Connected Mining Market Size and Forecast (2026–2034), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Component (Solutions, Services); By Technology (Internet of Things (IoT), Artificial Intelligence & Analytics, Automation Systems, Cloud Computing, Cybersecurity Solutions, Others); By Application (Fleet Management, Predictive Maintenance, Remote Operations, Worker Safety & Monitoring, Asset Tracking, Production Optimization, Others); By End User (Coal Mining, Metal Mining, Mineral Mining, Others), and Geography

2026-05-27

ICT

Ekta Chaurasia (Team Lead)

Description

Connected Mining Market Overview

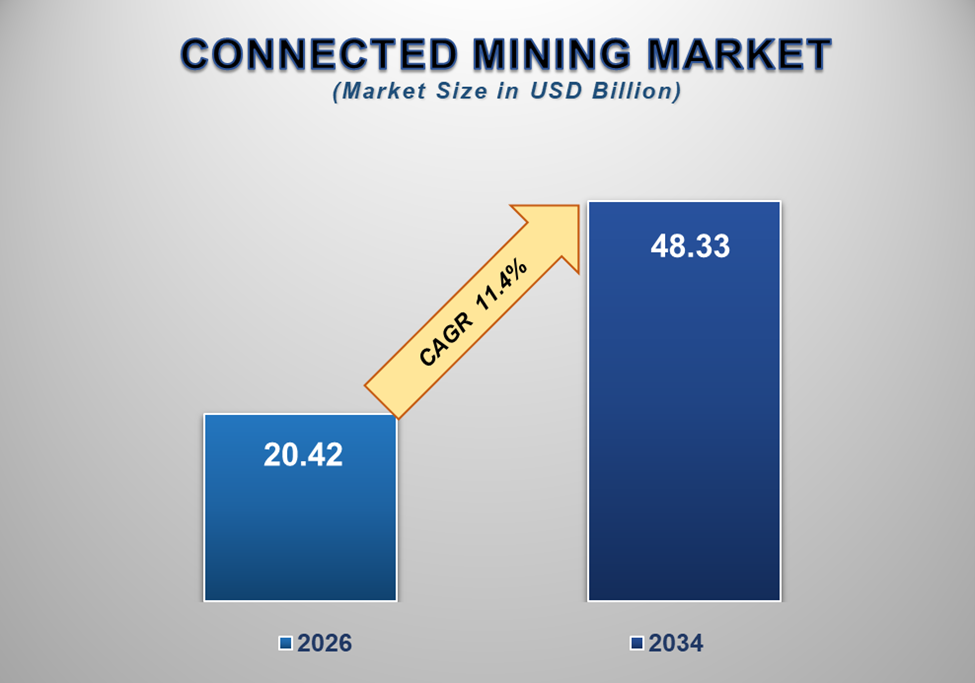

The global Connected

Mining market was valued at USD 20.42 billion in 2026 and is

projected to reach USD 48.33 billion by 2034, expanding at a CAGR of 11.4%

during the forecast period. The market is experiencing strong growth due to

increasing adoption of digital mining technologies, rising demand for

operational efficiency, growing focus on worker safety, and expanding

integration of IoT-enabled monitoring systems across mining operations

worldwide.

Connected mining

refers to the integration of advanced digital technologies, automation systems,

data analytics, cloud platforms, and IoT-enabled communication networks within

mining operations to improve productivity, operational visibility, safety, and

resource management. It enables real-time connectivity between mining

equipment, workers, control centers, and production systems through intelligent

digital ecosystems.

Mining companies

are increasingly transforming traditional mining operations into highly

automated and data-driven environments to improve efficiency and reduce

operational costs. Connected mining solutions provide centralized monitoring

capabilities, predictive analytics, remote asset management, and intelligent

automation that enhance overall mine productivity.

The growing

complexity of mining activities, combined with rising global demand for

minerals, metals, and energy resources, is significantly driving the adoption

of connected mining technologies. Mining operators are under increasing

pressure to maximize production output while ensuring worker safety,

environmental sustainability, and regulatory compliance.

Advanced

technologies such as artificial intelligence, machine learning, autonomous

vehicles, digital twins, edge computing, and industrial IoT are revolutionizing

modern mining operations. These technologies enable real-time data collection,

predictive maintenance, automated drilling, remote operations, and optimized

fleet management.

Additionally,

mining companies are increasingly investing in smart mining infrastructure to

reduce equipment downtime, improve fuel efficiency, optimize ore extraction

processes, and minimize workplace accidents. The integration of connected

systems also supports sustainability initiatives through energy optimization

and emissions monitoring.

As the mining

industry continues its digital transformation journey, the connected mining

market is expected to witness substantial growth through 2034.

Connected Mining Market Drivers and OpportunitiesRising Adoption of Automation and Smart Mining Technologies Is Driving Market Growth

The increasing

adoption of automation technologies across mining operations is one of the

primary drivers of the connected mining market. Mining companies are rapidly

deploying intelligent automation systems to improve productivity, minimize

manual intervention, and optimize operational performance.

Autonomous haul

trucks, robotic drilling systems, automated conveyor systems, and remotely

operated machinery are becoming increasingly common in modern mining

environments. These technologies help improve operational precision while

reducing labor-intensive activities and safety risks.

Connected mining

solutions provide centralized control and real-time monitoring capabilities

that allow operators to manage multiple mining assets simultaneously. Real-time

communication between equipment, sensors, and control centers improves

decision-making and operational efficiency.

Furthermore, increasing labor shortages and rising operational costs within the mining sector are encouraging companies to adopt automated and connected technologies to maintain profitability and long-term sustainability.

Growing Focus

on Worker Safety and Predictive Maintenance Is Fueling Market Expansion

Worker safety

remains a major concern within the mining industry due to the hazardous nature

of underground and open-pit mining operations. Connected mining technologies

significantly enhance workplace safety through continuous monitoring,

predictive analytics, and automated alert systems.

IoT-enabled

wearable devices, environmental sensors, and real-time communication platforms

help monitor worker health, equipment conditions, gas levels, temperature

fluctuations, and hazardous operational zones. These systems enable faster

emergency response and reduce accident risks.

Predictive

maintenance is another key growth driver for the connected mining market.

Mining equipment operates under extreme environmental conditions, making

machinery failures highly costly and operationally disruptive. Connected

sensors and AI-powered analytics platforms enable mining companies to monitor

equipment performance continuously and identify potential failures before

breakdowns occur.

This predictive approach helps reduce unplanned downtime, lower maintenance costs, extend equipment lifespan, and improve overall operational reliability.

Expansion of

Remote Operations and Digital Twin Technologies Presents Significant

Opportunities

The growing

adoption of remote mining operations presents substantial opportunities for the

connected mining market. Mining companies are increasingly utilizing

centralized remote operation centers to monitor and manage geographically

dispersed mining sites from a single location.

Remote

operations improve operational efficiency, reduce workforce exposure to

hazardous environments, and support better resource allocation. High-speed

communication networks, cloud computing, and edge processing technologies are

enabling seamless connectivity between mining sites and centralized control

centers.

Digital twin

technology is also emerging as a transformative opportunity within the

connected mining industry. Digital twins create virtual replicas of mining

operations, equipment, and production systems, allowing operators to simulate

processes, optimize workflows, and improve decision-making capabilities.

Additionally,

increasing investments in sustainable mining practices and environmental

monitoring are creating further opportunities for connected mining solutions.

Mining companies are increasingly utilizing digital technologies to monitor

emissions, optimize water usage, improve energy efficiency, and support

regulatory compliance initiatives.

As mining companies continue prioritizing digital transformation and operational modernization, the demand for connected mining technologies is expected to rise significantly.

Connected

Mining Market Scope

|

Report

Attributes |

Description |

|

Market Size

in 2026 |

USD

20.42 Billion |

|

Market

Forecast in 2034 |

USD 48.33 Billion |

|

CAGR %

2026-2034 |

11..4% |

|

Base Year |

2025 |

|

Historic

Data |

2021-2025 |

|

Forecast

Period |

2026-2034 |

|

Report USP |

Production,

Consumption, Company Share, Company Heatmap, Company Production, Service

Type, Growth Factors and more |

|

Segments

Covered |

∙ By Component |

|

Regional

Scope |

● North America |

|

Country

Scope |

U.S. |

Connected

Mining Market Report Segmentation Analysis

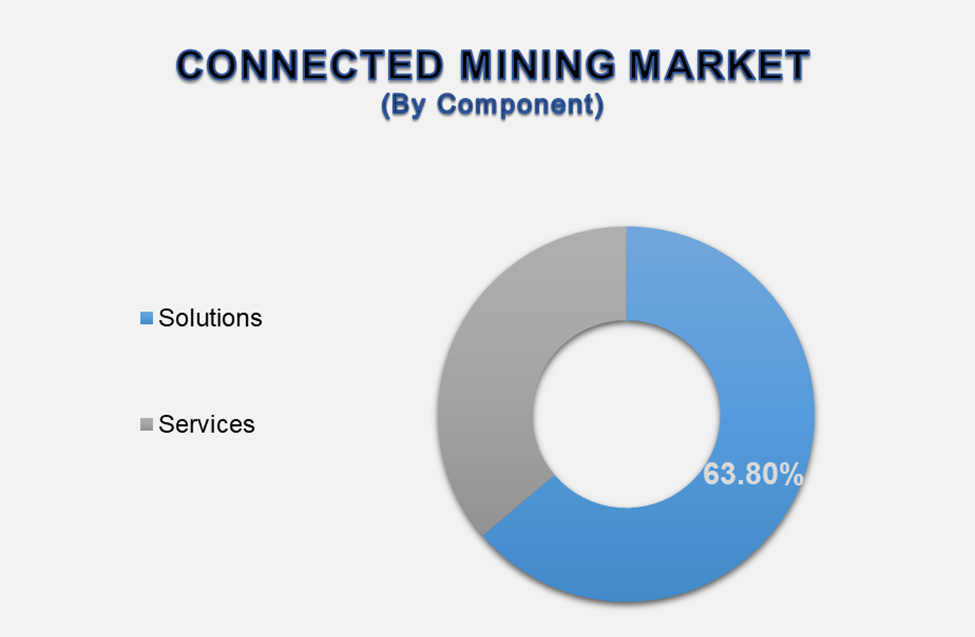

The global connected mining market industry analysis is segmented by component, by technology, by application, by end user, and by region.

Solutions

Segment Is Expected to Dominate the Market During the Forecast Period

The solutions

segment accounted for approximately 63.8% of the global market, making

it the dominant component category.

Connected mining

solutions include fleet management systems, predictive maintenance platforms,

industrial IoT systems, remote monitoring software, production optimization

tools, and advanced analytics platforms.

Mining companies

are increasingly investing in integrated digital platforms capable of providing

real-time operational visibility and intelligent automation capabilities. These

solutions help optimize mine productivity, improve resource allocation, and reduce

operational risks.

The increasing demand for data-driven decision-making and operational efficiency is significantly contributing to segment growth.

Internet of

Things (IoT) Segment Is Expected to Lead the Market by Technology

The IoT segment

dominates the market due to its critical role in enabling real-time

connectivity and communication across mining operations.

IoT-enabled

sensors and monitoring devices are widely utilized to collect operational data

related to equipment performance, environmental conditions, worker safety, fuel

consumption, and production activities.

These connected systems provide mining operators with actionable insights that improve productivity, predictive maintenance, and operational safety. The rapid expansion of industrial IoT ecosystems and wireless communication infrastructure is further supporting segment growth.

Fleet

Management Segment Is Expected to Dominate the Market by Application

Fleet management

represents the leading application segment within the connected mining market

due to the extensive use of heavy machinery and transportation equipment in

mining operations.

Connected fleet

management systems enable mining companies to monitor vehicle performance, fuel

usage, driver behavior, route optimization, and maintenance schedules in real

time.

These systems help improve equipment utilization, reduce fuel consumption, minimize downtime, and enhance overall operational efficiency. The increasing deployment of autonomous and semi-autonomous mining vehicles is also contributing significantly to segment expansion.

Metal Mining

Segment Is Expected to Dominate the End-User Market

The metal mining

segment accounts for the largest market share due to rising global demand for

industrial metals such as copper, iron ore, nickel, lithium, and rare earth

elements.

Metal mining

operations are increasingly adopting connected technologies to improve ore

extraction efficiency, optimize production planning, and manage complex,

large-scale operations more effectively.

The growing demand for critical minerals used in electric vehicles, renewable energy systems, and advanced electronics is further accelerating digital transformation within metal mining operations.

The following

segments are part of an in-depth analysis of the global Connected Mining

market:

|

Market Segments |

|

|

By

Component |

∙ Solutions |

|

By Technology |

∙

Internet of Things (IoT) |

|

By

Application |

∙

Fleet Management |

|

By

End User |

∙

Coal Mining |

Connected

Mining Market Share Analysis by Region

North America is

projected to hold the largest share of the global connected mining market over

the forecast period.

North America

accounted for approximately 36.9% of the global market in 2026, driven

by strong adoption of mining automation technologies, advanced industrial

infrastructure, and increasing investments in smart mining initiatives.

The United

States and Canada are major contributors due to the presence of technologically

advanced mining companies and the increasing deployment of autonomous mining

equipment and IoT-enabled operational systems.

Asia Pacific is

expected to register the highest CAGR during the forecast period due to rapid

industrialization, growing mining activities, increasing demand for critical

minerals, and rising investments in mining modernization programs.

Countries such

as China, India, and Australia are significantly expanding smart mining

infrastructure and digital transformation initiatives to improve operational

efficiency and resource management.

Latin America

and the Middle East & Africa are also witnessing increasing adoption of

connected mining technologies due to large-scale mineral extraction projects

and rising foreign investments in mining operations.

Connected

Mining Market Competition Landscape Analysis

The connected

mining market is highly competitive and technology-intensive, with leading

companies focusing on industrial automation, AI-driven analytics, cloud-based

mining platforms, and advanced IoT integration solutions.

Companies are

increasingly investing in research and development activities aimed at

improving autonomous mining capabilities, operational intelligence,

cybersecurity protection, and predictive maintenance technologies.

Strategic

collaborations between mining operators, technology providers,

telecommunications companies, and industrial automation firms are becoming

increasingly common as organizations seek to develop fully integrated smart

mining ecosystems.

Global

Connected Mining Market Recent Developments News:

In March 2026 – Mining companies

accelerated the deployment of AI-powered predictive maintenance systems for

heavy equipment monitoring.

In January 2026 – Autonomous haul trucks and connected fleet management systems

witnessed increased adoption across large mining sites.

In October 2025 – Industrial IoT sensor networks expanded significantly within

underground mining operations for safety monitoring.

In August 2025 – Mining operators invested heavily in remote operation centers

and cloud-based production management platforms.

In June 2025 – Advanced digital twin technologies were introduced to optimize

mine planning and operational simulation capabilities.

The Global

Connected Mining Market is dominated by a few large companies, such as

∙ Caterpillar Inc.

∙ Komatsu Ltd.

∙ Hitachi Construction Machinery Co., Ltd.

∙ Sandvik AB

∙ Hexagon AB

∙ ABB Ltd.

∙ Cisco Systems, Inc.

∙ SAP SE

∙ IBM Corporation

∙ Rockwell Automation, Inc.

∙ Siemens AG

∙ Trimble Inc.

∙ Epiroc AB

∙ Wenco International Mining Systems Ltd.

∙ Schneider Electric SE

∙ Nokia Corporation

∙ Ericsson AB

∙ Accenture plc

∙ Others

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1.

Global Connected Mining

Market Introduction and Market Overview

1.1. Objectives of the Study

1.2. Global Connected Mining Market Scope and Market Estimation

1.2.1.

Global Connected Mining Market

Size (US$ Million), Market CAGR (%), Market Forecast (2026 - 2034)

1.2.2.

Global Connected Mining Market

Revenue Share (%) and Growth Rate (Y-o-Y), 2021 - 2034

1.3. Market Segmentation

1.3.1.

Component of Global Connected

Mining Market

1.3.2.

Technology of Global Connected

Mining Market

1.3.3.

Application of Global Connected

Mining Market

1.3.4.

End User of Global Connected

Mining Market

1.3.5.

Region of Global Connected

Mining Market

1.4. Competition Coverage List of Market Participants

1.5. Market Definition

2.

Executive Summary

2.1. Global Connected Mining Market Snapshot

2.1.1.

Global Connected Mining Market

Size Estimation, 2021 - 2034

2.1.2.

Global Connected Mining Market

CAGR Analysis, 2026 - 2034

2.2. Global Connected Mining Market Revenue Share Analysis

2.3. Global Connected Mining Market Trends Analysis

2.4. REGIONAL OUTLOOK

2.5. Competitive Insights

3.

Global Connected Mining

Market Dynamics

3.1. Global Connected Mining Market Drivers

3.1.1.

Rising Adoption of Automation

and Smart Mining Technologies

3.1.2.

Increasing Focus on Operational

Efficiency and Productivity

3.1.3.

Growing Demand for Worker

Safety and Remote Monitoring Solutions

3.2. Global Connected Mining Market Restraints

3.2.1.

High Initial Investment and

Infrastructure Costs

3.2.2.

Cybersecurity Risks and Data

Privacy Concerns

3.3. Global Connected Mining Market Opportunities

3.3.1.

Expansion of Digital Twin and

Predictive Maintenance Technologies

3.3.2.

Growing Adoption of AI and

IoT-Based Mining Operations

3.4. Global Connected Mining Market Challenges

3.5. Porter’s Five Forces Analysis

3.6. PESTEL Analysis

3.7. Value Chain Analysis

3.8. Technology Landscape

3.9. Regulatory Framework

3.10.

COVID-19 Impact Analysis

4.

Global Connected Mining

Market Size Analysis and Forecast, by Component

4.1. Market Overview

4.2. Solutions

4.3. Services

5.

Global Connected Mining

Market Size Analysis and Forecast, by Technology

5.1. Market Overview

5.2. Internet of Things (IoT)

5.3. Artificial Intelligence & Analytics

5.4. Automation Systems

5.5. Cloud Computing

5.6. Cybersecurity Solutions

5.7. Others

6.

Global Connected Mining

Market Size Analysis and Forecast, by Application

6.1. Market Overview

6.2. Fleet Management

6.3. Predictive Maintenance

6.4. Remote Operations

6.5. Worker Safety & Monitoring

6.6. Asset Tracking

6.7. Production Optimization

6.8. Others

7.

Global Connected Mining

Market Size Analysis and Forecast, by End User

7.1. Market Overview

7.2. Coal Mining

7.3. Metal Mining

7.4. Mineral Mining

7.5. Others

8.

Global Connected Mining

Market Size Analysis and Forecast, by Region

8.1. North America

8.2. Europe

8.3. Asia Pacific

8.4. Latin America

8.5. Middle East & Africa

9.

North America Connected

Mining Market Size Analysis and Forecast

9.1. Market Overview

9.2. North America Connected Mining Market Size and Forecast, 2021 - 2034

9.2.1.

By Component

9.2.2.

By Technology

9.2.3.

By Application

9.2.4.

By End User

9.2.5.

By Country

9.2.5.1.

U.S.

9.2.5.2.

Canada

10. Europe Connected Mining Market Size Analysis and Forecast

10.1.

Market Overview

10.2.

Europe Connected Mining Market

Size and Forecast, 2021 - 2034

10.2.1.

By Component

10.2.2.

By Technology

10.2.3.

By Application

10.2.4.

By End User

10.2.5.

By Country

10.2.5.1.

Germany

10.2.5.2.

U.K.

10.2.5.3.

France

10.2.5.4.

Italy

10.2.5.5.

Spain

10.2.5.6.

Switzerland

10.2.5.7.

Rest of Europe

11. Asia Pacific Connected Mining Market Size Analysis and Forecast

11.1.

Market Overview

11.2.

Asia Pacific Connected Mining

Market Size and Forecast, 2021 - 2034

11.2.1.

By Component

11.2.2.

By Technology

11.2.3.

By Application

11.2.4.

By End User

11.2.5.

By Country

11.2.5.1.

China

11.2.5.2.

India

11.2.5.3.

Japan

11.2.5.4.

South Korea

11.2.5.5.

Australia

11.2.5.6.

Rest of Asia Pacific

12. Latin America Connected Mining Market Size Analysis and Forecast

12.1.

Market Overview

12.2.

Latin America Connected Mining

Market Size and Forecast, 2021 - 2034

12.2.1.

By Component

12.2.2.

By Technlogy

12.2.3.

By Application

12.2.4.

By End Use

12.2.5.

By Country

12.2.5.1.

Brazil

12.2.5.2.

Mexico

12.2.5.3.

Argentina

12.2.5.4.

Rest of Latin America

13. Middle East & Africa Connected Mining Market Size Analysis and

Forecast

13.1.

Market Overview

13.2.

Middle East & Africa

Connected Mining Market Size and Forecast, 2021 - 2034

13.2.1.

By Component

13.2.2.

By Technology

13.2.3.

By Application

13.2.4.

By End User

13.2.5.

By Country

13.2.5.1.

Saudi Arabia

13.2.5.2.

UAE

13.2.5.3.

South Africa

13.2.5.4.

Rest of Middle East &

Africa

14. Competition Landscape

14.1.

Market Share Analysis of Key

Players

14.2.

Competitive Benchmarking

14.3.

Product and Service Portfolio

Analysis

14.4.

Strategic Initiatives

14.5.

Mergers and Acquisitions

14.6.

Partnerships and Collaborations

15. Company Profiles

15.1.

Caterpillar Inc.

15.1.1.

Company Overview

15.1.2.

Financial Overview

15.1.3.

Product Portfolio

15.1.4.

Recent Developments

15.1.5.

Business Strategy

15.2.

Komatsu Ltd.

15.3.

Hitachi Construction Machinery

Co., Ltd.

15.4.

Sandvik AB

15.5.

Hexagon AB

15.6.

ABB Ltd.

15.7.

Cisco Systems, Inc.

15.8.

SAP SE

15.9.

IBM Corporation

15.10.

Rockwell Automation, Inc.

15.11.

Siemens AG

15.12.

Trimble Inc.

15.13.

Epiroc AB

15.14.

Wenco International Mining

Systems Ltd.

15.15.

Schneider Electric SE

15.16.

Nokia Corporation

15.17.

Ericsson AB

15.18.

Accenture plc

15.19.

Others

16. Research Findings and Conclusion

17. Assumptions and Acronyms Used

18. Research Methodology

18.1.

Primary Research

18.2.

Secondary Research

18.3.

Market Size Estimation

18.4.

Forecasting Methodology

18.5.

Data Triangulation

18.6.

Research Assumptions

18.7.

Limitations

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables