Blue Hydrogen Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Technology (Steam Methane Reforming, Gas Partial Oxidation, Auto Thermal Reforming), By Transportation (Pipeline, Cryogenic Liquid Tankers, Others), By Application (Chemicals, Refinery, Power Generation, Others), and Geography

2026-01-02

Energy & Power

Ekta Chaurasia (Team Lead)

Description

Blue Hydrogen Market Overview

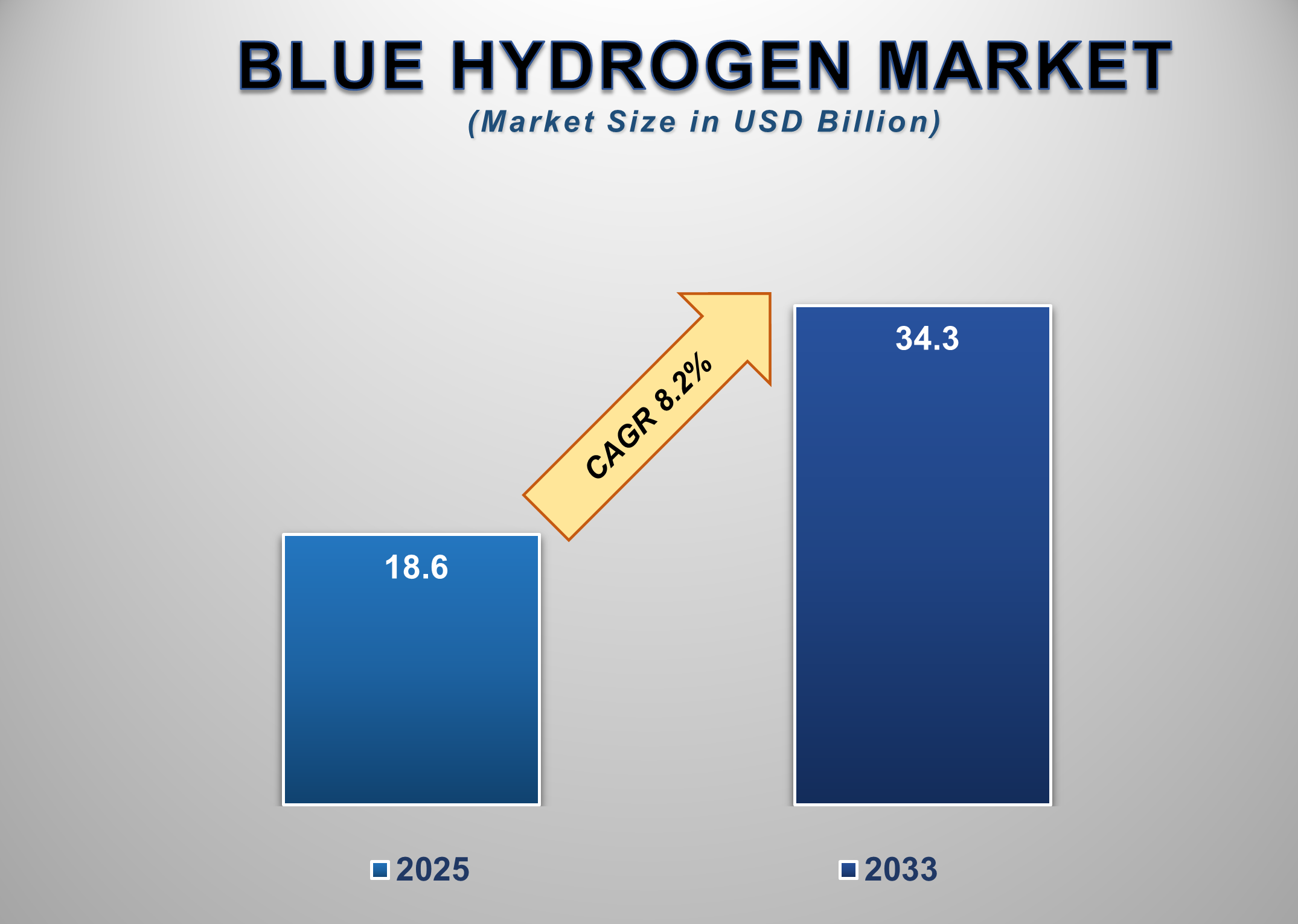

The global blue hydrogen market is expanding rapidly as the world accelerates its shift toward cleaner fuels and low-carbon industrial processes. Valued at USD 18.6 billion in 2025, the market is projected to grow to USD 34.3 billion by 2033, registering a strong CAGR of 8.2%. Blue hydrogen produced from natural gas with carbon capture, utilization, and storage (CCUS) has emerged as a critical transitional energy source capable of decarbonizing hard-to-abate sectors such as power generation, refining, ammonia production, and heavy industry. As global governments commit to net-zero targets, demand for low-emission hydrogen continues to surge across both developed and emerging markets.

Growing investment in CCUS

infrastructure, rising carbon taxes, and strong policy support for clean

hydrogen are key drivers of market growth. The hydrogen sector is also

benefitting from multi-billion-dollar funding programs in the U.S., Canada,

Europe, Japan, and South Korea aimed at establishing hydrogen hubs, advancing

transportation corridors, and enabling industrial-scale adoption. Blue hydrogen

offers a viable pathway to accelerate the broader hydrogen economy by providing

large-scale volumes at competitive costs compared to green hydrogen, which is

still limited by electrolyzer availability and renewable energy economics. Over

the forecast period, the integration of CCUS with natural gas reforming will

play a decisive role in accelerating the global energy transition, reinforcing

blue hydrogen’s position as a cornerstone of clean energy strategies.

Blue Hydrogen Market

Drivers and Opportunities

Escalating Global

Decarbonization Mandates Are Driving Large-Scale Adoption of Blue Hydrogen

Global commitments to carbon neutrality are causing a fundamental

shift in industrial, energy, and mobility systems, positioning blue hydrogen as

an essential decarbonization solution. Governments worldwide are implementing

stringent emission standards and carbon pricing mechanisms, compelling

industries to transition toward cleaner feedstocks and low-emission fuels. Blue

hydrogen allows companies to significantly cut CO₂ emissions while leveraging

existing natural gas infrastructure, enabling a smoother and more economically

viable transition compared to immediate adoption of green hydrogen. Major

economies, including the United States, the UK, Germany, Canada, Japan, and

South Korea, are developing hydrogen roadmaps that allocate substantial funding

and policy incentives for hydrogen production using carbon capture

technologies. Industrial clusters such as steel, cement, refining, and

chemicals are adopting blue hydrogen to comply with carbon reduction

regulations while maintaining operational efficiency. The commercial

transportation sector is also evaluating blue hydrogen as a potential fuel for

heavy-duty trucks, ships, and aviation, where electrification remains

technically challenging. The rapid expansion of CCUS capacity and technological

advancements in carbon capture rates are strengthening the business case for

blue hydrogen. With global emissions policies tightening and fossil-based

industries under increasing scrutiny, the demand for blue hydrogen is expected

to grow significantly through 2033.

Growing Investment in CCUS Infrastructure and Natural Gas

Reforming Is Strengthening Market Growth

Carbon capture, utilization, and storage (CCUS) technologies are

evolving rapidly, allowing natural gas reforming processes to produce hydrogen

with minimal carbon emissions. Steam methane reforming (SMR) and auto-thermal

reforming (ATR) combined with high-efficiency CO₂ capture systems are becoming

the preferred technologies for large-scale blue hydrogen production. As global

CCUS infrastructure expands, operational costs are decreasing, making blue

hydrogen competitive with conventional hydrogen and, in some regions, even with

early-stage green hydrogen. Globally, governments and private companies are

announcing large-scale CCUS investments and pipeline networks designed to

transport captured CO₂ to permanent storage sites. The U.S. Inflation Reduction

Act (IRA), EU Innovation Fund, Canada’s CCUS tax credits, and the UK’s Carbon

Capture & Storage Clusters are accelerating deployment at unprecedented

speed. Industrial players in oil & gas, refining, chemicals, and

fertilizers are integrating blue hydrogen into their long-term decarbonization

strategies to reduce carbon exposure and stabilize future operations.

Emerging Economies’ Industrialization and Energy Transition

Creating Strong Growth Opportunities

Emerging economies, particularly in Asia Pacific, the Middle East,

and Latin America, represent an enormous opportunity for blue hydrogen

adoption. As these regions expand industrial production, strengthen energy

security, and pursue emission reduction goals, hydrogen is gaining strategic

importance in national energy plans. Countries such as India, China, Saudi

Arabia, the UAE, and Brazil are investing heavily in building hydrogen-ready

infrastructure, expanding natural gas networks, and developing CCUS capabilities

to support blue hydrogen production. Rapid growth in refining, petrochemicals,

ammonia, and steel sectors in these regions is driving the need for cleaner

industrial feedstocks. Blue hydrogen, with its cost advantages over green

hydrogen and compatibility with existing industrial systems, is emerging as the

preferred transition fuel. The Middle East, in particular, is positioning

itself as a global hydrogen export hub due to its abundant natural gas

reserves, low production costs, and strong government backing. Asia-Pacific

nations are also pursuing hydrogen imports to meet clean energy requirements,

creating demand for global-scale blue hydrogen production and transportation

networks. Infrastructure investments in hydrogen pipelines, LNG retrofit

systems, and CO₂ storage reservoirs will further elevate blue hydrogen’s role

in emerging markets. With supportive policies and rising industrial

requirements, emerging economies will remain pivotal in driving global blue

hydrogen demand through 2033.

Blue Hydrogen Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 18.6 Billion |

|

Market Forecast in 2033 |

USD 34.3 Billion |

|

CAGR % 2025-2033 |

8.2% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Technology,

Transportation, Application |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Blue Hydrogen Market

Report Segmentation Analysis

The blue hydrogen market is segmented into technology,

transportation, application, and geography.

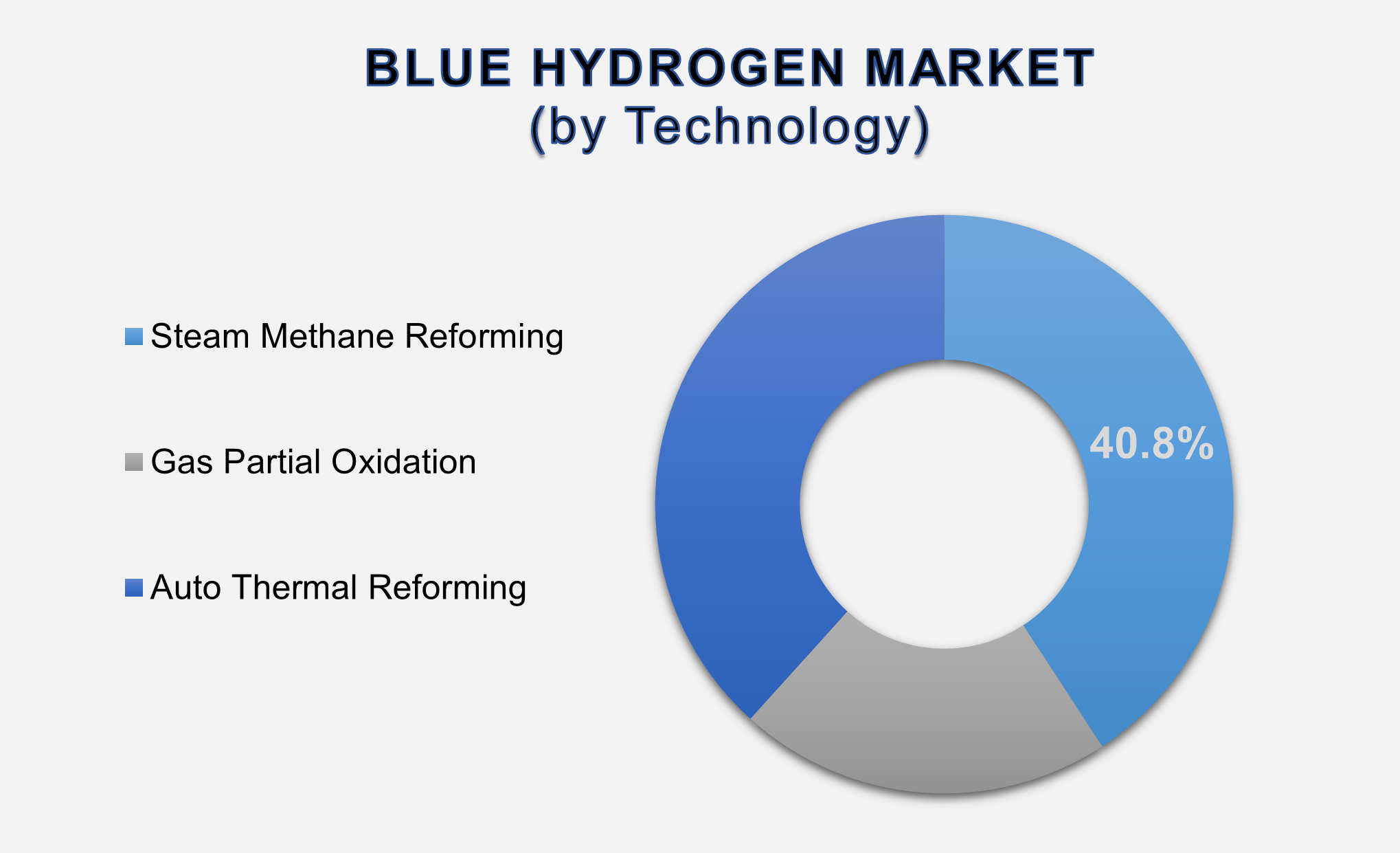

The Steam Methane

Reforming segment accounted for the largest market share in the global market.

Steam methane reforming (SMR) leads the global blue hydrogen market with a 40.8% share, supported by its technical maturity, large-scale deployment capabilities, and cost advantages compared to other reforming methods. SMR is widely used in refinery, chemical, and fertilizer industries due to its high hydrogen yield and compatibility with integrated CCUS systems. When combined with modern carbon capture technologies, SMR can achieve over 90–95% CO₂ capture efficiency, significantly reducing lifecycle emissions and making it one of the most commercially viable pathways for low-carbon hydrogen production. SMR’s well-established supply chain, existing natural gas infrastructure, and global availability of reforming technologies provide further advantages. The ongoing expansion of hydrogen hubs in the U.S., Canada, UK, and Middle East is heavily reliant on SMR due to its scalability and proven performance. Additionally, advancements in catalysts, process intensification, and heat integration are improving efficiency while lowering operating costs. As industries seek dependable and cost-effective solutions to decarbonize operations, SMR is expected to maintain its dominance through 2033, even as auto-thermal reforming gains traction for large-scale integrated CCUS projects.

Pipeline segment

accounted for the largest market share in the global market.

Pipeline transportation dominates

the blue hydrogen market due to its reliability, lower operational costs, and

suitability for high-volume hydrogen delivery to industrial clusters. Mature

natural gas pipeline networks allow repurposing of existing infrastructure for

hydrogen blends or pure hydrogen transport, significantly reducing new capital

investment requirements. Industrial facilities located within large energy hubs

such as those in North America, Europe, and the Middle East are particularly

well-positioned to benefit from pipeline-based hydrogen movement. Hydrogen

pipelines support continuous supply to refineries, chemical plants, power

stations, and steel industries, enabling efficient integration into downstream

processes. Several countries are developing hydrogen corridor projects to

expand pipeline networks, including the European Hydrogen Backbone (EHB), U.S.

Gulf Coast hydrogen pipelines, and large-scale infrastructure initiatives in

Japan and South Korea. As hydrogen demand accelerates, pipeline networks will

play a critical role in establishing long-term, cost-effective supply systems.

While cryogenic liquid tankers and carriers serve long-distance transport and

export markets, pipelines remain the preferred mode for industrial regions

where demand is concentrated. With increasing government support and

infrastructure modernization programs, the pipeline segment will continue to

grow steadily throughout the forecast period.

The Chemicals segment

accounted for the largest market share in the global market.

The chemicals segment leads the

global market, driven by extensive hydrogen use in ammonia production, methanol

synthesis, and various industrial chemical processes. Blue hydrogen is becoming

increasingly important as chemical manufacturers aim to reduce carbon emissions

from large-scale production facilities while maintaining output efficiency.

Ammonia plants, in particular, represent one of the highest hydrogen-consuming

industries, making them prime adopters of low-carbon hydrogen pathways. Blue

hydrogen provides an economically viable substitute for conventional hydrogen

derived from natural gas without carbon capture, enabling industries to meet

carbon-neutrality targets while avoiding major disruptions to existing

processes. Growing demand for low-carbon ammonia as a fertilizer component and

emerging fuel source is further driving segment growth. Methanol producers also

rely on hydrogen, and integrating blue hydrogen into production lines allows

them to achieve substantial emission reductions. With increasing regulatory

pressure and expanding clean hydrogen adoption across chemical, fertilizer, and

petrochemical industries, the chemical segment is expected to remain the

primary consumer of blue hydrogen throughout the forecast period.

The following segments are

part of an in-depth analysis of the global Blue Hydrogen market:

|

Market Segments |

|

|

by Technology |

●

Steam Methane

Reforming ●

Gas Partial

Oxidation ●

Auto Thermal

Reforming |

|

by

Transportation |

●

Pipeline ●

Cryogenic Liquid

Tankers |

|

by Application |

●

Chemicals ●

Refinery ●

Power Generation ●

Others |

Blue Hydrogen Market

Share Analysis by Region

North America is

anticipated to hold the biggest portion of the Blue Hydrogen Market globally

throughout the forecast period.

North

America leads due to aggressive federal funding, rapid deployment of hydrogen

hubs, and strong industrial demand across refining, chemicals, and power

sectors. The U.S. Inflation Reduction Act (IRA) provides substantial tax

credits for hydrogen production and CCUS, significantly improving commercial

viability. The region also benefits from extensive natural gas reserves,

large-scale CCUS facilities, and ongoing pipeline development projects.

Canada’s hydrogen and CCUS strategy further strengthens regional leadership,

especially in Alberta and British Columbia. With significant investments in

hydrogen storage, pipelines, and export terminals, North America will continue

dominating the blue hydrogen landscape.

Asia-Pacific is expected to grow

at the highest CAGR. Asia-Pacific’s rapid growth is driven by strong

industrialization, rising energy demand, and national commitments to reduce

carbon emissions. China, Japan, South Korea, and India are investing heavily in

hydrogen ecosystems, including large-scale reforming units, CCUS

infrastructure, and hydrogen-ready industrial plants. Japan and South Korea are

exploring blue hydrogen imports to support transportation and power generation

sectors, while the Middle East is emerging as a key exporter to Asia-Pacific

markets. Supportive policies, energy transition targets, and expanding heavy

industries will continue powering APAC’s strong growth trajectory.

Blue Hydrogen Market

Competition Landscape Analysis

The global blue hydrogen market

is moderately consolidated, with major energy companies, industrial gas

manufacturers, and technology providers driving innovation and capacity

expansion. Key players focus on scaling CCUS-integrated hydrogen production, developing

large industrial hubs, and establishing transportation infrastructure.

Strategic partnerships between oil & gas companies, utilities, and

government agencies are accelerating project development.

Global Blue Hydrogen

Market Recent Developments News:

- In March 2022 – Air Products Inc. announced

the construction of a new zero-carbon liquid hydrogen production facility

in Casa Grande, Arizona. The plant is designed to support the growing

demand for clean hydrogen and is scheduled to be operational by 2023.

- In January 2022 – Linde plc signed an

agreement with Yara to build and supply a 24 MW electrolysis-based

hydrogen plant. The facility will produce clean hydrogen to support

decarbonization efforts in the industrial sector.

The Global Blue Hydrogen Market Is Dominated by a Few Large Companies, such as

●

Air Liquide

●

Air Products and

Chemicals

●

Linde

●

Shell

●

BP

●

ExxonMobil

●

TotalEnergies

●

Equinor

●

Siemens Energy

●

Mitsubishi Power

●

Kawasaki Heavy

Industries

●

Toshiba Energy Systems

●

Doosan Fuel Cell

●

Uniper

●

Engie

●

BASF

●

SABIC

●

Yara International

●

CF Industries

●

Haldor Topsoe

● Others

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Blue Hydrogen

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Blue Hydrogen Market Scope and Market Estimation

1.2.1.Global Blue Hydrogen Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Blue Hydrogen

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Technology of Global Blue

Hydrogen Market

1.3.2.Transportation of Global Blue

Hydrogen Market

1.3.3.Application of Global Blue

Hydrogen Market

1.3.4.Region of Global Blue

Hydrogen Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Blue Hydrogen Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Blue Hydrogen Market Estimates

& Forecast Trend Analysis, by Technology

4.1.

Global

Blue Hydrogen Market Revenue (US$ Bn) Estimates and Forecasts, by Technology, 2020

- 2033

4.1.1.Steam Methane Reforming

4.1.2.Gas Partial Oxidation

4.1.3.Auto Thermal Reforming

5. Global

Blue Hydrogen Market Estimates

& Forecast Trend Analysis, by Transportation

5.1.

Global

Blue Hydrogen Market Revenue (US$ Bn) Estimates and Forecasts, by Transportation,

2020 - 2033

5.1.1.Pipeline

5.1.2.Cryogenic Liquid Tankers

6. Global

Blue Hydrogen Market Estimates

& Forecast Trend Analysis, by Application

6.1.

Global

Blue Hydrogen Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

6.1.1.Chemicals

6.1.2.Refinery

6.1.3.Power Generation

6.1.4.Others

7. Global

Blue Hydrogen Market Estimates

& Forecast Trend Analysis, by Region

7.1.

Global

Blue Hydrogen Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020

- 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Blue

Hydrogen Market: Estimates &

Forecast Trend Analysis

8.1.

North

America Blue Hydrogen Market Assessments & Key Findings

8.1.1.North America Blue

Hydrogen Market Introduction

8.1.2.North America Blue

Hydrogen Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Technology

8.1.2.2. By Transportation

8.1.2.3. By Application

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Blue

Hydrogen Market: Estimates &

Forecast Trend Analysis

9.1.

Europe

Blue Hydrogen Market Assessments & Key Findings

9.1.1.Europe Blue Hydrogen

Market Introduction

9.1.2.Europe Blue Hydrogen

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Technology

9.1.2.2. By Transportation

9.1.2.3. By Application

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Blue

Hydrogen Market: Estimates &

Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Blue Hydrogen Market Introduction

10.1.2.

Asia

Pacific Blue Hydrogen Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Technology

10.1.2.2. By Transportation

10.1.2.3. By Application

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Blue

Hydrogen Market: Estimates &

Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Blue Hydrogen Market Introduction

11.1.2.

Middle East & Africa Blue Hydrogen Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Technology

11.1.2.2. By Transportation

11.1.2.3. By Application

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Blue Hydrogen Market: Estimates &

Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Blue Hydrogen Market Introduction

12.1.2.

Latin

America Blue Hydrogen Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1. By Technology

12.1.2.2. By Transportation

12.1.2.3. By Application

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Blue Hydrogen Market Product Mapping

14.2.

Global

Blue Hydrogen Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3.

Global

Blue Hydrogen Market Tier Structure Analysis

14.4.

Global

Blue Hydrogen Market Concentration & Company Market Shares (%) Analysis,

2024

15.

Company

Profiles

15.1.

Air Liquide

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. Air

Products and Chemicals

15.3. Linde

15.4. Shell

15.5. BP

15.6. ExxonMobil

15.7. TotalEnergies

15.8. Equinor

15.9. Siemens

Energy

15.10. Mitsubishi

Power

15.11. Kawasaki

Heavy Industries

15.12. Toshiba

Energy Systems

15.13. Doosan

Fuel Cell

15.14. Uniper

15.15. Engie

15.16. BASF

15.17. SABIC

15.18. Yara

International

15.19. CF

Industries

15.20. Haldor

Topsoe

15.21. Others

16. Research

Transportationology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables