Dry Eye Syndrome Treatment Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Product (Anti-inflammatory Products, Cyclosporine, Corticosteroids, Artificial Tears and Lubricants, Others); By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Others); and Geography

2025-12-16

Healthcare

Swetal (Research Analyst)

Description

Dry Eye

Syndrome Treatment Market Overview

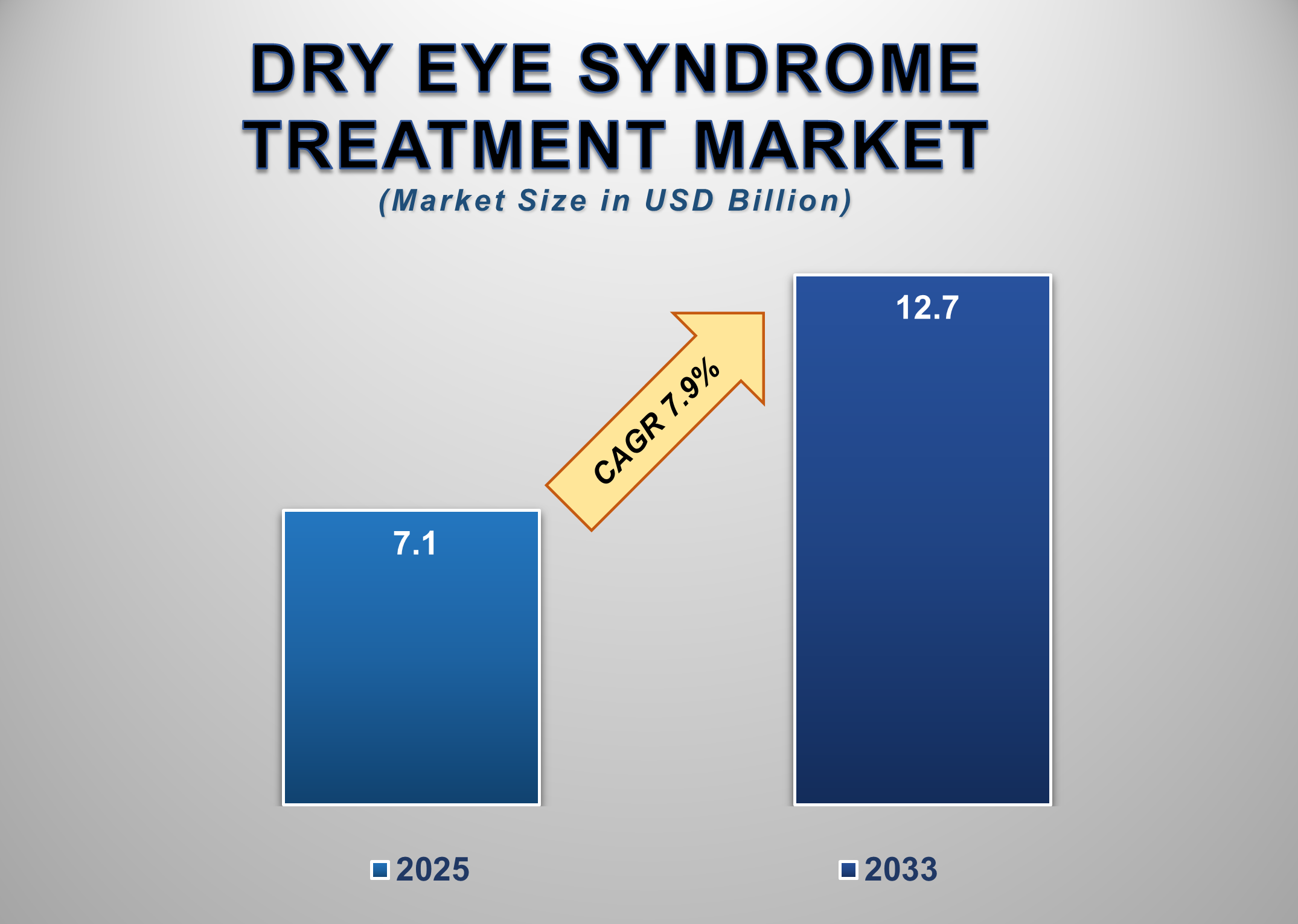

The Global Dry Eye Syndrome Treatment Market is gaining traction due to the increasing incidence of ocular surface diseases and growing awareness about eye health among the aging and digitally active population. Valued at USD 7.1 billion in 2025, the market is projected to expand to USD 12.7 billion by 2033, exhibiting a robust CAGR of 7.9% during the forecast period. Dry eye syndrome, a condition caused by insufficient lubrication or poor-quality tears, affects millions globally and is associated with lifestyle changes, including prolonged exposure to screens, air-conditioned environments, and environmental pollution.

Product innovation, evolving

regulatory frameworks, and the introduction of targeted biologics such as

cyclosporine and lifitegrast are driving market growth. Additionally, the

rising adoption of e-commerce platforms and personalized treatment regimes is

enhancing patient access to specialized therapies. With continuous advancements

in drug delivery platforms and regenerative medicine, the dry eye treatment

landscape is poised for significant expansion across developed and emerging

markets.

Dry Eye Syndrome Treatment Market Drivers and

Opportunities

The

Growing Prevalence of Digital Eye Strain Among All

Age Groups Is Driving the Dry Eye Syndrome Treatment Market Growth

The

widespread use of digital devices such as smartphones, laptops, and tablets has

led to a surge in digital eye strain, a primary contributor to dry eye

syndrome. As screen time increases across all age demographics, especially among working professionals and students, ocular surface disorders have become more prevalent. The

COVID-19 pandemic magnified this trend, with remote working and online learning

accelerating prolonged exposure to screens.

Digital

devices reduce blink rate and increase tear film evaporation, triggering

symptoms such as irritation, burning, and blurred vision. As a result, the

demand for artificial tears, lubricants, and anti-inflammatory medications has

increased substantially. Both over-the-counter (OTC) and prescription

treatments are in high demand, with ophthalmologists now prioritizing early

detection and management to prevent chronic ocular damage. Manufacturers are

focusing on formulating preservative-free products, long-acting gels, and

combination therapies to improve treatment compliance and long-term efficacy.

OTC product lines are expanding to cater to the growing self-care trend among

consumers, fueling segment growth. With continued technological integration and

consumer education, digital eye strain is set to remain a dominant growth

driver in the global dry eye syndrome treatment market.

Rising

Geriatric Population and Age-Associated Ocular Diseases Are Fueling Demand for

Dry Eye Treatments

Aging

is a well-established risk factor for developing dry eye syndrome, with the

condition more prevalent among people aged 50 and above. The global geriatric

population (aged 60 and above) is growing rapidly, particularly in the Asia Pacific, Europe, and North America. Age-related

changes, such as reduced tear secretion,

hormonal fluctuations in postmenopausal women, and increased incidence of

chronic diseases like diabetes, make elderly

individuals more susceptible to severe dry eye symptoms. As longevity

increases, the number of patients seeking medical intervention for ocular

health is expanding. This trend has led to greater demand for

prescription-based treatments, including

cyclosporine, corticosteroids, and novel biologic agents. Moreover,

age-associated comorbidities often require polypharmacy, further exacerbating

ocular surface drying and inflammation.

The

healthcare ecosystem is responding with specialized geriatric eye care

programs, awareness initiatives, and accessible reimbursement frameworks in

countries like Japan, Germany, and the U.S. Innovations in tear film modulators

and sustained-release inserts also align with the needs of elderly patients,

enhancing convenience and adherence. Therefore, the demographic shift toward an

aging population is a major growth catalyst for the market.

Opportunity for the Dry

Eye Syndrome Treatment Market

Advancements in Regenerative and Biologic Therapies Are

Creating High-Value Opportunities in the Global Market

The

emergence of regenerative and biologic therapies presents lucrative

opportunities for players in the dry eye syndrome treatment market. Novel drug

candidates, such as nerve growth factor (NGF) analogs and gene-modulating

formulations, are under development to address the root cause of tear film

dysfunction rather than providing temporary symptomatic relief. These therapies

aim to repair ocular nerve damage, promote corneal healing, and stimulate

natural tear production.

Biologic

agents such as cyclosporine and lifitegrast have already demonstrated success

in reducing inflammation associated with chronic dry eye. Additionally,

innovations in drug delivery systems like nanocarriers, micellar gels, and

dissolvable inserts improve bioavailability and extend the duration of action,

reducing treatment burden. Companies are investing in targeted breastmilk-based

drops, stem cell-derived exosomes, and autologous serum-based formulations,

signaling a shift toward personalized ocular care. Moreover, increasing

clinical trial activity and supportive regulatory pathways, particularly in

regions like the U.S., Japan, and South Korea, are accelerating product

approvals and market entry timelines. As R&D pipelines expand and real-world

evidence supports clinical efficacy, advanced biologics and regenerative

products are expected to transform the treatment landscape over the next

decade.

Dry Eye Syndrome

Treatment Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 7.1 Billion |

|

Market Forecast in 2033 |

USD 12.7 Billion |

|

CAGR % 2025-2033 |

7.9% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Product ●

By Distribution

Channel |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Dry Eye Syndrome

Treatment Market Report Segmentation Analysis

The global Dry Eye Syndrome

Treatment market industry analysis is segmented by product, by distribution

channel, and by region.

The

Anti-Inflammatory Products segment accounted for the

largest market share in the global Dry Eye Syndrome Treatment market

By

Product, the market is segmented into Anti-inflammatory Products, Cyclosporine,

Corticosteroids, Artificial Tears & Lubricants, and Others. The

Anti-inflammatory Products segment accounted for the largest share of the

global dry eye syndrome treatment market in 2025. This dominance is attributed

to the widespread adoption of anti-inflammatory formulations, particularly corticosteroids, cyclosporine ophthalmic

emulsions, and lifitegrast for managing moderate to severe dry eye conditions.

These products address the root cause of inflammation in the ocular surface,

making them preferred options among ophthalmologists for both acute and chronic

cases. Their ability to improve tear quality and reduce corneal damage has

cemented their role in clinical practice. Furthermore, ongoing research into

novel anti-inflammatory mechanisms and drug delivery systems is enhancing

treatment efficacy and safety profiles. The introduction of biodegradable

inserts and nanodispersion-based eye drops reinforces this segment’s strong

growth trajectory.

The Hospital

Pharmacies segment is segmented into Hospital Pharmacies, Retail Pharmacies,

Online Pharmacies, and Others

By

Distribution Channel, the market includes Hospital Pharmacies, Retail

Pharmacies, Online Pharmacies, and Others. The Hospital Pharmacies segment

holds the largest share due to the high volume of prescriptions dispensed

through integrated hospital networks, particularly for immunomodulatory dry eye

treatments that require specialist consultation. The presence of in-house

ophthalmologists and the availability of

advanced diagnostics make hospitals the

preferred settings for treating severe or chronic cases.

The following segments are

part of an in-depth analysis of the global Dry Eye Syndrome Treatment Market:

|

Market

Segments |

|

|

By Product |

●

Anti-inflammatory

Products o

Cyclosporine o

Corticosteroids o

Others ●

Artificial Tears and

Lubricants ●

Others |

|

By

Distribution Channel |

●

Hospital Pharmacies ●

Retail Pharmacies ●

Online Pharmacies ●

Others |

Dry Eye Syndrome Treatment Market Share Analysis

by Region

The

Asia Pacific region is projected to hold the largest

share of the global Dry Eye Syndrome Treatment market over the forecast period

The Asia Pacific (APAC) region is expected to dominate the

global dry eye syndrome treatment market in 2025, accounting for 38.9% of total

revenue. This leadership is attributed to the region’s large aging population,

rising diabetes prevalence, and increased exposure to digital screens among

young adults and working professionals. Countries like Japan, South Korea,

China, and India are experiencing a surge in market penetration due to growing

ophthalmic disease awareness, rising disposable incomes, and the expansion of specialty eye care facilities. The

pharmaceutical landscape in APAC is also benefiting from localized drug

manufacturing, government-backed initiatives for eye care accessibility, and

innovations in biologics and biosimilar eye drops. Strategic partnerships

between global innovators and regional players further support distribution and

regulatory compliance.

Dry Eye Syndrome Treatment Market Competition

Landscape Analysis

The global dry

eye syndrome treatment market is moderately competitive, with the presence of

established players focused on innovating treatment modalities and enhancing

drug delivery methods. Key companies are investing in clinical trials,

strategic partnerships, and regional market expansion to strengthen their

portfolio.

Global Dry Eye Syndrome Treatment Market Recent

Developments News:

- In October 2024, Novaliq and

Laboratoires Théa announced that Vevizye®, a water-free 0.1% ciclosporin

eye drop, received marketing approval from the European Commission for the

treatment of dry eye disease in adults. It is the first and only

formulation of its kind approved in Europe.

- In June 2024, Oculis reported

positive Phase 2b results for licaminlimab, an anti-TNFα eye drop for dry

eye disease. The trial demonstrated significant improvement in DED signs,

particularly in patients with a specific TNFR1 biomarker, showing rapid

reduction in corneal inflammation and a favorable safety profile.

- In May 2024, Nordic Pharma, Inc., launched LACRIFILL® Canalicular Gel,

an FDA-cleared, cross-linked hyaluronic acid gel that temporarily blocks

tear drainage to improve natural tear retention. Administered in-office,

it provides six months of effect, is reimbursed under CPT code 68761, and

was featured at Kiawah Eye 2024 to support adoption by ophthalmic

practices.

The Global Dry Eye Syndrome Treatment Market is

dominated by a few large companies, such as

●

Allergan

●

Novartis

●

Johnson & Johnson

●

Bausch + Lomb

●

Santen Pharmaceutical

●

Sun Pharmaceutical

●

Otsuka Pharmaceutical

●

Regeneron

Pharmaceuticals

●

Aldeyra Therapeutics

●

Kala Pharmaceuticals

●

Novaliq GmbH

●

Sylentis

●

Mitotech

●

HanAll Biopharma

●

Aerie Pharmaceuticals

●

Akorn

●

Thea Pharma

●

Ursapharm

●

Alcon

●

RxSight

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global Dry Eye Syndrome

Treatment Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Dry Eye Syndrome Treatment Market Scope and Market Estimation

1.2.1.Global Dry Eye Syndrome

Treatment Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Dry Eye Syndrome

Treatment Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product of Global Dry Eye

Syndrome Treatment Market

1.3.2.Distribution Channel of

Global Dry Eye Syndrome Treatment Market

1.3.3.Region of Global Dry Eye

Syndrome Treatment Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Dry Eye Syndrome Treatment Market

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

2.10.

Key

Regulation

3. Global

Dry Eye Syndrome Treatment Market

Estimates & Historical Trend Analysis (2020 - 2024)

4. Global

Dry Eye Syndrome Treatment Market

Estimates & Forecast Trend Analysis, by Product

4.1.

Global

Dry Eye Syndrome Treatment Market Revenue (US$ Bn) Estimates and Forecasts, by Product,

2020 - 2033

4.1.1.Anti-inflammatory Products

4.1.1.1.

Cyclosporine

4.1.1.2.

Corticosteroids

4.1.1.3.

Others

4.1.2.Artificial Tears and

Lubricants

4.1.3.Others

5. Global

Dry Eye Syndrome Treatment Market

Estimates & Forecast Trend Analysis, by Distribution

Channel

5.1.

Global

Dry Eye Syndrome Treatment Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution

Channel, 2020 - 2033

5.1.1.Hospital Pharmacies

5.1.2.Retail Pharmacies

5.1.3.Online Pharmacies

5.1.4.Others

6. Global

Dry Eye Syndrome Treatment Market

Estimates & Forecast Trend Analysis, by Region

6.1.

Global

Dry Eye Syndrome Treatment Market Revenue (US$ Bn) Estimates and Forecasts, by Region,

2020 - 2033

6.1.1.North America

6.1.2.Europe

6.1.3.Asia Pacific

6.1.4.Middle East & Africa

6.1.5.Latin America

7. North America Dry

Eye Syndrome Treatment Market:

Estimates & Forecast Trend Analysis

7.1.

North

America Dry Eye Syndrome Treatment Market Assessments & Key Findings

7.1.1.North America Dry Eye

Syndrome Treatment Market Introduction

7.1.2.North America Dry Eye

Syndrome Treatment Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

7.1.2.1. By Product

7.1.2.2. By Distribution

Channel

7.1.2.3.

By

Country

7.1.2.3.1. The U.S.

7.1.2.3.2. Canada

8. Europe Dry

Eye Syndrome Treatment Market:

Estimates & Forecast Trend Analysis

8.1.

Europe

Dry Eye Syndrome Treatment Market Assessments & Key Findings

8.1.1.Europe Dry Eye Syndrome

Treatment Market Introduction

8.1.2.Europe Dry Eye Syndrome

Treatment Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Product

8.1.2.2. By Distribution

Channel

8.1.2.3.

By

Country

8.1.2.3.1.

Germany

8.1.2.3.2.

Italy

8.1.2.3.3.

U.K.

8.1.2.3.4.

France

8.1.2.3.5.

Spain

8.1.2.3.6.

Switzerland

8.1.2.3.7. Rest

of Europe

9. Asia Pacific Dry

Eye Syndrome Treatment Market:

Estimates & Forecast Trend Analysis

9.1.

Asia

Pacific Market Assessments & Key Findings

9.1.1.Asia Pacific Dry Eye

Syndrome Treatment Market Introduction

9.1.2.Asia Pacific Dry Eye

Syndrome Treatment Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product

9.1.2.2. By Distribution

Channel

9.1.2.3.

By

Country

9.1.2.3.1.

China

9.1.2.3.2.

Japan

9.1.2.3.3.

India

9.1.2.3.4.

Australia

9.1.2.3.5.

South

Korea

9.1.2.3.6. Rest of Asia Pacific

10. Middle East & Africa Dry

Eye Syndrome Treatment Market:

Estimates & Forecast Trend Analysis

10.1.

Middle

East & Africa Market Assessments & Key Findings

10.1.1.

Middle East & Africa Dry Eye Syndrome Treatment Market

Introduction

10.1.2.

Middle East & Africa Dry Eye Syndrome Treatment Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Product

10.1.2.2. By Distribution

Channel

10.1.2.3.

By

Country

10.1.2.3.1. UAE

10.1.2.3.2. Saudi

Arabia

10.1.2.3.3. South

Africa

10.1.2.3.4. Rest

of MEA

11. Latin America

Dry Eye Syndrome Treatment Market:

Estimates & Forecast Trend Analysis

11.1.

Latin

America Market Assessments & Key Findings

11.1.1.

Latin

America Dry Eye Syndrome Treatment Market Introduction

11.1.2.

Latin

America Dry Eye Syndrome Treatment Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

11.1.2.1. By Product

11.1.2.2. By Distribution

Channel

11.1.2.3.

By

Country

11.1.2.3.1. Brazil

11.1.2.3.2. Argentina

11.1.2.3.3. Mexico

11.1.2.3.4. Rest

of LATAM

12. Country Wise Market:

Introduction

13.

Competition

Landscape

13.1.

Global

Dry Eye Syndrome Treatment Market Product Mapping

13.2.

Global

Dry Eye Syndrome Treatment Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

13.3.

Global

Dry Eye Syndrome Treatment Market Tier Structure Analysis

13.4.

Global

Dry Eye Syndrome Treatment Market Concentration & Company Market Shares (%)

Analysis, 2024

14.

Company

Profiles

14.1.

Allergan

14.1.1.

Company

Overview & Key Stats

14.1.2.

Financial

Performance & KPIs

14.1.3.

Product

Portfolio

14.1.4.

SWOT

Analysis

14.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

14.2. Novartis

14.3. Johnson

& Johnson

14.4. Bausch +

Lomb

14.5. Santen

Pharmaceutical

14.6. Sun

Pharmaceutical

14.7. Otsuka

Pharmaceutical

14.8. Regeneron

Pharmaceuticals

14.9. Aldeyra

Therapeutics

14.10. Kala

Pharmaceuticals

14.11. Novaliq

GmbH

14.12. Sylentis

14.13. Mitotech

14.14. HanAll

Biopharma

14.15. Aerie

Pharmaceuticals

14.16. Akorn

14.17. Thea

Pharma

14.18. Ursapharm

14.19. Alcon

14.20. RxSight

14.21. Others

15. Research

Methodology

15.1.

External

Transportations / Databases

15.2.

Internal

Proprietary Database

15.3.

Primary

Research

15.4.

Secondary

Research

15.5.

Assumptions

15.6.

Limitations

15.7.

Report

FAQs

16. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables