Crop Insurance Market Size and Forecast (2025–2033), Global and Regional Analysis, Share, Trends, and Industry Outlook, By Type (Multi-peril Crop Insurance (MPCI), Crop-hail Insurance, Revenue Insurance), By Coverage (Yield Protection, Revenue Protection, Price Protection), By Distribution Channel (Government Agencies, Insurance Companies, Others), and Geography

2026-01-02

Agriculture Industry

Jaya Bundele (Research Analyst)

Description

Crop Insurance Market Overview

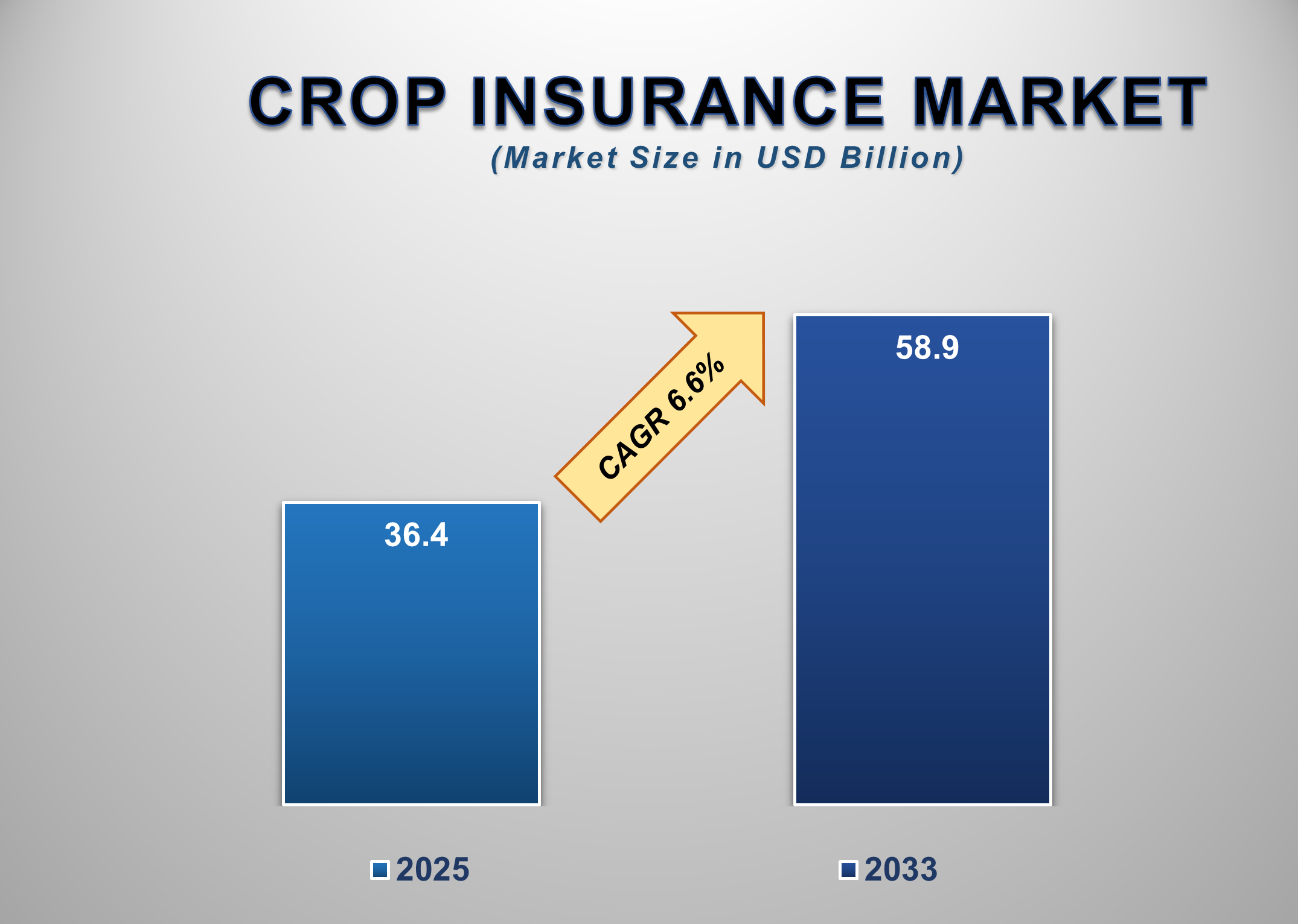

The Global Crop Insurance Market is experiencing steady expansion as nations strengthen agricultural resilience amid rising climate uncertainties, increased production risks, and the need for financial protection for farmers. Valued at USD 36.4 billion in 2025, the market is projected to reach USD 58.9 billion by 2033, reflecting a CAGR of 6.6%. Farmers worldwide face rising economic exposure due to unpredictable weather patterns, disease outbreaks, pest infestations, and volatile commodity prices. Crop insurance provides a crucial financial buffer that helps stabilize farmers’ incomes, reduces reliance on emergency government subsidies, and strengthens food security systems. The market has evolved from simple yield-based protection to sophisticated revenue and price protection products supported by advanced data analytics, remote sensing, and predictive risk modeling.

Government-led programs remain

fundamental to market expansion, particularly in developing economies where

subsidies and public-private partnerships (PPPs) make insurance more affordable

for smallholder farmers. Meanwhile, private insurers are advancing innovative

index-based insurance models and digital distribution platforms to expand

reach. Technological integration is growing rapidly, with satellite-based

monitoring, AI-driven risk scoring, and automated claims management enhancing

accuracy and operational efficiency. With climate risks intensifying globally,

the industry is expected to witness strong demand from both large commercial

farms and smallholders seeking stable risk mitigation solutions. Moreover,

digital transformation and expanded government funding will play a pivotal role

in accelerating global market penetration over the forecast period.

Crop Insurance Market

Drivers and Opportunities

Rising Climate Variability and Weather-related Losses Are

Driving the Crop Insurance Market Growth

Rising climate instability is one of the strongest forces

accelerating the demand for crop insurance globally. Farmers are increasingly

exposed to extreme weather events, including droughts, floods, heatwaves,

hailstorms, and unseasonal rainfall. These unpredictable changes are directly

impacting yields, lowering farm productivity, and threatening the stability of

agricultural supply chains. As climate change intensifies, crop losses have

become more frequent and severe, increasing the financial burden on farmers and

governments alike. Crop insurance provides essential risk transfer mechanisms

that help stabilize farm incomes and reduce reliance on emergency relief

programs. This is especially critical in emerging economies where agriculture

remains the backbone of rural livelihoods.

Furthermore, governments worldwide are strengthening subsidy

programs and expanding public-private partnerships to increase insurance

penetration among smallholders. These initiatives are supported by advancements

in remote sensing, precision agriculture, and climate modeling tools, which

allow insurers to assess risks more accurately and streamline claims

processing. Index-based insurance solutions triggered by satellite or weather

station data are also gaining traction, offering faster and more transparent

claim settlements. As farmers become increasingly aware of the financial risks

associated with climate unpredictability, demand for protection is rising. This

combination of climate-driven vulnerabilities and technological maturity is

expected to fuel sustained market growth throughout the forecast period.

Growing Adoption of Digital Agricultural Platforms and

InsurTech Innovations Is Supporting Market Expansion

Digitization is transforming the crop insurance industry, enabling

faster enrollment, customized policy design, and more accurate loss assessment.

The increasing adoption of digital agriculture tools such as mobile-based farm

management platforms, remote sensing technologies, and AI-driven analytics is

helping insurers create data-rich risk profiles. These tools enable

high-precision underwriting by analyzing soil data, crop health, vegetation

indices, and regional climate patterns. As a result, insurers can provide

tailored insurance products that better reflect the actual risk exposure of

individual farms. Digital payment systems and mobile wallets are further

promoting accessibility in rural areas, allowing farmers to purchase coverage

and receive claim payouts seamlessly.

InsurTech-driven innovations such as satellite-based crop

monitoring, automated yield forecasting, blockchain-enabled claim verification,

and drone-assisted field assessments are reshaping the value chain.

Weather-index and parametric insurance models supported by IoT sensors are

seeing widespread adoption due to their fast, transparent claim workflows.

Governments and private insurers are leveraging these technologies to reduce

fraud, minimize administrative costs, and expand coverage to remote regions where

traditional field-based assessments are challenging. As digital ecosystems

mature and smartphone penetration increases, the industry is witnessing

improved insurance literacy and stronger farmer engagement. This technological

acceleration is expected to solidify digital channels as a major growth

contributor for the global crop insurance market.

Growing Government Support and Subsidized Insurance Programs

Are Creating Significant Market Opportunities Worldwide

Governments worldwide are increasing their focus on agricultural

risk management, opening major growth opportunities for crop insurance

providers. Subsidized programs that lower premiums for farmers are expanding in

countries such as India, China, the U.S., and Brazil, helping improve

affordability and insurance penetration levels. Many nations are implementing

reforms to encourage private sector participation in public crop insurance

schemes, fostering competition and improving product innovation. Strengthened

public-private partnerships (PPPs) are emerging as a key opportunity area,

enabling insurers to scale operations while reducing fiscal burdens on

governments. Another promising opportunity lies in expanding insurance coverage

for high-value crops, horticulture crops, and specialty farming systems that

traditionally lacked structured risk protection. With increased investment in

agricultural modernization, agribusiness firms and cooperatives are adopting

group insurance models, opening new B2B revenue streams for insurers. Enhanced

adoption of climate-resilient seed varieties and precision farming practices is

also reshaping coverage needs, paving the way for dynamic and customized

insurance products. As governments continue to strengthen agricultural resilience

frameworks, insurers are positioned to leverage policy reforms, digital

schemes, and expanded subsidy networks. These developments are expected to

unlock strong market opportunities across Asia-Pacific, Latin America, and

Africa during the forecast period.

Crop Insurance Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 36.4 Billion |

|

Market Forecast in 2033 |

USD 58.9 Billion |

|

CAGR % 2025-2033 |

6.6% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Type, By

Coverage, By Distribution Channel |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Crop Insurance Market

Report Segmentation Analysis

The Global Crop Insurance Market

is segmented by Type, by Coverage, by Distribution Channel, and by Geography.

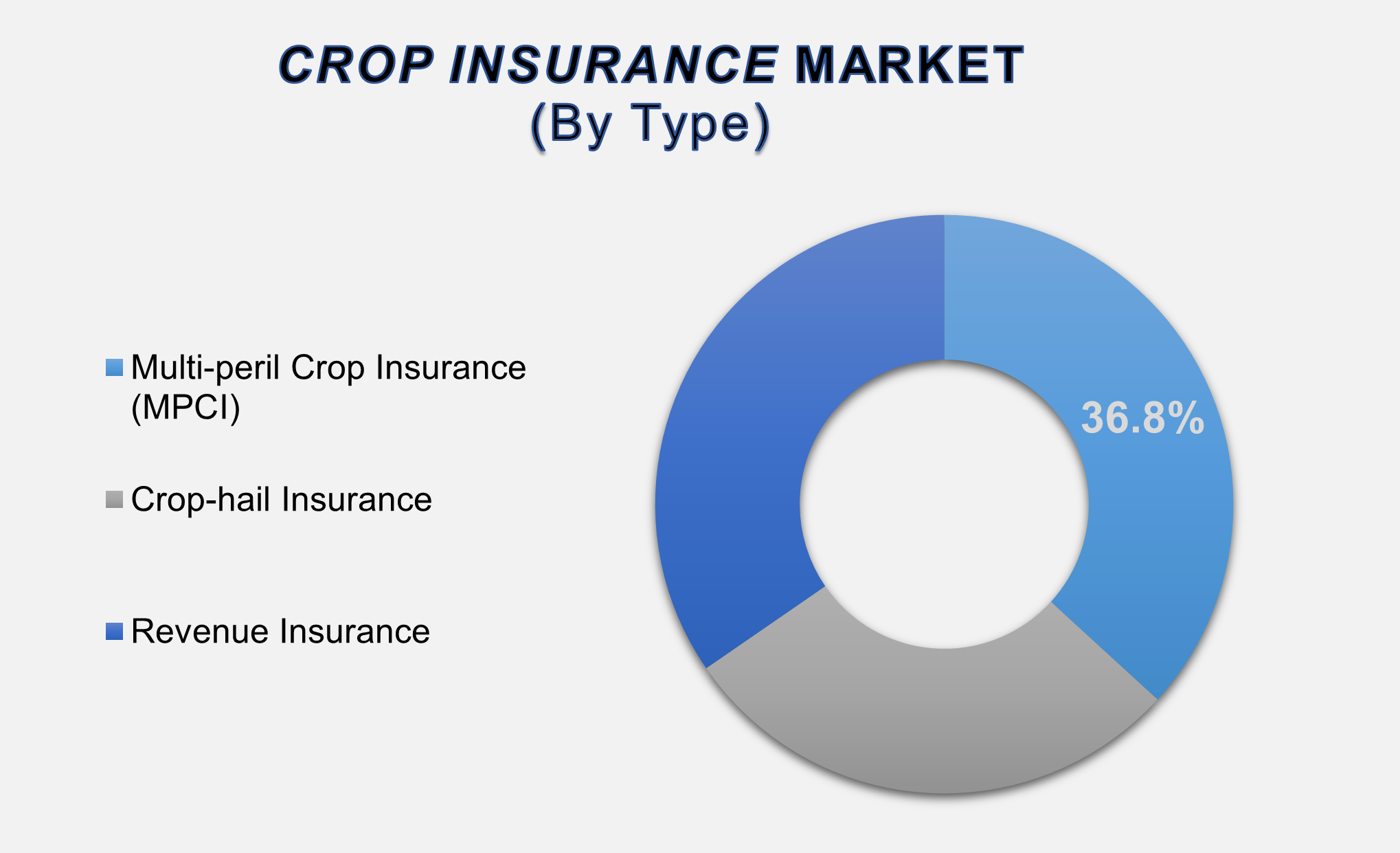

The Multi-peril Crop

Insurance (MPCI) Segment Accounted for the Largest Market Share in the Global

Crop Insurance Market

The

Multi-peril Crop Insurance (MPCI) segment accounted for the largest market

share in the global crop insurance market and continues to dominate due to its

extensive risk coverage and widespread adoption among farmers. This segment

offers comprehensive protection against multiple risks, including drought,

flood, pests, diseases, and adverse weather events, making it the most reliable

option for managing unpredictable farming conditions. MPCI policies are

particularly preferred in developing economies, where climatic variations and

yield uncertainties pose significant challenges for farmers. Governments in

countries such as India, China, and Brazil actively support MPCI through

subsidies and public-private partnerships, further strengthening its adoption.

The segment’s growth is also driven by digital innovations such as satellite-based monitoring, remote sensing, and automated claim settlement systems, which increase transparency and reduce administrative complexities. Insurers are enhancing MPCI offerings by integrating AI-based predictive models to assess yield and climate risks with greater accuracy. As climate volatility intensifies globally, MPCI is expected to remain the cornerstone of agricultural risk mitigation strategies, especially for staple crops such as wheat, rice, maize, and soybeans. The rising need for comprehensive coverage and government-backed affordability measures will ensure sustained dominance for MPCI throughout the forecast period.

Yield Protection Segment

Leads the Market Under the Coverage Category

The

Yield Protection segment accounted for the largest share within the coverage

category and continues to gain traction as farmers seek stable income security

amid rising yield variability. This segment protects growers against losses

stemming from lower-than-expected crop yields caused by adverse weather, pests,

and disease outbreaks. Yield Protection is particularly valued in regions where

agriculture is highly vulnerable to climatic fluctuations, including

Asia-Pacific, Africa, and Latin America. The segment’s popularity is reinforced

by government-led programs that make yield-based insurance policies affordable

and accessible through premium subsidies. Advancements in digital agriculture

are strengthening this coverage type, with satellite imaging, crop-health

monitoring, and vegetation index analytics significantly improving yield

estimation accuracy. These technologies enable insurers to assess risks more

effectively and expedite claims processing, enhancing overall service

reliability. Growth is further supported by increasing adoption of modern

farming techniques, precision agriculture, and standardized yield-data

collection practices, which contribute to better actuarial assessments. As

weather-related uncertainties continue to escalate, the Yield Protection

segment is expected to maintain its leading position, driven by rising farmer

awareness and investments in agricultural productivity enhancement tools.

Government Agencies

Segment Accounted for the Largest Share in the Global Crop Insurance Market

The

Government Agencies segment accounted for the largest share in the global crop

insurance market, supported by strong public-sector involvement in structuring,

funding, and distributing agricultural insurance programs. In most countries,

crop insurance is heavily subsidized to ensure that small and marginal farmers

can afford adequate protection. Government agencies play a pivotal role in

premium support, claim verification, policy administration, and partnership

formation with private insurers. Nations such as India, China, the U.S., and

several European countries operate extensive public crop insurance schemes

covering millions of farmers annually. This dominance is further reinforced by

the development of policies tailored specifically for local agricultural

conditions, supported by regulatory frameworks that mandate coverage for

vulnerable crops. The segment is also benefiting from digitization initiatives

within government programs, such as mobile-based enrollment, online claim

tracking, Aadhaar-linked farmer databases (in India), and remote sensing-based

assessments. By expanding subsidy frameworks, enhancing financial literacy, and

investing in digital agriculture infrastructure, governments are strengthening

risk management mechanisms across the farming ecosystem. Given the strategic

importance of food security and rural economic stability, government agencies

are expected to retain their leadership in the distribution of crop insurance

throughout the forecast period.

The following segments are

part of an in-depth analysis of the global Crop Insurance market:

|

Market Segments |

|

|

by Type |

●

Multi-peril Crop

Insurance (MPCI) ●

Crop-hail Insurance ●

Revenue Insurance |

|

by Coverage |

●

Yield Protection ●

Revenue Protection ●

Price Protection |

|

By

Distribution Channel |

●

Government Agencies ●

Insurance Companies ●

Others |

Crop Insurance Market

Share Analysis by Region

The Asia Pacific region

is projected to hold the largest share of the global Crop Insurance market over

the forecast period

Asia-Pacific

dominated the global crop insurance market with a 40.1% share in 2025, driven

by strong government-led programs, increasing farmer awareness, and rapidly

expanding adoption of risk mitigation solutions. Countries such as China and

India operate some of the world’s largest agricultural insurance schemes,

supported by extensive premium subsidies, digital enrollment systems, and

improved access to financial services. These programs offer large-scale

coverage for staple crops and high-value horticulture, enabling millions of

smallholder farmers to safeguard their livelihoods. Climate change, frequent

floods, droughts, and pest outbreaks further elevate demand for comprehensive

insurance solutions across the region.

North

America is projected to register the fastest CAGR during the forecast period

due to advanced risk modeling techniques, strong regulatory frameworks, and

high adoption of revenue-based insurance products. The United States, in

particular, exhibits a mature and technologically sophisticated crop insurance

market backed by robust federal support and sophisticated loss assessment

tools. Europe is also witnessing steady growth, driven by Common Agricultural

Policy (CAP) reforms, digital agriculture expansion, and rising climate-related

losses. Emerging markets in Latin America and Africa are increasingly adopting

index-based insurance models supported by government initiatives and

international development agencies. Overall, global crop insurance penetration

is accelerating as climate resilience becomes a central priority for

agricultural economies.

Crop Insurance Market

Competition Landscape Analysis

The Global Crop Insurance Market

is moderately consolidated, with a blend of government-backed institutions,

multinational insurance providers, and regional players actively participating

in policy distribution and risk underwriting. Leading companies focus on

developing innovative coverage models, digital claim settlement systems, and

satellite-driven monitoring solutions to enhance underwriting accuracy.

Strategic partnerships with government agencies, agritech startups, and

international development organizations are common, enabling insurers to expand

outreach to rural and underserved farming communities.

Global Crop Insurance

Market Recent Developments News:

- In

December 2024, the Agriculture Insurance Company of India

Limited (AIC) launched ‘Fal Suraksha Bima,’ a specialized insurance

product for banana and papaya crops. Announced during AIC’s 22nd

Foundation Day, the initiative offers tailored risk coverage to protect

farmers against losses from natural calamities and other unforeseen

events, reinforcing AIC’s focus on crop-specific agricultural resilience.

- In September 2024,

Alpha Omega secured a contract with the U.S. Department of Agriculture

(USDA) to modernize its crop insurance programs. The partnership will

leverage Alpha Omega’s expertise in AI, cybersecurity, and digital

transformation to enhance risk management systems and strengthen the

resilience of American agriculture against climate variability.

The Global Crop Insurance Market

Is Dominated by a Few Large Companies, such as

●

Kshema General

Insurance Limited

●

QBE Insurance Ltd.

●

Chubb

●

Zurich

●

Sompo

●

Great American

Insurance Company

●

American International

Group, Inc.

●

Agriculture Insurance

Company of India Limited

●

Tokio Marine HCC

●

FBL Financial Group,

Inc

●

Others

FAQs

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Crop Insurance

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Crop Insurance Market Scope and Market Estimation

1.2.1.Global Crop Insurance

Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Crop Insurance

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Type of Global Crop

Insurance Market

1.3.2.Coverage of Global Crop

Insurance Market

1.3.3.Distribution Channel of

Global Crop Insurance Market

1.3.4.Region of Global Crop

Insurance Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Crop Insurance Market

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

2.10.

Key

Regulation

3. Global

Crop Insurance Market Estimates

& Historical Trend Analysis (2020 - 2024)

4.

Global Crop Insurance

Market Estimates & Forecast Trend

Analysis, by Type

4.1.

Global

Crop Insurance Market Revenue (US$ Bn) Estimates and Forecasts, by Type, 2020 -

2033

4.1.1.Multi-peril Crop Insurance

(MPCI)

4.1.2.Crop-hail Insurance

4.1.3.Revenue Insurance

5.

Global Crop Insurance

Market Estimates & Forecast Trend

Analysis, by Coverage

5.1.

Global

Crop Insurance Market Revenue (US$ Bn) Estimates and Forecasts, by Coverage, 2020

- 2033

5.1.1.Yield Protection

5.1.2.Revenue Protection

5.1.3.Price Protection

6.

Global Crop Insurance

Market Estimates & Forecast Trend

Analysis, by Distribution Channel

6.1.

Global

Crop Insurance Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution

Channel, 2020 - 2033

6.1.1.Government Agencies

6.1.2.Insurance Companies

6.1.3.Others

7. Global

Crop Insurance Market Estimates

& Forecast Trend Analysis, by region

1.1.

Global

Crop Insurance Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020

- 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East & Africa

1.1.5.Latin America

8. North America Crop

Insurance Market: Estimates &

Forecast Trend Analysis

8.1.

North

America Crop Insurance Market Assessments & Key Findings

8.1.1.North America Crop

Insurance Market Introduction

8.1.2.North America Crop

Insurance Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Type

8.1.2.2. By Coverage

8.1.2.3. By Distribution

Channel

8.1.2.4.

By

Country

8.1.2.4.1.

The

U.S.

8.1.2.4.2.

Canada

9. Europe Crop

Insurance Market: Estimates &

Forecast Trend Analysis

9.1.

Europe

Crop Insurance Market Assessments & Key Findings

9.1.1.Europe Crop Insurance

Market Introduction

9.1.2.Europe Crop Insurance

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Type

9.1.2.2. By Coverage

9.1.2.3. By Distribution

Channel

9.1.2.4.

By

Country

9.1.2.4.1. Germany

9.1.2.4.2. Italy

9.1.2.4.3. U.K.

9.1.2.4.4. France

9.1.2.4.5. Spain

9.1.2.4.6. Switzerland

9.1.2.4.7.

Rest of Europe

10. Asia Pacific Crop

Insurance Market: Estimates &

Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Crop Insurance Market Introduction

10.1.2.

Asia

Pacific Crop Insurance Market Size Estimates and Forecast (US$ Billion) (2020 -

2033)

10.1.2.1. By Type

10.1.2.2. By Coverage

10.1.2.3. By Distribution

Channel

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6.

Rest

of Asia Pacific

11. Middle East & Africa Crop

Insurance Market: Estimates &

Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Crop Insurance Market Introduction

11.1.2.

Middle East & Africa Crop Insurance Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Type

11.1.2.2. By Coverage

11.1.2.3. By Distribution

Channel

11.1.2.4.

By

Country

11.1.2.4.1. South

Africa

11.1.2.4.2. UAE

11.1.2.4.3. Saudi

Arabia

11.1.2.4.4.

Rest of MEA

12. Latin America

Crop Insurance Market: Estimates &

Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Crop Insurance Market Introduction

12.1.2.

Latin

America Crop Insurance Market Size Estimates and Forecast (US$ Billion) (2020 -

2033)

12.1.2.1. By Type

12.1.2.2. By Coverage

12.1.2.3. By Distribution

Channel

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Mexico

12.1.2.4.3. Argentina

12.1.2.4.4.

Rest of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Crop Insurance Market Product Mapping

14.2.

Global

Crop Insurance Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3.

Global

Crop Insurance Market Tier Structure Analysis

14.4.

Global

Crop Insurance Market Concentration & Company Market Shares (%) Analysis,

2024

15.

Company

Profiles

15.1. Kshema

General Insurance Limited

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all

the players mentioned below

15.2. QBE Insurance

Ltd.

15.3. Chubb

15.4. Zurich

15.5. Sompo

15.6. Great

American Insurance Company

15.7. American

International Group, Inc.

15.8. Agriculture

Insurance Company of India Limited

15.9. Tokio Marine

HCC

15.10. FBL Financial

Group, Inc

15.11. Other

Prominent Players

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables