Cardiovascular Devices Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Product (Diagnostic & Monitoring Devices, Surgical Devices); By Application (Coronary Artery Disease, Cardiac Arrhythmia, Heart Failure, Others); By End User (Hospitals, Specialty Clinics, Others); And Geography

2025-08-19

Healthcare

Swetal (Research Analyst)

Description

Cardiovascular Devices Market Overview

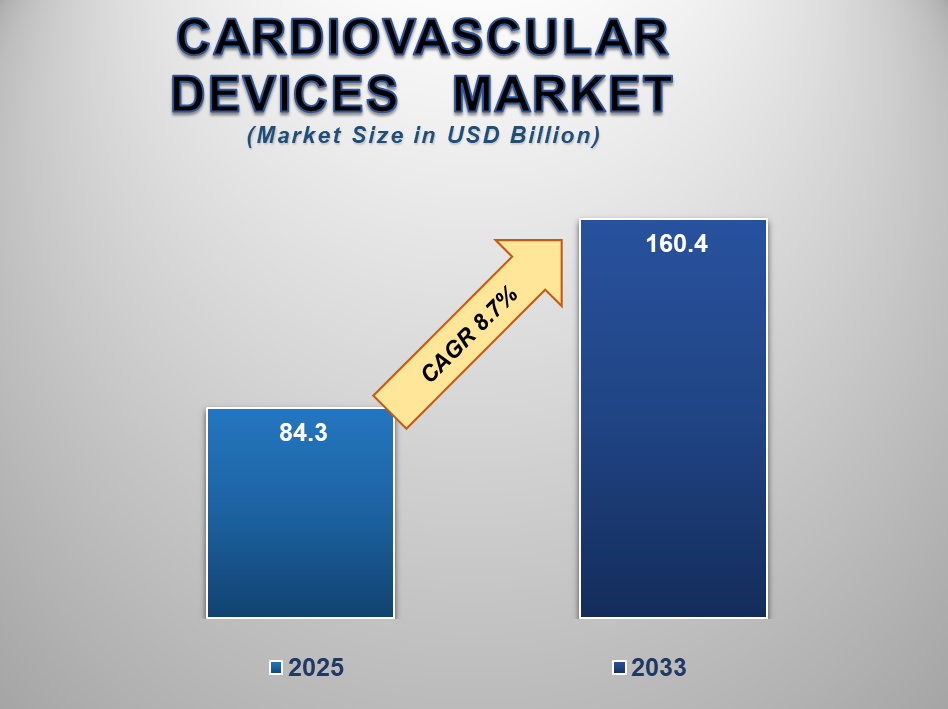

The global Cardiovascular Devices

Market was valued at USD 84.3 billion in 2025 and is projected to reach USD

160.4 billion by 2033, growing at a CAGR of 8.7% during the forecast period.

Cardiovascular diseases (CVDs) continue to be the leading cause of death

globally, placing immense pressure on healthcare systems and driving demand for

advanced diagnostic, monitoring, and treatment solutions.

The adoption of minimally

invasive procedures, the rising geriatric population, and growing awareness of

preventive cardiac care are key market drivers. Technological innovations in

wearable cardiac monitors, implantable defibrillators, stents, catheters, and

advanced imaging modalities are expanding the ability to detect, treat, and

manage heart disease earlier and more effectively. Government initiatives to

improve heart health awareness, investments in modern healthcare

infrastructure, and favorable reimbursement policies are further supporting

market growth. However, regulatory complexities and high costs of certain

advanced devices could slightly hinder adoption in lower-income regions.

Overall, with an expanding product pipeline and continued R&D investments,

the cardiovascular devices market is positioned for steady expansion over the

coming decade.

Cardiovascular Devices

Market Drivers and Opportunities

The growing burden of cardiovascular diseases is anticipated

to drive the market during the forecast period

The rising prevalence of

cardiovascular diseases globally is a central driver of the market’s growth.

According to the WHO, CVDs are responsible for about 32% of all global deaths,

with coronary artery disease and stroke being the most prevalent. Urbanization,

poor dietary habits, tobacco use, physical inactivity, and increasing obesity

have compounded cardiovascular risks, particularly in middle- and low-income

countries where healthcare access is still evolving. As a result, health

systems are emphasizing early detection, regular screening, and long-term

monitoring of heart conditions. The demand for diagnostic and monitoring tools

such as ECG systems, mobile cardiac telemetry, wearable monitors, and cardiac

imaging is increasing significantly. These devices support timely intervention,

reduce hospitalizations, and improve patient outcomes. Governments are

investing in public health initiatives that promote cardiac health awareness

and screening, contributing to rising diagnosis rates. The market is also benefiting

from a surge in elective cardiac procedures as hospitals catch up on delayed

surgeries from the COVID-19 pandemic era. Furthermore, an aging global

population, which is at higher risk of chronic heart conditions, is expected to

steadily increase demand for cardiovascular diagnostics and treatments over the

next decade, further driving market expansion.

Technological advancements in minimally invasive and

connected cardiovascular devices are transforming the market

Advancements in cardiovascular

device technology are enabling a shift toward less invasive, more personalized,

and real-time patient care. The development of miniaturized implantable

devices—such as leadless pacemakers and implantable loop recorders has significantly

improved patient comfort, reduced complication rates, and shortened recovery

times. Similarly, wearable cardiac monitors, smart ECG patches, and AI-powered

diagnostics are transforming remote patient monitoring and allowing physicians

to detect abnormalities like arrhythmias and ischemia earlier than ever.

Artificial intelligence and machine learning are now being incorporated into

diagnostic imaging systems and monitoring platforms to enable predictive

analytics, improve accuracy, and support early interventions. Devices with

wireless connectivity can transmit data to clinicians in real time, allowing

for timely adjustments in treatment plans and enhancing chronic care

management. These innovations are particularly valuable in post-operative monitoring,

outpatient follow-up, and home-based care. Further, integration with electronic

health records (EHRs) is enhancing coordination across the care continuum.

Manufacturers are heavily investing in R&D to develop next-gen solutions

that are not only precise and reliable but also cost-effective and easy to use.

These developments are expected to reshape cardiovascular treatment delivery

models and sustain market momentum throughout the forecast period.

Opportunity for the Cardiovascular Surgical Devices Market

Expanding healthcare infrastructure and medical tourism in

emerging markets create significant opportunities

Emerging economies, particularly

in the Asia Pacific, Latin America, and the Middle East, are experiencing rapid

growth in healthcare infrastructure and access. Governments are investing in

hospital modernization, the establishment of specialized cardiac centers, and

the procurement of advanced diagnostic and surgical equipment. Additionally,

awareness of heart disease prevention and treatment is rising across urban

populations, leading to increased demand for cardiovascular screening and

interventional services. Medical tourism is also playing a vital role,

especially in countries like India, Thailand, and Malaysia, where high-quality

cardiac procedures are offered at a fraction of the cost compared to developed

markets. International patients are increasingly opting for valve replacements,

coronary bypass surgeries, and angioplasty in these markets, creating a strong

demand for surgical cardiovascular devices. To tap into this opportunity,

multinational players are forming local partnerships, investing in domestic

manufacturing, and tailoring their devices for price-sensitive markets without

compromising on quality. Furthermore, increased penetration of health insurance

and public reimbursement programs in developing nations is improving

affordability and encouraging the uptake of cardiovascular interventions. As a

result, emerging markets are anticipated to contribute significantly to global

cardiovascular device market growth over the next decade.

Cardiovascular Devices Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 84.3 Billion |

|

Market Forecast in 2033 |

USD 160.4 Billion |

|

CAGR % 2025-2033 |

8.7% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production Capacity, growth factors, and more |

|

Segments Covered |

●

By Product ●

By Application ●

By End-user |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Cardiovascular Devices Market Report Segmentation Analysis

The global Cardiovascular Devices

Market industry analysis is segmented by Product, by Application, by End-user,

and by region.

The Diagnostic & Monitoring Devices segment accounted for

the largest market share in the global Cardiovascular Devices market

By Product, the market is segmented into Diagnostic & Monitoring Devices and Surgical Devices. The Diagnostic & Monitoring Devices segment held the largest share in 2024, accounting for 55.8% of the global market. The segment’s dominance stems from the widespread use of devices such as ECG machines, Holter monitors, implantable cardiac monitors, cardiac diagnostic catheters, and cardiovascular ultrasound systems. These devices are essential for detecting and managing a wide range of cardiovascular conditions, from early-stage hypertension and arrhythmias to more complex ischemic heart diseases. Increased adoption of remote cardiac monitoring solutions, including mobile cardiac telemetry (MCT) and smartphone-enabled ECG devices, is further fueling segment growth.

The Coronary Artery Disease (CAD) segment accounted for the

largest market share in the global Cardiovascular Devices market

By Application, the market is

categorized into Coronary Artery Disease, Cardiac Arrhythmia, Heart Failure,

and Others. Among these, the Coronary Artery Disease (CAD) segment accounted

for the largest market share in 2024 and is projected to maintain dominance

throughout the forecast period. CAD remains the most common type of heart

disease globally and a leading cause of death. It is closely associated with

lifestyle risk factors such as poor diet, lack of exercise, high cholesterol,

hypertension, and smoking. The demand for advanced interventional devices,

including coronary stents, guidewires, catheters, and occlusion devices, has

grown significantly to manage CAD. Innovations like drug-eluting stents,

bioresorbable scaffolds, and improved balloon angioplasty catheters have

enhanced procedural success and long-term outcomes.

The Hospitals segment accounted for the largest market share

in the global Cardiovascular Devices market

By End User, the market is

segmented into Hospitals, Specialty Clinics, and Others. In 2024, hospitals

accounted for the largest share of the cardiovascular devices market and are

expected to remain the dominant segment throughout the forecast period. Hospitals

are the central hubs for comprehensive cardiovascular care, offering services

such as emergency intervention, diagnostics, surgical treatment, and

post-operative rehabilitation. They are well-equipped with advanced

infrastructure like catheterization labs, hybrid operating rooms, and cardiac

ICUs. Cardiovascular procedures often require multidisciplinary teams and

immediate access to imaging, lab testing, and intensive care, which hospitals

are uniquely suited to provide.

The following segments are part

of an in-depth analysis of the global Cardiovascular Devices Market:

|

Market Segments |

|

|

By Product |

●

Diagnostic &

Monitoring Devices o ECG o Implantable Cardiac Monitors o Holter Monitors o Mobile Cardiac Telemetry o MRI o Cardiovascular Ultrasound ▪

2D ▪

3D/4D ▪

Doppler o Cardiac Diagnostic Catheters o PET Scanner ●

Surgical Devices o Cardiac Resynchronization Therapy (CRT) ▪

CRT-Defibrillator ▪

CRT-Pacemaker o Implantable Cardioverter Defibrillators (ICDs) ▪

Single Chamber ICDs ▪

Dual Chamber ICDs o Pacemakers ▪

Conventional

Pacemakers ▪

Leadless Pacemakers o Coronary Stents o Catheters o Guidewires o Cannula o Valves o Occlusion Devices o

Others |

|

By Application |

●

Coronary Artery

Disease (CAD) ●

Cardiac Arrhythmia ●

Heart Failure ●

Others |

|

By End-User |

●

Hospitals ●

Specialty Clinics ●

Others |

Global Cardiovascular

Devices Market Share Analysis by Region

The North America region is projected to hold the largest

share of the global Cardiovascular Devices market over the forecast period.

North America led the global

cardiovascular devices market in 2024, accounting for 47.7% of total revenue,

and is expected to maintain its leading position through 2033. The region

benefits from a strong healthcare ecosystem, high awareness levels, rapid

adoption of new technologies, and supportive reimbursement structures. The U.S.

remains a key market, with a high prevalence of heart disease and significant

per capita healthcare expenditure. The presence of major cardiovascular medical

device market companies such as Medtronic, Abbott, and Boston Scientific also

enhances innovation and market penetration in the region. Additionally,

government-funded health initiatives, widespread cardiac screening programs,

and investments in digital and AI-based technologies are enabling improved

disease management and early intervention. Remote cardiac monitoring,

telehealth integration, and home care services are expanding rapidly,

especially among the aging population. Canada, with its public healthcare

system and emphasis on preventive care, is also contributing to regional

growth. Collectively, these factors will sustain North America’s leadership in

the cardiovascular devices market over the forecast horizon.

Asia Pacific is projected to

register the highest compound annual growth rate (CAGR) in the global

cardiovascular devices market from 2025 to 2033. The region’s growth is driven

by a surge in heart disease prevalence, rapid urbanization, improving income

levels, and increased government investment in healthcare infrastructure.

Countries like China, India, Japan, and South Korea are scaling up their

cardiac care capabilities through new hospitals, diagnostic labs, and

catheterization centers. Government-supported health insurance schemes and

medical tourism are increasing access to advanced procedures, such as stenting,

valve repair, and pacemaker implantation. In addition, the growing presence of

local manufacturers and partnerships with global players are helping bring

affordable and high-quality devices to market. Digital health adoption is also

accelerating, driven by widespread smartphone penetration and mobile health

applications. As cardiovascular risk factors continue to rise across all age

groups in the region, the demand for diagnostic, monitoring, and surgical

cardiovascular devices is set to increase sharply.

Cardiovascular Devices Market Competition Landscape Analysis

The global

cardiovascular devices market is moderately consolidated, with several dominant

players and a growing number of emerging companies focusing on innovation,

product diversification, and global expansion. Major players like Medtronic,

Boston Scientific, Abbott, and Edwards Lifesciences continue to invest heavily

in R&D to advance their offerings in minimally invasive therapies,

structural heart devices, and implantable monitors.

Global Cardiovascular

Devices Market Recent Developments News:

- In June 2024 – Abbott achieved CE Mark approval in

Europe for its AVEIR Dual Chamber (DR) Leadless Pacemaker System, marking

a revolutionary advancement in cardiac rhythm management. As the world's

first dual-chamber leadless

pacemaker, the system features two miniaturized devices (each 90% smaller

than conventional pacemakers) that synchronously pace the right atrium

(AVEIR AR) and right ventricle (AVEIR VR) through innovative wireless

communication technology, offering patients a less invasive treatment

option for bradyarrhythmias.

- In September 2024 – Boston Scientific obtained PMDA

approval in Japan for its FARAPULSE Pulsed Field Ablation (PFA) System,

introducing a paradigm shift in atrial fibrillation treatment. This

non-thermal ablation technology provides a safer, more efficient

alternative to traditional radiofrequency ablation for pulmonary vein

isolation in paroxysmal AF patients, with reduced risk of collateral

tissue damage.

- In July 2024 – Edwards Lifesciences exercised its

option to fully acquire Innovalve Bio-Medical Ltd., accelerating its

development of transcatheter mitral valve replacement (TMVR) solutions.

This strategic move builds upon Edwards' 2017 initial investment and

strengthens its position in the emerging structural heart market.

- In February 2024 – Edwards Lifesciences made medical history as its

EVOQUE Tricuspid Valve Replacement System became the first FDA-approved

transcatheter therapy for treating tricuspid regurgitation (TR),

addressing a critical unmet need for patients with this debilitating

valvular heart disease. The approval establishes a new treatment standard

for TR patients ineligible for open-heart surgery.

The Global Cardiovascular

Devices Market is dominated by a few large companies, such as

●

Boston Scientific

Corporation

●

Medtronic

●

Abbott

●

B. Braun SE

●

Terumo Corporation

●

Edwards Lifesciences

Corporation

●

Koninklijke Philips NV.

●

BIOTRONIK SE & Co.

KG

●

GE Healthcare

Technologies, Inc.

●

Siemens Healthineers

AG

●

Johnson & Johnson

●

Baxter International

Inc

●

Getinge AB

●

Lepu Medical

Technology Co., Ltd

●

Nihon Kohden

Corporation

●

MicroPort Scientific

Corporation

●

Japan Lifeline Co.,

Ltd.

●

AngioDynamics, Inc.

●

Artivion Inc

●

Sahajanand Medical

Technologies Limited

●

W.L. Gore &

Associates, Inc.

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

- Global Cardiovascular Devices Market Introduction and Market Overview

- Objectives of the Study

- Global Cardiovascular Devices Market Scope and Market Estimation

- Global Cardiovascular Devices Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Cardiovascular Devices Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

- Market Segmentation

- Product of Global Cardiovascular Devices Market

- Application of Global Cardiovascular Devices Market

- End-user of Global Cardiovascular Devices Market

- Region of Global Cardiovascular Devices Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Cardiovascular Devices Market

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Cardiovascular Devices Market Estimates & Historical Trend Analysis (2020 - 2024)

- Global Cardiovascular Devices Market Estimates & Forecast Trend Analysis, by Product

- Global Cardiovascular Devices Market Revenue (US$ Bn) Estimates and Forecasts, by Product, 2020 - 2033

- Diagnostic & Monitoring Devices

- ECG

- Implantable Cardiac Monitors

- Holter Monitors

- Mobile Cardiac Telemetry

- MRI

- Cardiovascular Ultrasound

- 2D

- 3D/4D

- Doppler

- Cardiac Diagnostic Catheters

- PET Scanner

- Surgical Devices

- Cardiac Resynchronization Therapy (CRT)

- CRT-Defibrillator

- CRT-Pacemaker

- Implantable Cardioverter Defibrillators (ICDs)

- Single Chamber ICDs

- Dual Chamber ICDs

- Pacemakers

- Conventional Pacemakers

- Leadless Pacemakers

- Coronary Stents

- Catheters

- Guidewires

- Cannula

- Valves

- Occlusion Devices

- Others

- Cardiac Resynchronization Therapy (CRT)

- Diagnostic & Monitoring Devices

- Global Cardiovascular Devices Market Revenue (US$ Bn) Estimates and Forecasts, by Product, 2020 - 2033

- Global Cardiovascular Devices Market Estimates & Forecast Trend Analysis, by Application

- Global Cardiovascular Devices Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- Coronary Artery Disease (CAD)

- Cardiac Arrhythmia

- Heart Failure

- Others

- Global Cardiovascular Devices Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- Global Cardiovascular Devices Market Estimates & Forecast Trend Analysis, by End-user

- Global Cardiovascular Devices Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2020 - 2033

- Hospitals

- Specialty Clinics

- Others

- Global Cardiovascular Devices Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2020 - 2033

- Global Cardiovascular Devices Market Estimates & Forecast Trend Analysis, by region

- Global Cardiovascular Devices Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Cardiovascular Devices Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020 - 2033

- North America Cardiovascular Devices Market: Estimates & Forecast Trend Analysis

- North America Cardiovascular Devices Market Assessments & Key Findings

- North America Cardiovascular Devices Market Introduction

- North America Cardiovascular Devices Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product

- By Application

- By End-user

- By Country

- The U.S.

- Canada

- North America Cardiovascular Devices Market Assessments & Key Findings

- Europe Cardiovascular Devices Market: Estimates & Forecast Trend Analysis

- Europe Cardiovascular Devices Market Assessments & Key Findings

- Europe Cardiovascular Devices Market Introduction

- Europe Cardiovascular Devices Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product

- By Application

- By End-user

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Switzerland

- Rest of Europe

- Europe Cardiovascular Devices Market Assessments & Key Findings

- Asia Pacific Cardiovascular Devices Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Cardiovascular Devices Market Introduction

- Asia Pacific Cardiovascular Devices Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product

- By Application

- By End-user

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Cardiovascular Devices Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Cardiovascular Devices Market Introduction

- Middle East & Africa Cardiovascular Devices Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product

- By Application

- By End-user

- By Country

- South Africa

- UAE

- Saudi Arabia

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Cardiovascular Devices Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Cardiovascular Devices Market Introduction

- Latin America Cardiovascular Devices Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product

- By Application

- By End-user

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Cardiovascular Devices Market Product Mapping

- Global Cardiovascular Devices Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Cardiovascular Devices Market Tier Structure Analysis

- Global Cardiovascular Devices Market Concentration & Company Market Shares (%) Analysis, 2023

- Company Profiles

- Boston Scientific Corporation

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Boston Scientific Corporation

* Similar details would be provided for all the players mentioned below

- Medtronic

- Abbott

- Braun SE

- Terumo Corporation

- Edwards Lifesciences Corporation

- Koninklijke Philips N.V.

- BIOTRONIK SE & Co. KG

- GE Healthcare Technologies, Inc.

- Siemens Healthineers AG

- Johnson & Johnson

- Baxter International Inc

- Getinge AB

- Lepu Medical Technology Co., Ltd

- Nihon Kohden Corporation

- MicroPort Scientific Corporation

- Japan Lifeline Co., Ltd.

- AngioDynamics, Inc.

- Artivion Inc

- Sahajanand Medical Technologies Limited

- L. Gore & Associates, Inc.

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables