Global Diabetes Management Apps Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Functionality (Blood Glucose Monitoring Apps, Insulin Tracking Apps, Diet & Nutrition Planning Apps, Physical Activity Tracking Apps, Others); By Device Type (Handheld Devices, Wearable Devices); By End User (Self/Home Healthcare, Hospitals & Specialty Diabetes Clinics, Academic & Research Institutes); and Geography

2025-12-16

Healthcare

Swetal (Research Analyst)

Description

Diabetes

Management Apps Market Overview

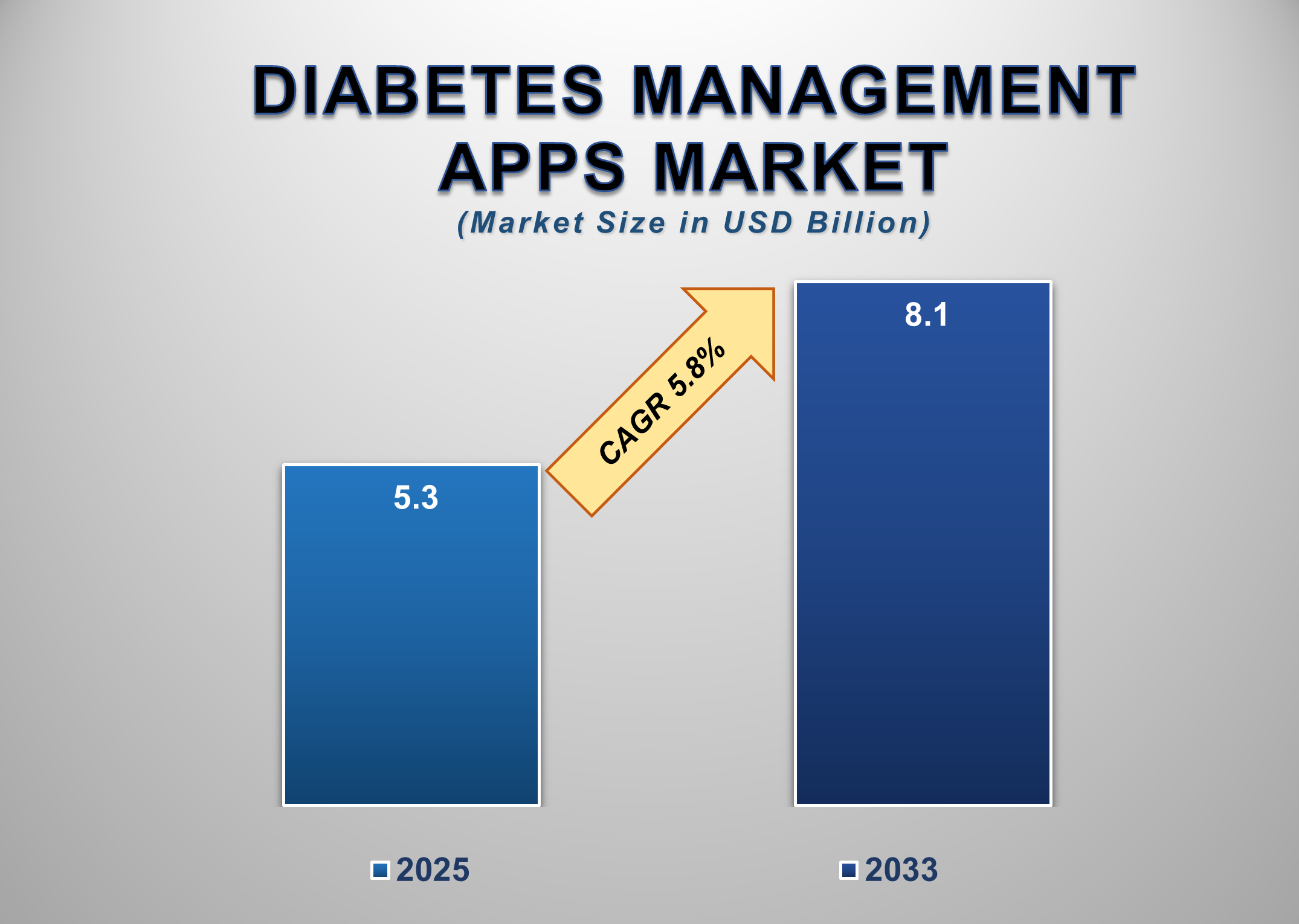

The Global Diabetes Management Apps Market Size is valued at USD 5.3 billion in 2025 and is projected to reach USD 8.1 billion by 2033, registering a CAGR of 5.8% during 2025–2033. Diabetes management apps provide digital tools for tracking blood glucose, insulin dosing, diet, physical activity, and medication adherence, and are increasingly integrated with glucometers, continuous glucose monitors (CGMs), wearables, and electronic health records. The market growth is driven by rising diabetes prevalence, expanding smartphone penetration, advances in connected health ecosystems, and growing acceptance of telehealth and remote patient monitoring among clinicians and patients.

Blood glucose monitoring apps

lead the market in functionality due to their direct role in glycemic control

and integration with monitoring devices. Self/home healthcare is the largest

end-user segment as patients increasingly adopt apps for daily management and

remote clinician communication. North America holds the largest regional share

(40.1% in 2025) because of high technology adoption and supportive

reimbursement frameworks, while Asia-Pacific is expected to register the

highest CAGR, driven by expanding mobile healthcare access, rising diabetes

incidence, and growing investment in digital health initiatives.

Diabetes

Management Apps Market Drivers and Opportunities

Rising Prevalence of Diabetes

and Increased Focus on Remote Chronic Disease Management are Driving the

Diabetes Management Apps Market Growth

The global prevalence of diabetes,

both type 1 and type 2, continues to rise, placing long-term pressure on

healthcare systems and increasing demand for scalable, cost-effective

management tools. Diabetes management apps address this need by enabling

continuous self-monitoring, automated logging of blood glucose readings,

reminders for medication and insulin dosing, and data sharing with healthcare

providers. Remote monitoring reduces the frequency of in-person visits while

improving glycemic control via timely clinician intervention and behavioral

nudges.

Healthcare systems and payers are

increasingly interested in digital therapeutics that lower complication rates

and hospitalizations associated with poorly controlled diabetes. Integration of

apps with CGMs and insulin pumps further elevates their clinical utility,

enabling trend analysis, predictive alerts for hypoglycemia/hyperglycemia, and

more precise insulin titration. In addition, regulatory recognition of digital

health solutions and growing reimbursement pilot programs in several markets

have encouraged app developers and device manufacturers to collaborate,

accelerating adoption. The combined pressure of rising disease burden and the

clinical/financial incentives for effective remote monitoring underpins robust

demand growth for diabetes management apps.

Growing Integration of

Connected Devices and AI-Enabled Personalization Is Accelerating Adoption of

Diabetes Management Apps

Technological convergence linking

blood glucose meters, wearables, CGMs, and insulin delivery devices with

smartphone apps is a major enabler for market expansion. Apps that

automatically ingest device data remove manual logging friction and improve

data fidelity. On top of device connectivity, the increasing use of artificial

intelligence and machine learning enables personalized recommendations:

adaptive meal suggestions, activity-based insulin adjustment prompts, and

predictive analytics that forecast glucose excursions.

Personalization increases user

engagement and clinical relevance, leading to better adherence and outcomes.

Clinical-grade analytics and decision-support features are also being

integrated into clinician dashboards, facilitating teleconsultations and remote

titration workflows. Consumer expectations for seamless interoperability,

secure cloud storage, and data visualization are pushing app vendors and device

OEMs toward open ecosystems and standardized data formats (e.g., FHIR). As

interoperability and AI capabilities deepen, apps become indispensable tools

for both patients and providers, driving sustained market uptake.

Emerging Markets’ Expansion of

Mobile Health Infrastructure Is Poised to Create Significant Opportunities in

the Diabetes Management Apps Market Worldwide

Rapid smartphone penetration,

falling mobile data costs, and expanding digital health initiatives in

Asia-Pacific, Latin America, and parts of Africa create a sizable opportunity

for diabetes app adoption. In regions with constrained healthcare access, apps

serve as primary touchpoints for education, screening, and ongoing disease

management. Localized apps that support regional languages, dietary patterns,

and culturally appropriate coaching are especially well-positioned. Moreover,

partnerships between app developers, telecom providers, and local health

ministries—plus integration of apps into national noncommunicable disease

strategies—can accelerate scale. Pay-for-performance pilots and value-based

care models in emerging markets also incentivize the deployment of remote

monitoring tools that reduce acute care utilization. Startups that offer

low-cost, offline-capable solutions, and global players that tailor features

for regional needs, will find sizable addressable markets as digital health

infrastructure matures.

Diabetes Management Apps Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 5.3 Billion |

|

Market Forecast in 2033 |

USD 8.1 Billion |

|

CAGR % 2025-2033 |

5.8% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Functionality,

By Device Type, By End User |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Diabetes Management Apps Market Report Segmentation Analysis

The global Diabetes Management

Apps Market is segmented by functionality, Device Type, End User, and by

Region.

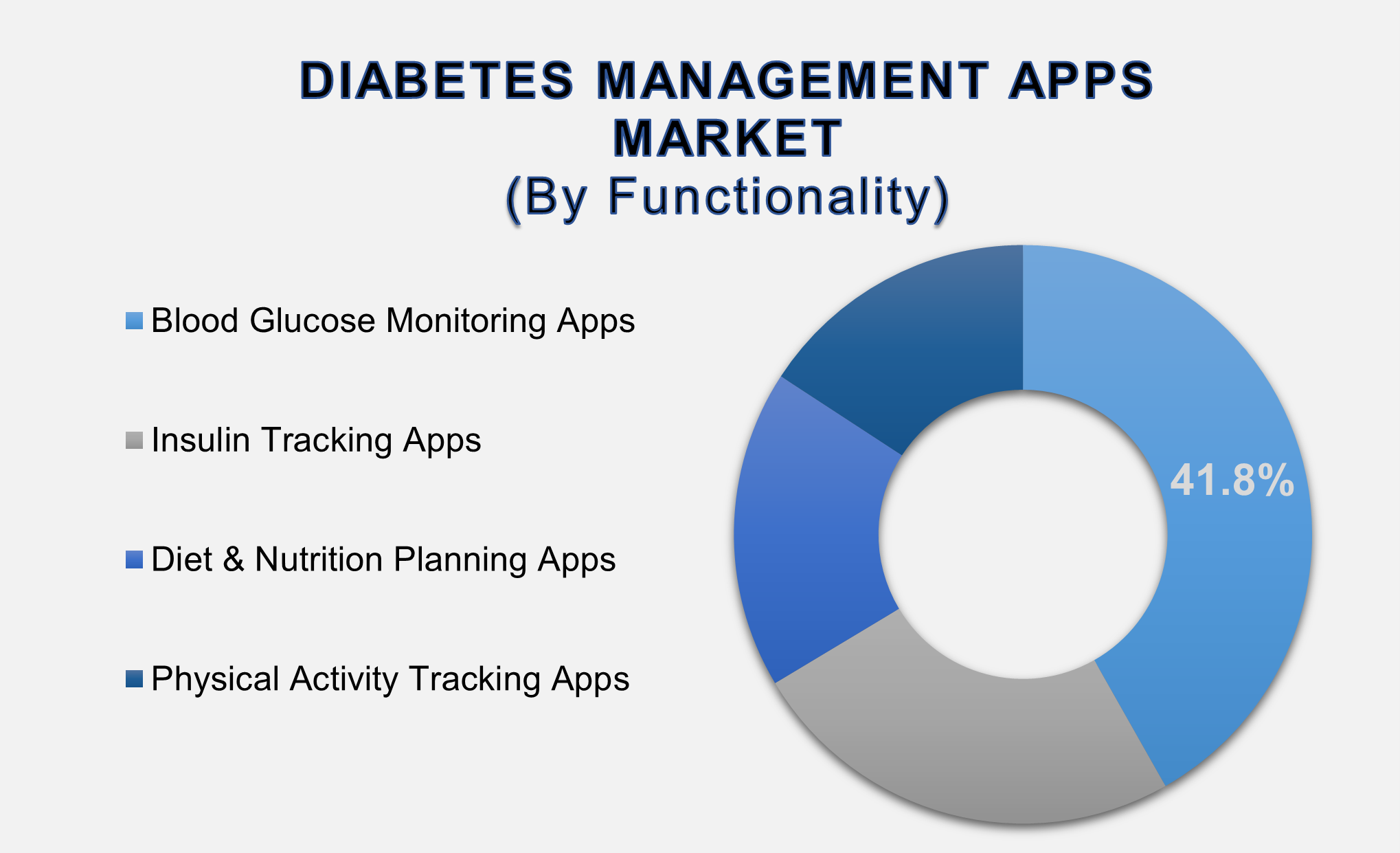

The Blood Glucose Monitoring

Apps segment accounted for the largest market share in the global Diabetes

Management Apps market

By Functionality, the market is segmented into Blood Glucose Monitoring Apps, Insulin Tracking Apps, Diet & Nutrition Planning Apps, Physical Activity Tracking Apps, and Others. The Blood Glucose Monitoring Apps segment accounted for the largest share of the global diabetes management apps market in 2025. This dominance stems from the direct clinical impact of glucose monitoring on therapy decisions and the broad integration of such apps with glucometers and CGM systems. Automated data capture, trend visualizations, and alerting for hypo/hyperglycemia increase the clinical utility and user engagement of these apps. Additionally, many payers and providers prioritize glucose monitoring as a key metric in remote diabetes care programs, which has driven app developers to focus on device interoperability, accuracy validation, and regulatory compliance. The emergence of FDA-cleared and CE-marked digital solutions has further enhanced trust among clinicians, accelerating recommendations and prescriptions of blood glucose monitoring apps. As continuous monitoring technologies evolve, the segment is expected to retain leadership due to its central role in glycemic control.

The Handheld Devices segment

accounted for the largest market share in the global Diabetes Management Apps

market

By Device Type, the market is

segmented into Handheld Devices and Wearable Devices. The Handheld Devices

segment accounted for the largest share in 2025, driven by widespread use of

smartphone-connected glucose meters and glucometers that pair with apps for

logging and analytics. Handheld devices remain prevalent due to their

cost-effectiveness, regulatory acceptance, and familiarity among patients.

While wearable CGMs and smart insulin pens are rapidly gaining

traction—particularly among type 1 patients and those requiring intensive

management—the larger installed base of handheld meters supports the continued

dominance of this segment. Integration of handheld device data into apps

simplifies workflows for patients managing diabetes at home, reinforcing adoption

across self-care users.

The Self/Home Healthcare

segment accounted for the largest market share in the global Diabetes

Management Apps market

By End User, the market is

segmented into Self/Home Healthcare, Hospitals & Specialty Diabetes

Clinics, and Academic & Research Institutes. The Self/Home Healthcare

segment accounted for the largest share in 2025, reflecting the consumer-driven

nature of diabetes apps and the shift toward patient-centric chronic care.

Individuals use apps to monitor daily glucose levels, track diet and activity,

and communicate summaries with clinicians. The convenience, privacy, and 24/7

accessibility of apps make them attractive for routine self-management.

Additionally, caregivers of pediatric and elderly patients increasingly rely on

remote monitoring features to supervise dosing and trends. Although

clinician-facing solutions for hospitals and specialty clinics are expanding,

the volume of individual users sustains self/home healthcare as the leading

end-user segment.

The following segments are

part of an in-depth analysis of the global Diabetes Management Apps Market:

|

Market

Segments |

|

|

By

Functionality |

●

Blood Glucose

Monitoring Apps ●

Insulin Tracking

Apps ●

Diet & Nutrition

Planning Apps ●

Physical Activity

Tracking Apps |

|

By Device Type |

●

Handheld Devices ●

Wearable Devices |

|

By End User |

●

Self/Home Healthcare ●

Hospitals &

Specialty Diabetes Clinics ●

Academic &

Research Institutes |

Diabetes

Management Apps Market Share Analysis by Region

The North America region is

projected to hold the largest share of the global Diabetes Management Apps

Market over the forecast period.

North America accounted for the

largest share of the global Diabetes Management Apps Market in 2025, capturing

40.1% of the market. This leadership is supported by high smartphone

penetration, advanced digital health ecosystems, broad reimbursement pilots for

remote monitoring, and a high prevalence of diabetes that has driven consumer

adoption. The U.S. market, in particular, benefits from early regulatory

frameworks for digital health solutions and established integrations between

device manufacturers and app developers.

Asia-Pacific (APAC) is projected

to be the fastest-growing region during the forecast period, driven by rising

diabetes incidence, expanding mobile internet access, and increasing

investments in telemedicine and mHealth initiatives. Countries such as China,

India, and Southeast Asian markets present large addressable populations and

rapid digital adoption, creating favorable conditions for localized diabetes

app offerings. Vendors that localize language support, accommodate regional

dietary patterns, and build partnerships with local healthcare ecosystems will

be best positioned to capture APAC growth.

Diabetes

Management Apps Market Competition Landscape Analysis

The Diabetes

Management Apps market is fragmented with a mix of specialist app developers

and device-oriented platform providers. Key players include mySugr, OneDrop,

Glucose Buddy, Diabetes: M, DarioHealth, FreeStyle LibreLink, and regional

leaders like BeatO and Health2Sync. Companies compete on device

interoperability, clinical validation, user experience, and integration with

telehealth services.

Global

Diabetes Management Apps Market Recent Developments News:

- In November 2024,

Medtronic received U.S. FDA clearance for an enhanced version of its

InPen® app featuring missed meal dose detection. This update paves the way

for the future launch of the Smart MDI (Multiple Daily Injections) system,

which will integrate with Medtronic’s Simplera continuous glucose monitor

(CGM) to support smarter insulin dosing.

- In January 2024, Abbott and

Tandem Diabetes Care announced the integration of the t:slim X2 insulin pump with Control-IQ

technology and Abbott’s FreeStyle Libre® 2 Plus sensor in the U.S. The

collaboration provides a hybrid closed-loop system designed to

automatically adjust insulin delivery to help reduce high and low glucose

events.

The Global Diabetes Management Apps Market is

dominated by a few large companies, such as

●

mySugr

●

OneDrop

●

Glucose Buddy

●

Diabetes: M

●

DarioHealth

●

FreeStyle LibreLink

●

Sugar Sense

●

BeatO

●

Health2Sync

●

GDm-Health

●

BlueStar

●

Klinio

●

Mighty Health

●

Gluroo

●

DiabNext

●

Vitadio

●

Wellthy

●

MediOrbit

●

Mendor

●

Breathe

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global Diabetes Management

Apps Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Diabetes Management Apps Market Scope and Market Estimation

1.2.1.Global Diabetes Management

Apps Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Diabetes Management

Apps Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Functionality of Global Diabetes

Management Apps Market

1.3.2.Device Type of Global Diabetes

Management Apps Market

1.3.3.End-use of Global Diabetes

Management Apps Market

1.3.4.Region of Global Diabetes

Management Apps Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Diabetes Management Apps Market

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

2.10.

Key

Regulation

3. Global

Diabetes Management Apps Market Estimates

& Historical Trend Analysis (2020 - 2024)

4.

Global Diabetes Management

Apps Market Estimates

& Forecast Trend Analysis, by Functionality

4.1.

Global

Diabetes Management Apps Market Revenue (US$ Bn) Estimates and Forecasts, by Functionality,

2020 - 2033

4.1.1.Blood Glucose Monitoring

Apps

4.1.2.Insulin Tracking Apps

4.1.3.Diet & Nutrition

Planning Apps

4.1.4.Physical Activity Tracking

Apps

5.

Global Diabetes Management

Apps Market Estimates

& Forecast Trend Analysis, by Device Type

5.1.

Global

Diabetes Management Apps Market Revenue (US$ Bn) Estimates and Forecasts, by Device

Type, 2020 - 2033

5.1.1.Handheld Devices

5.1.2.Wearable Devices

6.

Global Diabetes Management

Apps Market Estimates

& Forecast Trend Analysis, by End-use

6.1.

Global

Diabetes Management Apps Market Revenue (US$ Bn) Estimates and Forecasts, by End-use,

2020 - 2033

6.1.1.Self/Home Healthcare

6.1.2.Hospitals & Specialty

Diabetes Clinics

6.1.3.Academic & Research

Institutes

7. Global

Diabetes Management Apps Market Estimates

& Forecast Trend Analysis, by region

1.1.

Global

Diabetes Management Apps Market Revenue (US$ Bn) Estimates and Forecasts, by

region, 2020 - 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East & Africa

1.1.5.Latin America

8. North America Diabetes

Management Apps Market: Estimates &

Forecast Trend Analysis

8.1.

North

America Diabetes Management Apps Market Assessments & Key Findings

8.1.1.North America Diabetes

Management Apps Market Introduction

8.1.2.North America Diabetes

Management Apps Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Functionality

8.1.2.2. By Device

Type

8.1.2.3. By End-use

8.1.2.4.

By

Country

8.1.2.4.1.

The

U.S.

8.1.2.4.2.

Canada

9. Europe Diabetes

Management Apps Market: Estimates &

Forecast Trend Analysis

9.1.

Europe

Diabetes Management Apps Market Assessments & Key Findings

9.1.1.Europe Diabetes Management

Apps Market Introduction

9.1.2.Europe Diabetes Management

Apps Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Functionality

9.1.2.2. By Device

Type

9.1.2.3. By End-use

9.1.2.4.

By

Country

9.1.2.4.1. Germany

9.1.2.4.2. Italy

9.1.2.4.3. U.K.

9.1.2.4.4. France

9.1.2.4.5. Spain

9.1.2.4.6. Switzerland

9.1.2.4.7.

Rest of Europe

10. Asia Pacific Diabetes

Management Apps Market: Estimates &

Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Diabetes Management Apps Market Introduction

10.1.2.

Asia

Pacific Diabetes Management Apps Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1. By Functionality

10.1.2.2. By Device

Type

10.1.2.3. By End-use

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6.

Rest

of Asia Pacific

11. Middle East & Africa Diabetes

Management Apps Market: Estimates &

Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Diabetes Management Apps Market

Introduction

11.1.2.

Middle East & Africa Diabetes Management Apps Market Size

Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Functionality

11.1.2.2. By Device

Type

11.1.2.3. By End-use

11.1.2.4.

By

Country

11.1.2.4.1. South

Africa

11.1.2.4.2. UAE

11.1.2.4.3. Saudi

Arabia

11.1.2.4.4.

Rest of MEA

12. Latin America

Diabetes Management Apps Market:

Estimates & Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Diabetes Management Apps Market Introduction

12.1.2.

Latin

America Diabetes Management Apps Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

12.1.2.1. By Functionality

12.1.2.2. By Device

Type

12.1.2.3. By End-use

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Mexico

12.1.2.4.3. Argentina

12.1.2.4.4.

Rest of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Diabetes Management Apps Market Product Mapping

14.2.

Global

Diabetes Management Apps Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3.

Global

Diabetes Management Apps Market Tier Structure Analysis

14.4.

Global

Diabetes Management Apps Market Concentration & Company Market Shares (%)

Analysis, 2023

15.

Company

Profiles

15.1. mySugr

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all

the players mentioned below

15.2. OneDrop

15.3. Glucose Buddy

15.4. Diabetes:M

15.5. DarioHealth

15.6. FreeStyle

LibreLink

15.7. Sugar Sense

15.8. BeatO

15.9. Health2Sync

15.10. GDm-Health

15.11. BlueStar

15.12. Klinio

15.13. Mighty Health

15.14. Gluroo

15.15. DiabNext

15.16. Vitadio

15.17. Wellthy

15.18. MediOrbit

15.19. Mendor

15.20. Breathe

15.21. Other

Prominent Players

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables