Defence Cybersecurity Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Solution (Network Security, Endpoint Security, Application Security, Cloud Security, Data Security), By Deployment (On-Premise, Cloud), By Application (Military, Intelligence, Critical Infrastructure, Space), And Geography

2025-11-21

Aerospace & Defense

Ekta Chaurasia (Team Lead)

Description

Defence Cybersecurity

Market Overview

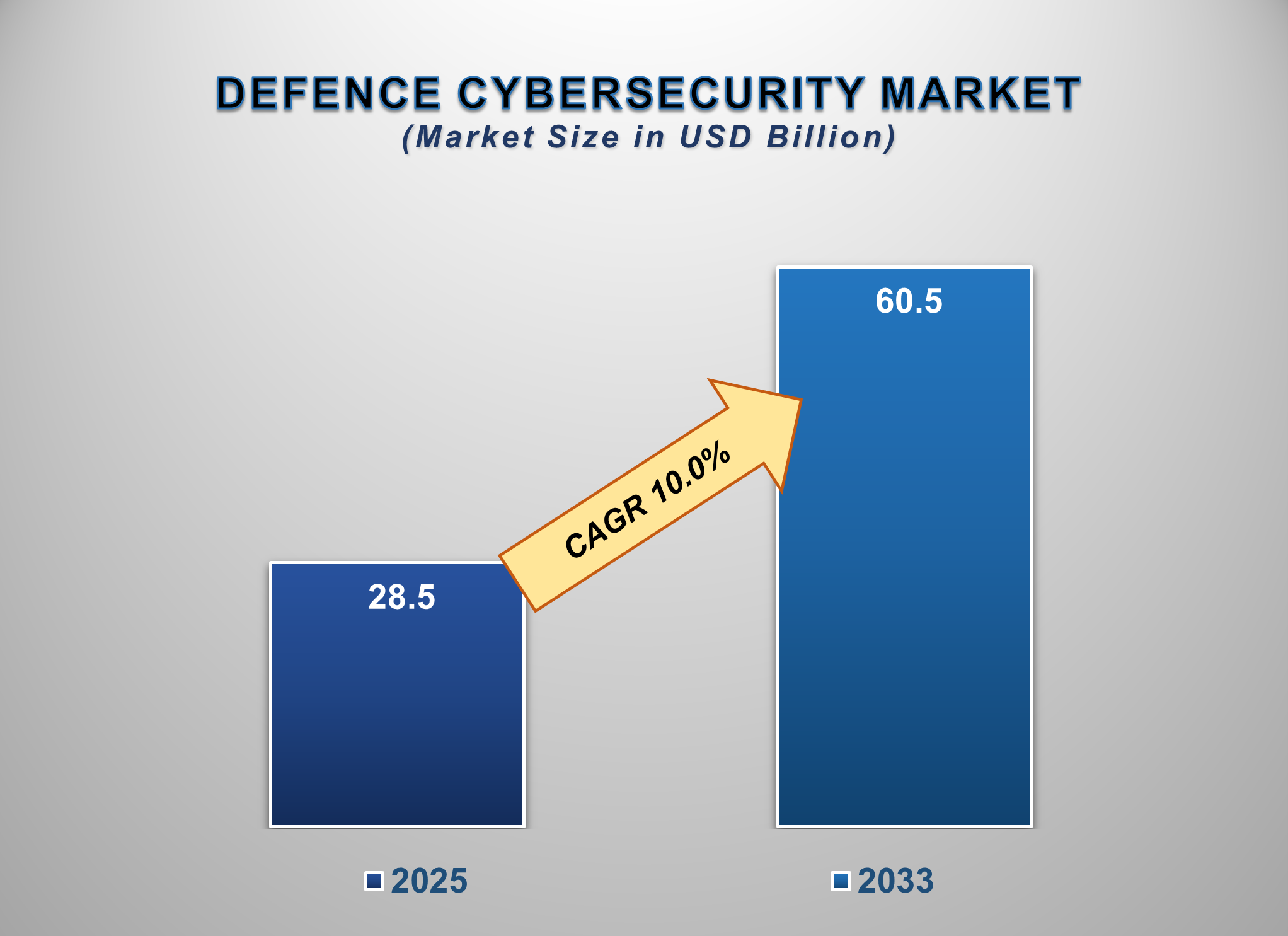

The Defence Cybersecurity Market is poised for substantial growth from 2025 to 2033, driven by the escalating sophistication of cyber threats, the digital transformation of military systems, and increased Defence spending on cyber capabilities. The market is projected to be valued at approximately USD 28.5 billion in 2025 and is forecasted to surge to nearly USD 60.5 billion by 2033, exhibiting a robust compound annual growth rate (CAGR) of 10.0% during this period.

Defence cybersecurity involves the protection of

military systems, networks, data, and critical infrastructure from digital

attacks, espionage, and disruption. Market growth is primarily fuelled by the

increasing frequency and complexity of state-sponsored cyberattacks, the

proliferation of connected devices on the battlefield (Internet of Battlefield

Things—IoBT), and the integration of advanced

technologies like AI and cloud computing into Defence operations. The shift

from traditional warfare to multi-domain operations, where cyber is a critical

domain, is a fundamental driver accelerating market investments. Supportive

government policies and mandates for securing national Defence assets, along

with rising geopolitical tensions, are key market enablers.

North America currently leads the market due to

its massive Defence budget and advanced technological base, while the

Asia-Pacific region is emerging as the fastest-growing market due to increasing

military modernization and rising cyber threats. With the continuous evolution

of cyber warfare tactics and the critical need to protect sensitive military

data and command-and-control systems, the Defence Cybersecurity Market is set

to remain a top priority for national security strategies over the next decade.

Defence Cybersecurity Market Drivers and

Opportunities

The

Proliferation of Sophisticated Cyber Threats is the Core Driver for the Defence Cybersecurity Market

Nation-states and sophisticated threat actors

are continuously developing advanced persistent threats (APTs), ransomware, and

other malicious cyber tools to target military secrets, disrupt critical

communications, and sabotage infrastructure. This escalating threat landscape

is forcing Defence organizations worldwide to significantly increase their

cybersecurity budgets. The need to protect sensitive data, from soldier-level

communications to strategic command systems, from espionage and theft is no

longer optional but a fundamental requirement for national security, directly

driving investment in advanced cybersecurity solutions.

Digital Transformation of Military Systems

is Catalyzing Massive Market Growth

Modern militaries are undergoing a rapid digital

transformation, incorporating cloud computing, AI, big data analytics, and

interconnected IoT devices into their operations. While this enhances

capabilities, it also dramatically expands the attack surface for adversaries.

The security of these new digital platforms, from connected soldier systems to

unmanned aerial vehicles (UAVs) and satellite networks, is paramount. This

transformation is creating massive demand for specialized cybersecurity

solutions tailored to the unique, high-stakes environment of military

operations, including resilient and secure communications and data links.

Technological Integration and Geopolitical

Tensions are Unlocking New Opportunities

The convergence of cybersecurity with other

cutting-edge technologies presents significant growth opportunities. The

integration of AI and machine learning for predictive threat intelligence,

automated threat detection, and real-time response is becoming a critical

capability. The rise of space as a contested domain has created a new frontier

for cybersecurity, requiring solutions to protect satellites and space-based

assets. Furthermore, increasing geopolitical rivalries and hybrid warfare

tactics are leading to sustained government funding for cyber Defence R&D.

Service diversification into areas like cyber warfare training, managed

security services, and proactive threat hunting allows companies to capture

additional value and become strategic partners to Defence agencies.

Defence Cybersecurity Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 28.5 Billion |

|

Market Forecast in 2033 |

USD 60.5 Billion |

|

CAGR % 2025-2033 |

10.0% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio, Technological Analysis, Company Market Share,

Company Heatmap, Pricing Analysis, Growth Factors and more |

|

Segments Covered |

●

By Solution ●

By Deployment ●

By Application |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Defence Cybersecurity Market Report Segmentation Analysis

The global Defence Cybersecurity

Market industry analysis is segmented by Solution, by Deployment, by

Application, and by Region.

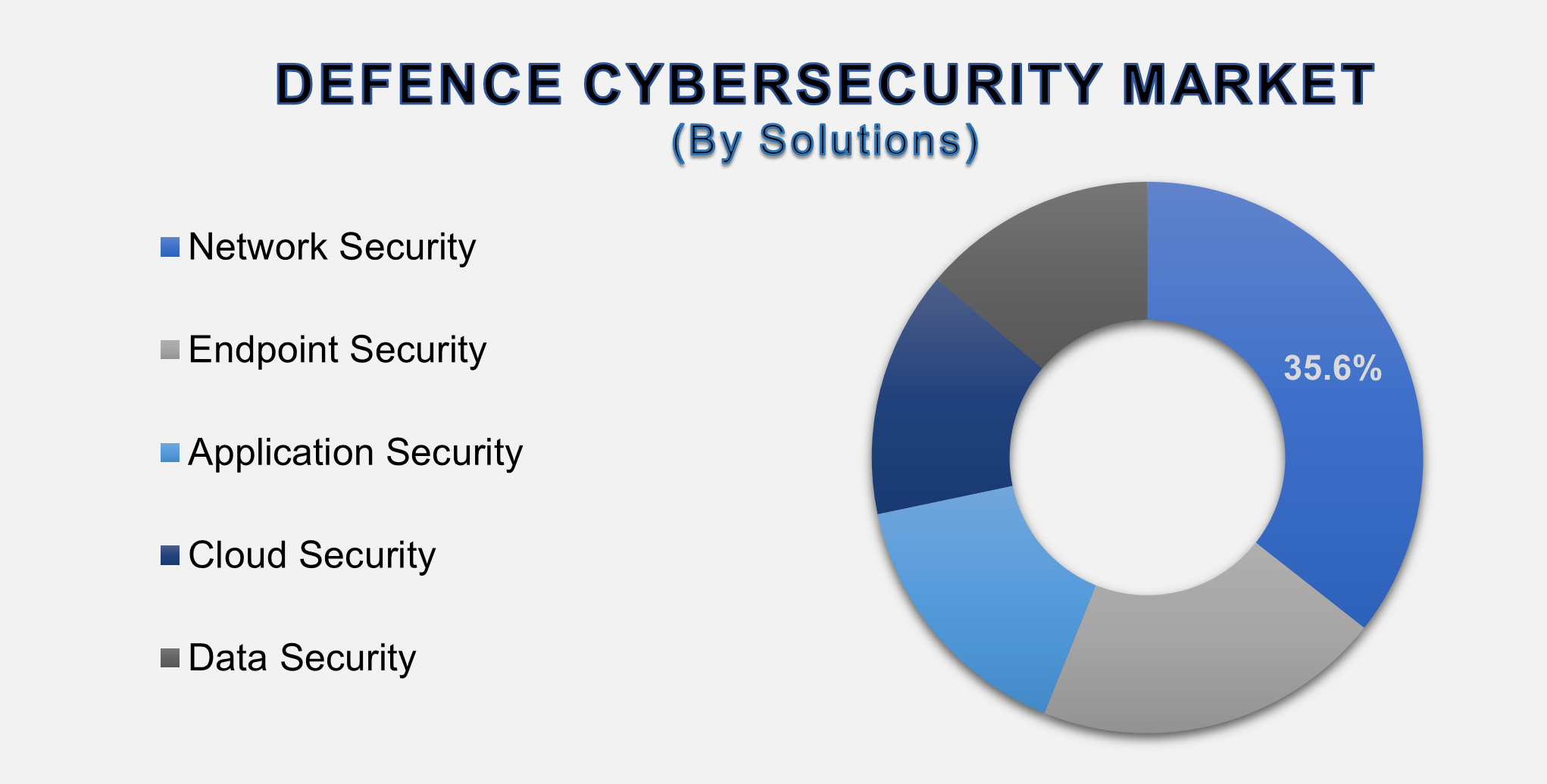

The Network Security segment is anticipated to command the

largest share in the global Defence Cybersecurity Market during the forecast

period.

Based on the Solution, the market is divided

into Network Security, Endpoint Security, Application Security, Cloud Security,

and Data Security. The Network Security segment dominates, accounting for the majority

of the market share. This is attributed to the

critical need to secure communication channels, command and control (C2)

systems, and data-in-transit from interception, manipulation, and

denial-of-service attacks, which are primary targets in cyber warfare.

The dominance of the Network Security segment is

rooted in the foundational role that secure and resilient networks play in

modern military operations. Every aspect of Defence, from real-time battlefield

communications and drone piloting to inter-agency data sharing, relies on

uncompromised network integrity. A breach in network security can lead to

catastrophic outcomes, including the disruption of missions, the loss of sensitive

data, and the manipulation of tactical information. Consequently, Defence agencies

prioritize investments in advanced firewalls, intrusion detection and

prevention systems (IDPS), and secure network infrastructure to create a

hardened digital perimeter that can withstand sophisticated attacks.

The On-Premise segment dominated the market in 2025 and is

projected to grow at a significant CAGR during the forecast period.

Based on Deployment, the market is segmented into

On-Premises and Cloud. The On-Premise segment holds the largest share.

This dominance is driven by the extreme sensitivity of military data and the

stringent requirements for data sovereignty, control, and air-gapped systems

that are isolated from public networks for maximum security.

The On-Premise segment's leadership is a direct

consequence of the unique security and regulatory demands of the Defence

sector. Military organizations often handle classified information that, by law

and policy, cannot be stored or processed on shared, multi-tenant cloud

infrastructure. On-premise solutions provide full control over the physical and

logical security of the servers and data, allowing for custom security

configurations and the implementation of air-gapped networks that are

physically disconnected from the internet. While cloud adoption is growing for

non-critical and unclassified data, the need for absolute control and isolation

for core military systems ensures the continued dominance of on-premise

deployments.

The Military segment is expected to hold a significant market

share in 2025.

By Application, the market is divided into

Military, Intelligence, Critical Infrastructure, and Space. The Military

segment is the major contributor, as it encompasses the largest and most

diverse set of cybersecurity needs, including army, navy, and air force

operations, battlefield communications, and weapon systems security.

The Military application segment's significant

market share stems from its all-encompassing scope and the direct link to

national Defence capabilities. This segment includes cybersecurity for

everything from naval ship combat systems and aircraft avionics to ground force

tactical networks and soldier-worn devices. The digitization of the battlefield

and the move towards network-centric warfare mean that every military branch

requires robust cybersecurity to ensure operational readiness and superiority.

The sheer scale of this segment, coupled with the high stakes of securing

active military platforms, makes it the largest and most critical application

area for Defence cybersecurity solutions.

The Critical Infrastructure segment is projected to grow at

the highest CAGR.

Based on Application, the market is segmented

into Military, Intelligence, Critical Infrastructure, and Space. While the Military

holds the largest share, the Critical Infrastructure segment is projected to

grow at the highest CAGR. This is due to the increasing recognition that

civilian critical infrastructure (energy grids, transportation, financial

systems) is a primary target in hybrid warfare, leading to increased crossover investment and collaboration between Defence and civilian

security agencies.

The following segments

are part of an in-depth analysis of the global Defence Cybersecurity Market:

|

Market Segments |

|

|

By Solution |

●

Network Security ●

Endpoint Security ●

Application Security ●

Cloud Security ●

Data Security |

|

By Application |

●

Military ●

Intelligence ●

Critical

Infrastructure ●

Space ●

Others |

|

By Deployment |

●

On-Premise ●

Cloud |

Defence Cybersecurity Market Share Analysis by Region

The North America region is anticipated to hold the largest

portion of the Defence Cybersecurity Market globally throughout the forecast

period.

North America is the leading segment, holding a

dominant share. This is a direct result of the region's massive Defence budget,

particularly in the United States, which has established the U.S. Cyber Command

and heavily invests in offensive and defensive cyber capabilities. The presence

of major Defence contractors and cybersecurity firms, coupled with a high level

of R&D funding, consolidates its leadership position.

The leadership of North America is anchored in

the United States' status as the world's largest Defence spender and its

proactive stance on cyber warfare. The U.S. Department of Defence (DoD) has

consistently prioritized cybersecurity in its budgets, launching numerous

initiatives and establishing dedicated cyber forces. The region is also home to

the world's leading Defence primes and cybersecurity technology companies,

fostering a robust ecosystem for innovation. High-profile cyber incidents

attributed to adversarial nation-states have further cemented cybersecurity as

a non-negotiable pillar of national security strategy, ensuring sustained and

significant investment.

Defence Cybersecurity Market Competition Landscape Analysis

The global Defence cybersecurity

market is highly competitive and fragmented, featuring a mix of large Defence

primes, specialized cybersecurity firms, and IT giants. The market is

characterized by stringent certification requirements, long sales cycles, and a

strong emphasis on R&D and innovation. Key strategies include forming

strategic partnerships and consortia to bid on large government contracts,

acquiring niche cybersecurity startups to gain specific technologies, and heavy

investment in R&D for AI-driven security and quantum-resistant

cryptography. Compliance with stringent government standards like NIST, FISMA,

and country-specific equivalents is a critical barrier to entry.

Global Defence Cybersecurity Market Recent Developments News:

- In February 2025, Lockheed Martin Corporation

announced a new contract to provide a unified cybersecurity platform for

the U.S. Army's tactical network, enhancing resilience against electronic

and cyberattacks.

- In January 2025, Northrop Grumman Corporation and

Palo Alto Networks formed a strategic partnership to deliver integrated

cyber Defence solutions for critical national infrastructure.

- In December 2024, Thales Group launched a new suite

of quantum-resistant encryption solutions designed to protect long-term

classified military communications.

- In October 2024, BAE Systems plc acquired a cloud security startup to

bolster its capabilities in securing Defence agencies' migration to hybrid

cloud environments.

The Global Defence

Cybersecurity Market Is Dominated by a Few Large Companies, such as

●

Lockheed Martin

Corporation

●

Northrop Grumman

Corporation

●

Raytheon Technologies

Corporation

●

Booz Allen Hamilton

Holding Corp.

●

BAE Systems plc

●

Thales Group

●

L3Harris Technologies,

Inc.

●

Leidos Holdings, Inc.

●

General Dynamics

Corporation

●

IBM Corporation

●

Cisco Systems, Inc.

●

Palo Alto Networks,

Inc.

●

Fortinet, Inc.

●

CrowdStrike Holdings,

Inc.

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Defence

Cybersecurity Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Defense Cybersecurity Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Defence

Cybersecurity Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Solution of Global Defence

Cybersecurity Market

1.3.2.Deployment of Global Defence

Cybersecurity Market

1.3.3.Application of Global Defence

Cybersecurity Market

1.3.4.Region of Global Defence

Cybersecurity Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Market

Entry Strategies

2.7.

Market

Dynamics

2.7.1.Drivers

2.7.2.Limitations

2.7.3.Opportunities

2.7.4.Impact Analysis of Drivers

and Restraints

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

3. Global

Defence Cybersecurity Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Defence Cybersecurity Market Estimates

& Forecast Trend Analysis, by Solution

4.1.

Global

Defence Cybersecurity Market Revenue (US$ Bn) Estimates and Forecasts, by Solution,

2020 - 2033

4.1.1.Network Security

4.1.2.Endpoint Security

4.1.3.Application Security

4.1.4.Cloud Security

4.1.5.Data Security

5. Global

Defence Cybersecurity Market Estimates

& Forecast Trend Analysis, by Deployment

5.1.

Global

Defence Cybersecurity Market Revenue (US$ Bn) Estimates and Forecasts, by Deployment,

2020 - 2033

5.1.1.On-Premise

5.1.2.Cloud

6. Global

Defence Cybersecurity Market Estimates

& Forecast Trend Analysis, by Application

6.1.

Global

Defence Cybersecurity Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

6.1.1.Military

6.1.2.Intelligence

6.1.3.Critical Infrastructure

6.1.4.Space

6.1.5.Others

7. Global

Defence Cybersecurity Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Defence Cybersecurity Market Revenue (US$ Bn) Estimates and Forecasts, by region,

2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Defence

Cybersecurity Market: Estimates &

Forecast Trend Analysis

8.1. North America Defence

Cybersecurity Market Assessments & Key Findings

8.1.1.North America Defence

Cybersecurity Market Introduction

8.1.2.North America Defence

Cybersecurity Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Solution

8.1.2.2.

By Deployment

8.1.2.3.

By Propulsion Type

8.1.2.4.

By Application

8.1.2.5. By Country

8.1.2.5.1. The U.S.

8.1.2.5.2. Canada

9. Europe Defence

Cybersecurity Market: Estimates &

Forecast Trend Analysis

9.1. Europe Defence

Cybersecurity Market Assessments & Key Findings

9.1.1.Europe Defence

Cybersecurity Market Introduction

9.1.2.Europe Defence

Cybersecurity Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Solution

9.1.2.2.

By Deployment

9.1.2.3.

By Propulsion Type

9.1.2.4.

By Application

9.1.2.5. By Country

9.1.2.5.1.

Germany

9.1.2.5.2.

Italy

9.1.2.5.3.

U.K.

9.1.2.5.4.

France

9.1.2.5.5.

Spain

9.1.2.5.6.

Switzerland

9.1.2.5.7. Rest

of Europe

10. Asia Pacific Defence

Cybersecurity Market: Estimates &

Forecast Trend Analysis

10.1. Asia Pacific Market

Assessments & Key Findings

10.1.1.

Asia

Pacific Defence Cybersecurity Market Introduction

10.1.2.

Asia

Pacific Defence Cybersecurity Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1.

By Solution

10.1.2.2.

By Deployment

10.1.2.3.

By Propulsion Type

10.1.2.4.

By Application

10.1.2.5. By Country

10.1.2.5.1. China

10.1.2.5.2. Japan

10.1.2.5.3. India

10.1.2.5.4. Australia

10.1.2.5.5. South Korea

10.1.2.5.6. Rest of Asia Pacific

11. Middle East & Africa Defence

Cybersecurity Market: Estimates &

Forecast Trend Analysis

11.1. Middle East & Africa

Market Assessments & Key Findings

11.1.1. Middle

East & Africa

Defence Cybersecurity Market Introduction

11.1.2. Middle

East & Africa

Defence Cybersecurity Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Solution

11.1.2.2.

By Deployment

11.1.2.3.

By Propulsion Type

11.1.2.4.

By Application

11.1.2.5. By Country

11.1.2.5.1. UAE

11.1.2.5.2. Saudi

Arabia

11.1.2.5.3. South

Africa

11.1.2.5.4. Rest

of MEA

12. Latin America

Defence Cybersecurity Market: Estimates

& Forecast Trend Analysis

12.1. Latin America Market

Assessments & Key Findings

12.1.1. Latin America Defence

Cybersecurity Market Introduction

12.1.2. Latin America Defence

Cybersecurity Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Solution

12.1.2.2.

By Deployment

12.1.2.3.

By Propulsion Type

12.1.2.4.

By Application

12.1.2.5. By Country

12.1.2.5.1. Brazil

12.1.2.5.2. Argentina

12.1.2.5.3. Mexico

12.1.2.5.4. Rest

of LATAM

13.

Country

Wise Market: Introduction

14.

Competition

Landscape

14.1. Global Defence

Cybersecurity Market Product Mapping

14.2. Global Defence

Cybersecurity Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3. Global Defence

Cybersecurity Market Tier Structure Analysis

14.4. Global Defence

Cybersecurity Market Concentration & Company Market Shares (%) Analysis,

2024

15.

Company

Profiles

15.1.

Lockheed Martin Corporation

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2.

Northrop Grumman Corporation

15.3.

Raytheon Technologies Corporation

15.4.

Booz Allen Hamilton Holding Corp.

15.5.

BAE Systems plc

15.6.

Thales Group

15.7.

L3Harris Technologies, Inc.

15.8.

Leidos Holdings, Inc.

15.9.

General Dynamics Corporation

15.10.

IBM Corporation

15.11.

Cisco Systems, Inc.

15.12.

Palo Alto Networks, Inc.

15.13.

Fortinet, Inc.

15.14.

CrowdStrike Holdings, Inc.

15.15.

Other Prominent Players

16. Research

Methodology

16.1. External Transportations /

Databases

16.2. Internal Proprietary

Database

16.3. Primary Research

16.4. Secondary Research

16.5. Assumptions

16.6. Limitations

16.7. Report FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables