Crop Protection Chemicals Market Size And Forecast (2025 - 2033), Global And Regional Growth, Trend, Share And Industry Analysis Report Coverage: By Type (Herbicides, Insecticides, Fungicides, Others), By Crop (Grains & Cereals, Pulses & Oilseeds, Fruits & Vegetables, Others), By Source (Synthetic, Bio-Based) By Mode Of Application (Foliar, Seed Treatment, Soil Treatment) And Geography

2025-11-04

Agriculture Industry

Jaya Bundele (Research Analyst)

Description

Crop Protection Chemicals Market Overview

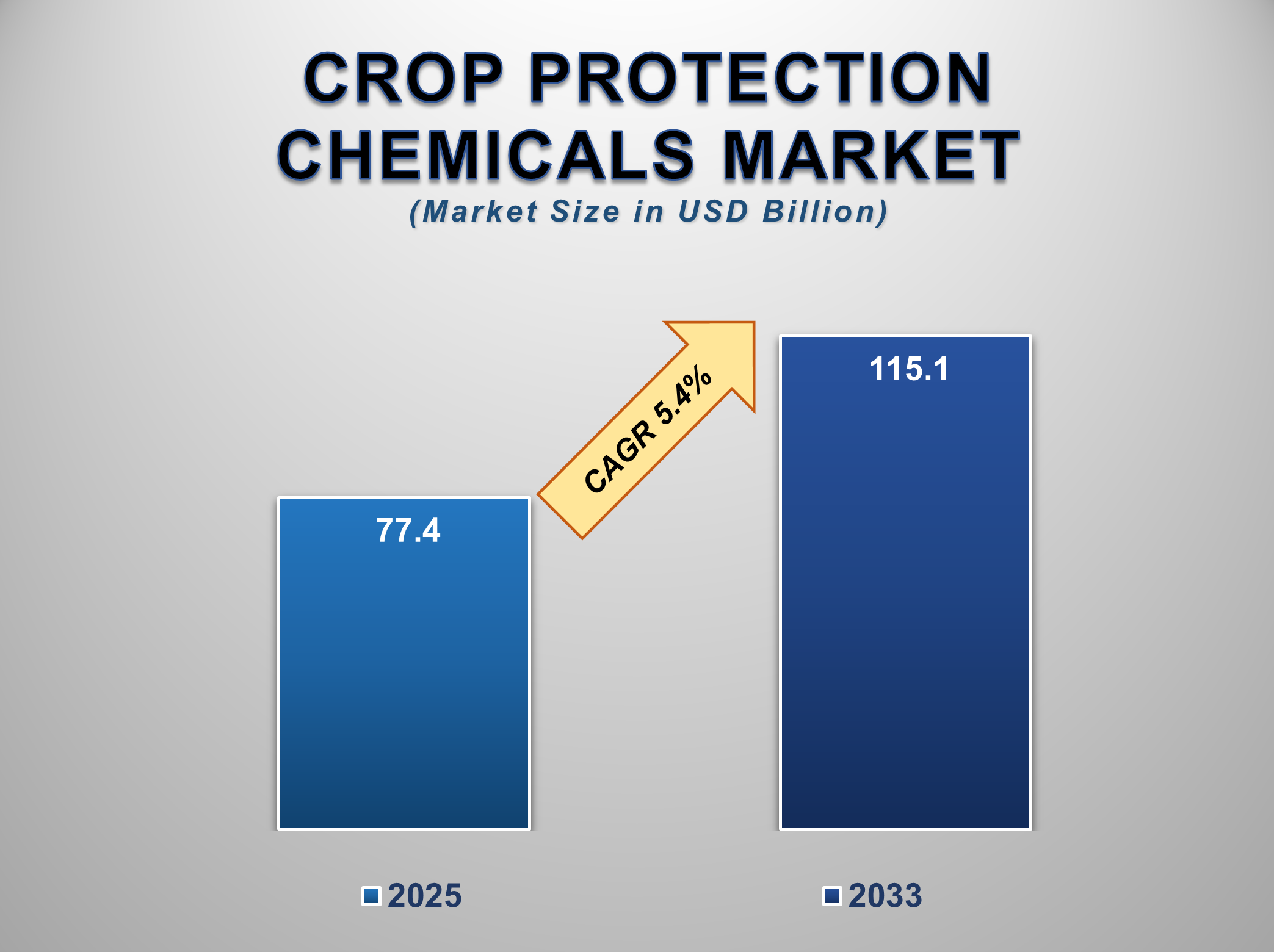

The Global Crop Protection Chemicals Market is projected to grow from USD 77.4 billion in 2025 to USD 115.1 billion by 2033, registering a CAGR of 5.4% during the forecast period. Market growth is driven by rising global food demand, increasing population, and the need to boost agricultural productivity through effective pest and disease control solutions.

Crop protection chemicals,

including herbicides, insecticides, fungicides, and biopesticides, play a vital

role in safeguarding crops from pests, weeds, and pathogens, thereby ensuring

better yield and quality. The ongoing shift toward sustainable and eco-friendly

farming practices is spurring demand for bio-based and low-toxicity products,

aligning with global sustainability goals. Furthermore, biotechnology

innovations and the development of novel active ingredients with higher

efficacy and lower environmental impact are fueling product advancements.

Government support through agricultural subsidies and productivity initiatives,

particularly in developing regions, is further stimulating adoption. However,

stringent environmental regulations and growing concerns over synthetic

pesticide residues are prompting manufacturers to invest heavily in R&D of

safer, more sustainable alternatives. With rising awareness of food security

and the increasing emphasis on green agriculture, the crop protection chemicals

market is set for steady, innovation-led growth globally.

Crop Protection Chemicals

Market Drivers and Opportunities

Technological Advancements in Chemical Formulations is

Anticipated to Lift the Crop Protection Chemicals Market During the Forecast

Period

The ongoing innovation in crop

protection chemical formulations is one of the critical factors driving growth

in the market. Agrochemicals traditionally exposed consumers and the

environment to risks, leading to regulatory pressure and consumer resistance.

Manufacturers have, in response, invested considerably in research and

development to design safer, more precise, and more benign formulations.

Advanced formulations involve microencapsulation technologies, slow-release

technologies, and nano-based pesticides that are aimed at boosting the activity

of active ingredients while minimizing their toxicity to non-target species.

Further, selective chemicals that target pests or pathogens but do not affect

beneficial insects or soil microbiota are in tune with sustainable agriculture.

Such advancements not only enhance efficacy but also decrease application

frequencies, lowering costs for producers. Besides, digital farming and

precision agriculture have complemented these new-generation chemicals to

enable site-specific application, further enhancing efficacy and minimizing

environmental impacts. Formulations with improved rainfastness, UV stability,

and longer residual activity are also growing in popularity, particularly in

areas with unstable weather patterns. Another significant development is the

introduction of both bio-based and naturally sourced pesticides, which are

finding increased application as single-point solutions or as mixtures with

traditional chemicals in integrated pest management systems. Such technological

advancements are particularly appealing in areas with strict regulations like

the EU, where environmental toxicity and chemical residue are of prime concern.

Overall, the revolution in crop protection chemistry is not only serving to

address older product concerns over safety and efficacy but is also growing the

market as it opens new opportunities for sustainability in pest and disease

control. This transformation, which is an ongoing trend, keeps the crop

protection chemicals business cutting-edge and futuristic.

Increasing Pest Resistance and Climate Change Impacts are

Vital Drivers for Influencing the Growth of the Global Crop Protection

Chemicals Market

The rising incidence of pest

resistance and the unpredictable impacts of climate change are heightening the

urgency for efficacious crop protection products, hence fueling demand.

Increased usage, over time, of certain chemical classes, like organophosphates

and pyrethroids, in repeated and uniform applications, has resulted in the

emergence of resistance among target pests. Pest populations with resistance

may cause catastrophic damage, prompting the need for farmers to switch to

newer, more effective formulations or integrated methods. Concurrently, climate

change is compounding these pressures through alterations in pest migration,

expansion of geographical host range, and multiplication of lifecycle frequency

with the increase in temperatures. Those regions that were earlier minimal

targets for certain insects or pathogens have now emerged as new hotspots, and,

in consequence, there is an increase in the usage of chemicals. Moreover,

irregular climatic occurrences like extended drought or high precipitation can

create conducive conditions enabling the increase of outbreaks of diseases and

proliferation of weeds, further prompting instances of chemical usage. Crop

protection chemicals, in these situations, act as an essential defense line to

stabilize crop production and ensure food availability. Firms are reacting to

these new pressures with novel active ingredients and resistance-breaking modes

of action to effectively manage shifting pest dynamics. In addition, government

policy and agri-extension departments are encouraging integrated pest

management methods where both chemical and non-chemical methods are utilized,

hence ensuring long-term sustainability. This coming together of ecological

pressure and technological response is not just fueling growth in the market

but also transforming product R&D pipelines throughout the agrochemical

space. With climate variability and pest resistance still unfolding, the need

for efficacious crop protection tools will further increase, cementing the

significance of this segment

Rise in Demand for Bio-Based and Eco-Friendly Products is

Poised to Create Significant Opportunities in the Global Crop Protection

Chemicals Market

The increasing worldwide

interest in sustainability and environmental stewardship is opening the door to

bio-based and green crop protection chemicals, which is a sizable opportunity

in the marketplace. Conventional synthetic chemicals, while effective, tend to

create concerns about toxicity, residues, and environmental degradation. As an

alternative, consumers, regulators, and interest groups are pressing for

greener, safer alternatives with a minimized ecological footprint but without

compromising crop protection. This has triggered significant investment in

biopesticides, which are extracted from natural sources such as plant

materials, beneficial microorganisms, and minerals. These solutions have

several benefits, among them reduced toxicity, biodegradability, and

compatibility with organic agriculture systems. Biopesticides also have fewer

chances of generating pest resistance, which is an increasing issue with

synthetic chemicals. With organic food demand growing worldwide and

certification standards tightening, farmers are turning to crop protection

products that are consistent with these marketplace expectations. Governments

in North America, the European Union, and other markets are also favoring the

introduction and use of bio-based products with regulatory fast-tracking,

research funding, and subsidies. The commercial acceptability of these green

products is increasing as progress in formulating technology increases shelf

life, stability, and performance under different environmental conditions.

Public-private investments, collaborations between agrochemical firms, and

biotech startups are also driving the pipeline of innovation in this space.

With sustainability becoming the cornerstone of agricultural policy and

consumer interest, demand for green crop protection products is likely to

surge, creating a large opportunity for firms with a willingness to commit to

green technology and marketplace education.

Crop Protection Chemicals Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 77.4 Billion |

|

Market Forecast in 2033 |

USD 115.1 Billion |

|

CAGR % 2025-2033 |

5.4% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, Company Share, Company Heatmap, Company

Production Capacity, Growth Factors, and more |

|

Segments Covered |

●

By Type ●

By Crop ●

By Source ●

By Mode of Application |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Russia 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19) South Africa |

Crop Protection Chemicals Market Report Segmentation Analysis

The Global Crop Protection

Chemicals Market industry analysis is segmented by Type, by Crop, by Source, by

Mode of Application, and by Region.

The Herbicides Segment Is Anticipated to Hold the Highest

Share of the Global Crop Protection Chemicals Market During the Projected

Timeframe

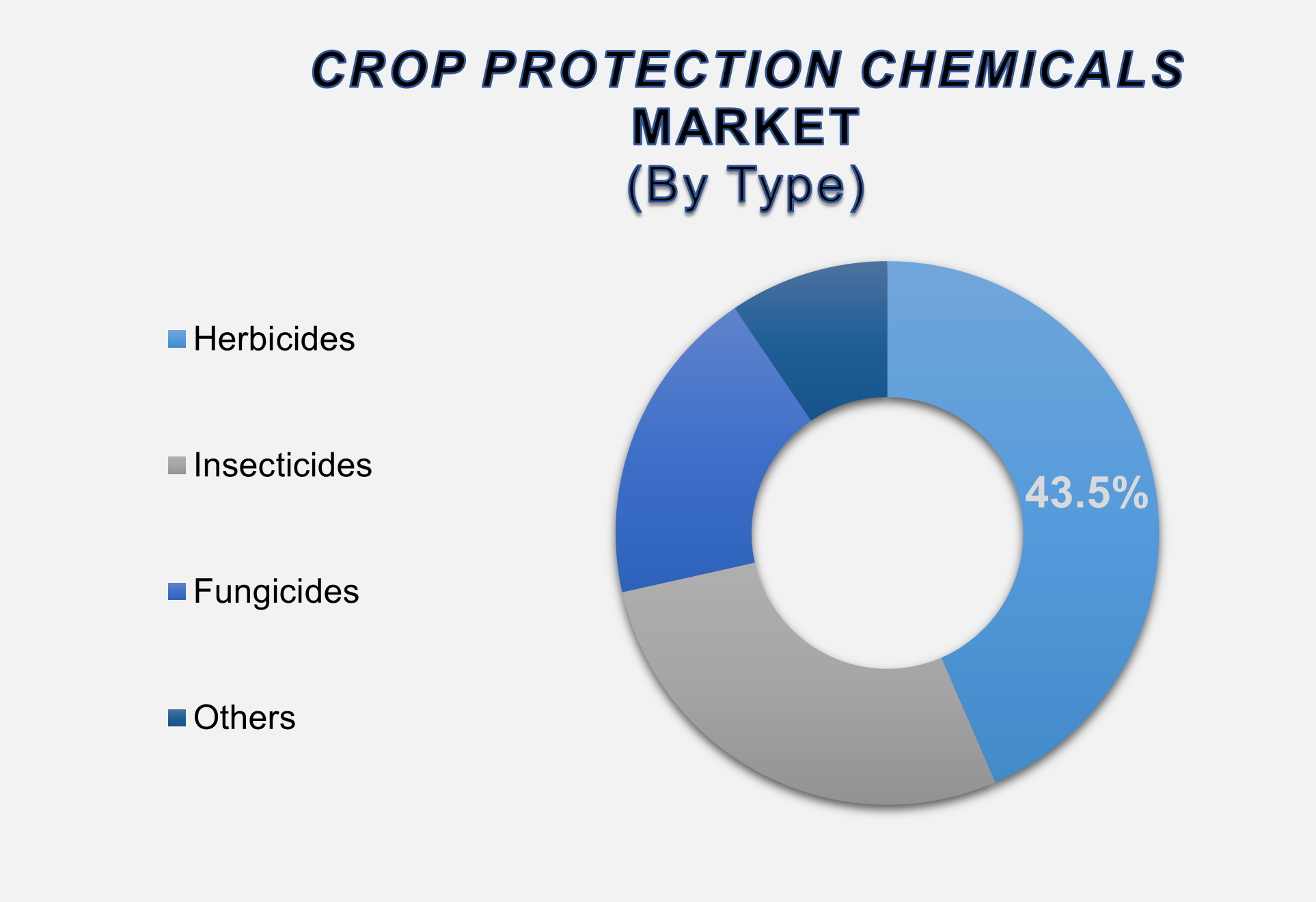

By Type, the market is categorized into Herbicides, Insecticides, Fungicides, and Others. Out of these, the herbicides segment is expected to have the largest share of 43.5% in the global crop protection chemicals market over the forecast period. Herbicides are commonly applied to suppress unwanted weeds and vegetation, which consume essential nutrients, water, and sunlight from crops. Their usage is high in the production of grains and cereals, where large-scale monocrop farming makes the crop vulnerable to weed invasion. The increasing demand for food grains globally, along with declining fallow land, is stimulating the usage of herbicides. The rising incidence of herbicide-resistant weed populations has increased demand for the new generation of herbicides, hence augmenting the growth of the segment.

The Grains & Cereals Segment Dominated the Market in 2024

And Is Predicted to Grow at The Highest CAGR Over the Forecast Period

By Crop, the market is segmented

into Grains & Cereals, Pulses & Oilseeds, Fruits & Vegetables, and

Others. In 2024, the grains & cereals segment led the market and is

expected to develop with the best CAGR throughout the forecast period. Wheat,

rice, and corn are common cereals and grains consumed all over the world and

form an important part of global agricultural production. With the increase in

demand due to population growth and food habits, these essential crops need to

be protected from pests, weeds, and diseases. Crop protection chemicals are

extensively applied in cereal farming to enhance yields and ensure food

security.

The Synthetic Segment Is Predicted to Grow at The Highest

CAGR Over the Forecast Period

By Source, the market is

bifurcated into Bio-based and Synthetic crop protection chemicals. The

synthetic segment is expected to register the highest growth at the highest

CAGR during the forecast period due to its established efficacy, broad-spectrum

activity, and extensive availability. The synthetic chemicals remain the

preferred option with farmers all over the world, predominantly in commercial

large-scale farming. These chemicals have predictable and consistent crop

protection efficacy against a broad spectrum of pests and pathogens. Despite

environmental concerns and regulatory issues hampering the use of synthetic

chemicals, technological advancements in formulation have resulted in the

introduction of safer and more targeted chemicals.

The Seed Treatment Segment Is Expected to Dominate the Market

During the Forecast Period

By Mode of Application, the

segment of the market is classified into Seed Treatment, Foliar, and Soil

Treatment. Seed Treatment is projected to lead the market through the forecast

period. Seed treatment encompasses the direct application of protective chemicals

to seeds prior to planting, which delivers early-season protection against

soil-borne fungal infections, pests, and diseases. This technique is finding

favor due to cost-effectiveness, targeted application, and environmental

benefits since it involves lesser volumes of chemicals compared to soil or

foliar treatments. Increasing demand for high-value seeds and ensuring robust

establishment of crops right at the starting point of the cultivation phase are

further driving the growth of seed treatment. Moreover, improvements in

microencapsulation and polymer coating technologies have enhanced treated seed

performance and safety. Owing to increased emphasis on integrated pest

management and precision farming, seed treatment is becoming a go-to

application method among global farmers.

The following segments are part of an in-depth analysis of the global

crop protection chemicals market:

|

Market Segments |

|

|

By Type |

●

Herbicides ●

Insecticides ●

Fungicides ●

Others |

|

By Crop |

●

Grains & Cereals ●

Pulses &

Oilseeds ●

Fruits &

Vegetables ●

Others |

|

By Source |

●

Synthetic ●

Bio-based |

|

By Mode of Application |

●

Foliar ●

Seed Treatment ●

Soil Treatment |

Crop Protection Chemicals

Market Share Analysis by Region

Asia Pacific is Projected

to Hold the Largest Share of the Global Crop Protection Chemicals Market Over

the Forecast Period

Asia-Pacific led the world's crop

protection chemicals market in the year 2024, with the highest share of about

36.5%, and is likely to hold the top spot in the forecast period. The dominance

of the region is due to the enormous farming lands in nations like China,

India, Indonesia, and Vietnam, where farming constitutes an important economic

activity. Rapid population growth and resultant demand for increased food

output have forced the use of modern farming methods, which involve intensive

use of crop protection chemicals, among regional farmers. Supporting government

policies that favor the application of agrochemicals, along with abundant

availability of rural labor and conducive climatic conditions for growing

variable crops, further spur the market. Increased awareness about crop damage

caused by pests, diseases, and weeds, and higher investment in R&D in the

farm space, have further driven the use of both synthetic and biologically

derived crop care products in the region.

Moreover, North America is expected to record the highest growth rate during the forecast period, which is spurred by sophisticated farming technologies, high use of genetically modified crops, and robust regulatory support that favors chemical use in a sustainable manner. The United States and Canada are putting sizable investments into precision farming, which encompasses the optimal use of pesticides, herbicides, and fungicides. This technology-led farming technique, coupled with increasing demand for crop quality and production among consumers, is likely to trigger high growth in the crop protection chemicals business in the region.

Crop Protection Chemicals

Market Competition Landscape Analysis

The global Crop Protection

Chemicals Market is poised for significant growth, with key players investing

heavily in technology and infrastructure. These companies are actively engaged

in research and development, strategic partnerships, and new product formulation

to enhance their market positions.

Global Crop Protection

Chemicals Market Recent Developments News:

●

In November 2023,

Insecticides (India) Limited launched four innovative crop protection products, Nakshatra, Supremo SP, Opaque, and Million, to address the growing demand from Rabi crop cultivation.

This expansion strengthens the company’s portfolio, offering farmers targeted

solutions for pest and disease management during India’s critical Rabi season.

●

In September 2023,

ADAMA Ltd., a global leader in crop protection, introduced two innovative

insecticides in India, Cosayr and Lapidos, featuring the advanced active ingredient

Chlorantraniliprole (CTPR) for the first time. These products are specifically

formulated to safeguard paddy and sugarcane crops, offering farmers enhanced

pest control and improved yield potential.

The Global Crop

Protection Chemicals Market is dominated

by a few large companies, such as

●

Bayer CropScience

●

Syngenta AG

●

BASF

●

Corteva, Inc.

●

FMC Corporation

●

ChemChina

●

Sumitomo Chemicals

●

UPL Ltd.

●

Nufarm

●

Rotam CropScience Ltd

● Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

- Global Crop Protection Chemicals Market Introduction and Market Overview

- Objectives of the Study

- Global Crop Protection Chemicals Market Scope and Market Estimation

- Global Crop Protection Chemicals Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Crop Protection Chemicals Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

- Market Segmentation

- Type of Global Crop Protection Chemicals Market

- Crop of Global Crop Protection Chemicals Market

- Source of Global Crop Protection Chemicals Market

- Mode of Application of Global Crop Protection Chemicals Market

- Region of Global Crop Protection Chemicals Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Key Product/Brand Analysis

- Technological Advancements

- Key Developments

- Porter’s Five Forces Analysis

- Bargaining Power of Suppliers

- Bargaining Power of Buyers

- Threat of Substitutes

- Threat of New Entrants

- Competitive Rivalry

- PEST Analysis

- Political Factors

- Economic Factors

- Social Factors

- Technology Factors

- Insights on Cost-effectiveness of Crop Protection Chemicals

- Key Regulation

- Global Crop Protection Chemicals Market Estimates & Historical Trend Analysis (2020 - 2024)

- Global Crop Protection Chemicals Market Estimates & Forecast Trend Analysis, by Type

- Global Crop Protection Chemicals Market Revenue (US$ Bn) Estimates and Forecasts, by Type, 2020 - 2033

- Herbicides

- Insecticides

- Fungicides

- Others

- Global Crop Protection Chemicals Market Revenue (US$ Bn) Estimates and Forecasts, by Type, 2020 - 2033

- Global Crop Protection Chemicals Market Estimates & Forecast Trend Analysis, by Crop

- Global Crop Protection Chemicals Market Revenue (US$ Bn) Estimates and Forecasts, by Crop, 2020 - 2033

- Grains & Cereals

- Pulses & Oilseeds

- Fruits & Vegetables

- Others

- Global Crop Protection Chemicals Market Revenue (US$ Bn) Estimates and Forecasts, by Crop, 2020 - 2033

- Global Crop Protection Chemicals Market Estimates & Forecast Trend Analysis, by Source

- Global Crop Protection Chemicals Market Revenue (US$ Bn) Estimates and Forecasts, by Source, 2020 - 2033

- Synthetic

- Bio-based

- Global Crop Protection Chemicals Market Revenue (US$ Bn) Estimates and Forecasts, by Source, 2020 - 2033

- Global Crop Protection Chemicals Market Estimates & Forecast Trend Analysis, by Mode of Application

- Global Crop Protection Chemicals Market Revenue (US$ Bn) Estimates and Forecasts, by Mode of Application, 2020 - 2033

- Foliar

- Seed Treatment

- Soil Treatment

- Global Crop Protection Chemicals Market Revenue (US$ Bn) Estimates and Forecasts, by Mode of Application, 2020 - 2033

- Global Crop Protection Chemicals Market Estimates & Forecast Trend Analysis, by Region

- Global Crop Protection Chemicals Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Crop Protection Chemicals Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

- North America Crop Protection Chemicals Market: Estimates & Forecast Trend Analysis

- North America Crop Protection Chemicals Market Assessments & Key Findings

- North America Crop Protection Chemicals Market Introduction

- North America Crop Protection Chemicals Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Type

- By Crop

- By Source

- By Mode of Application

- By Country

- The U.S.

- Canada

- North America Crop Protection Chemicals Market Assessments & Key Findings

- Europe Crop Protection Chemicals Market: Estimates & Forecast Trend Analysis

- Europe Crop Protection Chemicals Market Assessments & Key Findings

- Europe Crop Protection Chemicals Market Introduction

- Europe Crop Protection Chemicals Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Type

- By Crop

- By Source

- By Mode of Application

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Rest of Europe

- Europe Crop Protection Chemicals Market Assessments & Key Findings

- Asia Pacific Crop Protection Chemicals Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Crop Protection Chemicals Market Introduction

- Asia Pacific Crop Protection Chemicals Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Type

- By Crop

- By Source

- By Mode of Application

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Crop Protection Chemicals Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Crop Protection Chemicals Market Introduction

- Middle East & Africa Crop Protection Chemicals Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Type

- By Crop

- By Source

- By Mode of Application

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Crop Protection Chemicals Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Crop Protection Chemicals Market Introduction

- Latin America Crop Protection Chemicals Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Type

- By Crop

- By Source

- By Mode of Application

- By Country

- Brazil

- Argentina

- Mexico

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Crop Protection Chemicals Market Product Mapping

- Global Crop Protection Chemicals Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Crop Protection Chemicals Market Tier Structure Analysis

- Global Crop Protection Chemicals Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

- Bayer CropScience

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Bayer CropScience

* Similar details would be provided for all the players mentioned below

- Syngenta AG

- BASF

- Corteva, Inc.

- FMC Corporation

- ChemChina

- Sumitomo Chemicals

- UPL Ltd.

- Nufarm

- Rotam CropScience Ltd

- Others

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables