Dog Food and Snacks Market Size and Forecast (2020–2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product Type (Dry Food, Wet Food, Treats & Snacks, Frozen/Freeze-Dried, Veterinary Diets), By Distribution Channel (Specialty Stores, Supermarkets/Hypermarkets, Online Retail, Veterinary Clinics), By Life Stage (Puppy, Adult, Senior), By Source (Animal-Derived, Plant-Derived, Insect-Based), and Geography

2025-12-19

Consumer Products

Jaya Bundele (Research Analyst)

Description

Dog Food and

Snacks Market Overview

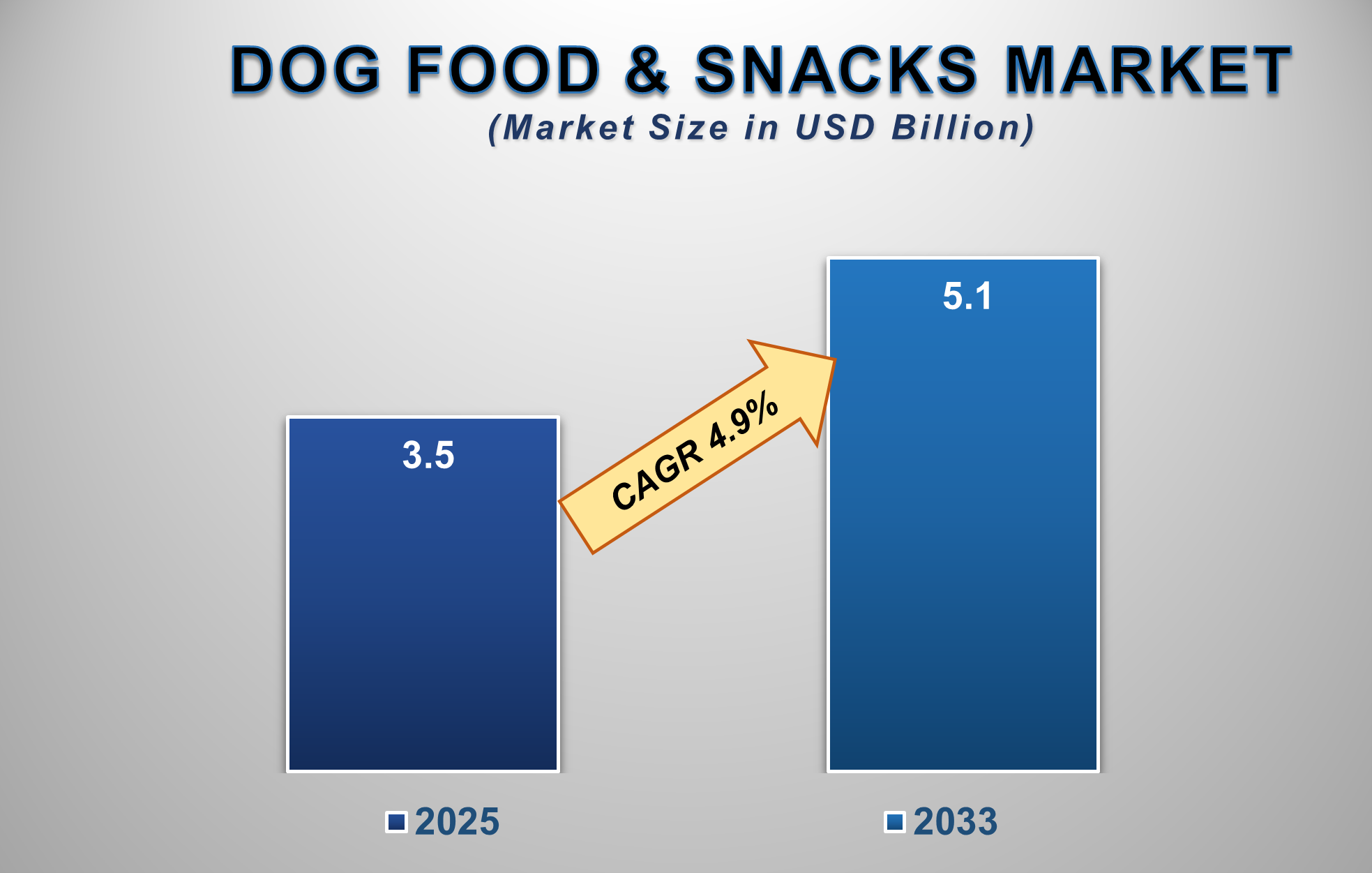

The Dog Food and Snacks Market is poised for robust growth between 2025 and 2033, fueled by the global rise in pet humanization, increasing pet ownership, and growing consumer focus on pet health and nutrition. The market is expected to be valued at USD 3.5 billion in 2025 and is projected to reach USD 5.1 billion by 2033, registering a CAGR of 4.9% during the forecast period.

The market has evolved from basic sustenance to a

sophisticated industry centered on health, wellness, and premiumization. Dog

owners are increasingly seeking out products with high-quality, natural

ingredients, functional benefits (such as joint support, skin & coat

health, and weight management), and tailored formulations. The trend of

"humanization" drives demand for gourmet snacks, subscription boxes,

and fresh/refrigerated meals. Innovations in alternative proteins (like insect,

plant-based, and lab-cultured) and sustainable packaging are reshaping the

landscape. North America remains the largest market due to high pet spending

and premiumization trends, while the Asia-Pacific region is witnessing explosive growth driven by rising disposable

incomes, urbanization, and a growing middle-class pet-owning population.

Dog Food and Snacks Market Drivers and

Opportunities

The Humanization of Pets

and Premiumization of Diets Is the Primary Market Driver

The most influential driver is the trend of pet

humanization, where pets are considered integral family members. This shift in

perception leads owners to prioritize high-quality nutrition, mirroring their

own health and wellness concerns. Demand is soaring for premium and

super-premium products featuring human-grade ingredients, grain-free recipes,

limited-ingredient diets (LID), and functional ingredients like probiotics,

omega fatty acids, and glucosamine. The rising incidence of pet obesity and

allergies is also pushing demand for specialized therapeutic and weight

management foods, often recommended by veterinarians. Furthermore, the desire

for convenience and personalized care is fueling growth in subscription-based

and direct-to-consumer (DTC) meal delivery services for pets.

The number of dog owners in the United States has seen a

significant and sustained increase over the past decade, solidifying the

nation's status as a pet-loving society. Following a notable surge during the

COVID-19 pandemic, growth has stabilized at a high level. According to the

American Pet Products Association (APPA), an estimated 65.1 million U.S.

households owned a dog in 2023-2024, representing approximately 50% of all

households. This marks a steady climb from roughly 63 million households in

2018. The total population of pet dogs is estimated at 77 million. This

growth is propelled by several key demographic shifts, including rising

millennial and Gen Z ownership groups that often prioritize pet parenting

before having children. Furthermore, increased adoption from shelters and

rescues, greater acceptance of pets in rental housing and workplaces, and the

continued cultural trend of pet humanization have all contributed to expanding

the base of dog owners. The financial commitment mirrors this rise, with total

U.S. pet industry expenditure soaring to over US$147 billion in 2023, a

substantial portion dedicated to dog food, treats, healthcare, and services,

underscoring the profound economic impact of this growing owner population.

E-commerce Expansion and Digital Influence Are Accelerating

Market Adoption

The rapid growth of online retail is fundamentally changing

how pet food is purchased. The convenience of home delivery, access to a wider

variety of niche brands, subscription models, and detailed product information

online are major growth catalysts. Social media platforms and "pet

influencers" on Instagram, TikTok, and YouTube play a significant role in

product discovery, reviews, and shaping consumer preferences. Digital

marketing, including targeted ads and influencer partnerships, is crucial for

brand building. Online platforms also facilitate the growth of

direct-to-consumer (DTC) brands that bypass traditional retail, offering

personalized nutrition plans and building strong community engagement with pet

owners.

Innovation in Ingredients, Sustainability, and Personalized

Nutrition Presents Significant Opportunities

Continuous innovation in product formulations and sourcing

is a major opportunity for market differentiation. The advent of novel protein

sources such as insect-based protein

(sustainable and hypoallergenic), plant-based options, and cultured meat

caters to environmental concerns and specific dietary

needs. Sustainability is a key differentiator, with opportunities in

eco-friendly packaging, carbon-neutral production, and ethically sourced

ingredients. The integration of technology, such as AI-driven nutritional apps,

DNA-based diet plans, and smart feeders that monitor intake, allows for

hyper-personalized pet nutrition. The growing focus on pet mental well-being

and longevity also opens avenues for products containing nootropics,

adaptogens, and advanced life-stage-specific

formulations. For manufacturers, opportunities lie in expanding into veterinary

therapeutic diets, creating functional treats

for training and dental health, and creating integrated pet wellness

ecosystems.

Dog Food and Snacks Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 3.5 Billion |

|

Market Forecast in 2033 |

USD 5.1 Billion |

|

CAGR % 2025-2033 |

4.9% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Service Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Product Type ●

By Life Stage ●

By Source ●

By Distribution

Channel |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Dog Food and Snacks Market Report Segmentation

Analysis

The

global Medica Spa Market is segmented by Product Type, Life Stage, Source,

Distribution Channel, and Region.

Dry Food Is Anticipated

to Command the Largest Market Share in 2025

Dry food (kibble) dominates the Product Type segment due to its convenience, cost-effectiveness, long shelf life, and dental health benefits. Its market leadership is anchored in high household penetration and being the staple diet for most dogs globally. Continuous innovation, such as the inclusion of freeze-dried raw coatings, functional kibble shapes, and breed-specific formulas, keeps this segment dynamic. The strong presence of global giants and private-label offerings in supermarkets ensures wide availability. While wet food and fresh options are growing faster in terms of premiumization, dry food's unbeatable value and versatility secure its leading position, especially in price-sensitive and emerging markets.

The Online Retail Segment

Is the Fastest-Growing Distribution Channel

Online

retail is the fastest-growing distribution channel, revolutionizing market

access. The convenience of subscription models, access to niche and premium

brands not available in local stores, competitive pricing, and

auto-replenishment features are key growth drivers. The COVID-19 pandemic

accelerated this shift, establishing online purchasing as a habitual channel

for pet owners. Direct-to-consumer (DTC) brands leverage this channel to build

direct relationships, offer personalized nutrition, and gather valuable

consumer data. While specialty pet stores and supermarkets remain significant

for immediate needs and in-person consultation, the growth trajectory of online

retail is unmatched, making it the most disruptive and opportunistic channel.

The following segments are

part of an in-depth analysis of the global Dog Food and Snacks Market:

|

Market

Segments |

|

|

By Product

Type |

●

Dry Food ●

Wet Food ●

Treats & Snacks ●

Frozen/Freeze-Dried ●

Veterinary Diets |

|

By Life Stage |

●

Puppy ●

Adult ●

Senior |

|

By Distribution Channel |

●

Specialty Stores ●

Supermarkets/Hypermarkets ●

Online Retail ●

Veterinary Clinics |

|

By Source |

●

Animal-Derived ●

Plant-Derived ●

Insect-Based |

Dog Food and

Snacks Market Share Analysis by Region

North America is

anticipated to hold the largest portion of the Dog Food and Snacks Market

globally throughout the forecast period.

North

America's leadership is driven by the highest rate of pet ownership, extreme

pet humanization trends, strong consumer spending power, and a mature retail

landscape. The United States is the single largest market, characterized by a

high willingness to spend on premium, natural, and functional products. The

region is a hub for innovation, with numerous startups and established players

constantly launching new products. Europe follows closely, with a strong

emphasis on regulatory standards, organic ingredients, and sustainability.

However, the Asia-Pacific region is the fastest-growing, fueled by rapid

urbanization, a growing middle class, declining birth rates leading to

increased pet adoption ("pet parenting"), and the Westernization of

pet care trends in countries like China, Japan, and India.

Dog Food and Snacks Market Competition Landscape

Analysis

The global market is

semi-consolidated, with a mix of multinational conglomerates, large

private-label manufacturers, and a rapidly growing number of niche,

direct-to-consumer startups. Competition centers on brand trust, ingredient

quality, scientific backing (veterinary endorsements), price, and marketing

reach. Leading players are actively acquiring niche brands to tap into premium

segments and gain innovation capabilities. Investment in sustainable practices

and transparent supply chains is becoming a key competitive differentiator.

Digital marketing, influencer partnerships, and robust e-commerce strategies

are critical for success. Private-label offerings from major retailers are also

intensifying price competition in the mass-market segment.

Global Dog Food and Snacks Market Recent Developments News:

- In January 2025, Mars Petcare launched a new line of

veterinary-prescription wellness diets available through a

direct-to-consumer platform with telehealth vet consultations.

- In October 2024, Nestlé Purina PetCare expanded its Beyond Nature's

Protein line into Europe, featuring insect-based protein as a primary

ingredient.

- In August 2024, Freshpet announced a major capacity expansion of its

kitchens to meet soaring demand for fresh, refrigerated pet food across

North America.

- In May 2024, The Honest Company entered the pet care space with a

line of organic, sustainably packaged dog treats and supplements.

The Global Dog Food and Snacks Market Is

Dominated by a Few Large Companies, such as

●

Mars, Incorporated

●

Nestlé Purina

●

Hill’s Pet Nutrition

●

The J.M. Smucker

Company

●

General Mills

●

Diamond Pet Foods

●

Spectrum Brands

●

Lupus Alimentos

●

Heristo AG

●

Total Alimentos

●

Unicharm Corporation

●

Mogina Alimentos

●

Bridge Petcare

●

Yantai China Pet Foods

Co., Ltd.

●

Freshpet

●

Other Prominent

Players

FAQs

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Dog Food and Snacks

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Dog Food and Snacks Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Dog Food and Snacks

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product Type of Global Dog

Food and Snacks Market

1.3.2.Life Stage of Global Dog

Food and Snacks Market

1.3.3.Source of Global Dog Food

and Snacks Market

1.3.4.Distribution Channel of Global

Dog Food and Snacks Market

1.3.5.Region of Global Dog Food

and Snacks Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Market

Entry Strategies

2.7.

Market

Dynamics

2.7.1.Drivers

2.7.2.Limitations

2.7.3.Opportunities

2.7.4.Impact Analysis of Drivers

and Restraints

2.8.

Porter’s

Five Forces Analysis

2.9.

Pricing

Analysis

2.10.

PEST

Analysis

3. Global

Dog Food and Snacks Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Dog Food and Snacks Market Estimates

& Forecast Trend Analysis, by Product Type

4.1.

Global

Dog Food and Snacks Market Revenue (US$ Bn) Estimates and Forecasts, by Product

Type, 2020 - 2033

4.1.1.Dry Food

4.1.2.Wet Food

4.1.3.Treats & Snacks

4.1.4.Frozen/Freeze-Dried

4.1.5.Veterinary Diets

5. Global

Dog Food and Snacks Market Estimates

& Forecast Trend Analysis, by Life Stage

5.1.

Global

Dog Food and Snacks Market Revenue (US$ Bn) Estimates and Forecasts, by Life

Stage, 2020 - 2033

5.1.1.Puppy

5.1.2.Adult

5.1.3.Senior

6. Global

Dog Food and Snacks Market Estimates

& Forecast Trend Analysis, by Source

6.1.

Global

Dog Food and Snacks Market Revenue (US$ Bn) Estimates and Forecasts, by Source

2020 - 2033

6.1.1.Animal-Derived

6.1.2.Plant-Derived

6.1.3.Insect-Based

7. Global

Dog Food and Snacks Market Estimates

& Forecast Trend Analysis, by Distribution Channel

7.1.

Global

Dog Food and Snacks Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution

Channel 2020 - 2033

7.1.1.Specialty Stores

7.1.2.Supermarkets/Hypermarkets

7.1.3.Online Retail

7.1.4.Veterinary Clinics

8. Global

Dog Food and Snacks Market Estimates

& Forecast Trend Analysis, by region

8.1.

Global

Dog Food and Snacks Market Revenue (US$ Bn) Estimates and Forecasts, by region,

2020 - 2033

8.1.1.North America

8.1.2.Europe

8.1.3.Asia Pacific

8.1.4.Middle East & Africa

8.1.5.Latin America

9. North America Dog

Food and Snacks Market: Estimates &

Forecast Trend Analysis

9.1.

North

America Dog Food and Snacks Market Assessments & Key Findings

9.1.1.North America Dog Food and

Snacks Market Introduction

9.1.2.North America Dog Food and

Snacks Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product

Type

9.1.2.2. By Life Stage

9.1.2.3. By Distribution

Channel

9.1.2.4. By Source

9.1.2.5.

By

Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Dog

Food and Snacks Market: Estimates &

Forecast Trend Analysis

10.1.

Europe

Dog Food and Snacks Market Assessments & Key Findings

10.1.1.

Europe

Dog Food and Snacks Market Introduction

10.1.2.

Europe

Dog Food and Snacks Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Product

Type

10.1.2.2. By Life Stage

10.1.2.3. By Distribution

Channel

10.1.2.4. By Source

10.1.2.5.

By

Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7. Rest

of Europe

11. Asia Pacific Dog

Food and Snacks Market: Estimates &

Forecast Trend Analysis

11.1.

Asia

Pacific Market Assessments & Key Findings

11.1.1.

Asia

Pacific Dog Food and Snacks Market Introduction

11.1.2.

Asia

Pacific Dog Food and Snacks Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

11.1.2.1. By Product

Type

11.1.2.2. By Life Stage

11.1.2.3. By Distribution

Channel

11.1.2.4. By Source

11.1.2.5.

By

Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Dog

Food and Snacks Market: Estimates &

Forecast Trend Analysis

12.1.

Middle

East & Africa Market Assessments & Key Findings

12.1.1.

Middle East & Africa Dog Food and Snacks Market

Introduction

12.1.2.

Middle East & Africa Dog Food and Snacks Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1. By Product

Type

12.1.2.2. By Life Stage

12.1.2.3. By Distribution

Channel

12.1.2.4. By End User

12.1.2.5.

By

Country

12.1.2.5.1. UAE

12.1.2.5.2. Saudi

Arabia

12.1.2.5.3. South

Africa

12.1.2.5.4. Rest

of MEA

13. Latin America

Dog Food and Snacks Market: Estimates

& Forecast Trend Analysis

13.1.

Latin

America Market Assessments & Key Findings

13.1.1.

Latin

America Dog Food and Snacks Market Introduction

13.1.2.

Latin

America Dog Food and Snacks Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

13.1.2.1. By Product

Type

13.1.2.2. By Life Stage

13.1.2.3. By Distribution

Channel

13.1.2.4. By Source

13.1.2.5.

By

Country

13.1.2.5.1. Brazil

13.1.2.5.2. Argentina

13.1.2.5.3. Mexico

13.1.2.5.4. Rest

of LATAM

14. Country Wise Market:

Introduction

15.

Competition

Landscape

15.1.

Global

Dog Food and Snacks Market Product Mapping

15.2.

Global

Dog Food and Snacks Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

15.3.

Global

Dog Food and Snacks Market Tier Structure Analysis

15.4.

Global

Dog Food and Snacks Market Concentration & Company Market Shares (%)

Analysis, 2024

16.

Company

Profiles

16.1.

Mars, Incorporated

16.1.1.

Company

Overview & Key Stats

16.1.2.

Financial

Performance & KPIs

16.1.3.

Product

Portfolio

16.1.4.

SWOT

Analysis

16.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

16.2. Nestlé Purina

16.3. Hill’s Pet

Nutrition

16.4. The J.M.

Smucker Company

16.5. General Mills

16.6. Diamond Pet

Foods

16.7. Spectrum

Brands

16.8. Lupus

Alimentos

16.9. Heristo AG

16.10. Total

Alimentos

16.11. Unicharm

Corporation

16.12. Mogina

Alimentos

16.13. Bridge

Petcare

16.14. Yantai China

Pet Foods Co., Ltd.

16.15. Freshpet

16.16. Other

Prominent Players

17. Research

Methodology

17.1.

External

Transportations / Databases

17.2.

Internal

Proprietary Database

17.3.

Primary

Research

17.4.

Secondary

Research

17.5.

Assumptions

17.6.

Limitations

17.7.

Report

FAQs

18. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables