Diagnostic Imaging Market Size and Forecast (2025 – 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Modality (X-ray Imaging Systems, CT Scanners, Ultrasound Systems, MRI Systems, Nuclear Imaging, Mammography, Fluoroscopy, Others); By Application (Cardiology, Neurology, Orthopedics, Gynecology, Oncology, Others); By End User (Hospitals, Specialty Clinics, Diagnostic Imaging Centers, Others); and Geography

2025-08-06

Healthcare

Swetal (Research Analyst)

Description

Diagnostic Imaging Market Overview

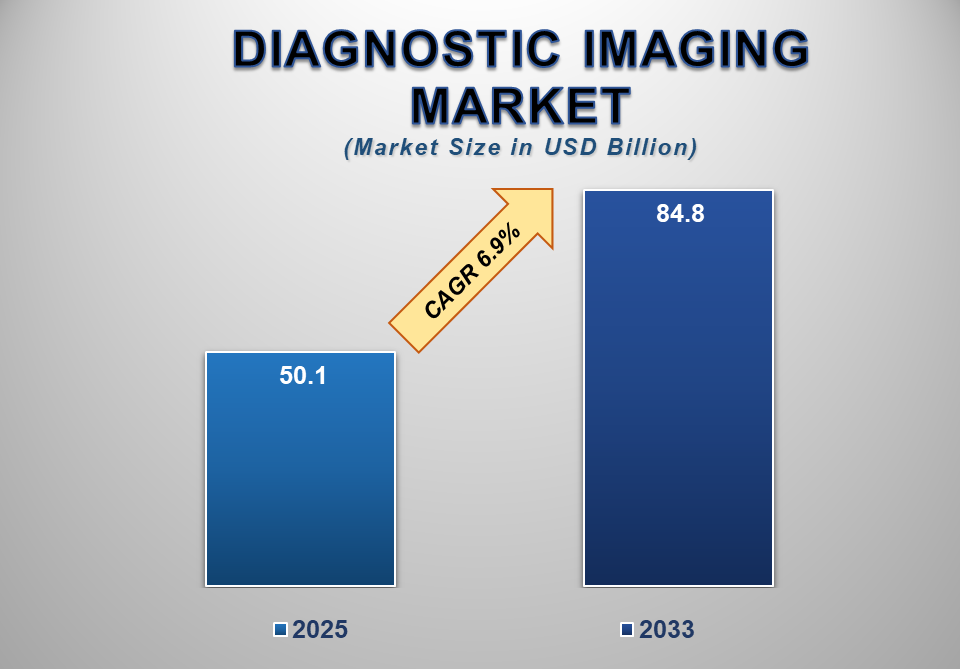

The Global Diagnostic Imaging Market size is experiencing robust growth, driven by the increasing prevalence of chronic diseases, rising demand for early and accurate diagnosis, and technological advancements in imaging modalities. According to market analysis, the Diagnostic Imaging Market is projected to grow from USD 50.1 billion in 2025 to USD 84.8 billion by 2033, registering a compound annual growth rate (CAGR) of 6.9% during the forecast period.

Diagnostic imaging plays a pivotal role in the modern global medical imaging market by enabling non-invasive visualization of the internal anatomy and physiological processes. The increasing global burden of cardiovascular, neurological, and oncological disorders has led to a surge in demand for advanced imaging solutions across healthcare settings. X-ray imaging remains the most widely adopted modality, especially for primary diagnostics and emergency care, followed by CT, MRI, and ultrasound technologies. The rise in aging populations, expanding healthcare access in emerging markets, and supportive reimbursement structures in developed economies are additional growth catalysts. Innovations such as AI-enhanced imaging, portable and handheld devices, and 3D/4D imaging continue to reshape clinical workflows and improve diagnostic accuracy. Moreover, integration of cloud-based imaging and teleradiology solutions enables faster and remote diagnostics, especially in underserved areas. The global shift toward value-based healthcare is further encouraging providers to invest in precision diagnostics that improve outcomes while minimizing costs.

Diagnostic Imaging Market Drivers and Opportunities

The increasing prevalence of chronic diseases and an aging population are anticipated to lift the Diagnostic Imaging market during the forecast period.

The global rise in chronic conditions such as cardiovascular diseases, cancer, orthopedic disorders, and neurological conditions is significantly boosting demand for diagnostic imaging. Aging populations in both developed and emerging regions are more susceptible to these conditions, necessitating timely and accurate diagnosis for effective disease management. As a result, healthcare systems are increasingly prioritizing the deployment of advanced imaging modalities, such as CT, MRI, and PET, which enable early detection and guide therapeutic decisions. For instance, cardiovascular imaging is in high demand due to the increasing burden of heart-related ailments, where modalities like echocardiography, CT angiography, and cardiac MRI provide crucial insights. Simultaneously, public health campaigns, government initiatives for cancer screening programs, and improved health insurance coverage are promoting access to diagnostic services. The expansion of diagnostic imaging services across ambulatory care centers and rural healthcare setups further contributes to market penetration. Moreover, advancements in image-guided therapies and hybrid imaging (PET-CT, SPECT-CT) enhance the clinical value of diagnostic imaging in therapeutic planning. These trends reflect a growing reliance on non-invasive imaging technologies as essential tools in disease prevention, monitoring, and personalized treatment approaches.

Technological advancements in imaging systems and AI integration are anticipated to lift the Diagnostic Imaging market during the forecast period.

Ongoing innovation in diagnostic imaging technologies presents a transformative growth driver for the global market. The integration of artificial intelligence (AI), machine learning, and deep learning algorithms is revolutionizing radiology by enabling faster image processing, automated anomaly detection, and decision support for clinicians. AI-powered tools are improving diagnostic accuracy and efficiency across modalities, while reducing interpretation variability and workload for radiologists. Additionally, the emergence of advanced image reconstruction techniques, ultra-high-resolution imaging, and dose-reduction technologies is enhancing patient safety and image clarity. The portable and handheld Diagnostic imaging devices market is expanding diagnostic access in point-of-care and remote settings, especially in underdeveloped healthcare markets. Hybrid modalities such as PET-MRI and PET-CT are facilitating comprehensive evaluations of complex conditions by combining functional and anatomical imaging. Furthermore, the adoption of cloud-based PACS systems and teleradiology solutions is enabling real-time collaboration among multidisciplinary teams, accelerating clinical decisions and improving workflow management. These technological innovations are reshaping diagnostic imaging practices globally, unlocking new market opportunities and improving patient care.

Opportunity for the Diagnostic Imaging Market

Growing demand for imaging in emerging economies is anticipated to lift the Diagnostic Imaging market during the forecast period.

Emerging economies represent a substantial opportunity for the diagnostic imaging market, driven by rapid urbanization, improving healthcare infrastructure, and rising healthcare awareness. Countries such as India, China, Brazil, Indonesia, and South Africa are witnessing increased investments in public and private healthcare facilities, including diagnostic imaging centers. The expansion of government-backed health insurance schemes and incentives for medical equipment procurement are facilitating the adoption of advanced imaging modalities in tier II and III cities. Moreover, the rising burden of non-communicable diseases in these regions is prompting early diagnostic initiatives and the introduction of nationwide screening programs, especially for cancer, tuberculosis, and cardiovascular conditions. International collaborations, funding from global health organizations, and local manufacturing of affordable imaging equipment are making diagnostic solutions more accessible. Additionally, training programs for radiologists and sonographers, and the establishment of mobile imaging units, are further contributing to market expansion. Manufacturers are customizing solutions for emerging markets by offering compact, cost-effective, and energy-efficient devices that cater to infrastructure limitations. As diagnostic imaging becomes a core component of preventative and primary healthcare delivery in these regions, market players have a strategic opportunity to expand their geographic footprint and revenue streams.

Diagnostic Imaging Market Scope

Diagnostic Imaging Market Report Segmentation Analysis

The global Diagnostic Imaging Market industry analysis is segmented by modality, by application, by end user, and by region.

The X-ray Imaging Systems segment accounted for the largest market share in the global Diagnostic Imaging market.

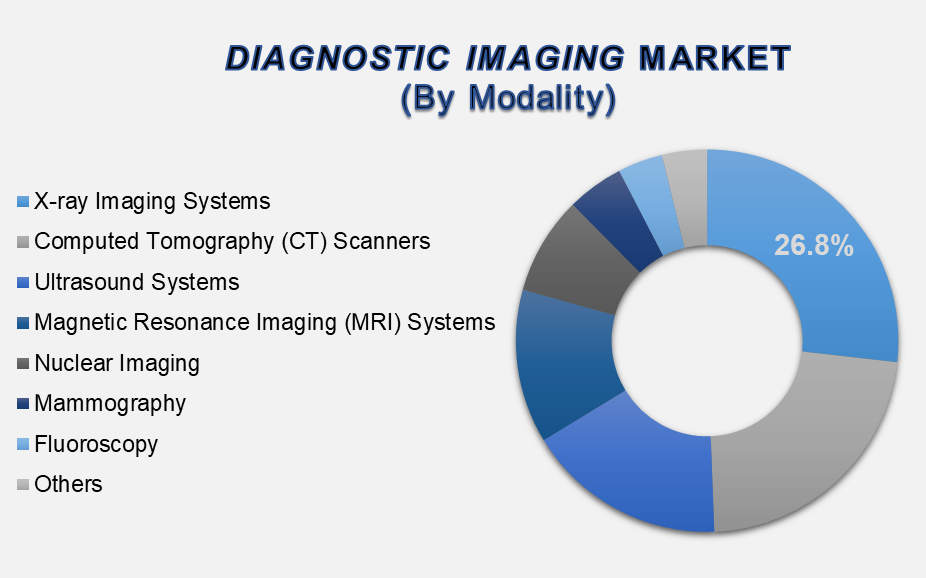

By Modality, the market is segmented into X-ray Imaging Systems, Computed Tomography (CT) Scanners, Ultrasound Systems, Magnetic Resonance Imaging (MRI) Systems, Nuclear Imaging, Mammography, Fluoroscopy, and Others. The X-ray Imaging Systems segment accounted for the largest market share at 26.8% due to its widespread use in emergency care, orthopedics, chest imaging, and general diagnostics. X-ray systems are cost-effective, fast, and commonly available across both public and private healthcare settings. The growing deployment of digital X-ray systems, portable devices, and AI-integrated imaging software continues to reinforce this segment's dominance.

The Cardiology segment holds the major share in the Diagnostic Imaging market.

By Application, the market is segmented into Cardiology, Neurology, Orthopedics, Gynecology, Oncology, and Others. Cardiology leads the global diagnostic imaging market owing to the increasing prevalence of cardiovascular diseases and growing adoption of non-invasive imaging for diagnosis, monitoring, and interventional planning. Modalities such as echocardiography, CT angiography, and cardiac MRI are widely utilized to detect structural and functional abnormalities, evaluate blood flow, and assess myocardial viability. The rising demand for accurate, real-time cardiac assessments in both hospital and outpatient settings supports continued growth in this segment.

The Hospitals segment accounted for the largest market share in the global Diagnostic Imaging market.

By End User, the market is segmented into Hospitals, Specialty Clinics, Diagnostic Imaging Centers, and Others. Hospitals dominate the global diagnostic imaging market due to their large-scale infrastructure, comprehensive diagnostic service offerings, and integration with inpatient and surgical care. Hospitals often serve as referral centers for advanced diagnostic procedures, and their ability to invest in high-cost imaging systems such as MRI, PET-CT, and interventional radiology suites strengthens their market share. The growing number of hospital-based radiology departments and focus on clinical efficiency and patient throughput further boost demand for advanced imaging solutions.

The following segments are part of an in-depth analysis of the global Diagnostic Imaging Market:

Diagnostic Imaging Market Share Analysis by Region

The North America region is projected to hold the largest share of the global Diagnostic Imaging market over the forecast period.

North America holds the dominant position in the global Diagnostic Imaging market, accounting for approximately 35.6% of the total market share. The region's leadership is driven by the presence of leading manufacturers, advanced healthcare infrastructure, high adoption of cutting-edge technologies, and supportive reimbursement policies. The U.S. accounts for the majority of the regional share, benefiting from robust investments in precision diagnostics, AI integration in radiology, and strong demand from aging populations. Strategic partnerships between healthcare providers and imaging technology firms further enhance clinical adoption.

In contrast, the Asia Pacific is forecasted to witness the highest CAGR in the Diagnostic Imaging market during the forecast period. Rapid urbanization, a growing middle class, and increasing healthcare expenditure in countries such as China, India, and South Korea are catalyzing the adoption of diagnostic imaging equipment. Government-led health initiatives, insurance expansions, and medical tourism are supporting imaging infrastructure upgrades across hospitals and diagnostic centers. The presence of local manufacturers and cost-competitive service providers contributes to broader access and affordability. As Asia Pacific healthcare systems continue to modernize, the region presents significant growth opportunities for both equipment manufacturers and service providers.

Diagnostic Imaging Market Competition Landscape Analysis

The market is competitive, with several established players and new entrants offering a range of products. Some of the key players are Siemens Healthineers, GE Healthcare, Philips Healthcare, Canon Medical Systems, Fujifilm Holdings, Hitachi Healthcare, Hologic, Shimadzu Corporation, Carestream Health, Samsung Medison, and Mindray Medical.

Global Diagnostic Imaging Market Recent Developments News:

In September 2023 - GE Healthcare announced a collaboration with Mayo Clinic to drive innovation in medical imaging and theranostics. The partnership focuses on developing advanced technologies to help healthcare providers accurately diagnose and precisely treat medical conditions while enabling personalized patient care.

In December 2022 - Koninklijke Philips N.V. introduced its Ultrasound Compact System 5000 Series, featuring premium image quality in a portable design. The system supports clinicians in making confident diagnoses across various clinical settings.

In June 2022 - Siemens Healthineers AG received FDA clearance for its new Symbia Pro.specta system, an advanced SPECT/CT (Single Photon Emission Computed Tomography/Computed Tomography) imaging solution. The system incorporates next-generation SPECT and CT imaging technologies to enhance diagnostic capabilities.

The Global Diagnostic Imaging Market is dominated by a few large companies, such as

Siemens Healthineers

GE Healthcare

Philips Healthcare

Canon Medical Systems

Fujifilm Holdings

Hitachi Healthcare

Hologic

Shimadzu Corporation

Carestream Health

Samsung Medison

Mindray Medical

Agfa-Gevaert

Esaote

Neusoft Medical

Konica Minolta

Planmed

Analogic Corporation

CurveBeam

United Imaging

Shenzhen Anke High-Tech

Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

- Global Diagnostic Imaging Market Introduction and Market Overview

- Objectives of the Study

- Global Diagnostic Imaging Market Scope and Market Estimation

- Global Diagnostic Imaging Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Diagnostic Imaging Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2033

- Market Segmentation

- Modality of Global Diagnostic Imaging Market

- Application of Global Diagnostic Imaging Market

- End-user of Global Diagnostic Imaging Market

- Region of Global Diagnostic Imaging Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Diagnostic Imaging Market

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Diagnostic Imaging Market Estimates & Historical Trend Analysis (2021 - 2024)

- Global Diagnostic Imaging Market Estimates & Forecast Trend Analysis, by Modality

- Global Diagnostic Imaging Market Revenue (US$ Bn) Estimates and Forecasts, by Modality, 2021 - 2033

- X-ray Imaging Systems

- Analog X-ray

- Digital X-ray

- Computed Tomography (CT) Scanners

- Low-slice CT

- Medium-slice CT

- High-slice CT

- Ultrasound Systems

- 2D Ultrasound

- 3D/4D Ultrasound

- Doppler Ultrasound

- Magnetic Resonance Imaging (MRI) Systems

- Low-field MRI (<1.5T)

- Mid-field MRI (1.5T)

- High-field MRI (3T and above)

- Nuclear Imaging

- Positron Emission Tomography (PET)

- Single Photon Emission Computed Tomography (SPECT)

- Mammography

- Film-screen mammography

- Digital mammography

- 3D tomosynthesis

- Fluoroscopy

- C-arm systems

- Fixed fluoroscopy

- Others

- Global Diagnostic Imaging Market Estimates & Forecast Trend Analysis, by Application

- Global Diagnostic Imaging Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2033

- Cardiology

- Neurology

- Orthopedics

- Gynecology

- Oncology

- Others

- Global Diagnostic Imaging Market Estimates & Forecast Trend Analysis, by End-user

- Global Diagnostic Imaging Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2021 - 2033

- Hospitals

- Specialty Clinics

- Diagnostic Imaging Centers

- Others

- Global Diagnostic Imaging Market Estimates & Forecast Trend Analysis, by region

- Global Diagnostic Imaging Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- North America Diagnostic Imaging Market: Estimates & Forecast Trend Analysis

- North America Diagnostic Imaging Market Assessments & Key Findings

- North America Diagnostic Imaging Market Introduction

- North America Diagnostic Imaging Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Modality

- By Application

- By End-user

- By Country

- The U.S.

- Canada

- Europe Diagnostic Imaging Market: Estimates & Forecast Trend Analysis

- Europe Diagnostic Imaging Market Assessments & Key Findings

- Europe Diagnostic Imaging Market Introduction

- Europe Diagnostic Imaging Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Modality

- By Application

- By End-user

- By Country

- Germany

- Italy

- U.K.

- France

- Spain

- Switzerland

- Rest of Europe

- Asia Pacific Diagnostic Imaging Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Diagnostic Imaging Market Introduction

- Asia Pacific Diagnostic Imaging Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Modality

- By Application

- By End-user

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East & Africa Diagnostic Imaging Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Diagnostic Imaging Market Introduction

- Middle East & Africa Diagnostic Imaging Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Modality

- By Application

- By End-user

- By Country

- South Africa

- UAE

- Saudi Arabia

- Rest of MEA

- Latin America Diagnostic Imaging Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Diagnostic Imaging Market Introduction

- Latin America Diagnostic Imaging Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Modality

- By Application

- By End-user

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Country Wise Market: Introduction

- Competition Landscape

- Global Diagnostic Imaging Market Product Mapping

- Global Diagnostic Imaging Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Diagnostic Imaging Market Tier Structure Analysis

- Global Diagnostic Imaging Market Concentration & Company Market Shares (%) Analysis, 2023

- Company Profiles

- Siemens Healthineers

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

* Similar details would be provided for all the players mentioned below

- GE Healthcare

- Philips Healthcare

- Canon Medical Systems

- Fujifilm Holdings

- Hitachi Healthcare

- Hologic

- Shimadzu Corporation

- Carestream Health

- Samsung Medison

- Mindray Medical

- Agfa-Gevaert

- Esaote

- Neusoft Medical

- Konica Minolta

- Planmed

- Analogic Corporation

- CurveBeam

- United Imaging

- Shenzhen Anke High-Tech

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables