Collision Avoidance Sensors Market Size and Forecast (2026 - 2034), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Sensor Type (Radar Sensors, LiDAR Sensors, Ultrasonic Sensors, Camera Sensors and Infrared Sensors); By Technology (Forward Collision Warning Systems, Automatic Emergency Braking Systems, Blind Spot Detection Systems, Lane Departure Warning Systems and Adaptive Cruise Control Systems); By Vehicle Type (Passenger Vehicles, Commercial Vehicles and Autonomous Vehicles); By Application (Automotive Safety Systems, Industrial Safety Systems, Aerospace & Defense, Robotics & Drones and Others) and Geography

2026-03-12

Semiconductor and Electronics

Ekta Chaurasia (Team Lead)

Description

Collision Avoidance Sensors Market Overview

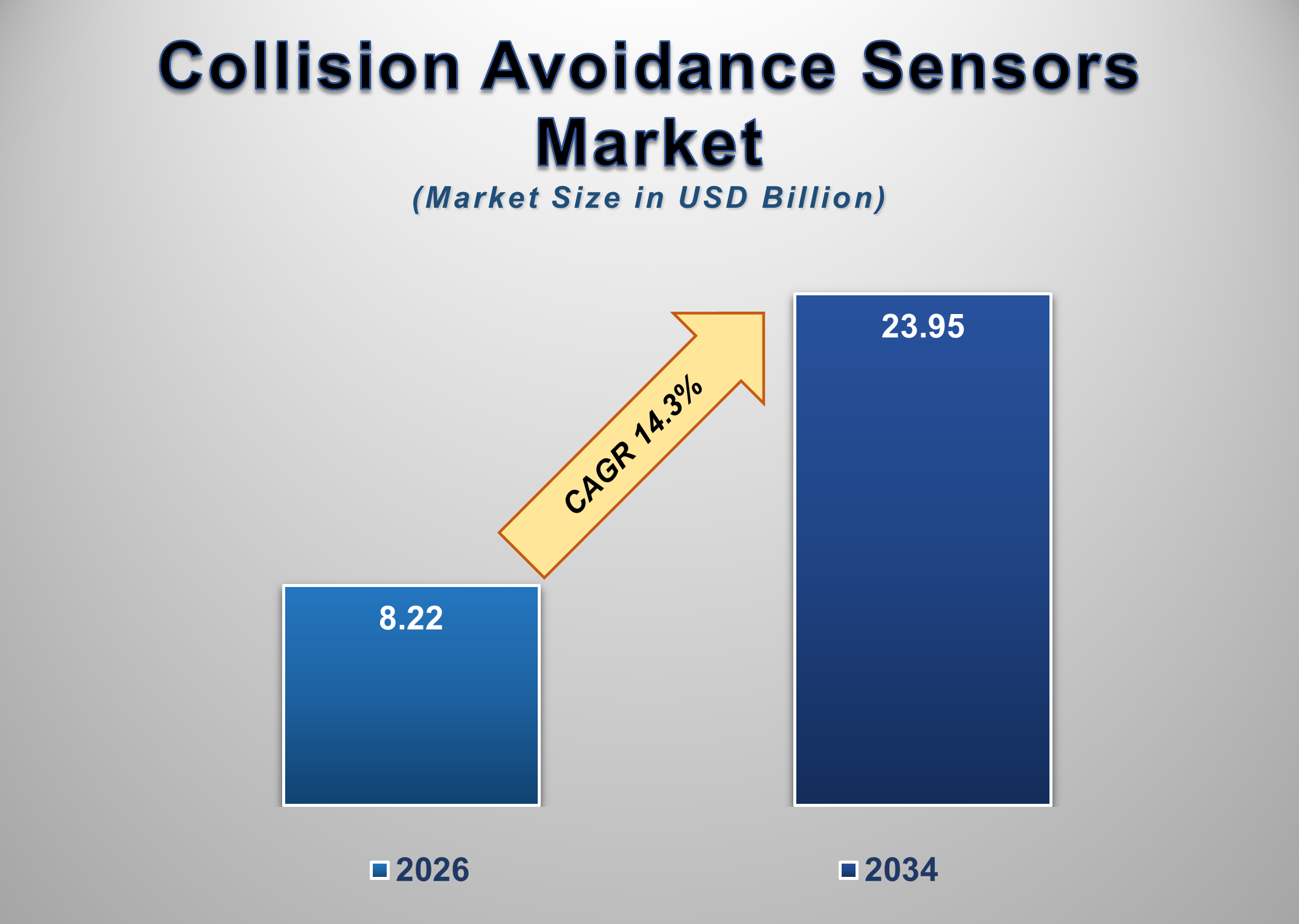

The global Collision Avoidance Sensors Market is witnessing substantial growth as industries increasingly prioritize safety technologies designed to prevent accidents and improve operational awareness. The market is valued at USD 8.22 billion in 2026 and is projected to reach USD 23.95 billion by 2034, expanding at a CAGR of 14.3% during the forecast period.

Collision avoidance sensors are advanced sensing devices designed to detect nearby objects, obstacles, vehicles, or pedestrians and provide real-time warnings or automatic corrective actions to prevent accidents. These sensors form a core component of modern driver assistance systems and autonomous technologies. By using technologies such as radar, LiDAR, ultrasonic sensing, and machine vision cameras, collision avoidance systems can analyze the environment around a vehicle or machine and identify potential hazards before a collision occurs.

In the automotive sector, these sensors play a vital role in advanced driver assistance systems (ADAS), enabling features such as automatic emergency braking, adaptive cruise control, blind-spot monitoring, and lane departure warnings. Increasing consumer awareness of vehicle safety, along with stringent government regulations mandating advanced safety systems, has significantly accelerated the adoption of collision-avoidance sensors across passenger and commercial vehicles.

Beyond automotive applications, collision avoidance sensors are also widely used in industries such as aerospace, robotics, industrial automation, and maritime navigation. In industrial environments, these sensors help prevent collisions among equipment in warehouses, factories, and construction sites, where automated machines and mobile robots operate in shared spaces with human workers.

Technological advancements are further enhancing the capabilities of these sensors. Improvements in sensor accuracy, signal processing algorithms, and artificial intelligence integration are enabling faster object detection and improved situational awareness. As industries continue to adopt automation and intelligent mobility systems, demand for reliable collision-avoidance sensors is expected to grow steadily over the coming years.

Collision Avoidance Sensors Market Drivers and Opportunities

Increasing Adoption of Advanced Driver Assistance Systems (ADAS) is anticipated to drive the Collision Avoidance Sensors market growth

The increasing adoption of advanced driver assistance systems in modern vehicles is a primary driver of the expansion of the collision-avoidance sensors market. Automakers are integrating sophisticated sensor technologies into vehicles to enhance driver awareness and improve road safety. Features such as forward collision warning, automatic emergency braking, blind-spot detection, and lane-keeping assistance rely heavily on sensor-based environmental monitoring systems.

Governments and safety organizations worldwide are also encouraging the adoption of ADAS technologies through regulatory frameworks and safety rating programs. For example, vehicle safety assessment programs in regions such as Europe, North America, and Asia increasingly require advanced safety technologies for higher safety ratings. These regulations are motivating automobile manufacturers to incorporate radar, camera, and ultrasonic sensors into both premium and mid-range vehicle models.

Additionally, consumer demand for safer vehicles has increased significantly in recent years. Buyers are increasingly prioritizing safety features when purchasing vehicles, prompting automakers to integrate multiple sensors and detection systems to improve driver protection and reduce accident risks. As a result, the adoption of collision avoidance sensors is expanding rapidly across the global automotive industry.

Rapid Development of Autonomous and Semi-Autonomous Vehicles is accelerating market expansion

The development of autonomous and semi-autonomous vehicles is significantly influencing the demand for advanced sensing technologies capable of accurately detecting surrounding objects and road conditions. Autonomous driving systems rely heavily on a combination of sensors, including radar, LiDAR, cameras, and ultrasonic sensors, to build a comprehensive understanding of the environment.

These sensors continuously collect real-time data about vehicle surroundings and transmit the information to onboard computing systems that analyze traffic patterns, detect obstacles, and determine safe driving actions. High-precision sensors are essential for enabling safe automated navigation, especially in complex urban environments where vehicles must detect pedestrians, cyclists, and other moving objects.

Furthermore, advancements in sensor fusion technologies are improving the reliability of collision avoidance systems. By combining data from multiple sensors, autonomous driving platforms can achieve higher accuracy in object detection and situational awareness. This integration of sensor technologies is driving increased investments in research and development across the automotive and electronics industries.

As the development of autonomous mobility ecosystems continues to accelerate, collision avoidance sensors will remain an indispensable component of intelligent transportation systems.

Expansion of Industrial Automation and Robotics presents significant market opportunities

The rapid expansion of industrial automation and robotics is creating new opportunities for collision avoidance sensor technologies. Automated machines, robotic systems, and autonomous mobile robots are increasingly deployed in warehouses, factories, logistics centers, and construction environments where safety is a critical priority.

Collision avoidance sensors enable automated machines to detect obstacles and prevent accidents during operation. For example, autonomous warehouse robots rely on sensors to navigate storage facilities, detect obstacles, and safely interact with human workers. Similarly, construction equipment equipped with proximity sensors can detect nearby workers and prevent accidental collisions.

In addition, the rise of smart factories and Industry 4.0 initiatives is driving the adoption of sensor-enabled automation systems capable of monitoring operational environments in real time. Advanced sensing technologies improve operational safety while also enhancing the efficiency of automated workflows.

As industries continue to integrate robotics, autonomous vehicles, and intelligent machines into their operations, the demand for reliable collision avoidance sensors is expected to increase significantly.

Collision Avoidance Sensors Market Scope

Collision Avoidance Sensors Market Report Segmentation Analysis

The global Collision Avoidance Sensors Market industry analysis is segmented by sensor type, technology, vehicle type, application, and region.

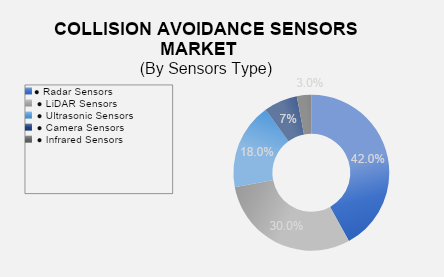

Radar Sensors dominate the Sensor Type Segment

By sensor type, the market is segmented into radar sensors, LiDAR sensors, ultrasonic sensors, camera sensors, and infrared sensors. Radar sensors currently dominate the market because they provide reliable object detection over long distances and perform effectively in challenging environmental conditions such as rain, fog, and low visibility. Automotive manufacturers widely use radar sensors in adaptive cruise control and collision warning systems due to their accuracy and durability.

Automatic Emergency Braking Systems lead the Technology Segment

Based on technology, the market includes forward collision warning systems, automatic emergency braking systems, blind spot detection systems, lane departure warning systems, and adaptive cruise control systems. Automatic emergency braking systems hold the largest share because they can automatically apply vehicle brakes when a collision risk is detected. This feature significantly reduces accident severity and is increasingly becoming a standard safety feature in modern vehicles.

Passenger Vehicles dominate the Vehicle Type Segment

In terms of vehicle type, the market is segmented into passenger vehicles, commercial vehicles, and autonomous vehicles. Passenger vehicles dominate the segment because global automobile manufacturers are rapidly integrating advanced safety technologies into cars to comply with safety regulations and enhance consumer protection.

Automotive Safety Systems represent the largest Application Segment

Based on application, the market is segmented into automotive safety systems, industrial safety systems, aerospace & defense, robotics & drones, and others. Automotive safety systems account for the largest market share due to widespread adoption of driver assistance technologies across passenger and commercial vehicles.

The following segments are part of an in-depth analysis of the global Collision Avoidance Sensors Market:

Market Segments

Collision Avoidance Sensors Market Share Analysis by Region

North America is projected to hold a significant share of the global collision avoidance sensors market due to strong adoption of advanced vehicle safety technologies and the presence of major automotive technology companies. The United States leads the regional market due to high penetration of ADAS technologies and strong consumer demand for vehicles equipped with advanced safety features.

Europe also represents a major market for collision avoidance sensors, supported by strict vehicle safety regulations and widespread adoption of driver assistance systems. Countries such as Germany, France, and the United Kingdom have well-established automotive manufacturing industries that actively integrate advanced sensor technologies into modern vehicles.

Asia-Pacific is expected to be the fastest-growing region during the forecast period. Rapid growth in vehicle production, increasing adoption of advanced automotive safety technologies, and expanding automotive manufacturing sectors in countries such as China, India, Japan, and South Korea are driving strong regional market growth.

Global Collision Avoidance Sensors Market Recent Developments News

o In July 2025, Bosch introduced an advanced radar-based collision avoidance sensor designed for next-generation driver assistance systems.

o In May 2025, Continental AG launched a new LiDAR sensor platform aimed at improving object detection capabilities for autonomous vehicles.

o In March 2025, Denso Corporation expanded its automotive sensor manufacturing capacity to support increasing demand for ADAS technologies.

The Global Collision Avoidance Sensors Market is dominated by a few large companies, such as

● Bosch

● Continental AG

● Denso Corporation

● Valeo SA

● ZF Friedrichshafen AG

● Aptiv PLC

● Analog Devices

● Texas Instruments

● Infineon Technologies

● Velodyne LiDAR

● Luminar Technologies

● Garmin Ltd.

● Honeywell International

● Omron Corporation

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Collision Avoidance Sensors Market Introduction and Market Overview 1.1. Objectives of the Study 1.2. Market Segmentation 1.2.1. Sensor Type of Global Collision Avoidance Sensors Market 1.2.2. Technology of Global Collision Avoidance Sensors Market 1.2.3. Vehicle Type of Global Collision Avoidance Sensors Market 1.2.4. Application of Global Collision Avoidance Sensors Market 1.2.5. Region of Global Collision Avoidance Sensors Market 1.3. Competition Coverage List of Market Participants 1.4. Market Definition: Collision Avoidance Sensors Market 2. Executive Summary 2.1. Global Collision Avoidance Sensors Market Estimation & Forecast 2.1.1. Global Collision Avoidance Sensors Market Size (US$ Million) Estimates & Historical Trend Analysis (2021 - 2025) 2.1.2. Global Collision Avoidance Sensors Overall Market Size (US$ Million), Growth Rate (Y-o- Y), Market CAGR (%), Market Forecast (2026 - 2034) 2.2. Snapshot of Global Collision Avoidance Sensors Market 2.3. Global Collision Avoidance Sensors Market Revenue Share (%) 2025 2.4. REGIONAL OUTLINE: Revenue CAGR, by Region 2.5. Key Competitors & Key Insights

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables