Cloud Kitchen Market Size and Forecast (2020-2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Type (Independent, Commissary/Shared Kitchen, Kitchen Pods), By Product Type (Burger/Sandwich, Pizza/Pasta, Chicken, Seafood, Mexican/Asian Food, Others), By Nature (Franchised, Standalone) And Geography

2025-12-03

Consumer Products

Jaya Bundele (Research Analyst)

Description

Cloud Kitchen Market Overview

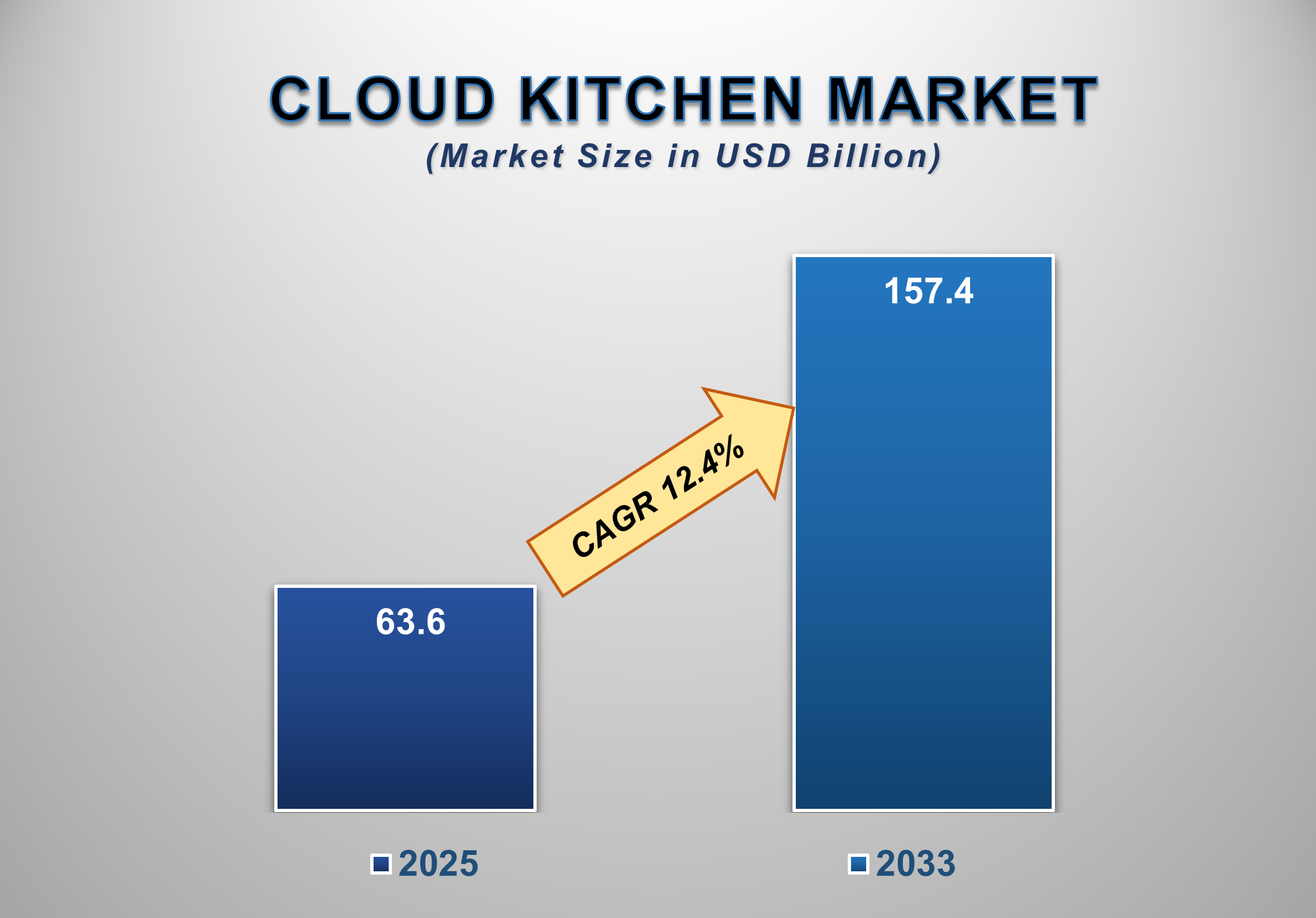

The Cloud Kitchen Market is poised for explosive growth from 2025 to 2033, driven by the paradigm shift in consumer dining habits, the relentless expansion of online food delivery platforms, and the increasing demand for operational efficiency in the food service sector. The market is projected to be valued at approximately USD 63.6 billion in 2025 and is forecasted to reach nearly USD 157.4 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 12.4% during this period.

A cloud kitchen, also known as a ghost kitchen

or virtual kitchen, is a food preparation facility that operates solely for

delivery, with no physical storefront or dine-in area. The market's robust

expansion is primarily fueled by the post-pandemic normalization of food

delivery, rising smartphone penetration, and the growing convenience offered by

food aggregator apps like Uber Eats, DoorDash, and Zomato.

The model offers significant economic advantages

over traditional restaurants, including lower startup costs, reduced overheads

(no prime real estate or front-of-house staff), and the ability to host

multiple brands from a single location, optimizing space and resources.

Furthermore, the ability to rapidly test new culinary concepts and menus with

minimal risk is a key factor attracting entrepreneurs and established

restaurant chains alike. North America and Europe are mature markets with high

adoption rates, while the Asia-Pacific region is expected to witness the

fastest growth due to its vast urban population, burgeoning middle class, and

deep penetration of food delivery services.

Cloud

Kitchen Market Drivers and Opportunities

Proliferation of Online Food Delivery

Services and Evolving Consumer Preferences are

the Primary Market Drivers

The unprecedented growth of online food delivery

(OFD) platforms is the most powerful engine for the cloud kitchen market. The

convenience of ordering food via a few taps on a smartphone has become

ingrained in modern urban life. This consumer shift is complemented by changing

lifestyles, with busier schedules and a growing preference for at-home dining

experiences. Cloud kitchens are intrinsically designed to serve this

delivery-first ecosystem, operating with optimized workflows for packaging and

speed, directly aligning with the core demands of both consumers and delivery

platforms. The symbiotic relationship between food aggregators, which

constantly seek to expand their restaurant portfolio and delivery reach, and

cloud kitchens, which rely on these platforms for order volume, creates a

self-reinforcing cycle of market expansion.

Operational Efficiency and Lower Barrier to

Entry for Food Brands are Driving Adoption

The significant economic benefits of the cloud

kitchen model are a critical catalyst for its adoption. Compared to traditional

restaurants, cloud kitchens eliminate costs associated with premium real

estate, dine-in ambience, and extensive front-of-house staffing. This lower

capital expenditure and operational overhead make it feasible for new brands to

launch and for existing chains to expand their geographic footprint rapidly and

cost-effectively. The multi-branding strategy, where a single kitchen operates

several virtual restaurant brands, allows for maximizing the utility of the

kitchen space, diversifying menu offerings, and capturing a larger share of the

delivery market. This operational efficiency directly translates to higher

profitability potential and a lower risk profile, attracting significant

investment from venture capitalists and established food service operators.

Integration of Advanced Technologies and

Expansion into Untapped Cuisines and Regions Present Significant Opportunities

The strategic integration of technology and the

exploration of new culinary and geographic frontiers are creating substantial

growth opportunities for the cloud kitchen market. Key opportunities lie in

leveraging data analytics and artificial intelligence (AI) to optimize menu

engineering, predict demand, manage inventory, and personalize marketing

campaigns. The development of automated kitchen equipment and robotics for

tasks like frying and flipping burgers can further enhance consistency and

efficiency. Geographically, rapidly growing economies in the Asia-Pacific, Latin America, and the Middle East offer

vast, unsaturated markets. Furthermore, there is immense potential in

specializing in underserved cuisines or

dietary trends, such as health-conscious meals, plant-based options, or

specific ethnic foods, delivered from a focused cloud kitchen. The emergence of

hybrid models, combining a small dine-in space with a delivery-optimized

kitchen ("phygital" model), and the growth of delivery-only grocery

and convenience items represent additional, innovative avenues for market

expansion and revenue diversification.

Cloud Kitchen Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 63.3 Billion |

|

Market Forecast in 2033 |

USD 157.4 Billion |

|

CAGR % 2025-2033 |

12.4% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Cycle Type ●

By Patient Age ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Cloud Kitchen Market Report Segmentation Analysis

The global

Cloud Kitchen Market industry analysis is segmented by Type, by Product Type,

by Nature, and by Region.

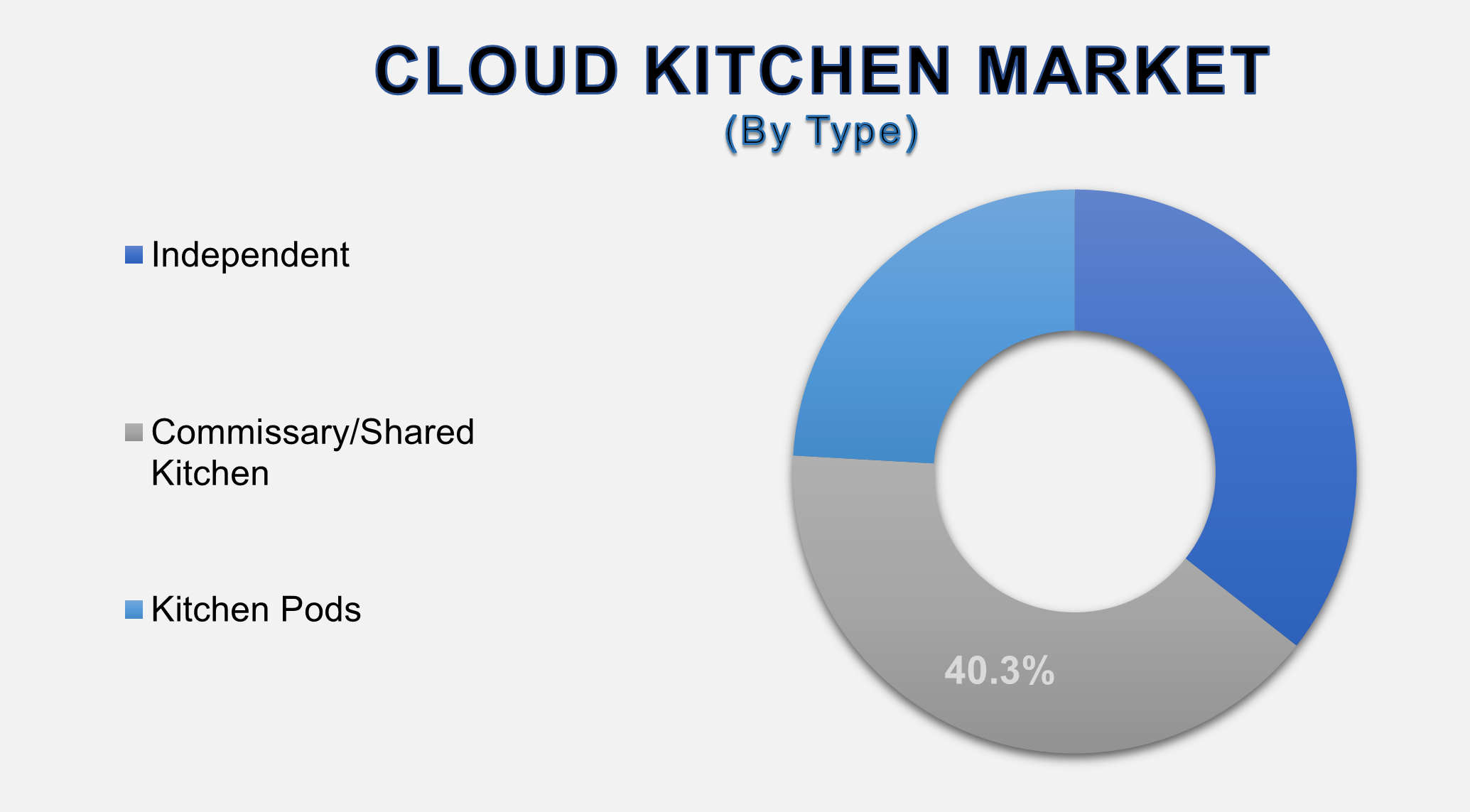

The

Commissary/Shared Kitchen segment is anticipated to command the largest market

share in 2025

The Type segment is categorised into Independent,

Commissary/Shared Kitchen, and Kitchen Pods. The dominance of the

Commissary/Shared Kitchen segment is attributed to its superior economic model

and scalability. These facilities house multiple food preparation stations for

different brands under one roof, sharing resources like utilities, storage, and

sometimes even staff. This model drastically reduces the individual operational

cost for each brand, making it highly attractive for small entrepreneurs and for

large chains looking to test new markets or concepts. The shared infrastructure

allows for greater efficiency and higher density of food production in urban

areas, catering directly to the multi-branding strategy that is central to the

cloud kitchen value proposition. While independent kitchens offer brand

control, the cost-sharing and collaborative advantages of commissary kitchens

secure their position as the segment with the

largest market share.

The Burger/Sandwich segment is projected to grow at a

significant CAGR.

The Product Type segment includes Burger/Sandwich,

Pizza/Pasta, Chicken, Seafood, Mexican/Asian Food, and Others. The

Burger/Sandwich segment's projected significant growth is driven by its

inherent suitability for the delivery model. These items have high consumer

demand, are familiar to a global audience, and generally maintain their quality

and integrity during transit better than more delicate cuisines. The simplicity

of their preparation allows for speed and consistency, which are critical for

high-volume delivery operations. Furthermore, the burger and sandwich space is

highly competitive and innovative, with numerous virtual brands specializing in

gourmet, ethnic-fusion, or health-conscious variations, all of which can be

efficiently produced and tested from a cloud kitchen environment. This

combination of delivery resilience and continuous menu innovation makes this

product type a fast-growing driver of the cloud kitchen market.

The Franchised segment is projected to witness the highest

growth rate.

The Nature segment is divided into Franchised and

Standalone. The Franchised segment's position as the fastest-growing channel is

a result of the powerful synergy between the cloud kitchen model and franchise

expansion strategies. Established restaurant brands are increasingly using

franchised cloud kitchens as a low-risk, capital-efficient method to enter new

neighborhoods or cities without the overhead of a full-scale restaurant. For

franchisees, the model offers a lower initial investment and operational cost.

The franchisor provides brand recognition, standardized recipes, and supply

chain support, which de-risks the venture for the kitchen operator. This

partnership model allows for rapid, asset-light geographic expansion, enabling

brands to achieve widespread market penetration and compete effectively in the

crowded food delivery landscape, thereby propelling the growth of this segment.

The

following segments are part of an in-depth analysis of the global Cloud Kitchen

Market:

|

Market

Segments |

|

|

By Type |

●

Independent ●

Commissary/Shared

Kitchen ●

Kitchen Pods |

|

By Product

Type |

●

Burger/Sandwich ●

Pizza/Pasta ●

Chicken ●

Seafood ●

Mexican/Asian Food ●

Others |

|

By Nature |

●

Franchised ●

Standalone |

Cloud Kitchen Market Share Analysis by Region

The

Asia-Pacific region is anticipated to hold the largest portion of the Cloud

Kitchen Market globally throughout the forecast period.

Asia-Pacific's dominance is driven by a perfect storm of

favorable conditions: a massive, densely populated urban youth demographic,

incredibly high penetration of smartphones and food delivery apps, and a strong

culture of eating out and ordering in. Countries like India, China, and

Indonesia have seen an explosion of local food aggregators (e.g., Zomato, Swiggy,

and Meituan) that have cultivated a robust delivery

ecosystem. The cost-effectiveness of the cloud kitchen model is particularly

appealing in these price-sensitive markets, allowing for a proliferation of

brands catering to diverse tastes. Supportive infrastructure developments and a

vast pool of culinary talent further contribute to the region's leadership. The

growing middle class with increasing disposable income is continuously

expanding the addressable market for delivered food.

India alone is a key growth engine within the APAC region.

The country's huge population, rapid urbanization, and the widespread adoption

of digital payments have created an ideal environment for cloud kitchens. The

relatively low cost of setting up a kitchen compared to a restaurant has led to

an entrepreneurial boom in the space. Major international brands are partnering

with local kitchen operators to gain a foothold, while homegrown virtual brands

are proliferating at an astonishing rate. The competitive delivery fees and

frequent promotions by aggregators keep the market highly dynamic and fuel

consistent order volume, making India a critical and rapidly expanding market

for cloud kitchen services.

Cloud Kitchen Market Competition Landscape Analysis

The global

cloud kitchen market is highly competitive and fragmented, featuring a diverse

mix of large, well-funded aggregator-owned kitchens (e.g., Rebel Foods, Kitchen

United), franchised outlets of major QSR chains, and a multitude of independent

operators and startups. Competition is based on delivery speed, food quality

and consistency, brand strength, operational efficiency, and effective digital

marketing. Key strategies include geographic expansion, technological

integration for kitchen automation and data analytics, and the continuous

launch of new virtual brands to capture emerging food trends. The market is

also seeing consolidation as larger players acquire successful smaller brands

to scale their portfolio quickly.

Global Cloud Kitchen Market Recent Developments News:

- In February 2025, Rebel Foods announced a

partnership with a major global beverage brand to launch a co-branded

virtual restaurant chain focused on snack combos across its kitchens in

Southeast Asia.

- In December 2024, Kitchen United secured a new

round of funding to expand its network of commissary kitchens across the

United States, focusing on suburban locations.

- In October 2024, DoorDash launched its own private-label virtual kitchen brand,

"DashCorner Kitchens," offering a rotating menu of trending

dishes available only on its platform.

- In August 2024, Wow! Momo reported a successful

pilot of AI-driven demand forecasting in its cloud kitchens, leading to a

15% reduction in food waste and improved inventory management.

The Global Cloud Kitchen Market Is Dominated by a

Few Large Companies, such as

●

Rebel Foods

●

Kitchen United

●

Zuul

●

Travis Kalanick's

CloudKitchens

●

Starbucks (testing the

model)

●

DoorDash Kitchens

●

Ghost Kitchen Brands

●

The Local Culinary

●

Keatz

●

Kitopi

●

Frankie's

●

Dahmakan

●

Swiggy (Access to its

own kitchens)

●

Zomato (Access to its

own kitchens)

●

Starbucks

●

Wow! Momo Foods

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Cloud Kitchen

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Cloud Kitchen Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Cloud Kitchen

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Type of Global Cloud

Kitchen Market

1.3.2.Product Type of Global Cloud

Kitchen Market

1.3.3.Nature of Global Cloud

Kitchen Market

1.3.4.Region of Global Cloud

Kitchen Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Market

Entry Strategies

2.7.

Market

Dynamics

2.7.1.Drivers

2.7.2.Limitations

2.7.3.Opportunities

2.7.4.Impact Analysis of Drivers

and Restraints

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

3. Global

Cloud Kitchen Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Cloud Kitchen Market Estimates

& Forecast Trend Analysis, by Type

4.1.

Global

Cloud Kitchen Market Revenue (US$ Bn) Estimates and Forecasts, by Type, 2020 -

2033

4.1.1.Independent

4.1.2.Commissary/Shared Kitchen

4.1.3.Kitchen Pods

5. Global

Cloud Kitchen Market Estimates

& Forecast Trend Analysis, by Product Type

5.1.

Global

Cloud Kitchen Market Revenue (US$ Bn) Estimates and Forecasts, by Product Type,

2020 - 2033

5.1.1.Burger/Sandwich

5.1.2.Pizza/Pasta

5.1.3.Chicken

5.1.4.Seafood

5.1.5.Mexican/Asian Food

5.1.6.Others

6. Global

Cloud Kitchen Market Estimates

& Forecast Trend Analysis, by Nature

6.1.

Global

Cloud Kitchen Market Revenue (US$ Bn) Estimates and Forecasts, by Nature 2020 -

2033

6.1.1.Franchised

6.1.2.Standalone

7. Global

Cloud Kitchen Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Cloud Kitchen Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020

- 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Cloud

Kitchen Market: Estimates &

Forecast Trend Analysis

8.1. North America Cloud

Kitchen Market Assessments & Key Findings

8.1.1.North America Cloud

Kitchen Market Introduction

8.1.2.North America Cloud

Kitchen Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Type

8.1.2.2.

By Product Type

8.1.2.3.

By Nature

8.1.2.4. By Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Cloud

Kitchen Market: Estimates &

Forecast Trend Analysis

9.1. Europe Cloud Kitchen

Market Assessments & Key Findings

9.1.1.Europe Cloud Kitchen

Market Introduction

9.1.2.Europe Cloud Kitchen

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Type

9.1.2.2.

By Product Type

9.1.2.3.

By Nature

9.1.2.4. By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Cloud

Kitchen Market: Estimates &

Forecast Trend Analysis

10.1. Asia Pacific Market

Assessments & Key Findings

10.1.1.

Asia

Pacific Cloud Kitchen Market Introduction

10.1.2.

Asia

Pacific Cloud Kitchen Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1.

By Type

10.1.2.2.

By Product Type

10.1.2.3.

By Nature

10.1.2.4. By Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Cloud

Kitchen Market: Estimates &

Forecast Trend Analysis

11.1. Middle East & Africa

Market Assessments & Key Findings

11.1.1. Middle

East & Africa

Cloud Kitchen Market Introduction

11.1.2. Middle

East & Africa

Cloud Kitchen Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Type

11.1.2.2.

By Product Type

11.1.2.3.

By Nature

11.1.2.4. By Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Cloud Kitchen Market: Estimates &

Forecast Trend Analysis

12.1. Latin America Market

Assessments & Key Findings

12.1.1. Latin America Cloud

Kitchen Market Introduction

12.1.2. Latin America Cloud

Kitchen Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Type

12.1.2.2.

By Product Type

12.1.2.3.

By Nature

12.1.2.4. By Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13.

Country

Wise Market: Introduction

14.

Competition

Landscape

14.1. Global Cloud Kitchen

Market Product Mapping

14.2. Global Cloud Kitchen

Market Concentration Analysis, by Leading Players / Innovators / Emerging

Players / New Entrants

14.3. Global Cloud Kitchen

Market Tier Structure Analysis

14.4. Global Cloud Kitchen

Market Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

Rebel Foods

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2.

Kitchen United

15.3.

Zuul

15.4.

Travis Kalanick's CloudKitchens

15.5.

Starbucks (testing the model)

15.6.

DoorDash Kitchens

15.7.

Ghost Kitchen Brands

15.8.

The Local Culinary

15.9.

Keatz

15.10.

Kitopi

15.11.

Frankie's

15.12.

Dahmakan

15.13.

Swiggy (Access to its own kitchens)

15.14.

Zomato (Access to its own kitchens)

15.15.

Starbucks

15.16.

Wow! Momo Foods

15.17.

Other Prominent Players

16. Research

Methodology

16.1. External Transportations /

Databases

16.2. Internal Proprietary

Database

16.3. Primary Research

16.4. Secondary Research

16.5. Assumptions

16.6. Limitations

16.7. Report FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables