Ceramics Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Type (Traditional, Advanced), By Application (Tiles, Sanitary Wares, Abrasives, Pottery, Bricks & Pipes, Others), By End-Use Industry (Building & Construction, Industrial, Medical, Others), and Geography

2026-02-25

Chemicals & Materials

Description

Ceramics Market Overview

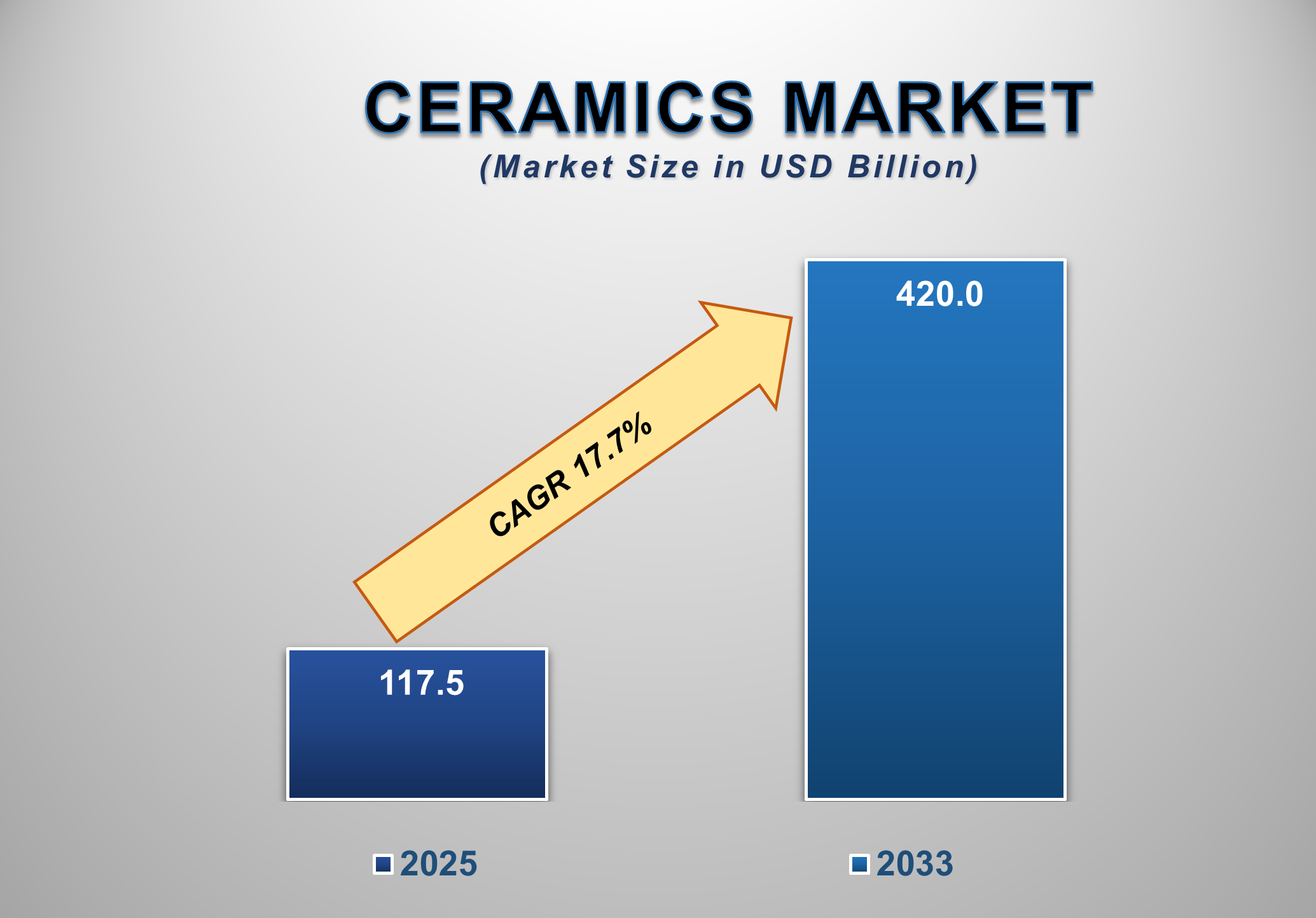

The global ceramics market was valued at USD 117.5 billion in 2025 and is projected to reach USD 420.0 billion by 2033, expanding at a strong CAGR of 17.7% during the forecast period. This significant growth is primarily driven by rapid urbanization, large-scale infrastructure development, rising demand from the construction sector, and increasing adoption of advanced ceramics across industrial and medical applications. Ceramics remain a foundational material across residential, commercial, and industrial value chains due to their durability, thermal resistance, and aesthetic versatility.

Traditional ceramics continue to

dominate the market, accounting for 57.6% of total revenue, supported by

widespread usage in tiles, sanitary ware, bricks, and pipes. Meanwhile,

advanced ceramics are gaining traction in high-performance applications such as

electronics, medical implants, aerospace components, and energy systems. The

growing emphasis on sustainable construction materials and long-lasting

infrastructure solutions is further strengthening ceramics demand globally.

Ceramics Market Drivers

and Opportunities

Rapid Urbanization and

Construction Activity Are Driving Market Growth

One of the primary drivers of the ceramics market is the rapid

pace of urbanization and construction activity worldwide. Growing population

density in urban areas, coupled with increasing investments in residential,

commercial, and public infrastructure projects, has significantly boosted

demand for ceramic tiles, sanitary ware, and structural ceramic products.

Governments across emerging economies are prioritizing housing development,

transportation networks, and urban infrastructure, directly contributing to

ceramics consumption.

Ceramic tiles are extensively used in flooring, wall cladding, and

exterior applications due to their durability, water resistance, and low

maintenance requirements. The rising preference for aesthetically appealing and

long-lasting building materials has further strengthened the role of ceramics

in modern construction. Additionally, renovation and remodeling activities in

developed economies are driving replacement demand for ceramic products.

Technological advancements such as digital printing on tiles, large-format

slabs, and customized ceramic designs have expanded product offerings and

increased adoption in premium construction projects. As construction activity

continues to rise globally, ceramics are expected to remain a core material

supporting infrastructure and real estate development.

Expanding Industrial and Medical Applications Are

Strengthening Market Expansion

The growing adoption of ceramics in industrial and medical

applications is another major growth driver for the ceramics market. Advanced

ceramics exhibit superior properties such as high thermal resistance,

electrical insulation, chemical stability, and mechanical strength, making them

ideal for demanding industrial environments. Industries such as electronics,

automotive, aerospace, and energy increasingly rely on ceramic components for

enhanced performance and durability.

In the medical sector, ceramics are widely used in dental

implants, orthopedic implants, prosthetics, and surgical instruments due to

their biocompatibility and wear resistance. The rising prevalence of chronic

diseases, aging populations, and increasing healthcare expenditure are

contributing to steady demand for medical ceramics. Additionally, ceramics are

gaining importance in renewable energy applications, including fuel cells,

solar panels, and battery systems. As industries continue to seek high-performance

materials capable of withstanding extreme conditions, the role of advanced

ceramics in industrial and medical sectors is expected to expand significantly.

Technological Innovation in Advanced Ceramics Presents Major

Growth Opportunities

Technological innovation represents a significant opportunity for

the ceramics market, particularly in the development and commercialization of

advanced ceramics. Continuous research and development efforts are leading to

the creation of high-purity, lightweight, and high-strength ceramic materials

with enhanced functional properties. These innovations are enabling ceramics to

penetrate new application areas such as semiconductor manufacturing, electric

vehicles, and next-generation medical devices.

Additive manufacturing and 3D printing of ceramics are emerging as transformative technologies, allowing for complex geometries, reduced material waste, and customized product designs. These advancements are particularly beneficial for aerospace, defense, and healthcare applications, where precision and performance are critical. Furthermore, the growing focus on sustainability is encouraging manufacturers to develop energy-efficient production processes and recyclable ceramic materials. As technological advancements continue to accelerate, advanced ceramics are expected to unlock new revenue streams and elevate the overall market growth trajectory

Ceramics Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 117.5 Billion |

|

Market Forecast in 2035 |

USD 420.0 Billion |

|

CAGR % 2025-2035 |

17.7% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2035 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Type ●

By Application ●

By End-Use

Industry |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Ceramics Market Report

Segmentation Analysis

The Global Ceramics Market

Industry Analysis Is Segmented By Type, By Application, By End-Use Industry,

and By Region.

The

Traditional Ceramics Segment Is Expected to Dominate

the Global Ceramics Market During the Forecast Period

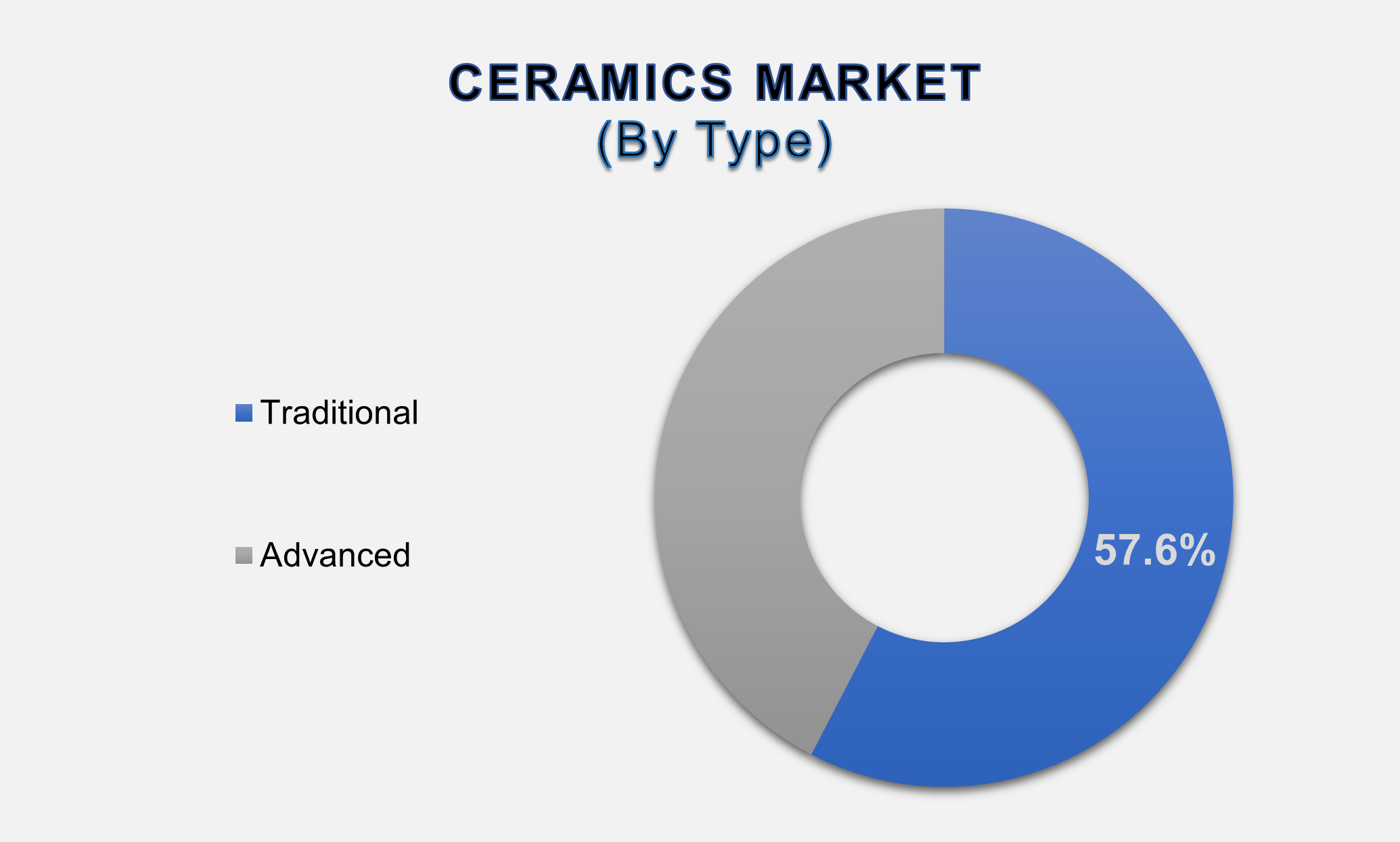

The traditional ceramics segment accounted for approximately 57.6% of the global ceramics market, driven by extensive usage in tiles, sanitary ware, bricks, pipes, and pottery. Traditional ceramics are widely preferred in construction applications due to their cost-effectiveness, durability, and ease of manufacturing. High demand from residential and commercial construction projects continues to support segment dominance. Ceramic tiles represent the largest application within traditional ceramics, benefiting from the rising demand for flooring and wall solutions in urban housing and infrastructure projects. Sanitary ware products such as toilets, washbasins, and bidets also contribute significantly to segment revenue, particularly in developing economies with expanding sanitation infrastructure. Despite increasing adoption of advanced ceramics, traditional ceramics are expected to maintain their leading position due to their broad applicability and strong demand fundamentals.

Tiles

Segment Is Expected to Dominate the Ceramics Market During the Forecast Period

The

tiles segment represents the largest application area in the ceramics market,

driven by widespread adoption in building and construction. Ceramic tiles are

favored for their resistance to moisture, stains, and wear, making them ideal

for residential, commercial, and industrial spaces. The availability of diverse

designs, textures, and finishes has further enhanced tile adoption.

Large-format tiles and digitally printed designs are gaining popularity in

premium construction projects, supporting higher value growth. Additionally,

increasing renovation activity in mature markets is contributing to replacement

demand for ceramic tiles. As urbanization and infrastructure development

continue, the tiles segment is expected to remain the dominant application within

the ceramics market.

Building

& Construction End-Use Industry Is Expected to Lead the Ceramics Market

Through 2033

The

building and construction segment accounts for the largest share of the

ceramics market, supported by strong demand for tiles, sanitary ware, bricks,

and pipes. Rapid urban development, housing projects, and commercial

construction are key contributors to segment growth. Ceramics are increasingly

used in sustainable and green building initiatives due to their long lifespan,

recyclability, and low maintenance requirements. As governments and private

developers invest in smart cities and infrastructure modernization, demand from

the building and construction sector is expected to remain robust.

The following segments are

part of an in-depth analysis of the global Ceramics Market:

|

Market Segments |

|

|

By Type |

●

Traditional ●

Advanced |

|

By Application |

●

Tiles ●

Sanitary Wares ●

Abrasives ●

Pottery ●

Bricks & Pipes ●

Others |

|

By End-Use

Industry |

●

Building &

Construction ●

Industrial ●

Medical ●

Others |

Ceramics Market Share

Analysis by Region

North America is

anticipated to hold the biggest portion of the Ceramics Market globally

throughout the forecast period.

Asia Pacific accounted for

approximately 38.0% of the global ceramics market in 2025, making it the

largest regional market. The region’s dominance is driven by rapid

urbanization, strong construction activity, and a well-established ceramics

manufacturing base. Countries such as China, India, and Southeast Asian nations

are witnessing large-scale infrastructure development, housing projects, and

industrial expansion, which significantly boost ceramics demand. Additionally,

the availability of raw materials, low production costs, and high domestic

consumption support regional market leadership.

Europe is expected to register

the highest CAGR during the forecast period, driven by growing demand for

advanced ceramics and sustainable construction materials. Increasing renovation

activities, stringent energy efficiency regulations, and rising adoption of

high-performance ceramics in industrial and medical applications are supporting

market growth. Countries such as Germany, Italy, and Spain are at the forefront

of technological innovation in ceramics manufacturing, positioning Europe as

the fastest-growing regional market through 2033.

Ceramics Market

Competition Landscape Analysis

The ceramics market is moderately

fragmented, with the presence of global manufacturers and strong regional

players. Competition is based on product quality, design innovation,

technological capabilities, pricing, and distribution reach. Strategic expansions,

capacity additions, and investments in advanced ceramics are key competitive

strategies.

Global Ceramics Market

Recent Developments News:

- In March 2024 – Landmark Ceramics celebrated a USD

72 million investment to expand its logistics and production capabilities

near Nashville, Tennessee. The project includes a new logistics hub and

expanded tile production capacity in the U.S.

- In April 2024 – Meghna Ceramic Industries invested

USD 45 million to increase production capacity at its factory near Dhaka,

Bangladesh. Since July 2023, the facility has been producing 51,000 square

meters of “Fresh Ceramics” tiles daily, strengthening the company’s

position in the tile market.

The Global Ceramics Market Is

Dominated by a Few Large Companies, such as

●

LIXIL Group

●

Kohler

●

Mohawk Industries

●

TOTO

●

Geberit

●

Roca

●

Kyocera Corporation

●

Saint-Gobain

●

Coorstek

●

3M Company

●

Villeroy & Boch

●

Lamosa

●

Cersanit

●

RAK Ceramics

●

NGK Spark

●

Arrow Group

●

Ceramtec

●

Iris Ceramica

●

Morgan Advanced

Materials

●

Kajaria

●

Florim

●

Nabel Ceramics

●

SCG

●

Fortune Brands Home

& Security

●

Casalgrande Padana

● Others

Frequently Asked Questions

1. Global Ceramics Market

Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Ceramics Market Scope and Market Estimation

1.2.1.Global Ceramics Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Ceramics Market

Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Type of Global Ceramics

Market

1.3.2.Application of Global Ceramics

Market

1.3.3.End-Use Industry of Global

Ceramics Market

1.3.4.Region of Global Ceramics

Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Ceramics Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Ceramics Market Estimates

& Forecast Trend Analysis, by Type

4.1.

Global

Ceramics Market Revenue (US$ Bn) Estimates and Forecasts, by Type, 2020 - 2033

4.1.1.Traditional

4.1.2.Advanced

5. Global

Ceramics Market Estimates

& Forecast Trend Analysis, by Application

5.1.

Global

Ceramics Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020

- 2033

5.1.1.Tiles

5.1.2.Sanitary Wares

5.1.3.Abrasives

5.1.4.Pottery

5.1.5.Bricks & Pipes

5.1.6.Others

6. Global

Ceramics Market Estimates

& Forecast Trend Analysis, by End-Use Industry

6.1.

Global

Ceramics Market Revenue (US$ Bn) Estimates and Forecasts, by End-Use Industry,

2020 - 2033

6.1.1.Building &

Construction

6.1.2.Industrial

6.1.3.Medical

6.1.4.Others

7. Global

Ceramics Market Estimates

& Forecast Trend Analysis, by Region

7.1.

Global

Ceramics Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Ceramics

Market: Estimates & Forecast Trend

Analysis

8.1.

North

America Ceramics Market Assessments & Key Findings

8.1.1.North America Ceramics

Market Introduction

8.1.2.North America Ceramics

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Type

8.1.2.2. By Application

8.1.2.3. By End-Use

Industry

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Ceramics

Market: Estimates & Forecast Trend

Analysis

9.1.

Europe

Ceramics Market Assessments & Key Findings

9.1.1.Europe Ceramics Market

Introduction

9.1.2.Europe Ceramics Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Type

9.1.2.2. By Application

9.1.2.3. By End-Use

Industry

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Ceramics

Market: Estimates & Forecast Trend

Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Ceramics Market Introduction

10.1.2.

Asia

Pacific Ceramics Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Type

10.1.2.2. By Application

10.1.2.3. By End-Use

Industry

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Ceramics

Market: Estimates & Forecast Trend

Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Ceramics Market Introduction

11.1.2.

Middle East & Africa Ceramics Market Size Estimates and

Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Type

11.1.2.2. By Application

11.1.2.3. By End-Use

Industry

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Ceramics Market: Estimates &

Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Ceramics Market Introduction

12.1.2.

Latin

America Ceramics Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1. By Type

12.1.2.2. By Application

12.1.2.3. By End-Use

Industry

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Ceramics Market Product Mapping

14.2.

Global

Ceramics Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3.

Global

Ceramics Market Tier Structure Analysis

14.4.

Global

Ceramics Market Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

LIXIL Group

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. Kohler

15.3. Mohawk

Industries

15.4. TOTO

15.5. Geberit

15.6. Roca

15.7. Kyocera

Corporation

15.8. Saint-Gobain

15.9. Coorstek

15.10. 3M

Company

15.11. Villeroy

& Boch

15.12. Lamosa

15.13. Cersanit

15.14. RAK

Ceramics

15.15. NGK

Spark

15.16. Arrow

Group

15.17. Ceramtec

15.18. Iris

Ceramica

15.19. Morgan

Advanced Materials

15.20. Kajaria

15.21. Florim

15.22. Nabel

Ceramics

15.23. SCG

15.24. Fortune

Brands Home & Security

15.25. Casalgrande

Padana

15.26. Others

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables