Global Drug of Abuse Testing Services Market Size and Forecast (2025 - 2033), With Regional Share and Segment Analysis Report Coverage: By Product Type (Analyzers, Immunoassay Analyzers, Chromatographic Devices, Breath Analyzers, Rapid Testing Devices, etc.), By Sample Type (Saliva, Breath, Urine, Blood, Hair & Sweat), By Testing Type (Pain Management Testing, Criminal Justice Testing, Workplace Screening), By End-user (Hospitals, Diagnostic Laboratories, On-the-spot Testing Centers, Forensic Laboratories), and Geography

2025-11-27

Healthcare

Swetal (Research Analyst)

Description

Drug of Abuse Testing Services Market Overview

The Global Drug of Abuse Testing Services Market is projected to reach USD 6.2 billion by 2033, up from USD 4.3 billion in 2025, reflecting a CAGR of 4.8% during 2025–2033. The rising prevalence of substance use disorders, increasing emphasis on workplace safety, and expanding legal and regulatory oversight in developed and developing economies are key factors bolstering the market growth. Drug of abuse (DOA) testing services play a crucial role in detecting the presence of illegal or controlled drugs in biological samples such as urine, saliva, blood, hair, and breath.

Market evolution is being shaped

by advanced testing technologies such as chromatographic devices, immunoassay

analyzers, and rapid oral fluid testing. Furthermore, service providers are

increasingly adopting laboratory automation and digital health integration to

improve robustness and accuracy in both laboratory-based and on-site testing

environments. The rise in opioid misuse and prescription drug monitoring

initiatives in regions like North America and Europe has paved the way for

consistent demand from hospitals, criminal justice systems, and workplace

screening programs.

Drug of Abuse Testing Services Market Drivers and

Opportunities

Rising Incidence of Substance Use Disorders Is Fueling the

Demand for Drug Abuse Testing

The

increasing incidence of drug misuse and dependency globally is a major driver

behind the growth of the drug abuse testing services market. According to the

United Nations Office on Drugs and Crime (UNODC), over 296 million people

worldwide used drugs in 2021, and nearly 39.5 million suffered from drug use

disorders. Rising opioid and stimulant abuse in both developed and emerging

economies has amplified the need for accurate, reliable, and accessible drug

testing services across clinical, criminal justice, and occupational safety

sectors. The greater availability of synthetic drugs, prescription medications,

and illicit substances like cannabis, cocaine, and opioids has made DOA testing

essential not only for medical assessments but also for legal and public safety

compliance. Pain management testing, in particular, has surged due to increased

opioid prescriptions, requiring regular toxicology screening to monitor patient

adherence and detect potential misuse. Furthermore, government-funded awareness

campaigns and legal policies aiming to reduce drug-related harm have

incentivized investments in both laboratory-based and rapid testing models.

Hospitals, rehabilitation centers, law enforcement agencies, and corporate

employers are prioritizing toxicological testing protocols, often in

partnership with third-party laboratories, to mitigate liability and uphold

safety standards. These factors collectively contribute to sustained demand for

drug abuse testing services globally.

Stringent Workplace and Public Safety Regulations Are

Accelerating the Adoption of Drug Testing Services

Across key sectors such as transportation, logistics, mining, healthcare, and aviation, mandatory drug testing policies are being implemented to minimize workplace accidents and enhance productivity. The adoption of drug testing services is no longer limited to law enforcement or healthcare facilities. It has expanded into corporate workplaces driven by OSHA-guided safety protocols and industry-specific regulations like the U.S. Department of Transportation (DOT) drug testing mandates.

In regions such as North America and Western Europe, workplace drug testing is compulsory in industries where impairment can lead to fatal incidents, such as in aviation, oil and gas, and construction. Employers are also using drug screening as part of pre-employment selection, periodic testing, and post-incident investigations. With the increase in remote work and gig economies, virtual and mobile-based drug testing services have gained traction, enabling compliance through flexible and tech-enabled platforms. Public safety initiatives, especially concerning DUI and crime control, have further accelerated the use of chromatographic and rapid breath or saliva analyzers by law enforcement authorities. Additionally, drug courts and community corrections conduct regular substance testing to monitor offenders, fueling demand across forensic labs. This tightening regulatory network and its ripple effect on testing adoption are expected to continue as governments upgrade surveillance around drug misuse.

Emerging

Markets' Expansion of Rapid and Mobile Testing Solutions Is Poised to Create

Significant Opportunities in The Drug Abuse Testing Market Worldwide

The expansion of rapid, cost-effective, and mobile drug testing technologies in emerging economies presents a substantial growth opportunity for market players. Regions like Asia Pacific, Latin America, and the Middle East are witnessing a surge in drug abuse cases, driven by socioeconomic transitions, urban drug trafficking networks, and high youth unemployment. As government bodies and private employers in these regions begin to adopt more structured drug testing protocols, the demand for quick and portable solutions is expected to escalate. Rapid tests such as point-of-care urine cups, oral swab devices, and handheld breath analyzers eliminate the need for laboratory infrastructure, making them particularly viable in rural or remote settings. Companies focusing on producing affordable test kits with high specificity and sensitivity can capture large market shares in low- and middle-income countries. Additionally, smartphone-based testing kits and digital reporting platforms are gaining popularity, enabling instant results and cloud-based record-keeping for employers and clinicians. Collaborations with local distributors, investments in diagnostic centers, and strategic marketing to public health authorities will open new revenue channels for market entrants. With government-backed anti-drug campaigns on the rise, especially in China, India, Brazil, and South Africa, rapid testing manufacturers and service providers are positioned for accelerated growth in the coming decade.

Drug of Abuse Testing

Services Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 4.3 Billion |

|

Market Forecast in 2033 |

USD 6.2 Billion |

|

CAGR % 2025-2033 |

4.8% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Product Type ●

By Sample Type ●

By Testing Type ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Drug of Abuse Testing

Services Market Report Segmentation Analysis

The global drug abuse testing

services market industry analysis is segmented by product type, by sample type,

by testing type, by end-user, and by region.

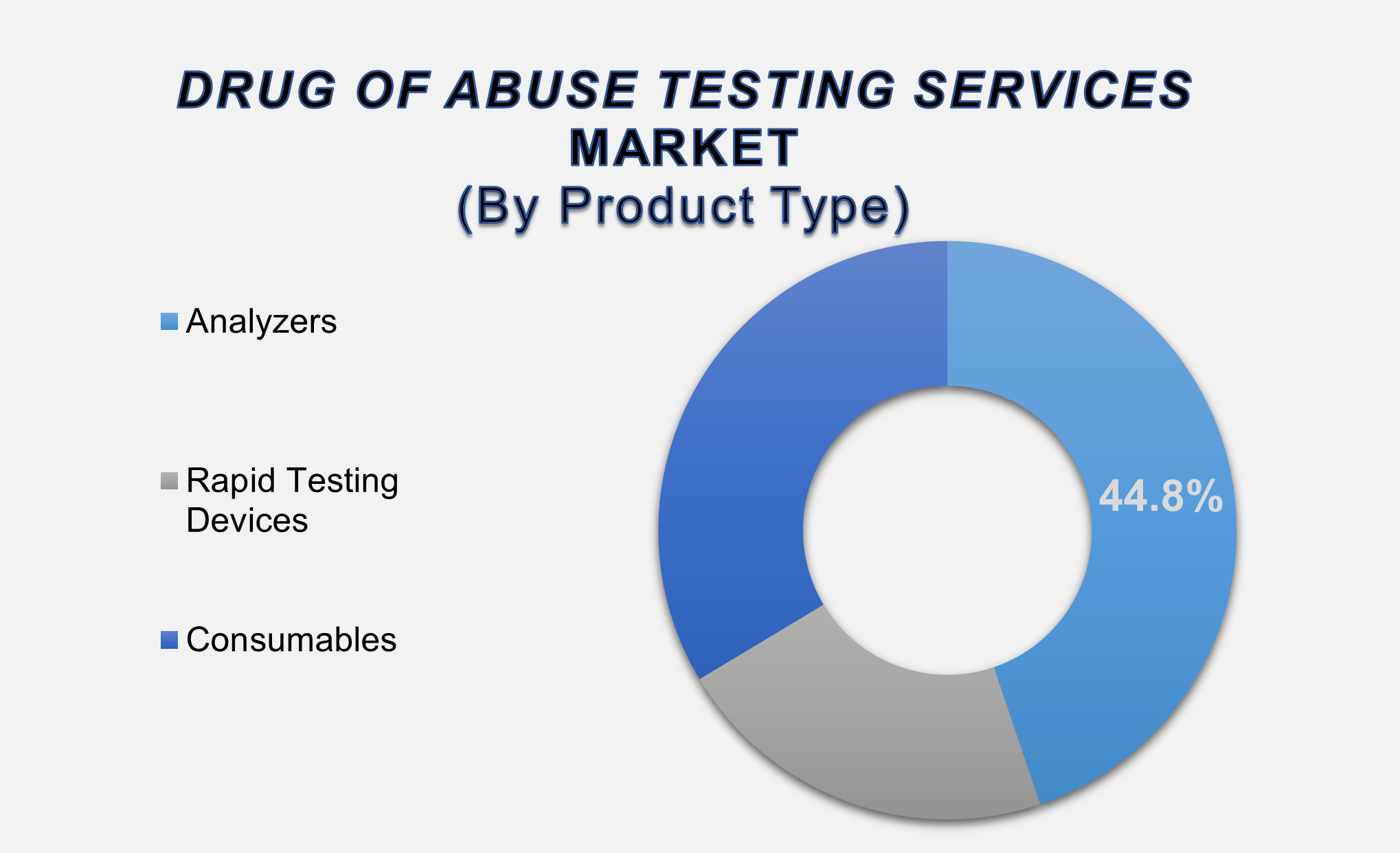

The

Analyzers Segment Accounted for the Largest Market

Share in the Global Drug of Abuse Testing Services Market

By

Product Type, the market is segmented into Analyzers, Immunoassays Analyzers,

Chromatographic Devices, Breath Analyzers, Rapid Testing Devices, Urine Testing

Devices, Oral Fluid Testing Devices, Consumables, Fluid Collection Devices, and

Others. The Analyzers segment dominates the global market, holding the largest

share in 2025. These analyzers are widely used in diagnostic laboratories and

forensic toxicology centers due to their high precision, rapid throughput, and

capability to process multiple drug panels at once. The growing focus on

accurate detection of poly-drug use, especially in criminal justice and

clinical pain management, is bolstering demand for advanced analyzers such as

LC-MS/MS and GC-MS devices. Continuous upgrades offering automated sampling,

real-time analytics, and cloud connectivity are also driving preferences for

these systems. Moreover, the rising adoption of evidence-based diagnostics in

hospital settings, fueled by increasing cases

of opioid overdose and recreational drug use,

is expected to sustain growth in this segment through 2033.

Urine

Sample Segment Held the Largest Share in the Global Drug of Abuse Testing

Services Market

By

Sample Type, the market is divided into Saliva, Breath, Urine, Blood, and Hair

& Sweat. The Urine segment accounted for the largest share of the global

market in 2025. Urine testing is considered the gold standard in drug screening

due to its ease of collection, low cost, and ability to detect a wide range of

substances and metabolites for longer durations. Commonly utilized in workplace

screenings, medical diagnostics, and post-accident investigations, urine

samples provide clear insights into both recent

and chronic drug use. Advancements in rapid urine-based test strips and

portable analyzers are enhancing result accuracy and turnaround time. Its

non-invasive nature and suitability for verifying compliance in pain management

or rehabilitation programs further support its dominance. Additionally,

organizations such as DOT and SAMHSA mandate urine-based drug testing for

federal and safety-sensitive positions, ensuring continued global demand in

this segment.

Criminal

Justice Testing Segment Accounted for the Largest Market Share in the Global

Drug Abuse Testing Services Market

By

Testing Type, the market is segmented into Pain Management Testing, Criminal

Justice Testing, Workplace Screening, and On-the-spot Testing. The Criminal

Justice Testing segment held the dominant position in 2025, driven by

increasing drug-related crimes, mandated testing by law enforcement agencies,

and parole/probation assessments. Government-led initiatives to identify

impaired driving, drug trafficking, and narcotics-fueled violence have

intensified the use of laboratory and rapid testing methods across correctional

facilities and legal frameworks. The segment benefits from established testing

protocols, long-term contracts with forensic labs, and multidisciplinary

toxicology research that supports court-admissible evidence. Investments in

high-throughput analyzers for narcotics profiling and integration of laboratory

information systems (LIS) are also contributing to the segment's growth. With

proactive drug legislation in advanced and emerging economies alike, the

criminal justice testing segment is projected to maintain market leadership

throughout the forecast period.

The following segments are

part of an in-depth analysis of the global Drug of Abuse Testing Services

market:

|

Market Segments |

|

|

By Product

Type |

●

Analyzers o

Immunoassays

Analyzers o

Chromatographic

Devices o

Breath Analyzers ●

Rapid Testing

Devices o

Urine Testing

Devices o

Oral Fluid Testing

Devices ●

Consumables o

Fluid Collection

Devices o

Others |

|

By Sample Type |

●

Saliva ●

Breath ●

Urine ●

Blood ●

Hair & Sweat |

|

By Testing

Type |

●

Pain Management

Testing ●

Criminal Justice

Testing ●

Workplace Screening |

|

By End-user |

●

Hospitals ●

Diagnostics

Laboratories ●

On-the-spot Testing ●

Forensic

Laboratories |

Drug of Abuse Testing

Services Market Share Analysis by Region

North America is

anticipated to hold the largest portion of the Drug Abuse Testing Services

Market globally throughout the forecast period.

North America accounted for the

largest share of the global drug abuse testing services market in 2025,

capturing approximately 39.9% of total revenue. The region's dominance is

primarily attributed to its structured regulatory environment, widespread substance

use issues, and well-established healthcare infrastructure. The U.S., in

particular, drives a significant portion of the market due to mandatory drug

testing programs across federal workplaces, DOT compliance, and an advanced

network of diagnostic laboratories. The opioid epidemic and rising incidence of

fentanyl-related overdoses have spurred federal and state governments to invest

in toxicology services and drug monitoring initiatives. Moreover, corporations

in North America are increasingly implementing pre-employment and random drug

screenings to reduce workplace accidents and liabilities.

Asia Pacific, on the other hand,

is anticipated to record the highest CAGR during 2025–2033 owing to growing

drug trafficking, increasing awareness of drug-related health risks, and

stricter enforcement of drug laws. Countries like China, India, and Indonesia

are witnessing an uptick in synthetic drug use, prompting governments to invest

in rapid testing services at transportation hubs, schools, and corporate

sectors. Improved access to healthcare and growing awareness among employers in

APAC's urban centers further support market expansion. Additionally, APAC holds

a cost advantage in manufacturing test devices, attracting multinational

companies to set up localized production units.

Drug of Abuse Testing

Services Market Competition Landscape Analysis

The drug abuse testing services

market is moderately fragmented, with leading players such as Quest

Diagnostics, Laboratory Corporation of America, Abbott Laboratories, and

Siemens Healthineers holding significant market shares. These companies focus

on developing advanced chromatographic devices, automated analyzers, and

digital toxicology platforms.

Global Drug of Abuse

Testing Services Market Recent Developments News:

- In September 2024,

Quest Diagnostics acquired select laboratory assets from Allina

Health, enhancing access to affordable, high-quality laboratory services

for patients and providers across Minnesota and western Wisconsin.

- In August 2024,

Quest Diagnostics signed an agreement with University Hospitals to

purchase select assets of its outreach laboratory services business,

expanding Quest’s diagnostic service footprint and strengthening its

collaboration with a leading academic health system.

- In May 2024,

Omega Laboratories partnered with Cannabix Technologies Inc. to

integrate the FAST™ THC Breathalyzer into its drug testing portfolio. This

collaboration established Omega as the exclusive laboratory service

provider for Cannabix, improving the accuracy and efficiency of cannabis

impairment testing.

The Global Drug of Abuse Testing

Services Market Is Dominated by a Few Large Companies, such as

●

Quest Diagnostics

●

Laboratory Corporation

of America

●

Abbott Laboratories

●

Siemens Healthineers

●

Roche Diagnostics

●

Thermo Fisher

Scientific

●

Danaher Corporation

●

Bio-Rad Laboratories

●

Merck KGaA

●

Synergy Health

●

Clinical Reference

Laboratory

●

Cordant Health

Solutions

●

Millennium Health

●

Precision Diagnostics

●

American Bio Medica

Corporation

●

Randox Laboratories

●

OraSure Technologies

●

Alere

●

LGC Limited

●

Psychemedics

Corporation

● Others

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global Drug of Abuse

Testing Services Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Drug of Abuse Testing Services Market Scope and Market Estimation

1.2.1.Global Drug of Abuse

Testing Services Overall Market Size (US$ Bn), Market CAGR (%), Market forecast

(2025 - 2033)

1.2.2.Global Drug of Abuse

Testing Services Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product Type of Global Drug

of Abuse Testing Services Market

1.3.2.Sample Type of Global Drug

of Abuse Testing Services Market

1.3.3.Testing Type of Global Drug

of Abuse Testing Services Market

1.3.4.End-user of Global Drug of

Abuse Testing Services Market

1.3.5.Region of Global Drug of

Abuse Testing Services Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Drug of Abuse Testing Services Market

Estimates & Historical Trend Analysis (2020 - 2024)

4. Global

Drug of Abuse Testing Services Market

Estimates & Forecast Trend Analysis, by Product

Type

4.1.

Global

Drug of Abuse Testing Services Market Revenue (US$ Bn) Estimates and Forecasts,

by Product Type, 2020 - 2033

4.1.1.Analyzers

4.1.1.1.

Immunoassays

Analyzers

4.1.1.2.

Chromatographic

Devices

4.1.1.3.

Breath

Analyzers

4.1.2.Rapid Testing Devices

4.1.2.1.

Urine

Testing Devices

4.1.2.2.

Oral

Fluid Testing Devices

4.1.3.Consumables

4.1.3.1.

Fluid

Collection Devices

4.1.3.2.

Others

5. Global

Drug of Abuse Testing Services Market

Estimates & Forecast Trend Analysis, by Sample

Type

5.1.

Global

Drug of Abuse Testing Services Market Revenue (US$ Bn) Estimates and Forecasts,

by Sample Type, 2020 - 2033

5.1.1.Saliva

5.1.2.Breath

5.1.3.Urine

5.1.4.Blood

5.1.5.Hair & Sweat

6. Global

Drug of Abuse Testing Services Market

Estimates & Forecast Trend Analysis, by Testing

Type

6.1.

Global

Drug of Abuse Testing Services Market Revenue (US$ Bn) Estimates and Forecasts,

by Testing Type, 2020 - 2033

6.1.1.Pain Management Testing

6.1.2.Criminal Justice Testing

6.1.3.Workplace Screening

7. Global

Drug of Abuse Testing Services Market

Estimates & Forecast Trend Analysis, by End-user

7.1.

Global

Drug of Abuse Testing Services Market Revenue (US$ Bn) Estimates and Forecasts,

by End-user, 2020 - 2033

7.1.1.Hospitals

7.1.2.Diagnostics Laboratories

7.1.3.On-the-spot Testing

7.1.4.Forensic Laboratories

8. Global

Drug of Abuse Testing Services Market

Estimates & Forecast Trend Analysis, by Region

8.1.

Global

Drug of Abuse Testing Services Market Revenue (US$ Bn) Estimates and Forecasts,

by Region, 2020 - 2033

8.1.1.North America

8.1.2.Europe

8.1.3.Asia Pacific

8.1.4.Middle East & Africa

8.1.5.Latin America

9. North America Drug

of Abuse Testing Services Market:

Estimates & Forecast Trend Analysis

9.1. North America Drug of

Abuse Testing Services Market Assessments & Key Findings

9.1.1.North America Drug of

Abuse Testing Services Market Introduction

9.1.2.North America Drug of

Abuse Testing Services Market Size Estimates and Forecast (US$ Billion) (2020 -

2033)

9.1.2.1.

By Product Type

9.1.2.2.

By Sample Type

9.1.2.3.

By Testing Type

9.1.2.4.

By End-user

9.1.2.5. By Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Drug

of Abuse Testing Services Market:

Estimates & Forecast Trend Analysis

10.1. Europe Drug of Abuse

Testing Services Market Assessments & Key Findings

10.1.1. Europe Drug of Abuse

Testing Services Market Introduction

10.1.2. Europe Drug of Abuse

Testing Services Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1.

By Product Type

10.1.2.2.

By Sample Type

10.1.2.3.

By Testing Type

10.1.2.4.

By End-user

10.1.2.5. By Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7. Rest

of Europe

11. Asia Pacific Drug

of Abuse Testing Services Market:

Estimates & Forecast Trend Analysis

11.1. Asia Pacific Market

Assessments & Key Findings

11.1.1.

Asia

Pacific Drug of Abuse Testing Services Market Introduction

11.1.2.

Asia

Pacific Drug of Abuse Testing Services Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

11.1.2.1.

By Product Type

11.1.2.2.

By Sample Type

11.1.2.3.

By Testing Type

11.1.2.4.

By End-user

11.1.2.5. By Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Drug

of Abuse Testing Services Market:

Estimates & Forecast Trend Analysis

12.1. Middle East & Africa

Market Assessments & Key Findings

12.1.1. Middle

East & Africa

Drug of Abuse Testing Services Market Introduction

12.1.2. Middle

East & Africa

Drug of Abuse Testing Services Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

12.1.2.1.

By Product Type

12.1.2.2.

By Sample Type

12.1.2.3.

By Testing Type

12.1.2.4.

By End-user

12.1.2.5. By Country

12.1.2.5.1. UAE

12.1.2.5.2. Saudi

Arabia

12.1.2.5.3. South

Africa

12.1.2.5.4. Rest

of MEA

13. Latin America

Drug of Abuse Testing Services Market:

Estimates & Forecast Trend Analysis

13.1. Latin America Market

Assessments & Key Findings

13.1.1. Latin America Drug of

Abuse Testing Services Market Introduction

13.1.2. Latin America Drug of

Abuse Testing Services Market Size Estimates and Forecast (US$ Billion) (2020 -

2033)

13.1.2.1.

By Product Type

13.1.2.2.

By Sample Type

13.1.2.3.

By Testing Type

13.1.2.4.

By End-user

13.1.2.5. By Country

13.1.2.5.1. Brazil

13.1.2.5.2. Argentina

13.1.2.5.3. Mexico

13.1.2.5.4. Rest

of LATAM

14.

Country

Wise Market: Introduction

15.

Competition

Landscape

15.1. Global Drug of Abuse

Testing Services Market Product Mapping

15.2. Global Drug of Abuse

Testing Services Market Concentration Analysis, by Leading Players / Innovators

/ Emerging Players / New Entrants

15.3. Global Drug of Abuse

Testing Services Market Tier Structure Analysis

15.4. Global Drug of Abuse

Testing Services Market Concentration & Company Market Shares (%) Analysis,

2024

16.

Company

Profiles

16.1.

Quest Diagnostics

16.1.1.

Company

Overview & Key Stats

16.1.2.

Financial

Performance & KPIs

16.1.3.

Product

Portfolio

16.1.4.

SWOT

Analysis

16.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

16.2.

Laboratory Corporation of America

16.3.

Abbott Laboratories

16.4.

Siemens Healthineers

16.5.

Roche Diagnostics

16.6.

Thermo Fisher Scientific

16.7.

Danaher Corporation

16.8.

Bio-Rad Laboratories

16.9.

Merck KGaA

16.10.

Synergy Health

16.11.

Clinical Reference Laboratory

16.12.

Cordant Health Solutions

16.13.

Millennium Health

16.14.

Precision Diagnostics

16.15.

American Bio Medica Corporation

16.16.

Randox Laboratories

16.17.

OraSure Technologies

16.18.

Alere

16.19.

LGC Limited

16.20.

Psychemedics Corporation

16.21.

Others

17. Research

Methodology

17.1. External Transportations /

Databases

17.2. Internal Proprietary

Database

17.3. Primary Research

17.4. Secondary Research

17.5. Assumptions

17.6. Limitations

17.7. Report FAQs

18. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables