Diabetes Management Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Product (Devices, Drugs); By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies); and Geography

2025-11-10

Healthcare

Swetal (Research Analyst)

Description

Diabetes Management Market Overview

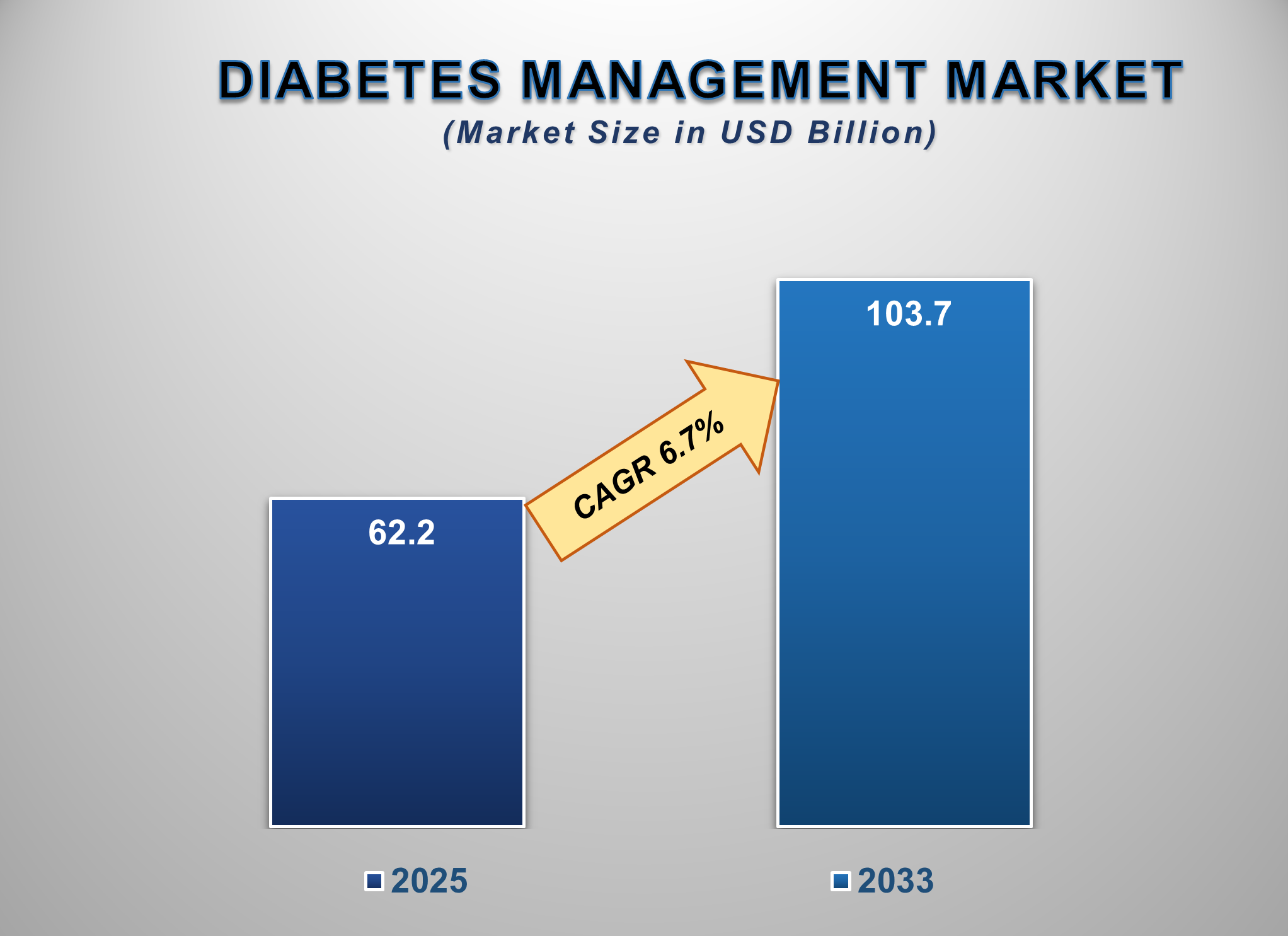

The Global Diabetes Management Market Size is projected to witness robust growth from 2025 to 2033, propelled by the escalating global prevalence of diabetes, increasing adoption of advanced technological solutions, and growing government initiatives for chronic disease management. Valued at approximately USD 62.2 billion in 2025, the market is expected to reach USD 103.7 billion by 2033, reflecting a compound annual growth rate (CAGR) of 6.7% over the forecast period.

The diabetes management market is

a critical and rapidly evolving sector within the global healthcare industry,

encompassing a wide array of products from monitoring devices to therapeutic

drugs. The market is experiencing a significant transformation, moving from

traditional management approaches to integrated, technology-driven solutions

focused on improving patient outcomes and quality of life. The high efficacy

and essential nature of insulin and other anti-diabetic medications continue to

form a substantial foundation of market revenue. A primary growth catalyst is

the expanding global diabetic population, which is strongly linked to the

rising incidence of risk factors such as obesity, sedentary lifestyles, and

unhealthy diets. The growing aging population, which has a higher

susceptibility to Type 2 diabetes, further fuels market expansion.

The market is also benefiting

from rapid technological innovation, particularly in the field of glucose

monitoring, with Continuous Glucose Monitoring (CGM) systems and smart insulin

pens revolutionizing patient care. These technologies offer real-time data,

improved glycemic control, and enhanced convenience. Furthermore, the

increasing penetration of digital health platforms and telehealth services is

facilitating remote patient monitoring and personalized care management. The

patent expiry of several blockbuster drugs has spurred robust generic

competition, improving affordability and access, especially in cost-sensitive

markets. North America remains the dominant region due to high healthcare

expenditure and early technology adoption, while the Asia-Pacific region is

anticipated to exhibit the fastest growth, driven by a large and

under-diagnosed patient pool and improving healthcare infrastructure.

Diabetes Management

Market Drivers and Opportunities

Rising Global Prevalence

of Diabetes and Associated Complications

The

increasing global incidence of diabetes mellitus is the fundamental driver for

this market. This surge is intrinsically linked to the growing prevalence of

obesity, physical inactivity, and population aging, which are major risk

factors for Type 2 diabetes. Diabetes is a chronic condition that requires

lifelong management, and its serious complications, including cardiovascular

disease, neuropathy, retinopathy, and nephropathy, create a substantial and

continuous demand for effective management tools and medications. Growing

public health awareness campaigns and screening programs are leading to earlier

diagnosis and a greater emphasis on proactive management to prevent

complications, thereby driving the adoption of various diabetes management

products.

The United States is confronting a severe and

expanding diabetes epidemic, a condition that affects a substantial portion of

the population and imposes a tremendous burden on the healthcare system.

According to the Centers for Disease Control and Prevention (CDC), over 38

million Americans have diabetes, with approximately 90-95% of cases being Type

2. The economic impact is staggering, with diagnosed diabetes costing the U.S.

economy over $400 billion annually in direct medical costs and reduced productivity.

This high prevalence is driven by a powerful confluence of demographic,

lifestyle, and health factors. Primarily, the high rates of obesity and

overweight individuals are a key driver, as excess body fat is a leading risk

factor for insulin resistance. Concurrently, sedentary lifestyles and dietary

patterns high in processed foods and sugars contribute significantly.

Furthermore, the aging population is a major factor, as the risk of Type 2

diabetes increases with age. Increased focus on preventive care and screening

is identifying more cases, further illuminating the scale of this public health

crisis.

Technological

Advancements and Shift Towards Digital Health

The

rapid pace of technological innovation is a significant driver for the diabetes

management market. The development and widespread adoption of CGM systems,

which provide real-time glucose readings without fingersticks, represent a

paradigm shift in patient care. Integrated systems like smart insulin pens and

automated insulin delivery (AID) systems are enhancing dosing accuracy and

adherence. The overarching trend towards digitalization, including mobile

health apps and cloud-based data platforms, allows for better data tracking,

remote consultation with healthcare providers, and personalized insights,

empowering patients to take a more active role in managing their condition.

Opportunity for the Diabetes Management Market

Expansion in Emerging Markets and Development of Personalized

& AI-Driven Solutions

A

significant opportunity lies in the vast untapped potential of emerging

economies in the Asia-Pacific, Latin America, and Africa. Rising disposable

incomes, improving healthcare access, and growing awareness of diabetes in

these regions are creating new growth frontiers. Companies that can offer

cost-effective monitoring devices and generic medications are poised to capture

a substantial market share. Furthermore, a major opportunity exists in the

development of next-generation, personalized therapies, including advanced

closed-loop AID systems, ultra-rapid and smart insulins, and the integration of

artificial intelligence (AI) and machine learning for predictive analytics in

glucose management. These innovations promise to automate and optimize diabetes

care, thereby appealing to a broader patient base and improving clinical

outcomes.

Diabetes Management

Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 62.2 Billion |

|

Market Forecast in 2033 |

USD 103.7 Billion |

|

CAGR % 2025-2033 |

6.7% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, Company Share, Company Heatmap, Company

Production Capacity, Growth Factors and more |

|

Segments Covered |

●

By Product ●

By Distribution Channel |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Netherlands 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19)

Egypt 20) South Africa |

Diabetes Management

Market Report Segmentation Analysis

The global Diabetes Management

Market industry analysis is segmented by product and by distribution channel.

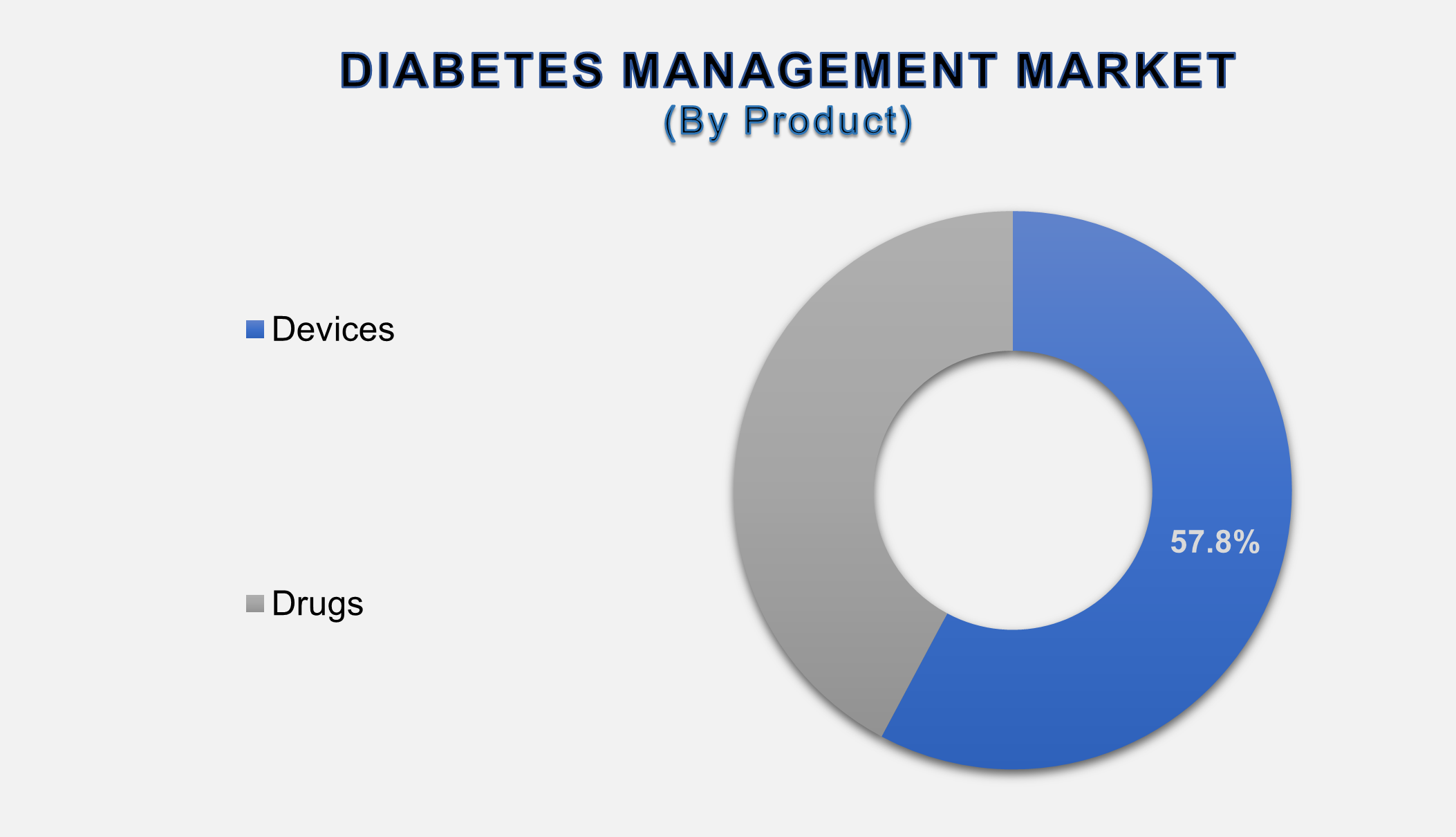

The Dominance of the Devices Product Segment

The Devices segment is the leading and

fastest-growing contributor to the diabetes management market. This dominance

is secured by the critical and continuous need for glucose monitoring and

insulin delivery. The segment is primarily driven by the revolutionary adoption

of Continuous Glucose Monitoring (CGM) systems, which offer superior glycemic

control and quality of life compared to traditional blood glucose meters (BGM).

Alongside CGMs, advanced insulin delivery devices

such as insulin pumps and smart pens are gaining significant traction due to

their precision and convenience. The constant technological innovation, leading

to more accurate, user-friendly, and integrated devices, ensures this segment's

continued leadership in driving market growth and revenue.

Within devices, the Blood Glucose Monitoring

Systems segment holds a dominant share, with CGM systems spearheading growth.

While traditional BGM strips and meters remain a massive market due to their

low cost and widespread availability, the shift towards CGM is undeniable. CGM

systems provide real-time, dynamic glucose information, trend data, and alerts

for highs and lows, enabling proactive diabetes management. The strong clinical

evidence supporting their benefits in reducing hypoglycemic events and improving

HbA1c levels, coupled with increasing insurance coverage, is driving their

rapid adoption among both Type 1 and Type 2 diabetes patients, cementing the

segment's leadership.

The Insulin Drugs Segment commands a major share of the

market

The Insulin segment commands a dominant market

share within drugs because it is a life-saving therapy for all Type 1 diabetic

patients and a critical treatment for many with advanced Type 2 diabetes.

Despite the emergence of new drug classes, insulin remains irreplaceable for a

large patient population.

The market includes a diverse range of products

from rapid-acting to long-acting analog insulins, which offer improved

pharmacokinetic profiles and reduced risk of hypoglycemia compared to human

insulin. The high cost of modern analog insulins and the chronic nature of the

disease, requiring daily administration, ensure that this segment continues to

generate substantial and steady revenue, even amid pricing pressures and

biosimilar competition.

The following segments are part of an in-depth analysis of the global

diabetes management market:

|

Market Segments |

|

|

By Product |

●

Devices o

Blood Glucose

Monitoring Systems o

Insulin Delivery

Devices o

Others ●

Drugs o

Insulin o

Oral Anti-diabetic

Drugs o

Non-Insulin

Injectables |

|

By Distribution Channel |

●

Hospital Pharmacies ●

Retail Pharmacies ●

Online Pharmacies |

Diabetes Management

Market Share Analysis by Region

The North America region is expected to

dominate the global diabetes management market during the forecast period.

North America is anticipated to be the

leader in the global Diabetes Management Market. This dominance is anchored by

the region's high healthcare expenditure, favourable reimbursement policies for

advanced devices like CGMs and insulin pumps, and a high prevalence of

diabetes. The presence of major market players, a strong focus on technological

innovation, and high awareness levels among patients and healthcare providers

in the U.S. and Canada create a highly conducive environment for market growth.

Furthermore, well-established regulatory pathways and a robust digital health

infrastructure secure North America's leading position.

Diabetes represents a profound and growing

public health challenge in the United States, affecting tens of millions of

individuals and placing an immense strain on the healthcare system. Current

data indicate

that over 38 million Americans have diabetes, with Type 2 diabetes accounting

for the vast majority of cases.

The economic impact is monumental, with

total estimated costs exceeding US$400 billion annually when factoring in

direct medical expenses and indirect costs from lost productivity and

disability. This high prevalence is driven by a powerful synergy of factors,

primarily the obesity epidemic, as excess weight is a leading risk factor for

insulin resistance. Concurrently, sedentary lifestyles, dietary habits, and an

aging population are major contributors. The burden of pre-diabetes, affecting

nearly 98 million American adults, highlights the scale of the potential future

patient pool. The condition's chronic nature and severe complications,

including heart disease, stroke, kidney failure, and blindness, underscore the

critical need for effective and continuous management solutions.

Global Diabetes

Management Market Recent Developments News:

- In January 2025, Dexcom, Inc. launched its

next-generation G7+ Continuous Glucose Monitoring system in the U.S.,

featuring an extended wear time and a smaller, more discreet form factor.

- In February 2025, Novo Nordisk A/S entered a

strategic collaboration with a digital therapeutics company to combine its

GLP-1 receptor agonists with a personalized digital coaching platform for

weight and diabetes management.

- In March 2025, Medtronic plc received FDA approval

for its new hybrid closed-loop system with enhanced automated insulin

delivery algorithms for improved overnight glycemic control.

- In April 2025, Eli Lilly and Company announced

positive Phase III results for a novel once-weekly dual GIP and GLP-1

receptor agonist, showing superior efficacy in blood glucose control and

weight reduction.

The Global Diabetes

Management Market is dominated by a few large companies, such as

●

Medtronic plc

●

Dexcom, Inc.

●

Abbott Laboratories

●

Roche Diagnostics

●

Insulet Corporation

●

Novo Nordisk A/S

●

Sanofi

●

Eli Lilly and Company

●

Merck & Co., Inc.

●

AstraZeneca PLC

●

Tandem Diabetes Care,

Inc.

●

LifeScan, Inc.

●

Ascensia Diabetes Care

●

Ypsomed Holding AG

●

Beta Bionics, Inc.

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global Diabetes Management

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Diabetes Management Market Scope and Market Estimation

1.2.1.Global Diabetes Management

Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Diabetes Management

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product of Global Diabetes

Management Market

1.3.2.Distribution Channel of

Global Diabetes Management Market

1.3.3.Region of Global Diabetes

Management Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Diabetes Management Market

2.8.

Incidence

and Prevalence of Diabetes, by key countries

2.9.

Key

Products/Brand Analysis

2.10.

Porter’s

Five Forces Analysis

2.11.

PEST

Analysis

2.12.

Key

Regulation

3. Global

Diabetes Management Market Estimates

& Historical Trend Analysis (2020 - 2024)

4.

Global Diabetes Management

Market Estimates & Forecast Trend

Analysis, by Product

4.1.

Global

Diabetes Management Market Revenue (US$ Bn) Estimates and Forecasts, by Product,

2020 - 2033

4.1.1.Devices

4.1.1.1.

Blood

Glucose Monitoring Systems

4.1.1.2.

Insulin

Delivery Devices

4.1.1.3.

Others

4.1.2.Drugs

4.1.2.1.

Insulin

4.1.2.2.

Oral

Anti-diabetic Drugs

4.1.2.3.

Non-Insulin

Injectables

5.

Global Diabetes Management

Market Estimates & Forecast Trend

Analysis, by Distribution Channel

5.1.

Global

Diabetes Management Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution

Channel, 2020 - 2033

5.1.1.Hospital Pharmacies

5.1.2.Retail Pharmacies

5.1.3.Online Pharmacies

6. Global

Diabetes Management Market Estimates

& Forecast Trend Analysis, by region

1.1.

Global

Diabetes Management Market Revenue (US$ Bn) Estimates and Forecasts, by region,

2020 - 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East & Africa

1.1.5.Latin America

7. North America Diabetes

Management Market: Estimates &

Forecast Trend Analysis

7.1. North America Diabetes

Management Market Assessments & Key Findings

7.1.1.North America Diabetes

Management Market Introduction

7.1.2.North America Diabetes

Management Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

7.1.2.1. By Product

7.1.2.2. By Distribution

Channel

7.1.2.3.

By

Country

7.1.2.3.1.

The

U.S.

7.1.2.3.2.

Canada

8. Europe Diabetes

Management Market: Estimates &

Forecast Trend Analysis

8.1.

Europe

Diabetes Management Market Assessments & Key Findings

8.1.1.Europe Diabetes Management

Market Introduction

8.1.2.Europe Diabetes Management

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Product

8.1.2.2. By Distribution

Channel

8.1.2.3.

By

Country

8.1.2.3.1. Germany

8.1.2.3.2. Italy

8.1.2.3.3. U.K.

8.1.2.3.4. France

8.1.2.3.5. Spain

8.1.2.3.6. Netherlands

8.1.2.3.7.

Rest of Europe

9. Asia Pacific Diabetes

Management Market: Estimates &

Forecast Trend Analysis

9.1.

Asia

Pacific Market Assessments & Key Findings

9.1.1.Asia Pacific Diabetes

Management Market Introduction

9.1.2.Asia Pacific Diabetes

Management Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product

9.1.2.2. By Distribution

Channel

9.1.2.3.

By

Country

9.1.2.3.1. China

9.1.2.3.2. Japan

9.1.2.3.3. India

9.1.2.3.4. Australia

9.1.2.3.5. South Korea

9.1.2.3.6.

Rest

of Asia Pacific

10. Middle East & Africa Diabetes

Management Market: Estimates &

Forecast Trend Analysis

10.1.

Middle

East & Africa Market Assessments & Key Findings

10.1.1.

Middle East & Africa Diabetes Management Market

Introduction

10.1.2.

Middle East & Africa Diabetes Management Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Product

10.1.2.2. By Distribution

Channel

10.1.2.3.

By

Country

10.1.2.3.1. UAE

10.1.2.3.2. Saudi

Arabia

10.1.2.3.3. South

Africa

10.1.2.3.4.

Rest of MEA

11. Latin America

Diabetes Management Market: Estimates

& Forecast Trend Analysis

11.1.

Latin

America Market Assessments & Key Findings

11.1.1.

Latin

America Diabetes Management Market Introduction

11.1.2.

Latin

America Diabetes Management Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

11.1.2.1. By Product

11.1.2.2. By Distribution

Channel

11.1.2.3.

By

Country

11.1.2.3.1. Brazil

11.1.2.3.2. Mexico

11.1.2.3.3. Argentina

11.1.2.3.4.

Rest of LATAM

12. Country Wise Market:

Introduction

13.

Competition

Landscape

13.1.

Global

Diabetes Management Market Product Mapping

13.2.

Global

Diabetes Management Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

13.3.

Global

Diabetes Management Market Tier Structure Analysis

13.4.

Global

Diabetes Management Market Concentration & Company Market Shares (%)

Analysis, 2024

14.

Company

Profiles

14.1. Medtronic plc

14.1.1.

Company

Overview & Key Stats

14.1.2.

Financial

Performance & KPIs

14.1.3.

Product

Portfolio

14.1.4.

SWOT

Analysis

14.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all

the players mentioned below

14.2. Dexcom, Inc.

14.3. Abbott

Laboratories

14.4. Roche

Diagnostics

14.5. Insulet

Corporation

14.6. Novo Nordisk

A/S

14.7. Sanofi

14.8. Eli Lilly and

Company

14.9. Merck &

Co., Inc.

14.10. AstraZeneca

PLC

14.11. Tandem

Diabetes Care, Inc.

14.12. LifeScan,

Inc.

14.13. Ascensia

Diabetes Care

14.14. Ypsomed

Holding AG

14.15. Beta Bionics,

Inc.

14.16. Other

Prominent Players

15. Research

Methodology

15.1.

External

Databases

15.2.

Internal

Proprietary Database

15.3.

Primary

Research

15.4.

Secondary

Research

15.5.

Assumptions

15.6.

Limitations

15.7.

Report

FAQs

16. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables