Distributed Temperature Sensing Market Size and Forecast (2026–2034), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage; Technology (Optical Time Domain Reflectometry (OTDR), Optical Frequency Domain Reflectometry (OFDR), Raman Scattering, Brillouin Scattering), Fiber Type (Single-Mode Fiber, Multimode Fiber), End Use (Oil & Gas, Power & Utilities, Mining, Infrastructure, Others), and Geography

2026-03-10

Semiconductor and Electronics

Ekta Chaurasia (Team Lead)

Description

Distributed Temperature Sensing Market Overview

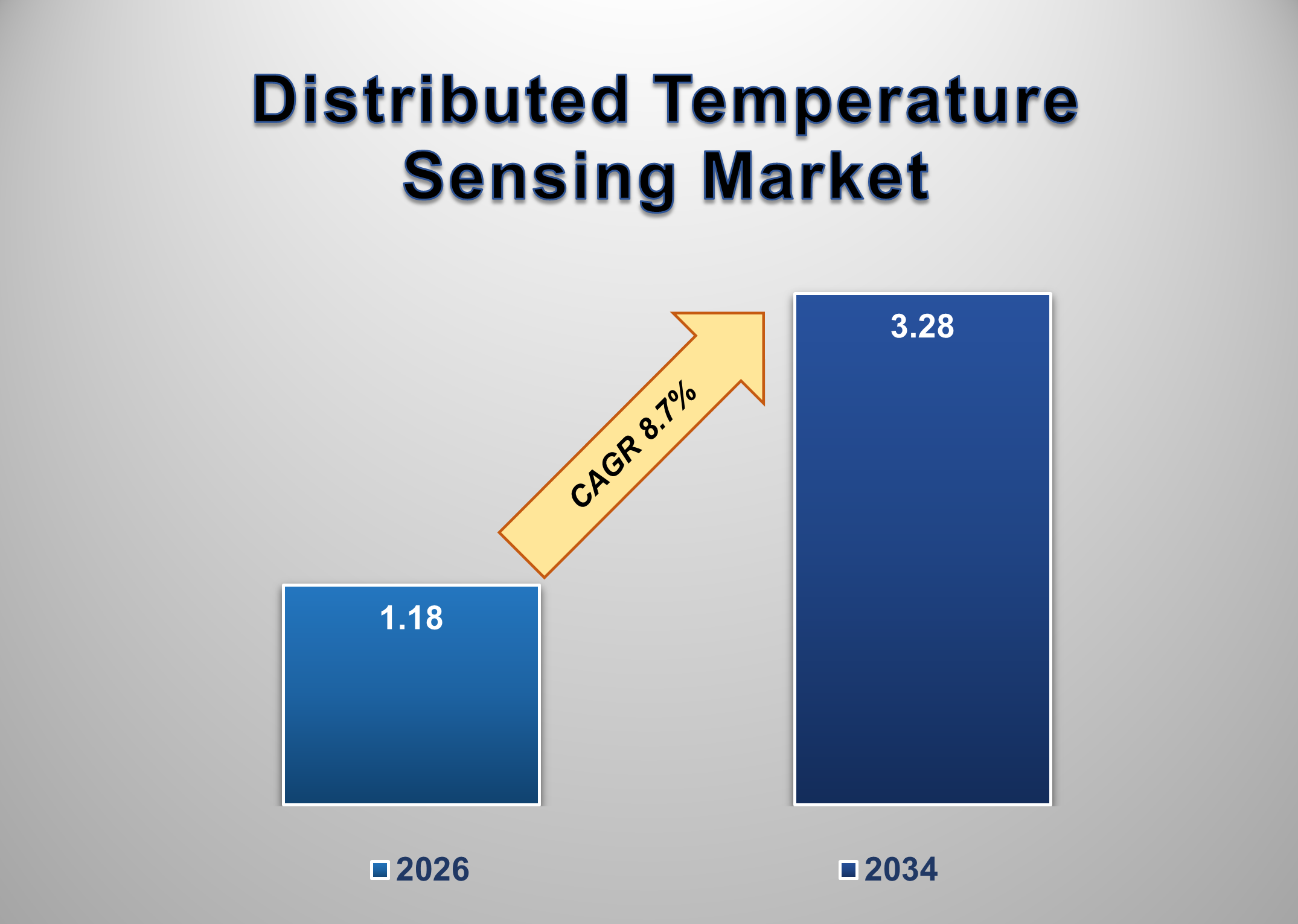

The global distributed temperature sensing (DTS) market is experiencing steady expansion, driven by increasing demand for continuous, real-time temperature monitoring across critical industrial assets. Valued at USD 1.18 billion in 2026, the market is projected to reach USD 3.28 billion by 2034, growing at a CAGR of 8.7% during the forecast period.

Distributed temperature sensing is an advanced fiber-optic sensing technology that enables continuous temperature measurement along the entire length of an optical fiber cable. Unlike conventional point sensors, DTS systems provide real-time temperature profiles over several kilometers, making them highly suitable for monitoring pipelines, power cables, tunnels, and large industrial facilities. The technology primarily relies on backscattered light analysis—such as Raman and Brillouin scattering, to detect temperature variations with high spatial resolution.

The market is strongly influenced by safety, asset integrity, and predictive maintenance requirements in industries where temperature anomalies can indicate potential failures or hazardous conditions. In oil & gas operations, DTS systems are deployed for wellbore monitoring, leak detection, and pipeline surveillance. In power transmission networks, utilities utilize DTS for underground and submarine cable temperature monitoring to prevent overheating and optimize load capacity.

Technological advancements in fiber optics, signal processing, and data analytics have significantly improved sensing accuracy, range, and integration capabilities. Modern DTS systems are increasingly combined with distributed acoustic sensing (DAS) and integrated into digital asset management platforms, enhancing their value proposition within Industry 4.0 environments.

Despite its growth trajectory, the market faces challenges including high installation costs, integration complexity with legacy infrastructure, and the requirement for specialized technical expertise. However, long-term operational benefits such as improved safety, reduced downtime, and enhanced asset lifespan continue to drive adoption.

As industries increasingly prioritize real-time monitoring and risk mitigation, distributed temperature sensing is expected to become a foundational component of advanced industrial sensing and monitoring ecosystems.

Distributed Temperature Sensing Market Drivers and Opportunities

Rising Demand for Asset Integrity Management in Oil & Gas Infrastructure

The oil & gas industry represents one of the most critical application areas for distributed temperature sensing systems. Exploration and production activities involve high-pressure, high-temperature environments where early detection of thermal anomalies is essential to prevent blowouts, leaks, or equipment failure. DTS systems are deployed in downhole environments to monitor well integrity, flow assurance, and reservoir performance. Continuous temperature profiling along pipelines also helps detect leaks, third-party intrusions, and insulation degradation.

In offshore and remote installations, where manual inspections are costly and hazardous, fiber-optic DTS solutions provide a reliable and maintenance-free monitoring alternative. As global energy companies intensify focus on operational safety and regulatory compliance, investments in advanced monitoring technologies such as DTS continue to rise.

Expansion of High-Voltage Power Cable Monitoring and Grid Modernization

Modern power transmission networks are increasingly adopting distributed temperature sensing for dynamic cable rating (DCR) and load optimization. Underground and submarine high-voltage cables are prone to overheating, which can significantly reduce operational lifespan and cause unexpected outages. DTS systems enable utilities to continuously monitor cable temperature profiles, allowing them to operate assets closer to their maximum capacity without compromising safety.

With grid modernization initiatives underway across North America, Europe, and Asia-Pacific, utilities are integrating fiber-optic monitoring systems into smart grid frameworks. Real-time temperature insights allow better load balancing, reduced energy losses, and improved infrastructure resilience. The global transition toward renewable energy and electrification further amplifies the need for advanced cable monitoring solutions.

Integration with Multi-Parameter Fiber-Optic Sensing and Smart Infrastructure Projects

A significant growth opportunity lies in the integration of distributed temperature sensing with multi-parameter fiber-optic systems, including distributed acoustic sensing (DAS) and distributed strain sensing (DSS). Combined sensing platforms enable comprehensive structural health monitoring across tunnels, bridges, rail networks, and industrial facilities.

Smart city and smart infrastructure projects increasingly require continuous environmental and structural monitoring. Fiber-optic cables embedded within civil infrastructure can provide simultaneous temperature, vibration, and strain data, enabling predictive maintenance and risk mitigation. The scalability and immunity of fiber-optic systems to electromagnetic interference make them particularly attractive for large-scale infrastructure deployments.

As urbanization accelerates and governments invest in resilient infrastructure, the integration of DTS within intelligent monitoring frameworks presents a substantial long-term market opportunity.

Distributed Temperature Sensing Market Scope

Distributed Temperature Sensing Market Report Segmentation Analysis

The global distributed temperature sensing market analysis is segmented by Technology, Fiber Type, End Use, and Region.

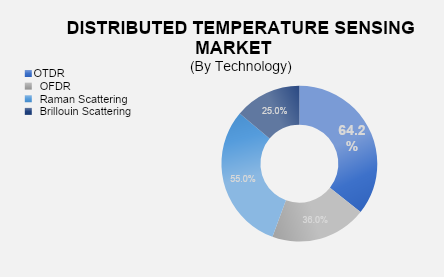

The Raman Scattering segment dominated the market in 2025 and is projected to grow at the highest CAGR during the forecast period.

By technology, the market includes OTDR, OFDR, Raman scattering, and Brillouin scattering techniques. Raman-based DTS systems account for the largest share due to their high temperature sensitivity and widespread deployment in industrial monitoring applications. Raman scattering technology measures temperature by analyzing intensity variations in backscattered light, offering accurate and stable measurements over long distances. Its reliability, scalability, and suitability for harsh environments have made it the preferred choice in oil & gas and power utility applications.

End Use Segment Analysis

The Oil & Gas segment holds the largest share of the end-use segment over the forecast period. Oil & gas operators utilize distributed temperature sensing for downhole monitoring, pipeline integrity management, and leak detection. Continuous temperature profiling enhances reservoir management, identifies flow irregularities, and reduces operational risks. Offshore platforms and long-distance pipelines particularly benefit from DTS deployment due to the reduced need for manual inspections and improved remote monitoring capabilities. As global energy production expands and safety regulations tighten, DTS adoption within oil & gas operations is expected to remain strong.

Distributed Temperature Sensing Market Share Analysis by Region

North America is projected to hold a significant share of the global distributed temperature sensing market over the forecast period.

The region’s dominance is attributed to extensive oil & gas infrastructure, advanced power transmission networks, and early adoption of smart grid technologies. The United States leads the market due to strong investment in shale exploration, pipeline safety monitoring, and utility modernization projects. Additionally, technological innovation and the presence of major fiber-optic sensing solution providers further support regional growth.

Distributed Temperature Sensing Market Recent Developments News

In February 2024, Schlumberger introduced an advanced fiber-optic sensing solution designed to enhance downhole temperature monitoring and reservoir analysis capabilities.

In August 2025, Halliburton expanded its distributed fiber-optic sensing portfolio to support integrated well monitoring solutions in offshore drilling operations.

In November 2025, AP Sensing launched a next-generation Raman-based DTS system optimized for high-voltage cable monitoring and smart grid applications.

Competitive Landscape

The Global Distributed Temperature Sensing Market is dominated by a few large companies, such as

Halliburton Company

Schlumberger Limited

AP Sensing GmbH

Silixa Ltd.

Luna Innovations Incorporated

Bandweaver Technologies Ltd.

Yokogawa Electric Corporation

Omnisens SA

Weatherford International plc

Fotech Solutions Ltd.

Sumitomo Electric Industries, Ltd.

Baker Hughes Company

OFS Fitel, LLC

VIAVI Solutions Inc.

NKT Photonics A/S

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

Distributed Temperature Sensing Market

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables