Drip Irrigation Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Component (Drip Tubing/Drip Lines, Emitters/Drippers, Valves, Fertigation Systems, Filters, Others), By Method (Surface, Subsurface), By Crop (Field Crops, Fruits & Nuts, Vegetable Crops, Others), and Geography

2026-01-02

Agriculture Industry

Jaya Bundele (Research Analyst)

Description

Drip Irrigation Market Overview

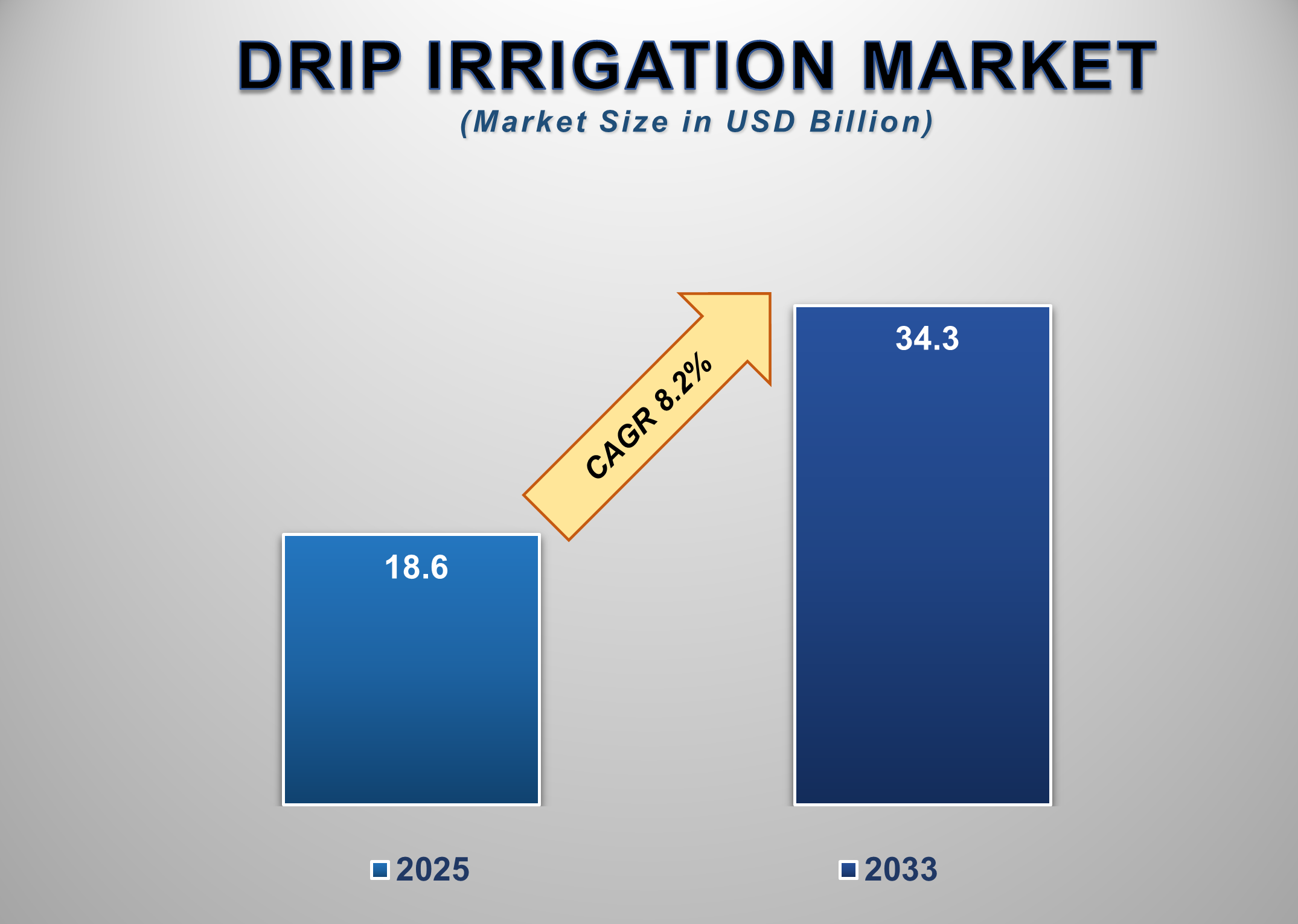

The Global Drip Irrigation Market is witnessing significant expansion as water scarcity, climate variability, and sustainable farming practices accelerate the global shift toward precision agriculture. Valued at USD 18.6 billion in 2025, the market is projected to reach USD 34.3 billion by 2033, registering a strong CAGR of 8.2%. Drip irrigation systems offer substantial water savings—up to 60%—compared with traditional flood irrigation while improving nutrient efficiency, crop yield, and soil health across diverse crop bases such as field crops, fruits, nuts, vegetables, and horticultural plantations. Rising pressure to increase agricultural productivity from shrinking arable land and escalating global food demand further strengthens adoption.

Government irrigation modernization schemes, especially across India, China, Israel, and the United States, play a vital role in subsidizing drip systems for small and large farms alike. Manufacturers are focusing on automation, smart irrigation controllers, and IoT-enabled fertigation to elevate system efficiency. As climate challenges intensify, drip irrigation is no longer limited to high-value crops but is rapidly penetrating broadacre farms, making it one of the most essential components of precision agriculture worldwide.

Drip Irrigation Market

Drivers and Opportunities

Rising Global Water

Stress and Sustainable Farming Needs Are Driving Growth in the Drip Irrigation

Market

Increasing global water

scarcity is one of the central forces propelling the adoption of drip

irrigation systems across developed and emerging economies. Many regions,

particularly Asia and the Middle East, face severe groundwater depletion,

irregular rainfall, and rising competition for water across residential,

industrial, and agricultural sectors. Because agriculture accounts for nearly

70% of total freshwater withdrawals globally, governments and farmers are under

growing pressure to adopt techniques that minimize wastage while sustaining

crop productivity. Drip irrigation’s ability to deliver water directly to the

root zone with minimal losses due to runoff or evaporation makes it the

preferred solution for resource-stressed agricultural regions. The efficiency

gains, often exceeding 90%, are far superior to traditional furrow or sprinkler

systems, enabling farmers to achieve higher yields per drop of water. Water-use

regulations and subsidy programs are expanding rapidly. Large-scale initiatives

such as India’s Per Drop More Crop scheme, Israel’s precision irrigation

programs, and U.S. NRCS incentives strongly encourage farmers to transition to

drip systems. With climate change intensifying drought cycles, irrigation

modernization has become a strategic global priority, making drip systems

indispensable for long-term agricultural resilience and food security.

Growing Demand for High-Value Crops and Precision Farming

Technologies Is Accelerating Market Expansion

The increasing cultivation of fruits, nuts, vegetables, and other

high-value crops is significantly boosting the demand for drip irrigation,

which ensures precise nutrient delivery and maximized yield quality. Modern

consumers are demanding premium produce, organic farm output, and consistent

supply throughout the year—factors that incentivize farmers to adopt controlled

irrigation technologies. Drip systems provide uniform moisture distribution,

resulting in improved crop size, reduced disease incidence, and optimized input

usage. These advantages make them ideal for horticultural crops, vineyards,

orchards, and greenhouse cultivation, where quality and consistency are

critical. Simultaneously, the rapid adoption of precision agriculture

technologies such as IoT-based field monitoring, soil moisture sensors,

automated fertigation controllers, and AI-based irrigation scheduling is

elevating the performance and attractiveness of drip irrigation systems.

Integrating sensors and smart valves ensures that water is applied only when

necessary, reducing labor dependency and operational costs. Market leaders are

increasingly designing modular, plug-and-play drip systems tailored to

smallholders as well as large commercial farms. As global agriculture

transitions toward data-driven production, drip irrigation is becoming a

foundational pillar supporting the modernization of farming practices

worldwide.

Government Subsidies and Expanding Adoption Across Emerging

Economies Are Creating Robust Growth Opportunities

Emerging economies, especially across Asia-Pacific, Latin America,

and Africa, represent substantial growth opportunities due to rapid

agricultural expansion, rising food demand, and increasing acceptance of

micro-irrigation. Governments in India, China, Indonesia, Brazil, and Mexico

are aggressively promoting drip irrigation through financial incentives, tax

benefits, and public–private partnerships that lower upfront installation

costs. As small- and medium-scale farmers gain access to affordable micro-irrigation

systems, penetration rates across field crops traditionally considered less

suitable for drip are rising sharply. Technological advancements are opening

new opportunities as low-cost drip lines, gravity-fed systems, solar-powered

pumps, and portable fertigation units become widely available. These

innovations make drip irrigation feasible even in remote areas without stable

electricity access. Furthermore, climate adaptation programs by global

organizations, including the World Bank, FAO, and UNDP, are increasingly

funding drip irrigation projects as part of climate-smart agriculture

initiatives. With APAC projected to grow at the highest CAGR through 2033 and

Africa showing early acceleration, the market is positioned for the long term.

Drip Irrigation Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 18.6 Billion |

|

Market Forecast in 2033 |

USD 34.3 Billion |

|

CAGR % 2025-2033 |

8.2% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

by Component,

Method, and Crop |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Drip Irrigation Market

Report Segmentation Analysis

The Drip Irrigation Market is segmented based on Component,

Method, Crop, and Geography.

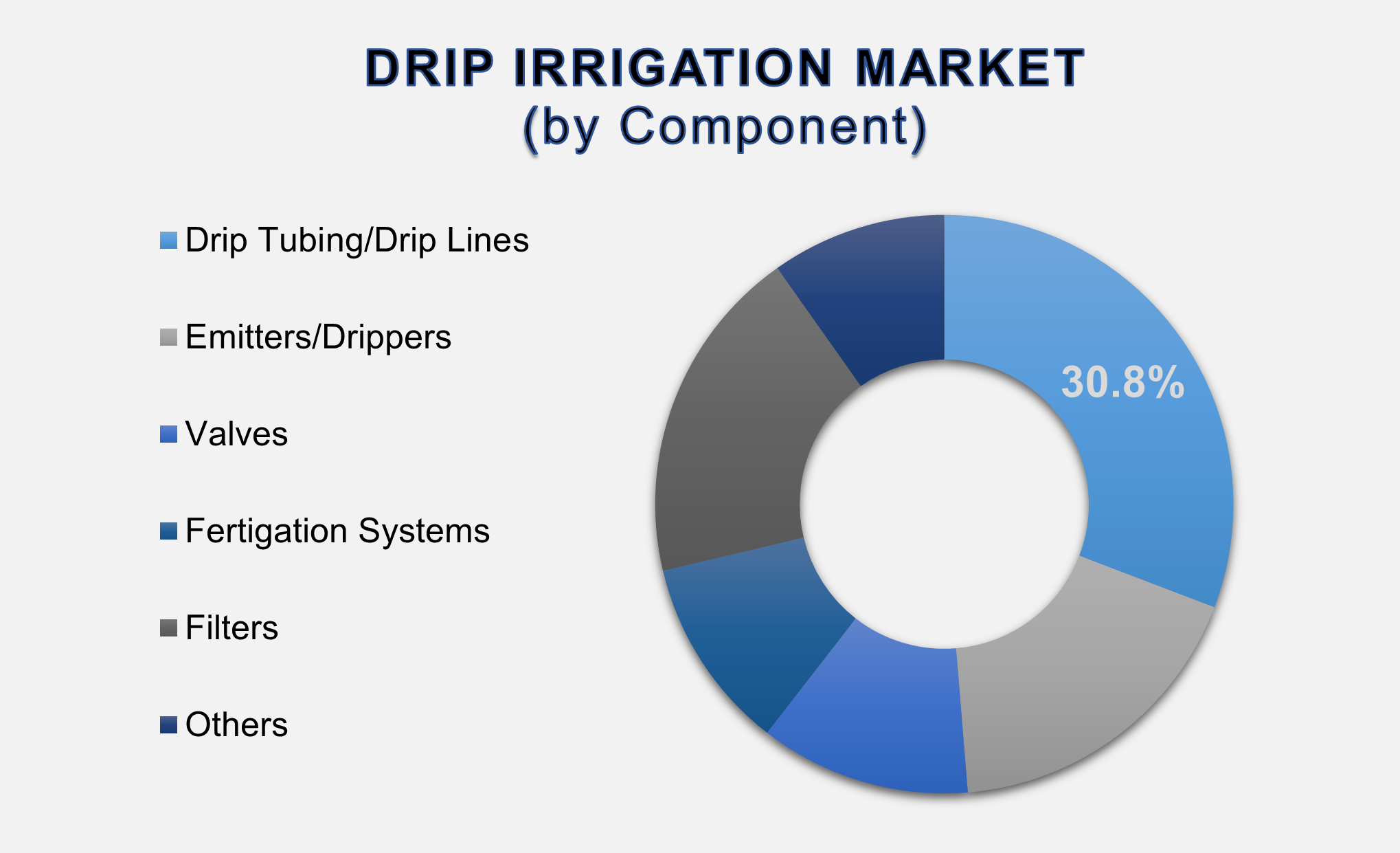

Drip Tubing/Drip Lines

Segment Accounted for the Largest Market Share in the Global Drip Irrigation

Market

The Drip Tubing/Drip Lines segment, accounting for 30.8% of the global market, represents the largest share due to its core role in water delivery within irrigation systems. Drip lines form the backbone of system infrastructure, enabling precise water discharge directly to plant roots. Their high usage across field crops, orchards, vineyards, and vegetable cultivation makes them indispensable in both surface and subsurface applications. Advancements in durable polyethylene tubing, pressure-compensated drip lines, and multi-season reusable systems have significantly enhanced product performance and longevity. Drip lines are particularly important in large-scale farming operations where uniform water distribution is critical to achieving consistent crop quality. Moreover, farmers increasingly prefer advanced drip tubing due to its compatibility with automation technologies and fertigation systems, allowing efficient nutrient delivery and improved crop management. As demand for high-efficiency irrigation grows, the drip tubing/drip lines segment will continue to dominate the market.

Surface Method Segment

Accounted for the Largest Market Share in the Global Drip Irrigation Market

The Surface drip irrigation

method holds the largest market share due to its widespread adoption across a

variety of crops and farming conditions. Surface systems are easier to install,

require lower initial investment, and offer high versatility, making them ideal

for smallholder farmers as well as large commercial operations. This method is

commonly used for vegetable crops, field crops, and horticulture applications

where above-ground placement enables easy maintenance, inspection, and seasonal

adjustments. Surface drip systems are particularly valuable in regions with

labor constraints and limited technical training, as they are simpler to manage

compared to subsurface alternatives. Additionally, the method supports

flexibility in crop rotation, a key requirement in diversified agriculture.

With expanding government support programs encouraging micro-irrigation

adoption and growing awareness of water-saving technologies, the surface method

is expected to maintain its dominant position in the market over the forecast

period.

The Field Crops Segment

Accounted for the Largest Market Share in the Global Drip Irrigation Market

The Field Crops segment leads the

market, driven by the increasing use of drip irrigation in crops such as

cotton, sugarcane, maize, soybean, and pulses. Traditionally reliant on flood

irrigation, field crop cultivation is now shifting toward drip systems due to

mounting water scarcity concerns and rising pressure to improve yield

efficiency. Drip irrigation helps farmers achieve significant water savings

while enhancing fertilizer uptake, translating into higher productivity and

profitability. Governments worldwide are actively promoting micro-irrigation

adoption in field crops through subsidies, especially in regions where crop

production contributes significantly to GDP. In India, China, the U.S., and

Brazil, drip adoption in large-acreage crops is expanding rapidly due to

mechanized installation technologies and improved affordability. As global

demand for food increases and arable land expansion becomes limited, the need

to maximize output per hectare will continue to propel drip irrigation adoption

in field crops.

The following segments are

part of an in-depth analysis of the global Drip Irrigation market:

|

Market Segments |

|

|

By Component |

●

Drip Tubing/Drip

Lines ●

Emitters/Drippers ●

Valves ●

Fertigation Systems ●

Filters ●

Others |

|

By Method |

●

Surface ●

Subsurface |

|

By Crop |

●

Field Crops ●

Fruits and Nuts ●

Vegetable Crops ●

Others |

Drip Irrigation Market

Share Analysis by Region

North America is

anticipated to hold the biggest portion of the Drip Irrigation Market globally

throughout the forecast period.

North America dominates the

Global Drip Irrigation Market, holding 41.1% of total revenue in 2025. The

region benefits from advanced agricultural practices, early adoption of

precision irrigation technologies, and significant investment in farm modernization.

U.S. growers increasingly rely on drip systems for high-value fruit, nut, and

vegetable crops, driven by stringent water-use regulations and the ongoing

megadrought affecting major agricultural states such as California. The strong

presence of leading irrigation companies, extensive R&D activities, and

favorable government programs are further strengthening market penetration.

Canada and Mexico also contribute significantly, with expanding horticulture

industries and rising demand for export-quality produce.

Meanwhile, the Asia-Pacific is

expected to be the fastest-growing region during the forecast period. Rapid

population growth, increasing food demand, and severe water scarcity are

fueling accelerated adoption of drip irrigation in India, China, and Southeast

Asia. Massive government subsidy programs and rising mechanization in emerging

economies are catalyzing large-scale adoption. Europe, Latin America, and the

Middle East are also important contributors, driven by greenhouse expansion and

water conservation initiatives. Overall, regional trends reflect strong global

momentum toward high-efficiency irrigation technologies.

Drip Irrigation Market

Competition Landscape Analysis

The Global Drip Irrigation Market

is highly competitive, with companies focusing on product innovation,

automation technologies, distribution expansion, and strategic partnerships.

Leading players such as NETAFIM, Rain Bird Corporation, Rivulis, The Toro

Company, Jain Irrigation Systems Ltd., Irritec S.p.A., Antelco, and others

continue to invest heavily in advanced filtration systems, smart controllers,

and precision fertigation units.

Global Drip Irrigation

Market Recent Developments News:

- In November 2024,

Netafim Italia acquired Tecnir S.r.l., a Faenza-based specialist in

irrigation system design and installation. This acquisition strengthens

Netafim's precision irrigation portfolio in Italy, combining local

expertise with global innovation to advance sustainable water management

for agricultural customers.

- In March 2024,

Hunter Industries Inc. launched updated HE and HEB Point-Source Emitters

in earth-tone colors for discreet landscape integration. The emitters

offer multiple flow rates and connection options, featuring color-coded

identification, coined edges for easy installation, and an optional

anti-clogging diffuser cap to prevent soil erosion.

The Global Drip Irrigation Market Is Dominated by a Few Large Companies, such as

●

ARKA

●

Antelco

●

Amiad Water Systems

Ltd.

●

AZUD

●

Chinadrip Irrigation

Equipment (Xiamen) Co., Ltd.

●

HUNTER INDUSTRIES INC.

●

Irritec S.p.A

●

Jain Irrigation

Systems Ltd.

●

Metzer

●

STF

●

NETAFIM

●

Rain Bird Corporation

●

Rivulis

●

The Toro Company

● Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Drip Irrigation

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Drip Irrigation Market Scope and Market Estimation

1.2.1.Global Drip Irrigation Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Drip Irrigation

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Material of Global Drip

Irrigation Market

1.3.2.Method of Global Drip

Irrigation Market

1.3.3.Crop of Global Drip

Irrigation Market

1.3.4.Region of Global Drip

Irrigation Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Drip Irrigation Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Drip Irrigation Market Estimates

& Forecast Trend Analysis, by Material

4.1.

Global

Drip Irrigation Market Revenue (US$ Bn) Estimates and Forecasts, by Material, 2020

- 2033

4.1.1.Drip Tubing/Drip Lines

4.1.2.Emitters/Drippers

4.1.3.Valves

4.1.4.Fertigation Systems

4.1.5.Filters

4.1.6.Others

5. Global

Drip Irrigation Market Estimates

& Forecast Trend Analysis, by Method

5.1.

Global

Drip Irrigation Market Revenue (US$ Bn) Estimates and Forecasts, by Method,

2020 - 2033

5.1.1.Surface

5.1.2.Subsurface

6. Global

Drip Irrigation Market Estimates

& Forecast Trend Analysis, by Crop

6.1.

Global

Drip Irrigation Market Revenue (US$ Bn) Estimates and Forecasts, by Crop, 2020

- 2033

6.1.1.Field Crops

6.1.2.Fruits and Nuts

6.1.3.Vegetable Crops

6.1.4.Others

7. Global

Drip Irrigation Market Estimates

& Forecast Trend Analysis, by Region

7.1.

Global

Drip Irrigation Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020

- 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Drip

Irrigation Market: Estimates &

Forecast Trend Analysis

8.1.

North

America Drip Irrigation Market Assessments & Key Findings

8.1.1.North America Drip

Irrigation Market Introduction

8.1.2.North America Drip

Irrigation Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Material

8.1.2.2. By Method

8.1.2.3. By Crop

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Drip

Irrigation Market: Estimates &

Forecast Trend Analysis

9.1.

Europe

Drip Irrigation Market Assessments & Key Findings

9.1.1.Europe Drip Irrigation

Market Introduction

9.1.2.Europe Drip Irrigation

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Material

9.1.2.2. By Method

9.1.2.3. By Crop

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Drip

Irrigation Market: Estimates &

Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Drip Irrigation Market Introduction

10.1.2.

Asia

Pacific Drip Irrigation Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

10.1.2.1. By Material

10.1.2.2. By Method

10.1.2.3. By Crop

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Drip

Irrigation Market: Estimates &

Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Drip Irrigation Market Introduction

11.1.2.

Middle East & Africa Drip Irrigation Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Material

11.1.2.2. By Method

11.1.2.3. By Crop

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Drip Irrigation Market: Estimates &

Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Drip Irrigation Market Introduction

12.1.2.

Latin

America Drip Irrigation Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

12.1.2.1. By Material

12.1.2.2. By Method

12.1.2.3. By Crop

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Drip Irrigation Market Product Mapping

14.2.

Global

Drip Irrigation Market Concentration Analysis, by Leading Players / Innovators

/ Emerging Players / New Entrants

14.3.

Global

Drip Irrigation Market Tier Structure Analysis

14.4.

Global

Drip Irrigation Market Concentration & Company Market Shares (%) Analysis,

2024

15.

Company

Profiles

15.1.

ARKA

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. Antelco

15.3. Amiad

Water Systems Ltd.

15.4. AZUD

15.5. Chinadrip

Irrigation Equipment (Xiamen) Co., Ltd.

15.6. HUNTER

INDUSTRIES INC.

15.7. Irritec

S.p.A

15.8. Jain

Irrigation Systems Ltd.

15.9. Metzer

15.10. STF

15.11. NETAFIM

15.12. Rain

Bird Corporation

15.13. Rivulis

15.14. The Toro

Company

15.15. Others

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables