Digital Wound Care Management Systems Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Product Type (Wound Assessment & Monitoring Software, Digital Wound Measurement Devices, Telemedicine & Remote Consultation Platforms and Others); By Wound Type (Chronic Wounds and Acute Wounds); By End-user (Hospitals & Clinics, Home Healthcare Settings, Long-term Care Facilities & Nursing Homes, Wound Care Specialty Centers) and Geography

2025-08-06

Healthcare

Swetal (Research Analyst)

Description

Digital Wound Care Management Systems Market Overview

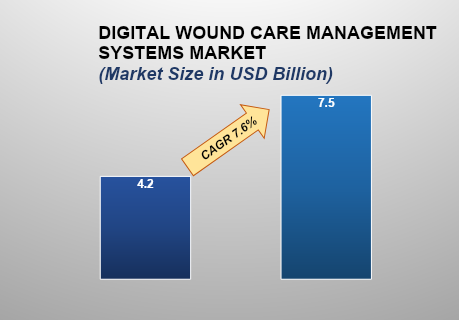

The digital wound care management systems market size is anticipated to experience substantial growth from 2025 to 2033, fuelled by the global incidence of wounds and an increase in surgical procedures, driving the digital wound care management systems market size. With an estimated valuation of approximately USD 4.22 billion in 2025, the market is expected to reach USD 7.54 billion by 2033, registering a robust compound annual growth rate (CAGR) of 7.6% over the decade.

Digital Wound Care Management Systems (DWCMS) represent sophisticated technology platforms to improve the assessment, documentation, and treatment of wounds by utilizing electronic tools. DWCMS combines electronic health records (EHRs), imaging technology, artificial intelligence (AI), and mobile apps to aid clinicians in providing more precise, efficient, and effective wound care. DWCMS enables real-time tracking of the wound healing process through the use of high-resolution imaging and measurement devices to monitor healing and recognize the onset of complications.

Artificial intelligence algorithms can support wound classification, infection risk assessment, and treatment guidance based on history and clinical protocols. Furthermore, the systems reduce documentation burden through the capability of digitized charting, standardization of reporting, and secure information exchange across multidisciplinary care groups. Telemedicine functions and remote patient monitoring additionally maintain a continuum of care, particularly in the care of patients in rural or home-care conditions. Integration of wearables and intelligent dressings is an increasingly popular development, enabling ongoing measurement of the conditions of wounds in terms of temperature, moisture, and pH.

By facilitating enhanced decision support and enhanced workflows, DWCMS can enhance patient outcomes, lower hospitalization and healthcare system costs, and improve compliance with regulatory requirements. DWCMS can aid in the collection of organized data and analytics to inform research as well. Although DWCMS is a valuable tool with various additional benefits, some challenges are noted, including the requirement for compatibility with different systems, security of the information, clinician education, and universal technology accessibility. As technology in the sector becomes increasingly advanced, DWCMS are likely to become integral parts of wound care strategies today and in the future, enabling proactive and decision-supportive management of wounds.

Digital Wound Care Management Systems Industry Drivers and Opportunities

Rising Incidence of Chronic Wounds is anticipated to lift the Digital Wound Care Management Systems Market during the forecast period

The rising incidence of chronic wounds in the elderly and diabetic populations is a key growth factor for the digital wound care management systems market. Diabetic foot ulcers cause significant health risks and can result in serious complications. With an aging world population and the growth of diabetic conditions, the demand for effective wound management solutions heightens.

Digital wound care systems provide advanced tools to monitor and manage these wounds, allowing for timely intervention and minimizing the risk of complications. Robust digital technology support ensures round-the-clock monitoring, enabling healthcare professionals to monitor healing progress in wounds and realign treatment plans in accordance. This anticipatory management not only enhances patient outcomes but also lowers the frequency of hospital visits as well as the overall healthcare bill.

Technological Advancements drive the global Digital Wound Care Management Systems Market

Technological innovations, including artificial intelligence (AI), telemedicine, and wearables, are revolutionizing the management of wound care. AI-driven diagnostics improve wound assessment precision through the analysis of images and the projection of healing trajectories. Telemedicine provides remote consultation capabilities to enable experts to reach far-flung populations without the necessity of physical visits. Wearable technology provides real-time monitoring of wound conditions and supplies information regarding factors such as moisture and temperature, both of which are vital in the effective management of wounds. All these technologies not only enhance the efficiency and efficacy of wound care but render it increasingly available, particularly to remote and underserved populations.

Opportunity for the Digital Wound Care Management Systems Market

Expansion of Telemedicine is a significant opportunity in the global Digital Wound Care Management Systems Market

The development of telemedicine creates a major growth prospect for the market of digital wound care management systems. Telemedicine improves the accessibility of specialized wound care to remote and rural populations who might struggle to reach conventional healthcare centers. Telemedicine enables healthcare professionals to evaluate wounds remotely, follow healing progress, and modify treatment plans in real-time. This enhances the outcomes of the patient while minimizing the frequency of visits to clinics, which in turn decreases the costs of healthcare. Telemedicine further supports patient-centered care by providing increased flexibility and convenience, contributing to greater patient satisfaction and compliance with treatment plans. As healthcare organizations increasingly adopt digital solutions, the incorporation of telemedicine into the management of wounds can take center stage in the healthcare delivery of the future.

Digital Wound Care Management Systems Market Scope

Digital Wound Care Management Systems Market Report Segmentation Analysis

The global Digital Wound Care Management Systems Market industry analysis is segmented by Product Type, by Wound Type, by End-use, and by region.

Wound Assessment & Monitoring Software Segment Holding the Largest Market Share

Wound Assessment & Monitoring Software has the largest market share in the Digital Wound Care Management Systems market because it plays a vital role in allowing for accurate, real-time wound measurement and monitoring. These software systems employ high-definition imaging, electronic measurement tools, and artificial intelligence to give accurate estimates of wound area, depth, tissue classification, and healing patterns. This information enables healthcare professionals to make timely, judicious decisions, streamlining the speed and impact of interventions. The software also allows for standardized documentation and longitudinal monitoring of healing, both of which are essential for clinical care and reimbursement.

Their capability to integrate smoothly with Electronic Health Records (EHRs) and accommodate remote monitoring makes them even more attractive. With chronic wounds needing to be monitored constantly, they become an indispensable aid to reducing care variability and maintaining consistency among caregivers. The software solutions can even be implemented in different care settings -- hospitals, outpatient clinics, and home healthcare -- making it easier to adopt them. With the rising focus on data-driven care and the increasing rate of chronic wounds, the demand for sophisticated wound assessment and monitoring software has been on the rise, making it the market leader.

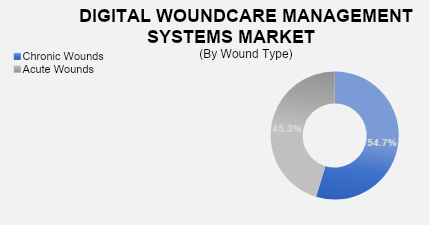

Chronic Wound Type Segment Holding Major Digital Wound Care Management Systems Market Share.

The Chronic Wound type segment has the largest market share in the Digital Wound Care Management Systems market, led by the rising incidence of chronic conditions like diabetes, vascular diseases, and pressure injuries. Chronic wounds, such as diabetic foot wounds, venous leg wounds, and pressure wounds, are most difficult to manage because of their delayed healing process and susceptibility to infection and recurrence. These wounds demand ongoing and specialist treatment, which digital systems can deliver. Digital wound care systems allow for regular and thorough monitoring of chronic wounds, enabling timely intervention and treatment plans. This is particularly vital in chronic wound care since the earlier the signs of complications are detected, the better the chance of averting negative results, including hospitalization or amputation.

Additionally, these systems enable the collection and analysis of data to improve treatment effectiveness and support clinical research. With the increasing burden of chronic illnesses across the globe, especially in aging populations, the demand for the treatment of chronic wounds is increasing. This increased patient population and the complexity of the management of chronic wounds make the segment a priority for healthcare professionals and technology vendors, both establishing it as the leading segment in the market for digital wound care.

Hospitals & Clinics End-user Segment Dominating in Digital Wound Care Management Systems Market

Hospitals and clinics are the leading end-users in the market for Digital Wound Care Management Systems owing to their large patient loads, presence of skilled medical professionals, and exposure to advanced healthcare technology. These institutions are the major treatment centers for complicated wounds needing regular examination, advanced treatment protocols, and multi-specialty care. Digital solutions for wound care are best suited for hospitals where standardization of documentation, accurate measurement, and evidence-based treatment become vital.

Integration into hospital electronic health records (EHRs) facilitates the uninterrupted flow of information, increasing both patient outcomes and clinical efficiency. Clinics profit in turn from computerized systems by providing services of an outpatient nature to lower the rate of hospital readmissions and allow for ongoing monitoring. Hospital and clinic participation in the use of computerized wound care also assists in regulatory compliance and improves billing accuracy, making these settings favorable for technology uptake.

The following segments are part of an in-depth analysis of the global digital wound care management systems market:

Digital Wound Care Management Systems Market Analysis of Share by Region

North America is projected to hold the largest share of the global Digital Wound Care Management Systems Market over the forecast period.

The Digital Wound Care Management Systems market in North America is expected to lead the marketplace during the forecasting period, attributed to various factors making the region a hub for healthcare progress and the uptake of innovative healthcare technology. The incidence of conditions like diabetic foot wounds and pressure wounds has increased immensely in the region, thanks to the prevalence of chronic conditions like obesity, cardiovascular diseases, and diabetes. There is a large patient population driving the demand for effective, information-driven solutions related to wound care. The region boasts a developed healthcare infrastructure, considerable healthcare spending, and a significant presence of major digital health technology players constantly engaging in technology development.

The region further boasts a widespread awareness among healthcare professionals and patients of the advantages offered by digital wound care solutions, including enhanced monitoring of wounds, shorter healing times, and enhanced patient outcomes. Favorable government policies and reimbursement schemes towards digital health services, particularly in the United States and Canada, further aid the growth of the market. The swift uptake of telemedicine and inclusion of electronic health records (EHRs) further hastened the roll-out of digital wound care solutions. All these factors combined make the region the leading market in the emerging market space.

Digital Wound Care Management Systems Market Analysis - Competition Landscape

The market is competitive, with several established players and new entrants offering a range of single-use endoscope products. Some of the key players include WoundZoom Inc., ARANZ Medical, Smith & Nephew, 3M, ConvaTec, Coloplast, WoundRight, eKare Inc., and others

Global Digital Wound Care Management Systems Market Recent Developments News:

In October 2024, Swift Medical released the Skin & Wound 2 platform, featuring AI technology and FHIR standards compliance. The platform provides submillimeter-accurate wound care assessments and integrates with electronic health records effortlessly.

In March 2024, Swift Medical raised a $4.5 million co-investment from DIGITAL, the Canadian Global Innovation Cluster for digital technologies. The investment funds the roll-out of AI solutions such as SmartTissue, AutoDepth, and HealingIndex to standardize wound care and deliver better outcomes -- and especially better outcomes for diverse skin tones.

In April 2023, Swift Medical entered into the PartnerConnect program of Zebra Technologies as an Independent Software Vendor and paired their wound management solution with Zebra's mobile computers to bring advanced wound care technology to healthcare professionals.

The Global Digital Wound Care Management Systems Market is dominated by a few large companies, such as

WoundZoom Inc.

ARANZ Medical

Smith & Nephew

3M

ConvaTec

Coloplast

WoundRight

eKare Inc.

WoundVision

Medline Industries

HealthTech Solutions

WoundCare Advantage

Mölnlycke Health Care

Carilex Medical

Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

- Global Single Use Endoscope Market Introduction and Market Overview

- Objectives of the Study

- Global Single Use Endoscope Market Scope and Market Estimation

- Global Single Use Endoscope Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Single Use Endoscope Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2033

- Market Segmentation

- Product Type of Global Single Use Endoscope Market

- Application of Global Single Use Endoscope Market

- End-user of Global Single Use Endoscope Market

- Region of Global Single Use Endoscope Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Single Use Endoscope Market

- Key Product/Brand Analysis

- Pricing Analysis

- Technological Advancements

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Single Use Endoscope Market Estimates & Historical Trend Analysis (2021 - 2024)

- Global Single Use Endoscope Market Estimates & Forecast Trend Analysis, by Product Type

- Global Single Use Endoscope Market Revenue (US$ Bn) Estimates and Forecasts, by Product Type, 2021 - 2033

- Flexible Endoscopes

- Bronchoscopes

- Colonoscopes

- Duodenoscopes

- Ureteroscopes

- Cystoscopes

- Rigid Endoscopes

- Laparoscopes

- Arthroscopes

- Sinuscopes

- Capsule Endoscopes

- Robot-assisted Endoscopes

- Global Single Use Endoscope Market Estimates & Forecast Trend Analysis, by Application

- Global Single Use Endoscope Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2033

- Gastrointestinal (GI) Diagnostics

- Pulmonary Procedures

- Urological Procedures

- Gynecological Procedures

- ENT (Ear, Nose, Throat) Procedures

- Orthopedic Procedures

- Others

- Global Single Use Endoscope Market Estimates & Forecast Trend Analysis, by End-user

- Global Single Use Endoscope Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2021 - 2033

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Specialty Clinics

- Diagnostic Imaging Centers

- Global Single Use Endoscope Market Estimates & Forecast Trend Analysis, by region

- Global Single Use Endoscope Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- North America Single Use Endoscope Market: Estimates & Forecast Trend Analysis

- North America Single Use Endoscope Market Assessments & Key Findings

- North America Single Use Endoscope Market Introduction

- North America Single Use Endoscope Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product Type

- By Application

- By End-user

- By Country

- The U.S.

- Canada

- Europe Single Use Endoscope Market: Estimates & Forecast Trend Analysis

- Europe Single Use Endoscope Market Assessments & Key Findings

- Europe Single Use Endoscope Market Introduction

- Europe Single Use Endoscope Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product Type

- By Application

- By End-user

- By Country

- Germany

- Italy

- U.K.

- France

- Spain

- Netherland

- Rest of Europe

- Asia Pacific Single Use Endoscope Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Single Use Endoscope Market Introduction

- Asia Pacific Single Use Endoscope Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product Type

- By Application

- By End-user

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East & Africa Single Use Endoscope Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Single Use Endoscope Market Introduction

- Middle East & Africa Single Use Endoscope Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product Type

- By Application

- By End-user

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Latin America Single Use Endoscope Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Single Use Endoscope Market Introduction

- Latin America Single Use Endoscope Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product Type

- By Application

- By End-user

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Country Wise Market: Introduction

- Competition Landscape

- Global Single Use Endoscope Market Product Mapping

- Global Single Use Endoscope Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Single Use Endoscope Market Tier Structure Analysis

- Global Single Use Endoscope Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

- Ambu A/S

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

* Similar details would be provided for all the players mentioned below

- Boston Scientific Corporation

- Olympus Corporation

- Karl Storz SE & Co. KG

- Fujifilm Holdings Corporation

- Stryker Corporation

- Medtronic plc

- Hoya Corporation (PENTAX Medical)

- Richard Wolf GmbH

- Coloplast A/S

- The Surgical Company Group

- Neoscope Inc.

- Consis Medical

- Prosurg Inc.

- Zhejiang UE Medical Corp.

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables