fully bio-based and biodegradable barrier

coating to replace the traditional PLA lining in paper cups, improving

recyclability.

- In April 2025, Starbucks expanded its "Bring

Your Own Cup" incentive program globally and reported that over 25%

of its beverages in key markets are now served in reusable or certified

compostable cups.

The Global Biodegradable

Cups Market is dominated by a few large companies, such as

●

Dart Container

Corporation

●

Huhtamaki Oyj

●

Graphic Packaging

International, LLC

●

Genpak, LLC

●

Pactiv LLC

●

Georgia-Pacific LLC

●

Detmold Group

●

Biopac UK Ltd.

●

Eco-Products, Inc.

●

Benders Paper Cups

●

Lollicup USA Inc.

●

Berry Global Inc.

●

Fabri-Kal Corporation

●

Fast Plast A/S

●

BioPak

●

Vegware Ltd.

●

Duni AB

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Biodegradable Cups

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Biodegradable Cups Market Scope and Market Estimation

1.2.1.Global Biodegradable Cups

Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Biodegradable Cups

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product Type of Global Biodegradable

Cups Market

1.3.2.Material Type of Global Biodegradable

Cups Market

1.3.3.End-user of Global Biodegradable

Cups Market

1.3.4.Region of Global Biodegradable

Cups Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Biodegradable Cups Market

2.8.

Key

Products/Brand Analysis

2.9.

Pricing

Analysis

2.10.

Porter’s

Five Forces Analysis

2.11.

PEST

Analysis

2.12.

Key

Regulation

3. Global

Biodegradable Cups Market Estimates

& Historical Trend Analysis (2020 - 2024)

4.

Global Biodegradable Cups

Market Estimates & Forecast Trend

Analysis, by Product Type

4.1.

Global

Biodegradable Cups Market Revenue (US$ Bn) Estimates and Forecasts, by Product

Type, 2020 - 2033

4.1.1.Hot Beverage Cups

4.1.2.Cold Beverage Cups

4.1.3.Soups & Broths Cups

4.1.4.Others

5.

Global Biodegradable Cups

Market Estimates & Forecast Trend

Analysis, by Material Type

5.1.

Global

Biodegradable Cups Market Revenue (US$ Bn) Estimates and Forecasts, by Material

Type, 2020 - 2033

5.1.1.Polylactic Acid (PLA)

& Blends

5.1.2.Paper & Paperboard

5.1.3.Bagasse

5.1.4.Others (PHA, Starch

Blends)

6.

Global Biodegradable Cups

Market Estimates & Forecast Trend

Analysis, by End-user

6.1.

Global

Biodegradable Cups Market Revenue (US$ Bn) Estimates and Forecasts, by End-user,

2020 - 2033

6.1.1.Foodservice Outlets

6.1.2.Institutional Catering

6.1.3.Households

6.1.4.Others

7. Global

Biodegradable Cups Market Estimates

& Forecast Trend Analysis, by region

1.1.

Global

Biodegradable Cups Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020

- 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East & Africa

1.1.5.Latin America

8. North America Biodegradable

Cups Market: Estimates & Forecast

Trend Analysis

8.1. North America Biodegradable

Cups Market Assessments & Key Findings

8.1.1.North America Biodegradable

Cups Market Introduction

8.1.2.North America Biodegradable

Cups Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Product

Type

8.1.2.2. By Material

Type

8.1.2.3. By End-user

8.1.2.4.

By

Country

8.1.2.4.1.

The

U.S.

8.1.2.4.2.

Canada

9. Europe Biodegradable

Cups Market: Estimates & Forecast

Trend Analysis

9.1.

Europe

Biodegradable Cups Market Assessments & Key Findings

9.1.1.Europe Biodegradable Cups

Market Introduction

9.1.2.Europe Biodegradable Cups

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product

Type

9.1.2.2. By Material

Type

9.1.2.3. By End-user

9.1.2.4.

By

Country

9.1.2.4.1. Germany

9.1.2.4.2. Italy

9.1.2.4.3. U.K.

9.1.2.4.4. France

9.1.2.4.5. Spain

9.1.2.4.6. Netherland

9.1.2.4.7.

Rest of Europe

10. Asia Pacific Biodegradable

Cups Market: Estimates & Forecast

Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Biodegradable Cups Market Introduction

10.1.2.

Asia

Pacific Biodegradable Cups Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

10.1.2.1. By Product

Type

10.1.2.2. By Material

Type

10.1.2.3. By End-user

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6.

Rest

of Asia Pacific

11. Middle East & Africa Biodegradable

Cups Market: Estimates & Forecast

Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Biodegradable Cups Market

Introduction

11.1.2.

Middle East & Africa Biodegradable Cups Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Product

Type

11.1.2.2. By Material

Type

11.1.2.3. By End-user

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4.

Rest of MEA

12. Latin America

Biodegradable Cups Market: Estimates

& Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Biodegradable Cups Market Introduction

12.1.2.

Latin

America Biodegradable Cups Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

12.1.2.1. By Product

Type

12.1.2.2. By Material

Type

12.1.2.3. By End-user

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Mexico

12.1.2.4.3. Argentina

12.1.2.4.4.

Rest of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Biodegradable Cups Market Product Mapping

14.2.

Global

Biodegradable Cups Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3.

Global

Biodegradable Cups Market Tier Structure Analysis

14.4.

Global

Biodegradable Cups Market Concentration & Company Market Shares (%)

Analysis, 2024

15.

Company

Profiles

15.1. Dart

Container Corporation

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all

the players mentioned below

15.2. Huhtamaki Oyj

15.3. Graphic

Packaging International, LLC

15.4. Genpak,

LLC

15.5. Pactiv

LLC

15.6. Georgia-Pacific

LLC

15.7. Detmold Group

15.8. Biopac UK

Ltd.

15.9. Eco-Products,

Inc.

15.10. Benders Paper

Cups

15.11. Lollicup® USA

Inc.

15.12. Berry Global

Inc.

15.13. Fabri-Kal

Corporation

15.14. Fast Plast

A/S

15.15. BioPak

15.16. Vegware Ltd.

15.17. Duni AB

15.18. Other

Prominent Players

16. Research

Methodology

16.1.

External

Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables