eClinical Solutions Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product (Electronic Data Capture (EDC) & Clinical Data Management Systems (CDMS), Clinical Trial Management Systems (CTMS), Clinical Analytics Platforms, Randomization and Trial Supply Management (RTSM), Electronic Clinical Outcome Assessment (eCOA), Safety Solutions, and Others), By Delivery Mode (Web-hosted, Licensed Enterprise, Cloud-based), By End-User (Pharmaceutical & Biotech Companies, Contract Research Organizations (CROs), Medical Device Manufacturers, and Others) And Geography

2025-12-03

Healthcare

Swetal (Research Analyst)

Description

eClinical Solutions Market Overview

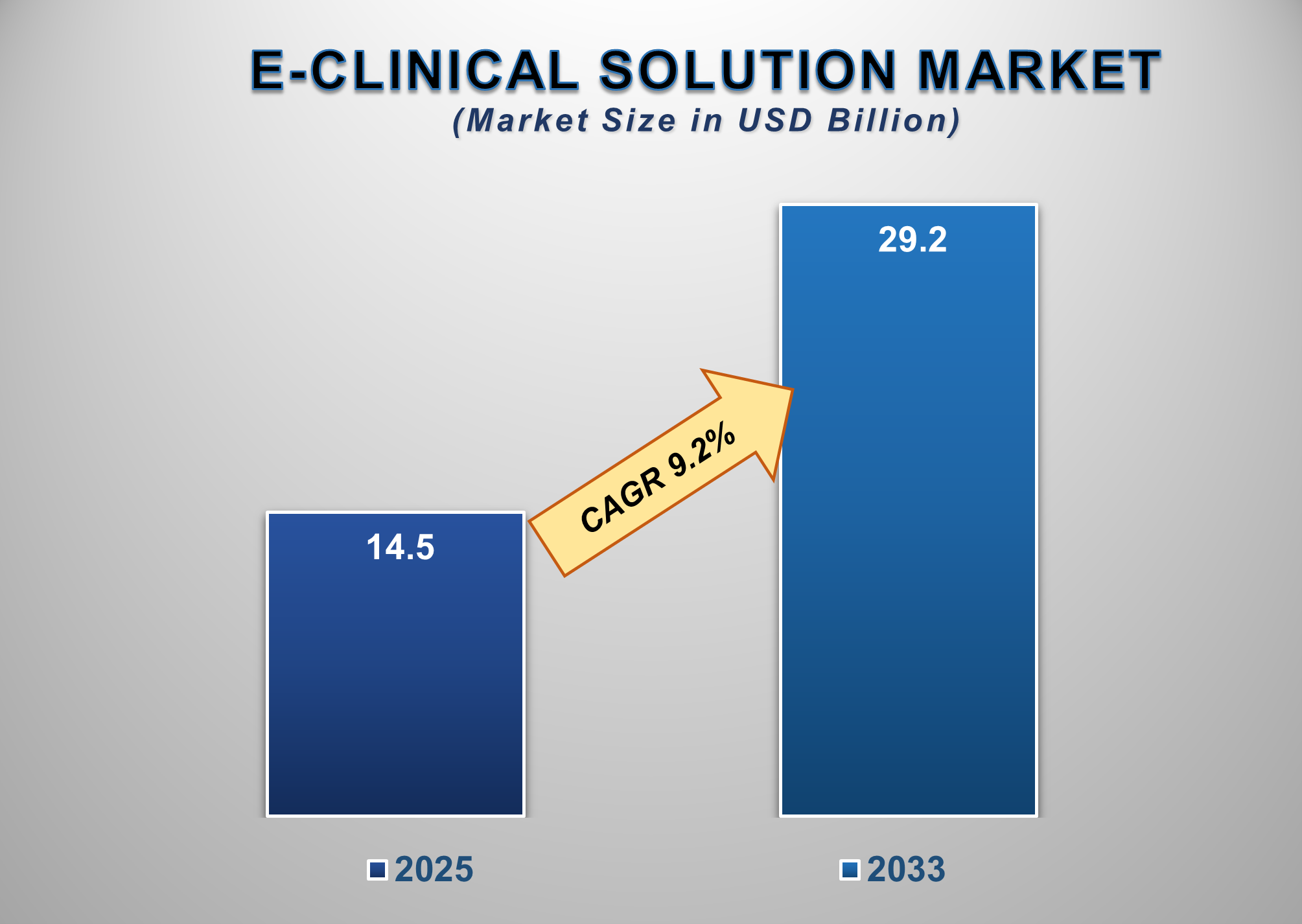

The eClinical Solutions Market is positioned for a period of dynamic and technologically driven growth from 2025 to 2033, fueled by the increasing complexity of clinical trials, a strong pipeline of new therapies, the global shift towards decentralized trials, and the imperative for greater efficiency and data quality in drug development. The market is projected to be valued at approximately USD 14.5 billion in 2025 and is forecasted to reach nearly USD 29.2 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 9.2% during this period.

eClinical solutions encompass a suite of

software technologies used to plan, manage, collect, and analyze data in clinical trials. This includes systems for data

capture (EDC), trial management (CTMS), patient-reported outcomes (eCOA), and

randomization (RTSM), among others. The market's significant expansion is

primarily driven by the pharmaceutical and biotechnology industry's relentless

pursuit of R&D efficiency and faster time-to-market for new drugs.

The adoption of novel trial designs, such as

decentralized clinical trials (DCTs), which rely heavily on digital tools, is a

major growth catalyst. Furthermore, stringent regulatory requirements for data

integrity and the growing volume of complex data from novel therapies are

compelling sponsors and CROs to invest in integrated and advanced eClinical

platforms. North America currently holds the largest market share due to its

high concentration of pharmaceutical companies and early technology adoption,

while the Asia-Pacific region is expected to witness the fastest growth, driven

by increasing clinical trial activity and cost advantages.

eClinical Solutions Market Drivers and Opportunities

The Rising Complexity of Clinical Trials and

the Imperative for R&D Efficiency is the Primary Market Driver

The increasing complexity of clinical trials,

driven by novel therapies (e.g., cell & gene, targeted oncology), adaptive

trial designs, and the need for real-world evidence, is the most powerful force

propelling the eClinical solutions market. Traditional paper-based methods are

incapable of handling the vast, diverse, and complex data generated by modern

trials. eClinical solutions streamline the entire trial lifecycle, from site

selection and patient recruitment to data collection, cleaning, and regulatory

submission. By automating workflows and providing centralized, real-time data

access, these systems significantly reduce trial cycle times, minimize errors,

and lower overall costs. In an industry where delays can cost millions per day,

the efficiency gains offered by integrated eClinical platforms are not just an

advantage but a necessity for maintaining a competitive R&D pipeline.

The global pharmaceutical R&D spending

continues to grow, underscoring the scale of the clinical trials ecosystem. In

2024, global R&D spending is estimated to have exceeded US$250 billion,

with thousands of clinical trials active worldwide. The pipeline of new drugs

is increasingly complex, with a significant portion focused on precision

medicine and biologics, which require more sophisticated data management. This

data highlights the immense operational challenge and the corresponding

opportunity for eClinical solutions to bring order and efficiency to a highly

complex and costly process.

The Paradigm Shift Towards Decentralized

Clinical Trials (DCTs) is Driving Strategic Adoption

The accelerated adoption of decentralized and

hybrid clinical trial models is a powerful catalyst for the eClinical solutions

market. The COVID-19 pandemic acted as a forcing function, demonstrating the

viability of using digital tools to conduct trial activities remotely. DCTs

leverage technologies like eCOA, eConsent, and telehealth to engage patients in

their homes, reducing the burden of site visits and expanding the potential

patient pool. eClinical solutions form the digital backbone of DCTs, enabling

the seamless integration of data from various sources, including wearables and

mobile apps, into the main clinical database. This shift not only enhances

patient centricity and recruitment/retention rates but also improves data

quality through more frequent and real-world data collection. Investing in a flexible and integrated eClinical suite is a strategic priority for sponsors and CROs.

The Integration of Advanced Analytics and the

Push for Interoperability Present Significant Opportunities

The strategic integration of advanced

technologies and the move towards unified platforms are creating significant

growth frontiers for the eClinical solutions market. Key opportunities lie in

the application of Artificial Intelligence (AI) and Machine Learning (ML) to

clinical data. AI-powered tools can automate data cleaning, identify potential

site or patient issues proactively, and even predict clinical outcomes, thereby

enhancing trial quality and speed. Furthermore, there is a strong market push for

interoperable platforms that can break down data silos between different

eClinical systems (e.g., EDC, CTMS, eCOA). For solution providers, investing in

AI-driven analytics modules, developing flexible cloud-native platforms that

can easily integrate with other systems, and offering comprehensive suites that

cover the entire trial continuum are key strategies to capture market share and

deliver greater value to clients.

eClinical Solutions

Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 14.5 Billion |

|

Market Forecast in 2033 |

USD 29.2 Billion |

|

CAGR % 2025-2033 |

9.2% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors, and more |

|

Segments Covered |

●

By Product ●

By Delivery Mode ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

eClinical Solutions

Market Report Segmentation Analysis

The global eClinical Solutions

Market industry analysis is segmented by Product, by Delivery Mode, by

End-User, and by Region.

The Electronic Data Capture (EDC) & CDMS

segment is anticipated to command a significant market share in 2025

The Product segment is categorised into EDC &

CDMS, CTMS, Clinical Analytics Platforms, RTSM, eCOA, Safety Solutions, and

Others. The EDC & CDMS segment holds a substantial and foundational share

of the market, as it represents the core system for collecting,

validating, and managing clinical trial data. The shift from paper Case Report

Forms (CRFs) to EDC has been largely completed in developed regions and is

accelerating globally. The critical importance of high-quality, audit-ready

data for regulatory submissions makes EDC/CDMS an indispensable and

non-negotiable component of virtually every clinical trial. Continuous

innovations, such as user-friendly interfaces, built-in compliance checks, and

integration capabilities with other systems, ensure that this segment remains

the cornerstone of the eClinical ecosystem.

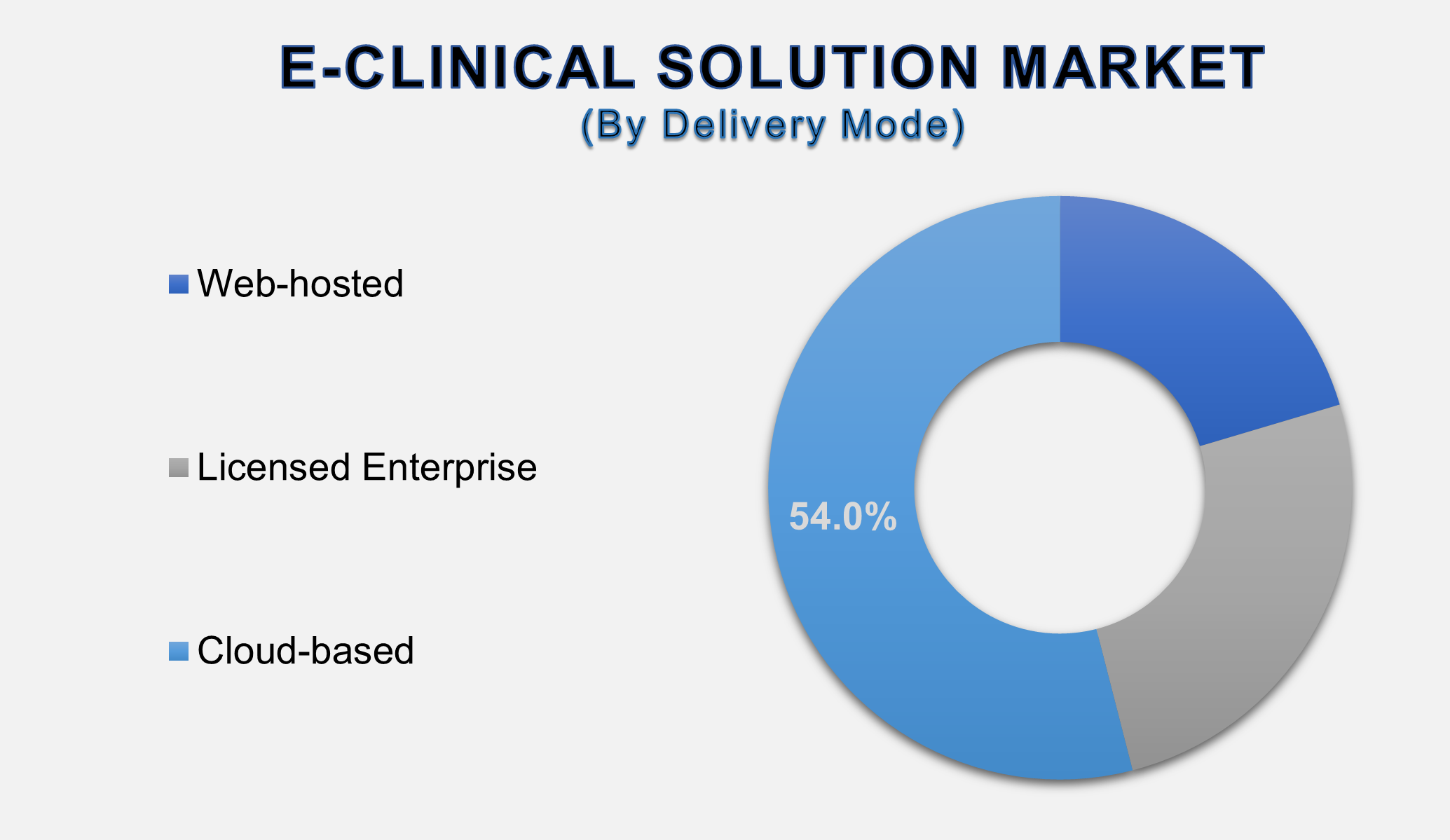

The Cloud-based Delivery Mode segment is

projected to grow at a significant CAGR.

The Delivery Mode segment includes Web-hosted,

Licensed Enterprise, and Cloud-based. The Cloud-based segment's projected

significant growth is driven by its superior scalability, flexibility, and

cost-effectiveness compared to on-premise licensed models. Cloud-based

eClinical solutions eliminate the need for expensive IT infrastructure and

maintenance, allowing even small biotech firms to access enterprise-level

technology. They enable real-time collaboration between globally dispersed

teams and sites, which is crucial for modern trials. The inherent agility of

the cloud also supports the rapid deployment and scaling required for

decentralized trial components. With robust security measures now standard, the

cloud-based SaaS (Software-as-a-Service) model is becoming the preferred

delivery mode for its operational and economic advantages.

The Contract Research Organizations (CROs) end-user

segment is projected to witness the highest growth rate.

The End-User segment is divided into

Pharmaceutical & Biotech Companies, Contract Research Organizations (CROs),

Medical Device Manufacturers, and Others. The CRO segment's position as the

fastest-growing channel is a direct result of the increasing outsourcing of

clinical trial activities by pharmaceutical sponsors. To manage multiple trials

for various clients efficiently and profitably, CROs are heavily investing in

integrated and scalable eClinical platforms that can standardize processes and

improve operational visibility. The competitive landscape among CROs also

drives technology adoption, as the ability to offer sophisticated,

technology-enabled trial execution becomes a key differentiator for winning

contracts. This makes CROs a primary and rapidly expanding customer base for

eClinical solution providers.

The following segments are part of an in-depth analysis of

the global eClinical Solutions Market:

|

Market

Segments |

|

|

By Product |

●

Electronic Data

Capture (EDC) & (CDMS) ●

Clinical Trial

Management Systems (CTMS) ●

Clinical Analytics

Platforms ●

Randomization and

Trial Supply Management (RTSM) ●

Electronic Clinical

Outcome Assessment (eCOA) ●

Safety Solutions ●

Others |

|

By Service |

●

Web-hosted ●

Licensed Enterprise ●

Cloud-based |

|

By End-user |

●

Pharmaceutical &

Biotech Companies ●

Contract Research

Organizations (CROs) ●

Medical Device

Manufacturers ●

Others |

eClinical Solutions

Market Share Analysis by Region

The North America region

is anticipated to hold the largest portion of the eClinical Solutions Market

globally throughout the forecast period.

North America's dominance is attributed to the

presence of a large number of global pharmaceutical and biotechnology

companies, a highly developed healthcare IT infrastructure, and stringent

regulatory standards from the U.S. FDA that encourage digital data submission.

The region is also an early adopter of advanced clinical technologies,

including decentralized trial models and AI-enabled platforms. High R&D

expenditure and a strong presence of leading eClinical solution vendors create

a mature and competitive market, solidifying North America's leading position.

The United States, in particular, is the world's

largest single market for eClinical solutions. The country's robust clinical

trial activity, favorable government initiatives promoting innovation in drug

development, and the high concentration of top-tier CROs and academic research

centers drive continuous demand for advanced and integrated eClinical software.

Major technological advancements and product launches are often first pioneered

in the U.S. market.

eClinical Solutions

Market Competition Landscape Analysis

The global eClinical solutions

market is competitive and features a mix of large, diversified software

companies, specialized best-of-breed providers, and CROs with proprietary

technology platforms. Competition is intensifying and centers on technological

innovation, product integration, regulatory compliance, and global customer

support. Key strategies include heavy investment in R&D for AI and

analytics capabilities, strategic acquisitions to broaden product portfolios,

and a focus on developing unified platforms to offer a seamless user

experience. Partnerships between technology providers and pharmaceutical

companies to co-develop solutions are also common.

Global eClinical

Solutions Market Recent Developments News:

- In February 2025, Medidata Solutions (a Dassault

Systèmes company) launched a new AI-powered module for its clinical cloud

designed to predict patient dropout risk in real-time, allowing for

proactive intervention.

- In December 2024, Veeva Systems announced a

strategic partnership with a global top-10 pharmaceutical company to

implement its unified Veeva Vault Clinical Suite across all its

development programs.

- In October 2024, IQVIA Holdings Inc. reported

strong growth in its technology solutions segment, driven by increased

adoption of its decentralized trial tools and AI-driven trial design

software.

- In August 2024, BioClinica (a subsidiary of LabCorp) received

regulatory clearance for its updated eCOA platform, which includes

enhanced language localization features for global trials.

The Global EClinical Solutions Market Is Dominated by a Few

Large Companies, such as

●

IQVIA Holdings Inc.

●

Medidata Solutions

●

Veeva Systems

●

Oracle Corporation

●

Bio-Optronics

●

Bioclinica (A LabCorp

Company)

●

Parexel International

Corporation (MAAS)

●

ERT (A Clario Company)

●

Datatrak

International, Inc.

●

ArisGlobal LLC

●

CRF Health

●

Signant Health

●

Castor

●

YPrime, LLC

●

Clinical Ink

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global E-Clinical

solutions Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

E-Clinical solutions Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global E-Clinical

solutions Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product Type of Global E-Clinical

solutions Market

1.3.2.Delivery Mode of Global E-Clinical

solutions Market

1.3.3.End-user of Global E-Clinical

solutions Market

1.3.4.Region of Global E-Clinical

solutions Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Market

Entry Strategies

2.7.

Market

Dynamics

2.7.1.Drivers

2.7.2.Limitations

2.7.3.Opportunities

2.7.4.Impact Analysis of Drivers

and Restraints

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

3. Global

E-Clinical solutions Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

E-Clinical solutions Market Estimates

& Forecast Trend Analysis, by Product Type

4.1.

Global

E-Clinical solutions Market Revenue (US$ Bn) Estimates and Forecasts, by Product

Type, 2020 - 2033

4.1.1.Repairs & Returns

4.1.2.Commercial Returns

4.1.3.End-of-Life Returns

4.1.4.Recalls

5. Global

E-Clinical solutions Market Estimates

& Forecast Trend Analysis, by Delivery Mode

5.1.

Global

E-Clinical solutions Market Revenue (US$ Bn) Estimates and Forecasts, by Delivery

Mode, 2020 - 2033

5.1.1.Returns Management

5.1.2.Refurbishment

5.1.3.Remanufacturing

5.1.4.Packaging

5.1.5.Others

6. Global

E-Clinical solutions Market Estimates

& Forecast Trend Analysis, by End-user

6.1.

Global

E-Clinical solutions Market Revenue (US$ Bn) Estimates and Forecasts, by End-user

2020 - 2033

6.1.1.E-commerce

6.1.2.Automotive

6.1.3.Pharmaceutical

6.1.4.Consumer Electronics

6.1.5.Retail

6.1.6.Others

7. Global

E-Clinical solutions Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

E-Clinical solutions Market Revenue (US$ Bn) Estimates and Forecasts, by region,

2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America E-Clinical

solutions Market: Estimates &

Forecast Trend Analysis

8.1. North America E-Clinical

solutions Market Assessments & Key Findings

8.1.1.North America E-Clinical

solutions Market Introduction

8.1.2.North America E-Clinical

solutions Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Product Type

8.1.2.2.

By Delivery Mode

8.1.2.3.

By End-user

8.1.2.4. By Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe E-Clinical

solutions Market: Estimates &

Forecast Trend Analysis

9.1. Europe E-Clinical

solutions Market Assessments & Key Findings

9.1.1.Europe E-Clinical

solutions Market Introduction

9.1.2.Europe E-Clinical

solutions Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Product Type

9.1.2.2.

By Delivery Mode

9.1.2.3.

By End-user

9.1.2.4. By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific E-Clinical

solutions Market: Estimates &

Forecast Trend Analysis

10.1. Asia Pacific Market

Assessments & Key Findings

10.1.1.

Asia

Pacific E-Clinical solutions Market Introduction

10.1.2.

Asia

Pacific E-Clinical solutions Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

10.1.2.1.

By Product Type

10.1.2.2.

By Delivery Mode

10.1.2.3.

By End-user

10.1.2.4. By Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa E-Clinical

solutions Market: Estimates &

Forecast Trend Analysis

11.1. Middle East & Africa

Market Assessments & Key Findings

11.1.1. Middle

East & Africa

E-Clinical solutions Market Introduction

11.1.2. Middle

East & Africa

E-Clinical solutions Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Product Type

11.1.2.2.

By Delivery Mode

11.1.2.3.

By End-user

11.1.2.4. By Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

E-Clinical solutions Market: Estimates

& Forecast Trend Analysis

12.1. Latin America Market

Assessments & Key Findings

12.1.1. Latin America E-Clinical

solutions Market Introduction

12.1.2. Latin America E-Clinical

solutions Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Product Type

12.1.2.2.

By Delivery Mode

12.1.2.3.

By End-user

12.1.2.4. By Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13.

Country

Wise Market: Introduction

14.

Competition

Landscape

14.1. Global E-Clinical

solutions Market Product Mapping

14.2. Global E-Clinical

solutions Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3. Global E-Clinical

solutions Market Tier Structure Analysis

14.4. Global E-Clinical

solutions Market Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

IQVIA Holdings Inc.

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2.

Medidata Solutions

15.3.

Veeva Systems

15.4.

Oracle Corporation

15.5.

Bio-Optronics

15.6.

Bioclinica (A LabCorp Company)

15.7.

Parexel International Corporation (MAAS)

15.8.

ERT (A Clario Company)

15.9.

Datatrak International, Inc.

15.10.

ArisGlobal LLC

15.11.

CRF Health

15.12.

Signant Health

15.13.

Castor

15.14.

YPrime, LLC

15.15.

Clinical Ink

15.16.

Other Prominent Players

16. Research

Methodology

16.1. External Transportations /

Databases

16.2. Internal Proprietary

Database

16.3. Primary Research

16.4. Secondary Research

16.5. Assumptions

16.6. Limitations

16.7. Report FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables