Dyspnea Treatment Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; Treatment Type (Supplemental Oxygen Therapy and Drug Therapy), Route of Administration (Oral, Inhalation, and Intravenous), End User (Hospitals, Specialty Centers, and Others), and Geography

2026-02-23

Life Sciences

Swetal (Research Analyst)

Description

Dyspnea

Treatment Market Overview

The global dyspnea

treatment market is experiencing steady growth, driven by the rising prevalence

of respiratory and cardiovascular diseases, increasing geriatric population,

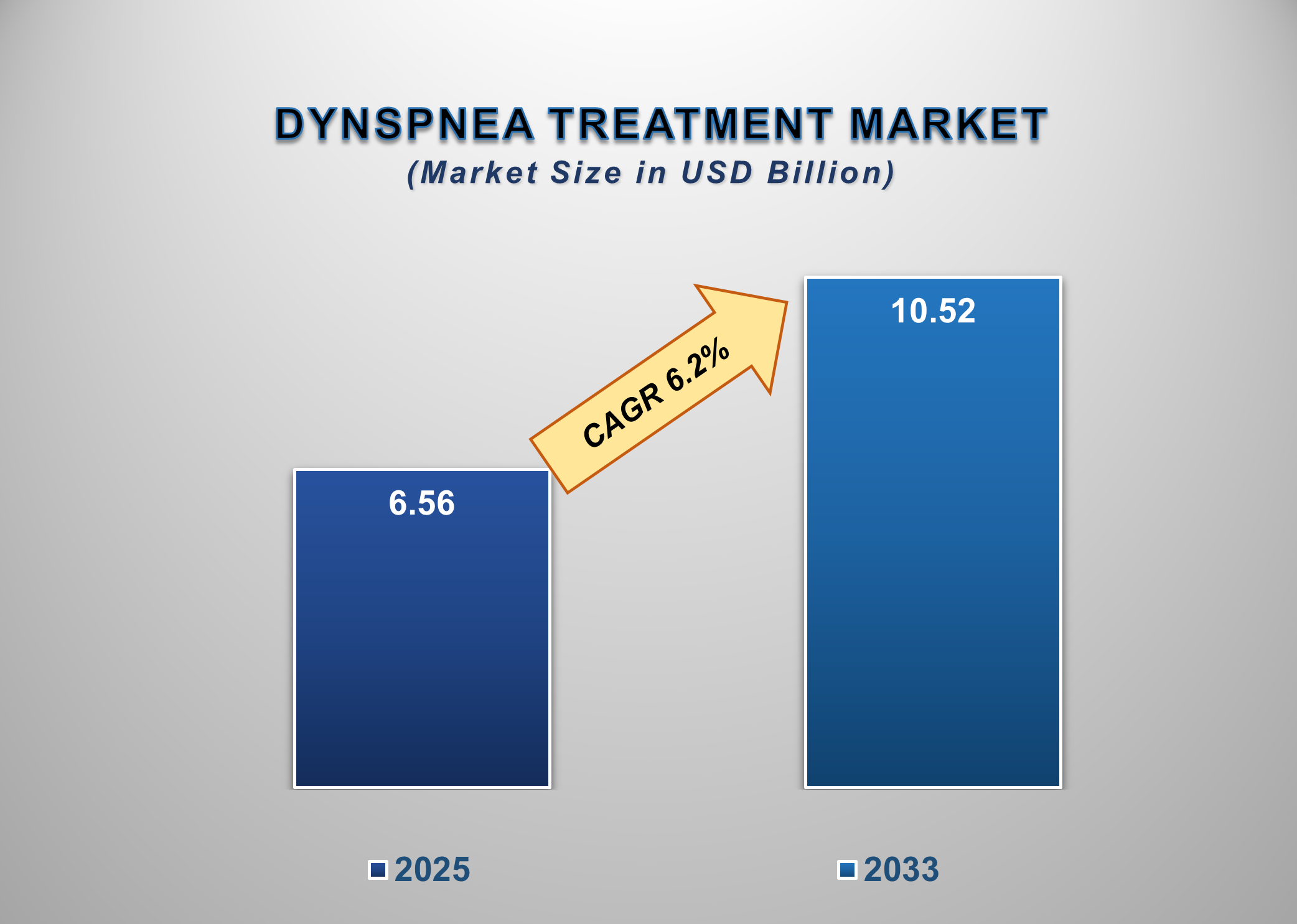

and advancements in respiratory treatment technologies. Valued at USD 6.56 billion in

2025, the market is projected to reach USD 10.52 billion by 2033, growing at a

CAGR of 6.2% during the forecast period.

Dyspnea, commonly referred to as shortness of breath, is a symptom associated with a wide range of acute and chronic conditions, including chronic obstructive pulmonary disease (COPD), asthma, heart failure, pulmonary fibrosis, pneumonia, and certain cancers. The dyspnea treatment market encompasses therapeutic interventions aimed at alleviating breathlessness, improving oxygenation, and enhancing patients’ overall quality of life. Treatment approaches are broadly categorized into supplemental oxygen therapy and drug therapy, along with supportive and palliative care measures.

The growing incidence of cardiovascular and

respiratory diseases worldwide is the main factor propelling the market.

Globally, the prevalence of COPD and asthma is rising due in large part to

rising air pollution, tobacco use, occupational lung illnesses, and aging

populations. Additionally, the number of patients needing dyspnea care has

increased due to the rising prevalence of heart failure and respiratory

problems following COVID-19. As populations age, there is an increasing need

for maintenance pharmaceutical treatment and long-term oxygen therapy,

especially in North America, Europe, and areas of the Asia-Pacific.

Medications that target underlying

inflammatory and obstructive pathways include bronchodilators, corticosteroids,

opioids (in palliative conditions), and combination inhalers. Supplemental

oxygen therapy, which is administered by portable devices, cylinders, and

concentrators, is still a mainstay for moderate to severe cases, especially in

chronic respiratory conditions. Smart inhaler systems and portable oxygen

concentrators are two examples of technological innovations that are enhancing

patient compliance and facilitating home-based care, which is driving market

expansion.

Improvements in emerging economies' healthcare

infrastructure, rising awareness of early diagnosis, and advantageous

reimbursement practices in developed nations are all contributing factors to

growth. However, obstacles, including expensive devices, complex regulatory

frameworks, and long-term medication adverse effects, could limit expansion.

Therefore, it is anticipated that the market for dyspnea treatments will

increase steadily over the next ten years, helped by the increasing prevalence

of the condition, advancements in respiratory treatments, and the growing trend

toward home healthcare solutions.

Dyspnea Treatment Market

Drivers and Opportunities

Rising Prevalence of Respiratory Disorders

One of the main factors

propelling the market for dyspnea treatments is the rise in chronic respiratory

ailments, including COPD,

asthma, and post-COVID lung disorders,

worldwide. Since dyspnea is a defining feature of many conditions, there is an

increasing need for treatment measures. For instance, estimates suggest that up

to 25 million people in the United States alone suffer from dyspnea, indicating

a significant clinical burden that needs continuous care. Moreover,

epidemiological data show that 13.7% of the global population may experience

dyspnea, with prevalence varying widely by region. The number of patients

looking for efficient treatment options, such as pharmaceutical medications and

supplementary oxygen therapy, is growing as a direct result of global air

pollution, smoking rates, and aging populations.

Technological Advancements and Innovation

Innovation in delivery

methods and treatment modalities is greatly supporting market expansion.

Improved oxygen concentrators, smart nebulizers, advanced inhaler systems, and

digital health integration are improving patient adherence, convenience, and clinical

results. In addition to its rapid onset and precise medication delivery, the

inhalation route, for instance, held a market share of more than 58% in

respiratory interventions. Furthermore, new treatments and regulatory approvals

are broadening treatment options; the rising clinical usage of biologics and

next-generation inhalation medications is facilitating uptake. In addition to

increasing effectiveness, these technological advancements help lessen adverse

effects, meet unmet medical

requirements, and attract more patients into organized treatment programs.

Expansion of Home-Based and Portable Therapies

The growth of home-based dyspnea management

systems presents a new opportunity. At-home treatment devices and portable

oxygen systems represent a high-growth market due to the increasing prevalence

of chronic respiratory disorders and the global trend toward outpatient care.

The increasing demand for easily accessible respiratory support outside of

hospitals is expected to fuel the wider oxygen treatment market's growth, which

is expected to reach USD 41.1 billion by 2033 at a 6.5% CAGR from USD 27.4 billion

in 2026. Compact concentrators, wearable respiratory devices, and remote

monitoring tools that satisfy patient demands for convenience and quality of

life present manufacturers with opportunities to expand their footprint as

healthcare infrastructures in emerging markets improve and reimbursement

support for long-term and home care strengthens.

Dyspnea Treatment Market Scope

|

Report Attributes |

Description |

|

Market Size in

2025 |

USD 6.56

Billion |

|

Market Forecast

in 2033 |

USD 10.5

Billion |

|

CAGR % 2025-2033 |

6.2% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Comprehensive

global Dyspnea Treatment Market size and forecast analysis, detailed

assessment of treatment types (Supplemental Oxygen Therapy and Drug Therapy),

route of administration analysis, end-user consumption trends, and regional

and country-level market dynamics. The report includes competitive landscape

evaluation, company market share analysis, pipeline and product innovation

insights, technological advancements in respiratory drug delivery and oxygen

systems, regulatory landscape assessment, reimbursement trends, and strategic

developments. It also covers key growth drivers, challenges, emerging

opportunities, and actionable strategic insights for pharmaceutical

companies, respiratory device manufacturers, healthcare providers, investors,

and stakeholders |

|

Segments Covered |

●

By

Treatment Type ●

By Route

of Administration ●

By End

User |

|

Regional Scope |

●

North

America ●

Europe ●

APAC ●

Latin

America ●

Middle

East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada

3)

U.K. 4)

Germany

5)

France

6)

Italy 7)

Spain 8)

Switzerland

9)

China

10)

India

11)

Japan 12)

South

Korea 13)

Australia 14)

Mexico

15)

Brazil

16)

Argentina

17)

Saudi

Arabia 18)

UAE 19)

South

Africa |

Dyspnea Treatment

Market Report Segmentation Analysis

The global Dyspnea

Treatment Market analysis is segmented by Treatment Type, Route of

Administration, End User, and Region.

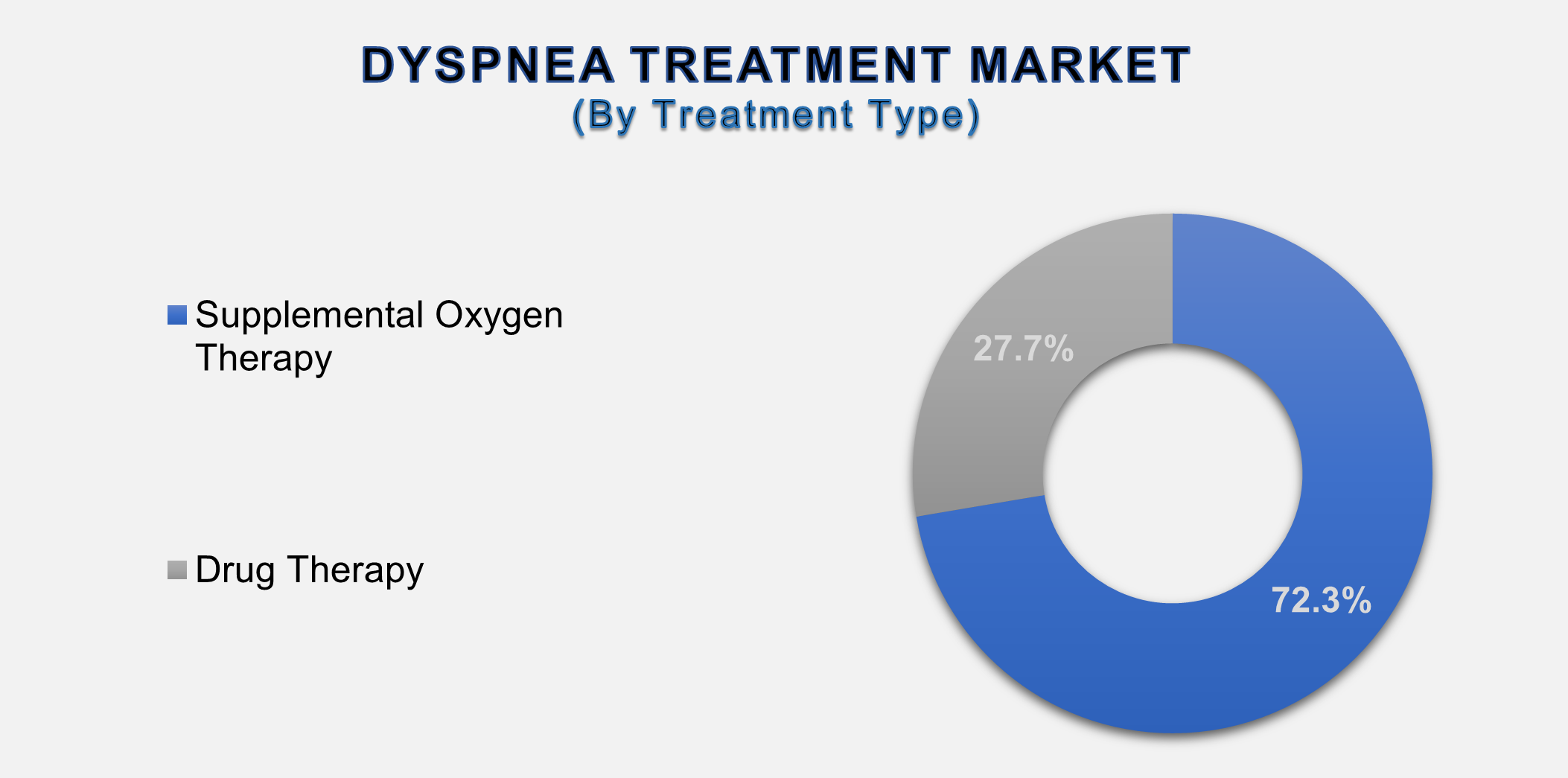

The Drug Therapy

segment dominated the market in 2025 and is projected to grow at the highest

CAGR during the forecast period.

By Treatment Type,

the Dyspnea Treatment Market is segmented into supplemental oxygen therapy and

drug therapy. The drug therapy segment accounts for the largest share of the

global Dyspnea Treatment Market. Drug therapy is essential for managing dyspnea

since it addresses the root causes, which include pulmonary hypertension, heart

failure, asthma, and chronic obstructive pulmonary disease (COPD). This section

covers combination inhalers, corticosteroids, opioids used in palliative care,

bronchodilators (beta-agonists and anticholinergics), and more recent

biologics. More than half of respiratory drug delivery worldwide is

inhalation-based, and inhaled drugs continue to be the favored route because of

their quicker onset and localized action. Pharmaceutical interventions are in

high demand because of the growing prevalence of COPD, which affects over 390

million people worldwide, and asthma, which affects around 260 million people.

The rising use of long-acting bronchodilators and combination therapies is enhancing

symptom management and lowering hospitalization rates, which increases the drug

therapy segment's share of the market for dyspnea treatments overall.

Inhalation holds

the highest share of the Route of Administration Segment over the forecast

period

Based on the Route of Administration, the market is bifurcated into

oral, inhalation, and intravenous. The inhalation segment accounts for the

largest share of the market. The inhalation segment is the most commonly used

route of administration for dyspnea medication therapy because of its quick

onset of action and precise lung delivery. Commonly administered inhaled drugs

are commonly prescribed for conditions such as COPD and asthma, including

combination inhalers, short-acting and long-acting bronchodilators, and inhaled

corticosteroids. More than 55–60% of respiratory drug delivery worldwide is

accomplished through inhalation-based therapies, which, in contrast to oral or

injectable formulations, minimize systemic side effects while offering quicker

symptom relief. The need for inhalers and nebulized drugs is still increasing because

there are over 390 million people with COPD and 260 million people with asthma

worldwide. Technological innovations like metered-dose inhalers (MDIs), dry

powder inhalers (DPIs), and smart inhalers are promoting segment expansion and

improving treatment adherence.

The Hospitals

Segment will probably dominate the market during the forecast period

In terms of End

User, the Dyspnea Treatment Market is segmented into hospitals, specialty

centers, and others. The hospitals segment holds the largest share of the

Dyspnea Treatment Market. The management of acute and severe instances of

dyspnea makes hospitals a significant end-user segment in the dyspnea therapy

industry. Patients who are experiencing heart failure, pneumonia, asthma

attacks, COPD exacerbations, or respiratory difficulties following surgery

frequently need prompt hospital-based assistance, which includes sophisticated

pharmaceutical treatment, oxygen therapy, and nebulization. According to

estimates from the worldwide health community, respiratory conditions cause

millions of hospital admissions every year, with COPD being the most common

reason for emergency room visits. High-flow oxygen therapy, noninvasive

ventilation, and injectable drugs are also primarily administered in hospitals

in critical care settings. In the market for dyspnea therapy, hospitals are a

major revenue-contributing segment because of the presence of specialist

respiratory units, qualified medical staff, and cutting-edge diagnostic

facilities that support early intervention and thorough management.

The following

segments are part of an in-depth analysis of the global Dyspnea Treatment

Market:

|

Market Segments |

|

|

By

Treatment Type |

●

Supplemental

Oxygen Therapy ●

Drug

Therapy |

|

By

Route of Administration |

●

Oral ●

Inhalation

●

Intravenous

|

|

By End

User |

●

Hospitals ●

Specialty

Centers ●

Others |

Dyspnea Treatment Market Share Analysis by

Region

The North America

region is projected to hold the largest share of the global Dyspnea Treatment

Market over the forecast period.

North

America is projected to hold the largest share of the global Dyspnea Treatment

Market during the forecast period. The region’s dominance is attributed to its

advanced healthcare infrastructure, strong reimbursement systems, and high

prevalence of respiratory and cardiovascular diseases. More than 16 million

adults in the U.S. are diagnosed with COPD, and over 25 million people suffer

from asthma, significantly increasing demand for dyspnea-related treatments.

Additionally, annual healthcare expenditure in the U.S. exceeds USD 4 trillion,

supporting access to advanced respiratory therapies and oxygen delivery

systems.

Global

Dyspnea Treatment Market Recent Developments News:

●

In July 2025,

Merck announced a ~$10 billion acquisition of Verona Pharma, a biotech focused

on lung diseases, including COPD treatments that help alleviate dyspnea

symptoms.

●

In December

2025, lightweight, energy-efficient portable oxygen concentrators and

AI-integrated respiratory monitoring tools were introduced, improving

accessibility to dyspnea management outside hospital settings.

The

Global Dyspnea Treatment Market is dominated by a few large companies, such as

●

Novartis AG

●

Boehringer

Ingelheim International GmbH

●

Mayne Pharma

Group Limited

●

Teva

Pharmaceutical Industries Ltd.

●

GlaxoSmithKline

plc

●

Bausch Health

Companies Inc.

●

Hikma

Pharmaceuticals plc

●

Lannett

Company, Inc.

●

Amneal

Pharmaceuticals LLC

●

Viatris Inc.

●

Lupin Limited

●

ANI

Pharmaceuticals, Inc.

●

Pfizer Inc.

●

Sun

Pharmaceutical Industries Ltd.

●

Ligand

Pharmaceuticals Incorporated

●

Nephron

Pharmaceuticals Corporation

●

Zydus

Lifesciences Limited

●

Cipla Limited

●

AstraZeneca

plc

● Aurobindo Pharma Limited

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1.

Global Dyspnea Treatment Market Introduction and Market Overview

1.1.

Objectives of the Study

1.2.

Global Dyspnea Treatment Market Scope and Market Estimation

1.2.1.Global Dyspnea

Treatment Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Dyspnea

Treatment Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market Segmentation

1.3.1.Treatment

Type of Global Dyspnea Treatment Market

1.3.2.Route of

Administration of Global Dyspnea Treatment Market

1.3.3.End User of

Global Dyspnea Treatment Market

2.

Executive

Summary

2.1.

Demand Side Trends

2.2.

Key Market Trends

2.3.

Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand and Opportunity Assessment

2.5.

Market Dynamics

2.5.1.Drivers

2.5.2.Limitations

2.5.3.Opportunities

2.5.4.Impact

Analysis of Drivers and Restraints

2.6.

Porter’s Five Forces Analysis

2.7.

PEST Analysis

2.8.

Key Regulation

2.9.

Key Developments

2.10. Value

Chain / Ecosystem Analysis

3.

Global

Dyspnea Treatment Market Estimates & Historical Trend Analysis (2020 - 2024)

4. Global Dyspnea Treatment Market Estimates & Forecast Trend Analysis, by Treatment Type

4.1.

Global Dyspnea Treatment Market Revenue (US$ Bn) Estimates and

Forecasts, by Treatment Type, 2020 - 2033

4.1.1.Supplemental

Oxygen Therapy

4.1.2.Drug Therapy

5. Global Dyspnea Treatment Market Estimates & Forecast Trend Analysis, by Route of Administration

5.1.

Global Dyspnea Treatment Market Revenue (US$ Bn) Estimates and

Forecasts, by Route of Administration, 2020 - 2033

5.1.1.Oral

5.1.2.Inhalation

5.1.3.Intravenous

6. Global Dyspnea Treatment Market Estimates & Forecast Trend Analysis, by End User

6.1.

Global Dyspnea Treatment Market Revenue (US$ Bn) Estimates and

Forecasts, by End User, 2020 - 2033

6.1.1.Hospitals

6.1.2.Specialty

Centers

6.1.3.Others

7.

Global

Dyspnea Treatment Market Estimates & Forecast Trend Analysis, by Region

7.1.

Global Dyspnea Treatment Market Revenue (US$ Bn) Estimates and

Forecasts, by Region, 2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East

& Africa

7.1.5.Latin America

8.

North America Dyspnea

Treatment Market: Estimates &

Forecast Trend Analysis

8.1.

North America Dyspnea Treatment Market Assessments & Key

Findings

8.1.1.North America

Dyspnea Treatment Market Introduction

8.1.2.North America

Dyspnea Treatment Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Treatment Type

8.1.2.2. By Route of Administration

8.1.2.3. By End User

8.1.2.4.

By Country

8.1.2.4.1.

The U.S.

8.1.2.4.2.

Canada

9.

Europe Dyspnea

Treatment Market: Estimates &

Forecast Trend Analysis

9.1.

Europe Dyspnea Treatment Market Assessments & Key Findings

9.1.1.Europe Dyspnea

Treatment Market Introduction

9.1.2.Europe Dyspnea

Treatment Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Treatment Type

9.1.2.2. By Route of Administration

9.1.2.3. By End User

9.1.2.4. By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Russia

9.1.2.4.7.

Rest

of Europe

10.

Asia Pacific Dyspnea

Treatment Market: Estimates &

Forecast Trend Analysis

10.1. Asia

Pacific Dyspnea Treatment Market Assessments & Key Findings

10.1.1.

Asia Pacific Dyspnea Treatment Market Introduction

10.1.2.

Asia Pacific Dyspnea Treatment Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

10.1.2.1. By Treatment Type

10.1.2.2. By Route of Administration

10.1.2.3. By End User

10.1.2.4.

By Country

10.1.2.4.1.

China

10.1.2.4.2.

Japan

10.1.2.4.3.

India

10.1.2.4.4.

Australia

10.1.2.4.5.

South Korea

10.1.2.4.6. Rest

of Asia Pacific

11.

Middle East & Africa Dyspnea Treatment Market:

Estimates & Forecast Trend Analysis

11.1. Middle

East & Africa Dyspnea Treatment Market Assessments & Key Findings

11.1.1.

Middle East & Africa Dyspnea

Treatment Market Introduction

11.1.2.

Middle East & Africa Dyspnea

Treatment Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Treatment Type

11.1.2.2. By Route of Administration

11.1.2.3. By End User

11.1.2.4.

By Country

11.1.2.4.1.

UAE

11.1.2.4.2.

Saudi Arabia

11.1.2.4.3.

South Africa

11.1.2.4.4. Rest of MEA

12.

Latin America Dyspnea

Treatment Market: Estimates &

Forecast Trend Analysis

12.1. Latin

America Event Industry Assessments & Key Findings

12.1.1.

Latin America Dyspnea Treatment Market Introduction

12.1.2.

Latin America Dyspnea Treatment Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

12.1.2.1. By Treatment Type

12.1.2.2. By Route of Administration

12.1.2.3. By End User

12.1.2.4.

By Country

12.1.2.4.1.

Brazil

12.1.2.4.2.

Mexico

12.1.2.4.3.

Argentina

12.1.2.4.4. Rest of LATAM

13.

Country Wise Market: Introduction

14. Competition

Landscape

14.1. Global

Dyspnea Treatment Market Product Mapping

14.2. Global

Dyspnea Treatment Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3. Global

Dyspnea Treatment Market Tier Structure Analysis

14.4. Global

Dyspnea Treatment Market Concentration & Company Market Shares (%)

Analysis, 2024

15. Company

Profiles

15.1.

Novartis AG

15.1.1.

Company Overview & Key Stats

15.1.2.

Financial Performance & KPIs

15.1.3.

Product Portfolio

15.1.4.

SWOT Analysis

15.1.5.

Business Strategy & Recent Developments

*

Similar details would be provided for all the players mentioned below

15.2.

Boehringer Ingelheim International GmbH

15.3.

Mayne Pharma Group Limited

15.4.

Teva Pharmaceutical Industries Ltd.

15.5.

GlaxoSmithKline plc

15.6.

Bausch Health Companies Inc.

15.7.

Hikma Pharmaceuticals plc

15.8.

Lannett Company, Inc.

15.9.

Amneal Pharmaceuticals LLC

15.10.

Viatris Inc.

15.11.

Lupin Limited

15.12.

ANI Pharmaceuticals, Inc.

15.13.

Pfizer Inc.

15.14.

Sun Pharmaceutical Industries Ltd.

15.15.

Ligand Pharmaceuticals Incorporated

15.16.

Nephron Pharmaceuticals Corporation

15.17.

Zydus Lifesciences Limited

15.18.

Cipla Limited

15.19.

AstraZeneca plc

15.20.

Other Prominent Players

16.

Research

Methodology

16.1. External

Transportations / Databases

16.2. Internal

Proprietary Database

16.3. Primary

Research

16.4. Secondary

Research

16.5. Assumptions

16.6. Limitations

16.7. Report

FAQs

17.

Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables