Connected Car Market Size and Forecast (2026 - 2034), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; Technology (3G, 4G/LTE, and 5G), Connectivity Solutions (Integrated, Embedded, and Tethered), Service (Driver assistance, Safety, Entertainment, Well-being, Vehicle management, and Mobility management), Sales Channel (OEM and Aftermarket), and Geography

2026-07-07

Automotive & Transportation (Mobility)

Ekta Chaurasia (Team Lead)

Description

Connected

Car Market Overview

The

global connected car market is experiencing strong growth, driven by increasing

demand for advanced in-vehicle connectivity, rising adoption of smart

technologies, and the growing integration of IoT in the automotive sector. Valued

at USD 14.81 billion in 2026, the market is projected to reach USD 37.75 billion

by 2034, growing at a CAGR of 14.3% during the forecast period.

Connected cars are vehicles equipped with

internet connectivity and advanced communication technologies that enable

real-time data transmission between

the car, driver, infrastructure, and external devices are referred to as

connected cars. By combining telematics, infotainment systems, advanced driver

assistance systems (ADAS), and vehicle-to-everything (V2X) communication, this

ecosystem enhances driving experience, safety, and

convenience.

The market has been

expanding rapidly as a result of growing consumer demand for better in-car

experiences, growing smart device use, and the quick advancement of automotive

electronics. Connectivity services like navigation, predictive maintenance,

remote diagnostics, and over-the-air (OTA) software upgrades are becoming more

and more integrated by automakers. Adoption is also being accelerated by the

promotion of intelligent transportation systems and automobile safety laws by

regional governments.

Increasing focus on vehicle safety and

security is a key driver of market growth. Features like collision avoidance alerts, real-time vehicle tracking,

and emergency call systems (eCall) are made possible by connected cars and significantly reduce the risk of accidents. Additionally, the development of 5G networks

is essential for providing dependable communication, low latency, and faster

data transmission, which supports cutting-edge applications like autonomous

driving.

In addition to their robust technological infrastructure, high vehicle

penetration, and early adoption of linked technology, North America and Europe

dominate the market from a regional standpoint. In the meantime, rapid

urbanization, rising disposable income, and expanding automobile production in

nations like China, Japan, and India are making Asia-Pacific a lucrative

market.

Despite the market's

potential for expansion, concerns with data privacy, cybersecurity threats, and

high implementation are present. However, it is anticipated that ongoing

developments in IoT, cloud computing, and artificial intelligence will resolve

these problems and open up new business prospects. As a result, the market for

connected cars is expected to grow significantly due to technical advancements,

changing consumer demands, and the automotive sector's move toward digitization

and mobility-as-a-service.

Connected Car Market Drivers and Opportunities

Rising Demand for Enhanced In-Car

Connectivity and User Experience

The need for sophisticated in-car networking services

is being driven by consumers' growing expectation that their cars would serve

as extensions of their digital lives. Convenience and customization are greatly

increased by modern connected cars' smooth connection with smartphones, voice

assistants, navigation systems, and entertainment platforms. Rather than being

high-end add-ons, features like infotainment services, remote car access, and

real-time traffic information are now considered standard. Additionally,

automakers are being encouraged to make significant investments in connection

solutions by the increasing use of digital ecosystems and subscription-based

services in automobiles. One of the main factors driving the global expansion

of the connected car industry is the shift in consumer preferences toward

smarter, more engaging driving experiences.

Increasing Focus on Vehicle Safety

and Government Regulations

The adoption of

connected car technology is being further accelerated by governments and regulatory

agencies around the world requiring the incorporation of cutting-edge safety

measures in automobiles. Connectivity is essential to the operation of systems

like collision detection, real-time diagnostics, vehicle tracking, and

emergency call (eCall). In addition to improving passenger safety, these

technologies aid in lowering traffic fatalities and accidents.

Vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication is

also becoming more and more necessary due to initiatives supporting smart city

development and intelligent transportation systems. As a result, automakers are

using connected solutions to enhance safety standards and adhere to laws, which

is a crucial factor in the market's growth.

Expansion of 5G and

Vehicle-to-Everything (V2X) Communication

By facilitating

quicker, more dependable, and low-latency communication, the deployment of 5G

networks offers a substantial opportunity for the connected car sector. The

development of vehicle-to-everything (V2X) technologies, which enable real-time

communication between automobiles, infrastructure, pedestrians, and networks,

is aided by this progress. The development of autonomous driving, traffic

control, and improved road safety depend on such capabilities. Furthermore,

real-time video streaming, cloud-based services, and over-the-air upgrades are

among the high-bandwidth applications that 5G enables. Automakers and

technology companies can use these skills to launch cutting-edge services,

generating new revenue streams and revolutionizing the future of mobility as

telecom infrastructure continues to grow globally.

Connected Car Market Scope

|

Report Attributes |

Description |

|

Market Size in 2026 |

USD 14.81 Billion |

|

Market Forecast in 2034 |

USD 37.75 Billion |

|

CAGR % 2026-2034 |

14.3% |

|

Base Year |

2024 |

|

Historic Data |

2021-2025 |

|

Forecast Period |

2026-2034 |

|

Report USP |

Comprehensive

global connected car market size and forecast analysis with detailed

segmentation by Technology, Connectivity Solutions, Service, Sales Channel,

and geography. The report provides in-depth insights into market share,

competitive landscape, and strategic positioning of key players. It includes

a detailed analysis of growth drivers, challenges, and emerging opportunities

influencing market expansion. The study evaluates technological advancements

in telematics, advanced driver assistance systems (ADAS),

vehicle-to-everything (V2X) communication, and over-the-air (OTA) updates,

along with evolving consumer demand for enhanced in-vehicle connectivity and

digital experiences. Additionally, the report offers regional and

country-level market trends, regulatory landscape assessment, and strategic

developments such as product launches, partnerships, collaborations, and

expansions, enabling stakeholders, automotive manufacturers, technology

providers, and investors to make informed business decisions |

|

Segments Covered |

●

By Technology ●

By Connectivity

Solutions ●

By Service ●

By Sales Channel |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Switzerland 9)

China 10) India 11) Japan 12) South Korea 13) Australia 14) Mexico 15) Brazil 16) Argentina 17) Saudi Arabia 18) UAE 19) South Africa |

Connected Car Market

Report Segmentation Analysis

The global connected car market

analysis is segmented by Technology, Connectivity Solutions, Service, Sales

Channel, and Region.

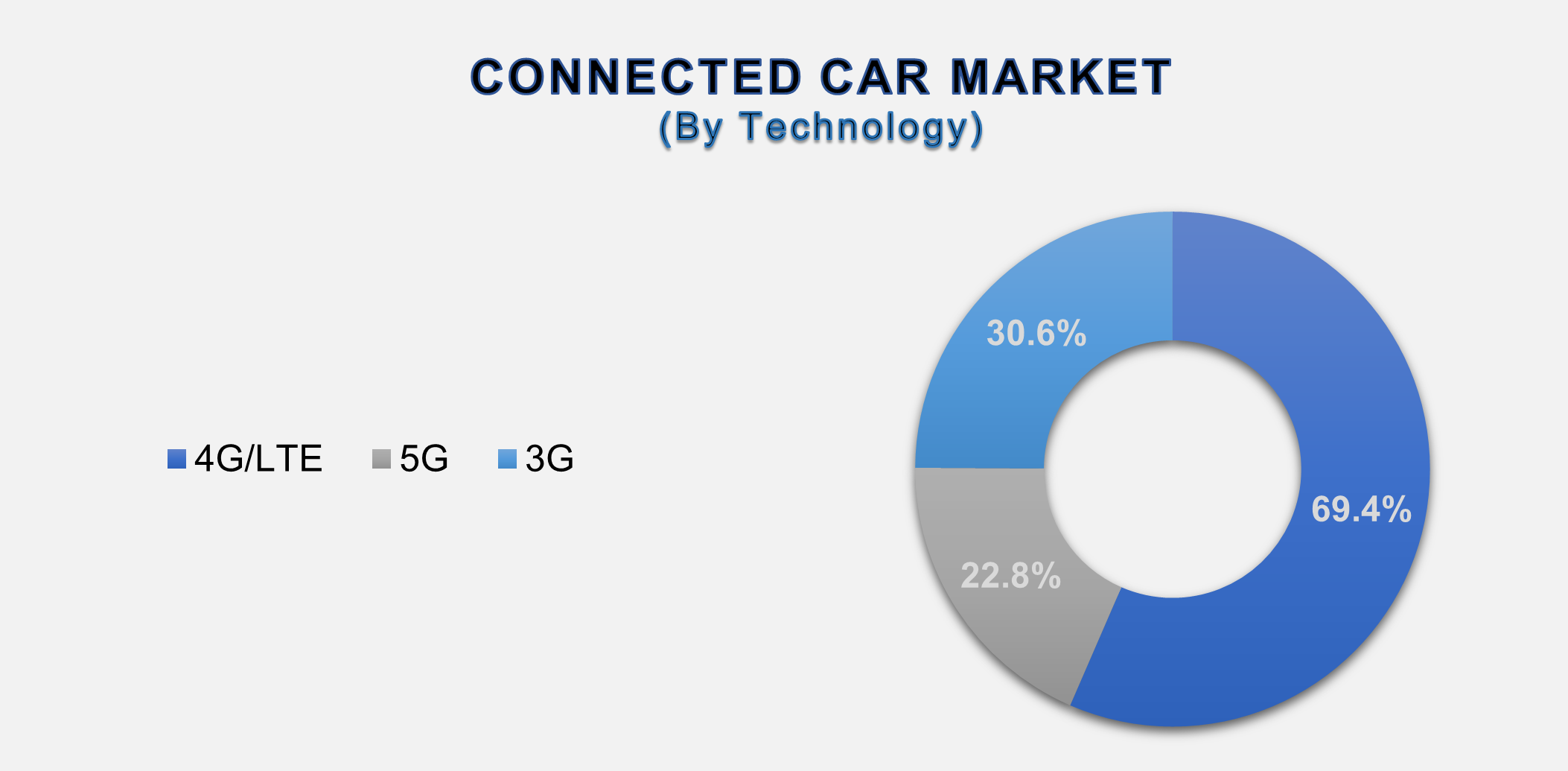

4G/LTE segment dominated

the market in 2025 and is projected to grow at the highest CAGR during the

forecast period.

By Technology, the connected car

market is segmented into 3G, 4G/LTE, and 5G. 4G/LTE dominates the connected car

market. 4G/LTE technology is essential for enabling connected car features

because it offers dependable, fast wireless communication. Real-time

navigation, remote diagnostics, infotainment streaming, and over-the-air (OTA)

updates are among the key features it provides. 4G/LTE continues to be the

foundation of contemporary connected car ecosystems due to its extensive

worldwide coverage and well-established infrastructure, guaranteeing reliable

access even in non-urban regions. LTE is used by automakers to provide

emergency support, vehicle tracking, and telematics services. Due to its

affordability, scalability, and interoperability with current technologies,

4G/LTE remains the dominant technology in the connected automobile sector,

despite the emergence of 5G.

Integrated segment holds

the highest share of the connectivity solutions segment over the forecast

period

Based on connectivity solutions, the

market is bifurcated into integrated,

embedded, and tethered. The integrated segment accounts for the largest share

of the market. The term "integrated connectivity" describes embedded

communication technologies that are included right into the car during

production, allowing for constant and easy internet access without the need for

additional equipment. To provide features like real-time navigation, remote

diagnostics, emergency services, and over-the-air (OTA) updates, these systems

usually use embedded SIM (eSIM) technology and specialized onboard modules.

Compared to tethered or smartphone-based connectivity, integrated solutions

offer greater security, dependability, and consistent performance. This

strategy is becoming more and more popular among automakers since it gives them

complete control over data, improves user experience, and supports cutting-edge

applications like telematics and vehicle-to-everything (V2X) communication,

making it a crucial market niche for connected cars.

Driver Assistance segment holds the highest share of the service

segment over the forecast period

Based on service, the market is

bifurcated into driver assistance, safety, entertainment, well-being, vehicle

management, and mobility management. The driver assistance segment accounts for

the largest share of the market. Driver assistance refers to a set of advanced

technologiesintended to decrease human error, increase vehicle safety, and improve

driving comfort. These systems, which are sometimes grouped under Advanced

Driver Assistance Systems (ADAS), use sensors, cameras, radar, and

communication elements to monitor the vehicle’s surroundings around the car and assist the driver in real time. Lane

departure warning, adaptive cruise control, automatic emergency braking,

parking assistance, and blind-spot recognition are some of the main features.

These systems can obtain real-time data due to connected automobile

connectivity, which increases their responsiveness and accuracy. Driver

assistance technologies are becoming commonplace as consumer awareness rises

and road safety laws tighten, which is crucial to the expansion of the

connected car market.

OEM segment holds the highest share of the sales

channel segment over the forecast period

Based on sales channel, the market is

bifurcated into OEM and aftermarket. The OEM segment accounts for the largest

share of the market. OEMs (Original Equipment Manufacturers) are key

players in the connected car market since they design, produce, and incorporate

connectivity technologies directly into automobiles. To provide seamless

connectivity, these businesses—which are mostly automakers—embed technology

like telematics units, infotainment platforms, and advanced driver assistance

systems (ADAS). To allow features like in-car digital services, real-time

diagnostics, and over-the-air (OTA) upgrades, OEMs work with software

developers, telecom operators, and technology providers. Better performance,

security, and user experience are guaranteed by their great control over

hardware and software integration. In an effort to create new revenue streams,

OEMs are concentrating more on digital ecosystems and subscription-based

services as competition heats up.

The following

segments are part of an in-depth analysis of the global Connected Car Market:

|

Market

Segments |

|

|

By

Technology |

● 4G/LTE ● 5G ● 3G |

|

By

Connectivity Solutions |

● Integrated ● Embedded ● Tethered |

|

By

Service |

● Driver assistance ● Safety ● Entertainment ● Well-being ● Vehicle management ● Mobility management |

|

By

Sales Channel |

● OEM ● Aftermarket |

Connected Car Market Share Analysis by Region

Europe region is projected

to hold the largest share of the global connected car market over the forecast

period.

Europe is projected to

hold the largest share of the global connected car market during the forecast

period. Strong legislative frameworks, high vehicle penetration, and early

adoption of automotive advances have made Europe a developed and

technologically advanced market for connected automobiles. The region has led

the way in enforcing car safety regulations, such as the mandatory installation

of eCall systems, which has greatly sped up the incorporation of connectivity

capabilities. Furthermore, the presence of leading

automotive manufacturers and a

solid automotive ecosystem foster ongoing innovation in advanced driving

assistance systems (ADAS), infotainment, and telematics.

Global Connected Car Market Recent Developments News:

·

In June 2024, the U.S.

Department of Transportation announced nearly USD 60 million in grants to accelerate

vehicle-to-everything (V2X) deployment, supporting connected vehicle

infrastructure and road safety initiatives.

·

In December 2024, Sonatus

expanded its connected vehicle software deployment to over 3 million vehicles

globally, highlighting the growing adoption of software-defined and OTA-enabled

platforms.

The Global Connected Car Market is dominated by a few large

companies, such as

· General Motors Company

· Ford Motor Company

· BMW AG

· Mercedes-Benz Group AG

· Toyota Motor Corporation

· Volkswagen AG

· Audi AG

· Tesla, Inc.

· Nissan Motor Corporation

· Hyundai Motor Company

· Robert Bosch GmbH

· Continental AG

· Qualcomm Technologies, Inc.

· Harman International

· Visteon Corporation

· NXP Semiconductors N.V.

· DENSO Corporation

· AT&T Inc.

· Verizon Communications Inc.

· TomTom International B.V.

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1.

Global

Connected Car Market Introduction and Market Overview

1.1. Objectives of the Study

1.2. Market Segmentation

1.2.1.Technology of Global Connected Car Market

1.2.2.Connectivity Solutions of Global Connected Car

Market

1.2.3.Service of Global Connected Car Market

1.2.4.Sales Channel of Global Connected Car Market

1.2.5.Region of Global Connected Car Market

1.3. Competition Coverage List of

Market Participants

1.4. Market Definition: Connected Car

Market

2.

Executive Summary

2.1. Global Connected Car Market

Estimation & Forecast

2.1.1.Global Connected Car Market Size

(US$ Million) Estimates & Historical Trend Analysis (2021 - 2025)

2.1.2.Global Connected Car Overall

Market Size (US$ Million), Growth Rate (Y-o-Y), Market CAGR (%), Market

forecast (2026 - 2034)

2.2. Snapshot of Global Connected Car

Market

2.3. Global Connected Car Market

Revenue Share (%) 2025

2.4. REGIONAL OUTLINE: Revenue CAGR,

by Region

2.5. Key Competitors & Key

Insights

3.

Market Overview (Qualitative

Analysis)

3.1. Demand Side Trends

3.2. Supply Side Trends /

Manufacturing Trends

3.3. Demand and Opportunity Assessment,

2026 - 2034

3.4. Market Dynamics

3.4.1.Drivers

3.4.2.Limitations

3.4.3.Opportunities

3.4.4.Impact Analysis of Drivers and

Restraints

3.5. Key Developments

3.6. Regulatory Landscape

3.7. Value Chain / Ecosystem Analysis

3.8. Porter’s Five Forces Analysis

3.8.1.Bargaining Power of Suppliers

3.8.2.Bargaining Power of Buyers

3.8.3.Threat of Substitutes

3.8.4.Threat of New Entrants

3.8.5.Competitive Rivalry

3.9. PEST Analysis

3.9.1.Political Factors

3.9.2.Economic Factors

3.9.3.Social Factors

3.9.4.Technology Factors

4.

Global Connected Car Market

Estimates & Forecast Trend Analysis, by Technology

4.1. Global Connected Car Market

Assessments & Key Findings, by Technology

4.2. Global Connected Car Market

Revenue (US$ Million) Estimates and Forecasts, by Technology, 2021 - 2034

4.2.1.4G/LTE

4.2.2.5G

4.2.3.3G

5.

Global Connected Car Market

Estimates & Forecast Trend Analysis, by Connectivity Solutions

5.1. Global Connected Car Market

Assessments & Key Findings, by Connectivity Solutions

5.2. Global Connected Car Market

Revenue (US$ Million) Estimates and Forecasts, by Connectivity Solutions, 2021

- 2034

5.2.1.Integrated

5.2.2.Embedded

5.2.3.Tethered

6.

Global Connected Car Market

Estimates & Forecast Trend Analysis, by Service

6.1. Global Connected Car Market

Assessments & Key Findings, by Service

6.2. Global Connected Car Market

Revenue (US$ Million) Estimates and Forecasts, by Service, 2021 - 2034

6.2.1.Driver assistance

6.2.2.Safety

6.2.3.Entertainment

6.2.4.Well-being

6.2.5.Vehicle management

6.2.6.Mobility management

7.

Global Connected Car Market

Estimates & Forecast Trend Analysis, by Sales Channel

7.1. Global Connected Car Market

Assessments & Key Findings, by Sales Channel

7.2. Global Connected Car Market

Revenue (US$ Million) Estimates and Forecasts, by Sales Channel, 2021 - 2034

7.2.1.OEM

7.2.2.Aftermarket

8.

Global Connected Car Market

Estimates & Forecast Trend Analysis, by Region

8.1. Global Connected Car Market

Assessments & Key Findings, by Region

8.2. Global Connected Car Market

Revenue (US$ Million) Estimates and Forecasts, by Region, 2021 - 2034

8.2.1.North America

8.2.2.Europe

8.2.3.Asia Pacific

8.2.4.Middle East & Africa

8.2.5.Latin America

9.

North

America Connected Car Market: Estimates & Forecast Trend Analysis

9.1.

North

America Connected Car Market Assessments & Key Findings

9.1.1.North America Connected Car

Market Introduction

9.1.2.North America Connected Car

Market Size Estimates and Forecast (US$ Million) (2021 - 2034)

9.1.2.1. By Technology

9.1.2.2. By Connectivity Solutions

9.1.2.3. By Service

9.1.2.4. By Sales Channel

9.1.2.5. By Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Connected

Car Market: Estimates & Forecast

Trend Analysis

10.1. Europe Connected Car Market

Assessments & Key Findings

10.1.1. Europe Connected Car Market

Introduction

10.1.2. Europe Connected Car Market Size

Estimates and Forecast (US$ Million) (2021 - 2034)

10.1.2.1. By Technology

10.1.2.2. By Connectivity Solutions

10.1.2.3. By Service

10.1.2.4. By Sales Channel

10.1.2.5. By Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7. Rest

of Europe

11. Asia Pacific Connected

Car Market: Estimates & Forecast

Trend Analysis

11.1. Asia Pacific Market Assessments

& Key Findings

11.1.1. Asia Pacific Connected Car

Market Introduction

11.1.2. Asia Pacific Connected Car

Market Size Estimates and Forecast (US$ Million) (2021 - 2034)

11.1.2.1. By Technology

11.1.2.2. By Connectivity Solutions

11.1.2.3. By Service

11.1.2.4. By Sales Channel

11.1.2.5. By Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Connected

Car Market: Estimates & Forecast

Trend Analysis

12.1. Middle East & Africa Market

Assessments & Key Findings

12.1.1. Middle

East & Africa Connected

Car Market Introduction

12.1.2. Middle

East & Africa Connected

Car Market Size Estimates and Forecast (US$ Million) (2021 - 2034)

12.1.2.1. By Technology

12.1.2.2. By Connectivity Solutions

12.1.2.3. By Service

12.1.2.4. By Sales Channel

12.1.2.5. By Country

12.1.2.5.1. South Africa

12.1.2.5.2. UAE

12.1.2.5.3. Saudi Arabia

12.1.2.5.4. Rest of MEA

13. Latin America

Connected Car Market: Estimates &

Forecast Trend Analysis

13.1. Latin America Market Assessments

& Key Findings

13.1.1. Latin America Connected Car

Market Introduction

13.1.2. Latin America Connected Car

Market Size Estimates and Forecast (US$ Million) (2021 - 2034)

13.1.2.1. By Technology

13.1.2.2. By Connectivity Solutions

13.1.2.3. By Service

13.1.2.4. By Sales Channel

13.1.2.5. By Country

13.1.2.5.1. Brazil

13.1.2.5.2. Mexico

13.1.2.5.3. Argentina

13.1.2.5.4. Rest of LATAM

14. Competition Landscape

14.1. Global Connected Car Market Technology

Mapping

14.2. Global Connected Car Market

Concentration Analysis, by Leading Players / Innovators / Emerging Players /

New Entrants

14.3. Global Connected Car Market Tier

Structure Analysis

14.4. Global Connected Car Market

Concentration & Company Market Shares (%) Analysis, 2025

15. Company Profiles

15.1. General Motors Company

15.1.1. Company Overview & Key Stats

15.1.2. Financial Performance & KPIs

15.1.3. Product Portfolio

15.1.4. SWOT Analysis

15.1.5. Business Strategy & Recent Developments

* Similar details would be provided for all

the players mentioned below

15.2. Ford Motor Company

15.3. BMW AG

15.4. Mercedes-Benz Group AG

15.5. Toyota Motor Corporation

15.6. Volkswagen AG

15.7. Audi AG

15.8. Tesla, Inc.

15.9. Nissan Motor Corporation

15.10. Hyundai Motor Company

15.11. Robert Bosch GmbH

15.12. Continental AG

15.13. Qualcomm Technologies, Inc.

15.14. Harman International

15.15. Visteon Corporation

15.16. NXP Semiconductors N.V.

15.17. DENSO Corporation

15.18. AT&T Inc.

15.19. Verizon Communications Inc.

15.20. Other Prominent

Players

16. Research

Findings & Conclusion

17. Assumption & Acronyms Used

18. Research

Methodology

18.1. External Transportations /

Databases

18.2. Internal Proprietary Database

18.3. Primary Research

18.4. Secondary Research

18.5. Assumptions

18.6. Limitations

18.7. Report FAQs

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables