Cold Chain Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Services (Cold Chain Storage, Cold Chain Transportation, Others), By Temperature Type (Chilled, Frozen), By Application (Fruits and Vegetables, Meat, Fish, And Seafood Products, Dairy Products, Processed Food Products, Healthcare Products, Others) And Geography

2025-10-31

Consumer Products

Jaya Bundele (Research Analyst)

Description

Cold Chain Market Overview

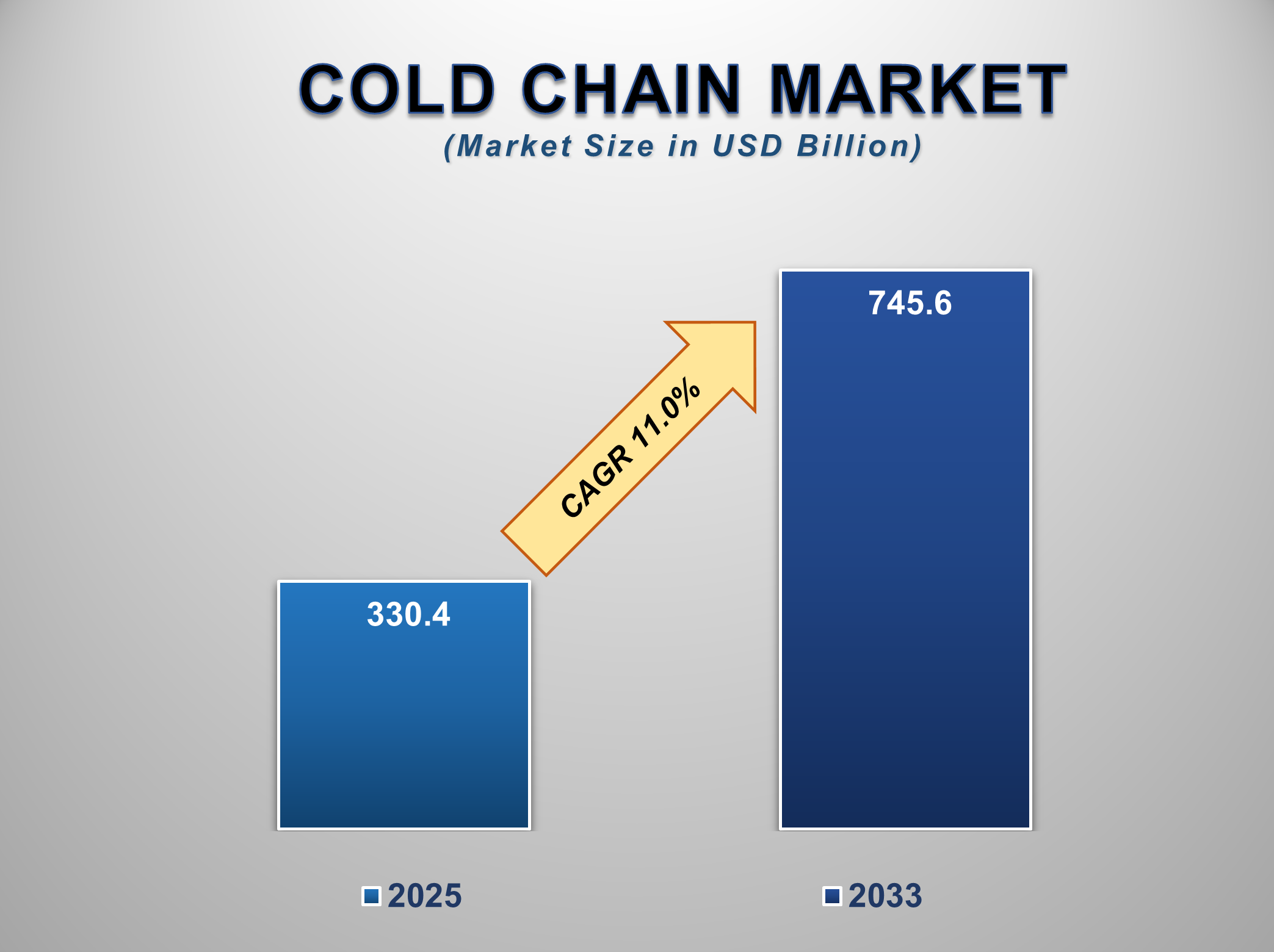

The global Cold Chain Market is projected to reach US$ 745.6 billion by 2033 from US$ 330.4 billion in 2025. The market is expected to register a CAGR of 11.0% during 2025–2033. This growth is primarily fuelled by the rising demand for temperature-sensitive products across industries such as pharmaceuticals, food & beverages, and chemicals.

Cold chains are defined as

temperature-managed supply chains that provide safe transportation, storage,

and delivery of perishables. With robust regulation surrounding the quality and

safety of food products and medications, companies are heavily investing in

cold chain infrastructure in the form of high-end refrigerator systems,

insulated shipping transport, and real-time monitoring systems. One of the

major driving reasons for the market includes the increasing need for frozen

and processed food as a result of urbanization, increasing income levels, and

changing food preferences. Also driving the market includes the rise in

e-commerce, as growing food expectations for fresh and perishable products to

be made available immediately contribute to driving cold chain logistics needs.

Cold chain market trends reveal a rise in the use of IoT-based tracking

systems, automated warehousing, and the use of blockchain for traceability that

improves efficiency and reduces spoilage. Government policies and investment in

transportation infrastructure in emerging nations also drive the cold chain

market to grow across the world.

Cold Chain Market Drivers

and Opportunities

Rising Demand for Perishable Food Products Is Anticipated to

Lift the Cold Chain Market During the Forecast Period

The increasing global demand

for perishables such as dairy products, meat products, seafood products,

fruits, and vegetables is largely driving the rise in the cold chain market.

With the rise in urbanization and expansion of middle-income households in emerging

economies, consumers are also preferring highly processed, frozen, and

convenience food products that require controlled storage and transportation

conditions. Besides that, globalization has made international trade of

perishables possible through long distances, hence the increase in the use of

cold chain logistics. Retailers' chains and e-commerce websites also fuel the

trend because a global supply of a broader range of perishables and

ready-to-eat foods, as well as fresh groceries that need to be transported and

warehoused in optimal temperatures, is made affordable. Food manufacturers as

well as retailers have also been forced to invest in cold transport and storage

due to this rising consumer preference. Moreover, international food safety standards

by organizations such as the FDA and WHO demand stringent compliance in terms

of temperatures to avert spoilage as well as contamination, hence the need for

a stringent cold chain infrastructure. These elements combined drive the

mounting rise in the cold chain market and make cold chain logistics a key

component in the global food supply chain.

Expansion of Global Trade in Temperature-Sensitive Goods Is a

Vital Driver for Influencing the Growth of the Global Cold Chain Market

Increased global trade in

temperature-sensitive products is another key driver of the cold chain market.

With international trade barriers diminishing and supply chains integrating,

there is an increasing need for advanced cold chain solutions to provide

product integrity over distances. Perishable products like fresh foods,

seafood, dairy products, and specialty chemicals are increasingly being

imported and exported across continents and need well-orchestrated cold chain

logistics. Advances in refrigeration and tracking technologies, including

GPS-based temperature monitoring and automated notification systems, have made

this expansion possible by improving supply chain visibility and management.

Governments and international bodies are also investing in the construction of

portside cold storage capacity to facilitate perishable exportation, for

example, in India, Brazil, and Vietnam. This investment adds to trade

competition that opens up new markets to local manufacturers. With the rise in

global food brands and health-focused consumers craving year-round access to

fresh imported products to match that timetable, the demand for dependable cold

chain solutions is building. Thus, international trade expansion, in

conjunction with the need for quality guarantees in the transportation of

products prone to heat and cold temperatures, continues to drive cold chain

market expansion.

Infrastructure Expansion in Developing Regions Is Poised to

Create Significant Opportunities in The Global Cold Chain Market

The global cold chain market is

expected to witness considerable growth through the establishment of cold

storage infrastructure in emerging markets in the Asia-Pacific, Latin America,

and Africa. These markets witness a steep increase in the demand for perishables

due to urbanization, growing disposable incomes, and changing consumption

patterns in favor of packaged and frozen food, fresh food products, and

temperature-sensitive biopharmaceuticals. In spite of the growing demand in

these markets, many of these markets lack a strong and reliable cold chain

infrastructure to support this churn and are highly desirable for investment

and expansion. The retail penetration by organized stores and e-commerce

platforms in these markets also adds to the demand for cold chain services.

Direct-to-consumer drug distribution and food imports across the border are

also becoming more prevalent, and for that to happen, a scalable cold chain

system must provide product safety and shelf life. Further, international development

agencies and private equity investors are investing in cold chain

infrastructure more and more as both a commercial opportunity and a source of

socioeconomic value. Thus, the emerging markets provide a unique opportunity

for cold chain companies to grow their operations, create tailored solutions,

and drive the future of temperature-conditioned logistics systems. Once the

gaps in infrastructure are bridged, these markets are set to make a major

contribution to the global cold chain market's overall expansion in the future.

Cold Chain Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 330.4 Billion |

|

Market Forecast in 2033 |

USD 745.6 Billion |

|

CAGR % 2025-2033 |

11.0% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production capacity, growth factors and more |

|

Segments Covered |

●

By Services ●

By Temperature Type ●

By Application |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Russia 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19) South Africa |

Cold Chain Market Report Segmentation Analysis

The Global Cold Chain Market

industry analysis is segmented by Services, by Temperature Type, by

Application, and by Region.

The Cold Chain Storage segment is anticipated to hold the

highest share of the global Cold Chain Market during the projected timeframe

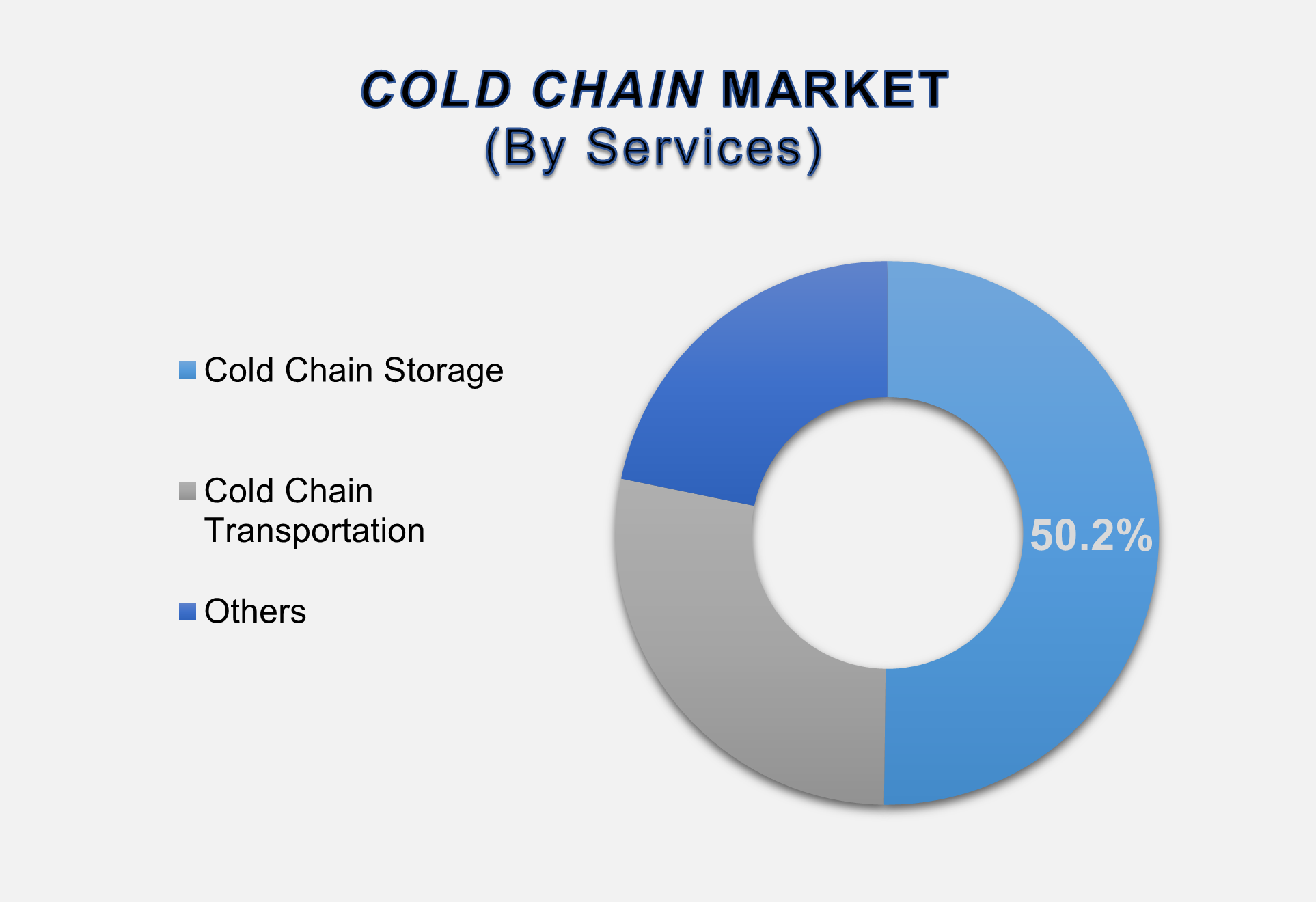

Based on Services, the market is segmented into Cold Chain Storage, Cold Chain Transportation, and others. In 2024, the Cold Chain Storage segment is anticipated to hold the highest share of 50.2% in the global cold chain market. This dominance is driven by the increasing demand for refrigerated storage facilities to preserve temperature-sensitive products such as dairy items, frozen foods, pharmaceuticals, and biologics. The growth of organized retail, the expansion of foodservice providers, and the rising popularity of ready-to-eat food items have contributed significantly to the need for advanced cold storage infrastructure. Moreover, regulations regarding food safety and pharmaceutical quality have mandated the use of compliant and controlled storage conditions, further fueling the segment’s growth.

The Frozen segment is anticipated to hold the highest share

of the market over the forecast period.

By Temperature Type, the market

is segmented into Chilled and Frozen. The Frozen segment is expected to capture

the largest part of the cold chain market worldwide in the forecast period.

This leadership comes due to the increasing global consumption of cold chain

frozen food products in the form of meat, seafood, ready-to-eat meals, and

bakery products that need to remain frozen along the supply chain to preserve

their quality and safety. Shifting lifestyles, urbanization, and the need for

food convenience have greatly fueled the use of frozen food globally. With the

expansion of frozen product lines across the food and pharmaceutical sector, as

well as in both food and healthcare industries, the frozen segment should

continue to dominate the temperature-controlled logistics in the next few

years.

The Dairy Products Construction segment dominated the market

in 2024 and is predicted to grow at the highest CAGR over the forecast period.

By Application, the market is

segmented into Fruits and Vegetables, Meat, Fish, and Seafood Products, Dairy

Products, Processed Food Products, Healthcare Products, and Others. Among

these, the Dairy Products segment was the largest in the cold chain market in

2024 and has the highest CAGR expected in the market in the forecast period.

Growth is chiefly triggered by the increased global consumption of milk,

cheese, butter, and other dairy by-products, which are highly perishable and

need stringent cold temperatures right from production to delivery. Rising

health awareness, the increasing need for high-protein diets, and the trend for

dairy-based food products are fueling the penetration of dairy product

consumption. With the government and industry stakeholders investing in

high-capacity chilled infrastructure, the dairy products segment will dominate

the cold chain application market in value as well as volume in the next

forecasted review period.

The following segments are part of an in-depth analysis of the global

cold chain market:

|

Market Segments |

|

|

By Services |

●

Cold Chain Storage ●

Cold Chain

Transportation ●

Others |

|

By Temperature Type |

●

Chilled ●

Frozen |

|

By Application |

●

Fruits and

Vegetables ●

Meat, Fish, And

Seafood Products ●

Dairy Products ●

Processed Food

Products ●

Healthcare Products ●

Others |

Cold Chain Market Share

Analysis by Region

North America is projected to hold the largest share of the

global Cold Chain Market over the forecast period

North America was the leader in

the cold chain market in 2024, capturing a substantial 38.2% of the market. The

leadership in the region stems from a well-established logistics system, high

technological advancements in cold storage and transportation, and stringent

food and pharmaceutical safety standards. The United States alone has a high

concentration of major companies heavily investing in cold storage and

transportation systems to accommodate developing demand in various industries.

Strong dependence on frozen and prepared food by consumers and a rising trend

for shopping through the internet for groceries have highly fueled the cold

chain demand in the retail and foodservice markets. In addition to this, the

biologics, vaccines, and specialty drug companies in North America are among

the major drivers of cold chain growth due to the delicate nature of these

products. Government regulations and standards, such as the Food Safety

Modernization Act (FSMA) in the U.S, are also increasingly fostering the need

for efficient cold chain systems that deliver quality and compliance along the

supply chain.

The Asia Pacific region is

expected to expand at the highest CAGR in the forecast period, driven by high

urbanization rates, growing middle-class earnings, rising need for consumables,

and strong investments in cold chain infrastructure in nations such as China,

India, and Southeast Asia.

Cold Chain Market

Competition Landscape Analysis

The cold chain market is highly

competitive and fragmented, with major players like AmeriCold Logistics,

Lineage Logistics, VersaCold, and Nichirei Logistics Group dominating the

space. To strengthen their competitive edge, these companies are expanding their

fleets of multi-compartment reefer vehicles, enabling them to deliver enhanced

services to customers. Additionally, leading firms are investing in advanced

technologies to improve operational efficiency, product safety, and supply

chain integrity.

Global Cold Chain Market

Recent Developments News:

●

In November 2024,

Lineage, Inc., acquired the assets of

Coldpoint, a Kansas City-based cold storage and logistics provider,

strengthening its presence in the region. The deal adds Coldpoint’s

621,000-square-foot facility with intermodal rail access to Lineage’s network,

enhancing connectivity along key protein supply routes. This strategic

expansion bolsters Lineage’s capabilities in serving U.S. ports and reinforces

its position as a leader in temperature-controlled logistics.

●

In November 2024, CJ

Logistics America unveiled a cutting-edge 270,000-square-foot cold storage

facility in Georgia, strategically positioned near major transport hubs in a

vital poultry-producing region. The warehouse features advanced refrigeration,

blast freezing technology, and 30,000 racked pallet positions, offering

customized storage for proteins, bakery goods, and finished products—complete

with on-site USDA inspection services. This expansion underscores CJ Logistics

America's dedication to providing world-class cold chain solutions for global

brands.

●

In December 2022, A.P.

Moller-Maersk (Denmark) launched its

state-of-the-art integrated cold chain facility at the Ruakura Superhub in

Hamilton, New Zealand. This strategic investment positions Hamilton as a

pivotal logistics hub within the country’s Golden Triangle, enhancing supply

chain efficiency for temperature-sensitive goods.

The Global Cold Chain Market is dominated by a few large

companies, such as

●

Americold Logistics

●

Lineage Logistics

●

AGRO Merchants Group

●

Nichirei Corporation

●

Preferred Freezer Services

●

Swire Cold Storage

●

Kloosterboer

●

DHL Global Forwarding

●

UPS Cold Chain Solutions

●

FedEx Custom Critical

●

Burris Logistics

●

Maersk Line

● Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

- Global Cold Chain Market Introduction and Market Overview

- Objectives of the Study

- Global Cold Chain Market Scope and Market Estimation

- Global Cold Chain Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Cold Chain Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

- Market Segmentation

- Services of Global Cold Chain Market

- Temperature Type of Global Cold Chain Market

- Application of Global Cold Chain Market

- Region of Global Cold Chain Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Key Product/Brand Analysis

- Technological Advancements

- Key Developments

- Porter’s Five Forces Analysis

- Bargaining Power of Suppliers

- Bargaining Power of Buyers

- Threat of Substitutes

- Threat of New Entrants

- Competitive Rivalry

- PEST Analysis

- Political Factors

- Economic Factors

- Social Factors

- Technology Factors

- Insights on Cost-effectiveness of Cold Chain

- Key Regulation

- Global Cold Chain Market Estimates & Historical Trend Analysis (2020 - 2024)

- Global Cold Chain Market Estimates & Forecast Trend Analysis, by Services

- Global Cold Chain Market Revenue (US$ Bn) Estimates and Forecasts, by Services, 2020 - 2033

- Cold Chain Storage

- Cold Chain Transportation

- Others

- Global Cold Chain Market Revenue (US$ Bn) Estimates and Forecasts, by Services, 2020 - 2033

- Global Cold Chain Market Estimates & Forecast Trend Analysis, by Temperature Type

- Global Cold Chain Market Revenue (US$ Bn) Estimates and Forecasts, by Temperature Type, 2020 - 2033

- Chilled

- Frozen

- Global Cold Chain Market Revenue (US$ Bn) Estimates and Forecasts, by Temperature Type, 2020 - 2033

- Global Cold Chain Market Estimates & Forecast Trend Analysis, by Application

- Global Cold Chain Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- Fruits and Vegetables

- Meat, Fish, and Seafood Products

- Dairy Products

- Processed Food Products

- Healthcare Products

- Others

- Global Cold Chain Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- Global Cold Chain Market Estimates & Forecast Trend Analysis, by Region

- Global Cold Chain Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Cold Chain Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

- North America Cold Chain Market: Estimates & Forecast Trend Analysis

- North America Cold Chain Market Assessments & Key Findings

- North America Cold Chain Market Introduction

- North America Cold Chain Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Services

- By Temperature Type

- By Application

- By Country

- The U.S.

- Canada

- North America Cold Chain Market Assessments & Key Findings

- Europe Cold Chain Market: Estimates & Forecast Trend Analysis

- Europe Cold Chain Market Assessments & Key Findings

- Europe Cold Chain Market Introduction

- Europe Cold Chain Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Services

- By Temperature Type

- By Application

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Rest of Europe

- Europe Cold Chain Market Assessments & Key Findings

- Asia Pacific Cold Chain Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Cold Chain Market Introduction

- Asia Pacific Cold Chain Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Services

- By Temperature Type

- By Application

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Cold Chain Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Cold Chain Market Introduction

- Middle East & Africa Cold Chain Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Services

- By Temperature Type

- By Application

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Cold Chain Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Cold Chain Market Introduction

- Latin America Cold Chain Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Services

- By Temperature Type

- By Application

- By Country

- Brazil

- Argentina

- Mexico

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Cold Chain Market Product Mapping

- Global Cold Chain Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Cold Chain Market Tier Structure Analysis

- Global Cold Chain Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

- Americold Logistics

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Americold Logistics

* Similar details would be provided for all the players mentioned below

- Lineage Logistics

- AGRO Merchants Group

- Nichirei Corporation

- Preferred Freezer Services

- Swire Cold Storage

- Kloosterboer

- DHL Global Forwarding

- UPS Cold Chain Solutions

- FedEx Custom Critical

- Burris Logistics

- Maersk Line

- Others

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables