Edge Computing Market Size and Forecast (2025 – 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Component (Hardware, Application/Software, Edge Cloud Infrastructure, Services, Network); By Enterprise Type (Small & Medium-sized Enterprises (SMEs), Large Enterprises); By Application (IoT Applications, Robotics & Automation, Predictive Maintenance, Remote Monitoring, Smart Cities, Others); By Industry (Manufacturing, Oil & Gas, BFSI, Healthcare, Retail, IT & Telecom, Automotive, Others); and Geography.

2025-09-10

ICT

Ekta Chaurasia (Team Lead)

Description

Edge Computing Market Overview

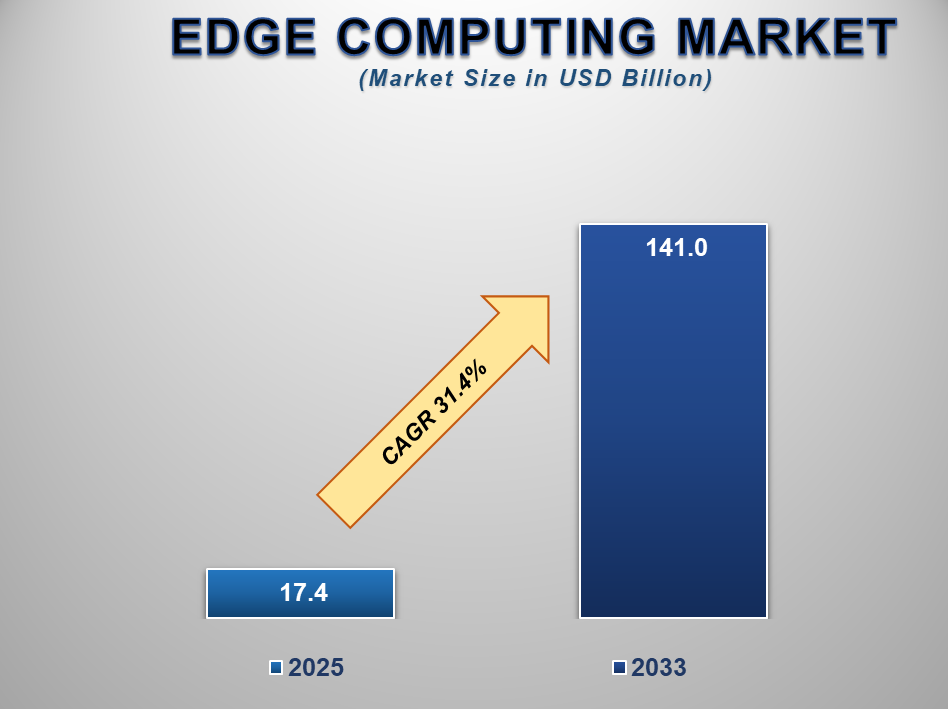

The global Edge Computing Market is experiencing exponential growth, driven by rapid digital transformation, the proliferation of IoT devices, and the increasing need for low-latency data processing. Valued at USD 17.4 billion in 2025, the market is projected to reach USD 141.0 billion by 2033, expanding at a remarkable CAGR of 31.4% during the forecast period.

Edge computing represents a

paradigm shift from centralized cloud computing to localized data processing

closer to the data source. This enables real-time decision-making, reduces

latency, improves bandwidth efficiency, and enhances overall network performance.

The rise of connected devices, autonomous systems, and smart cities has

significantly boosted demand for edge solutions across industries such as

manufacturing, healthcare, BFSI, IT & telecom, automotive, and energy.

Technological advancements, including AI integration, 5G rollout, and hybrid

cloud strategies, are further accelerating adoption. Enterprises are

increasingly deploying edge computing infrastructure to improve operational

efficiency, ensure data security, and handle mission-critical workloads.

Edge Computing Market

Drivers and Opportunities

Expanding IoT ecosystem drives the global Edge Computing

market

The explosive growth of IoT

devices is one of the primary factors fueling demand for edge computing.

Billions of connected sensors, smart devices, and industrial machines generate

massive amounts of data daily, overwhelming traditional centralized cloud systems.

Edge computing enables this data to be processed locally, improving efficiency,

reducing latency, and ensuring real-time insights. For industries like

manufacturing, energy, and healthcare, such low-latency processing is essential

for predictive maintenance, automation, and patient monitoring. With

IoT-enabled smart homes, connected vehicles, and wearable devices gaining

mainstream acceptance, edge computing provides the required scalability and

speed to handle the data influx. Furthermore, the advent of 5G networks

enhances the performance of IoT ecosystems by supporting high-speed

connectivity and ultra-reliable communications, which complements edge

deployments. Enterprises are recognizing that cloud-only models cannot keep up

with the pace of IoT data generation, making edge computing indispensable. This

expansion of IoT across consumer, industrial, and enterprise applications

ensures sustained growth for the global edge computing market.

Rising need for real-time data processing boosts the Edge

Computing market

The increasing reliance on

real-time applications across industries is a significant driver of the edge

computing market. Applications such as autonomous vehicles, robotics,

augmented/virtual reality (AR/VR), and financial trading systems demand

ultra-low latency and immediate responsiveness, which cloud computing alone

cannot provide. Edge computing bridges this gap by bringing computation closer

to data sources, enabling instant analysis and action. For instance, autonomous

vehicles must process sensor data locally to make split-second decisions, while

in healthcare, real-time monitoring of patient vitals requires immediate

analysis to prevent emergencies. The retail sector also benefits, as edge

solutions enable personalized shopping experiences through instant analytics.

Additionally, mission-critical sectors such as defense, utilities, and energy

are increasingly relying on edge computing to enhance operational resilience

and cybersecurity. As digital transformation deepens across industries, the demand

for real-time, localized data processing grows stronger, making edge computing

a core component of enterprise IT infrastructure and fueling market expansion.

Opportunity for the Edge Computing Market

Integration with AI and 5G presents lucrative opportunities

for the Edge Computing market

The convergence of edge computing with artificial intelligence (AI) and 5G connectivity is creating transformative opportunities for the global market. AI requires massive amounts of data for training and decision-making, and when combined with edge computing, it enables intelligent, real-time insights at the device level. For example, AI-powered cameras in smart cities can detect anomalies instantly, while AI-enabled robots in manufacturing can optimize production on the fly. The rollout of 5G networks further enhances these capabilities by delivering ultra-low latency and high bandwidth, making edge deployments faster and more reliable. Telecom operators are leveraging 5G-enabled edge infrastructure to provide new services such as network slicing and ultra-reliable low-latency communications (uRLLC). Moreover, the combination of AI, 5G, and edge opens new avenues in sectors like telemedicine, immersive entertainment, predictive analytics, and autonomous mobility. As enterprises seek intelligent, connected, and responsive systems, the integration of these technologies positions edge computing as a central enabler of next-generation digital ecosystems.

Edge Computing Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 17.4 Billion |

|

Market Forecast in 2033 |

USD 141.0 Billion |

|

CAGR % 2025-2033 |

31.4% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production Capacity, growth factors and more |

|

Segments Covered |

●

By Component ●

By Enterprise Type ●

By Application ●

By Industry |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Edge Computing Market Report Segmentation Analysis

The global Edge Computing Market

industry analysis is segmented by component, by enterprise type, by

application, by industry, and by region.

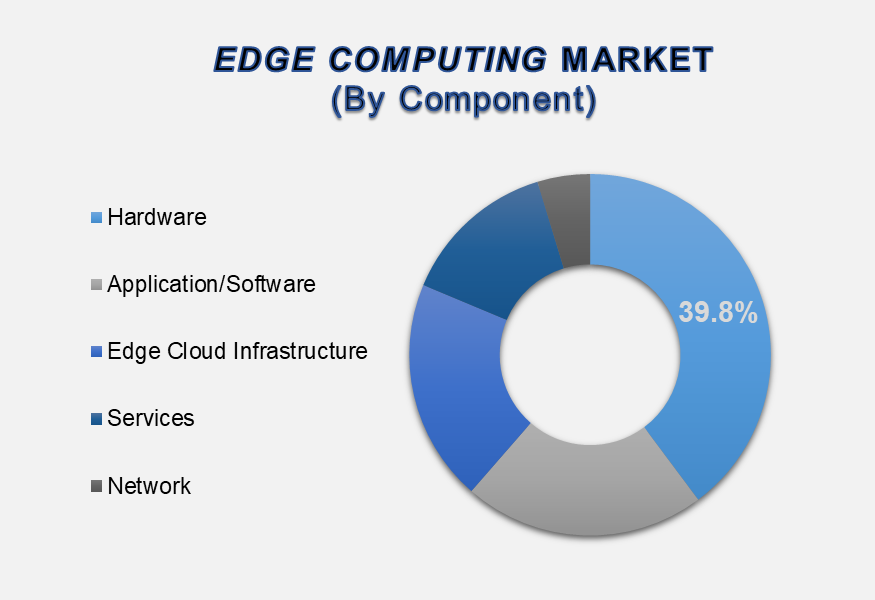

The Hardware segment accounted for the largest market share in the global Edge Computing market

By component, the market is divided into Hardware, Application/Software, Edge Cloud Infrastructure, Services, and Network. The hardware segment held the largest share at 39.8% in 2025. This dominance is attributed to the rising demand for edge servers, gateways, and IoT devices that enable localized data processing. Hardware plays a crucial role in managing workloads and ensuring low latency in mission-critical applications. With the proliferation of connected devices, industries such as manufacturing, healthcare, and retail require scalable hardware solutions for real-time analytics and automation. Continuous innovation in processors, GPUs, and microchips designed for AI and machine learning at the edge is further driving the segment. Companies like Intel, NVIDIA, and Huawei are heavily investing in hardware development to meet growing enterprise needs. Additionally, the rollout of 5G infrastructure is increasing demand for specialized edge devices, further reinforcing the hardware segment’s market leadership.

The IoT Applications segment accounted for the largest market

share in the global Edge Computing market

By application, the market is

categorized into IoT Applications, Robotics & Automation, Predictive

Maintenance, Remote Monitoring, Smart Cities, and Others. The IoT Applications

segment dominated in 2025, supported by the rapid expansion of smart homes,

industrial IoT, and connected devices. Edge computing provides the backbone for

IoT ecosystems by processing vast data streams locally, reducing latency, and

enhancing performance. For industries like automotive and logistics,

IoT-enabled edge solutions help improve fleet management, asset tracking, and

predictive maintenance. In healthcare, IoT sensors supported by edge

infrastructure enable continuous patient monitoring and real-time response. The

retail sector also benefits from IoT applications such as smart shelves,

customer analytics, and inventory management. Growing adoption of 5G technology

is expected to further accelerate IoT-driven edge deployments. The expanding

IoT ecosystem across consumer and industrial domains cements this segment’s

dominance in the global market.

The IT & Telecom segment accounted for the largest market

share in the global Edge Computing market

By industry, the market is

segmented into Manufacturing, Oil & Gas, BFSI, Healthcare, Retail, IT &

Telecom, Automotive, and Others. The IT & Telecom segment led the market in

2025, fueled by the industry’s early adoption of advanced edge technologies and

the growing demand for enhanced connectivity solutions. Telecom operators are

integrating edge computing with 5G infrastructure to provide high-speed,

low-latency services for enterprises and consumers. IT service providers are

deploying edge solutions to support data-intensive applications, AI models, and

real-time analytics. Furthermore, the telecom industry leverages edge

infrastructure for network slicing and cloud-native services, improving

customer experience and reducing operational costs. The expansion of cloud-native

technologies and partnerships between IT firms and telecom providers is also

driving this segment. As data consumption and mobile usage surge globally, IT

& telecom remain key verticals propelling the edge computing market.

The following segments are part

of an in-depth analysis of the global Edge Computing Market:

|

Market Segments |

|

|

By Component |

●

Hardware ●

Application/Software ●

Edge Cloud

Infrastructure ●

Services ●

Network |

|

By Enterprise Type |

●

Small &

Medium-sized Enterprises (SMEs) ●

Large Enterprises |

|

By Application |

●

IoT Applications ●

Robotics &

Automation ●

Predictive

Maintenance ●

Remote Monitoring ●

Smart Cities ●

Others |

|

By Industry |

●

Manufacturing ●

Oil & Gas ●

BFSI ●

Healthcare ●

Retail ●

IT & Telecom ●

Automotive ●

Others |

Edge Computing Market

Share Analysis by Region

The North America region is projected to hold the largest

share of the global edge computing market over the forecast period.

North America accounted for the

largest share of the global Edge Computing Market in 2025, with 38.9%. The

region’s dominance is driven by strong digital infrastructure, early adoption

of cloud-native and edge technologies, and significant investments in 5G

deployment. Major technology providers, including AWS, Microsoft, Google, and

IBM, are headquartered in the region and actively expanding their edge

portfolios. Industries such as healthcare, manufacturing, and BFSI in the U.S.

and Canada are increasingly deploying edge solutions for real-time analytics,

automation, and secure data processing. Moreover, supportive government

initiatives, favorable regulatory environments, and high enterprise IT spending

further strengthen North America’s leadership in this space.

The Asia Pacific region, however,

is projected to record the fastest CAGR during 2025–2033. Countries such as

China, Japan, South Korea, and India are investing heavily in 5G rollouts,

smart manufacturing, and smart city projects. Rapid urbanization, increasing

mobile usage, and the expansion of IoT ecosystems are creating strong demand

for edge computing solutions across sectors like retail, automotive, and

telecommunications. Government-led digital transformation initiatives and the

rise of local technology providers further accelerate market growth. With its

expanding population base and rising enterprise digitization, APAC is poised to

emerge as the most dynamic and fastest-growing regional market for edge

computing in the coming years.

Edge Computing Market Competition Landscape Analysis

The global

Edge Computing Market is highly competitive, with key players focusing on

technological innovation, strategic partnerships, and cloud-edge integration.

Leading companies include Amazon Web Services (AWS), Microsoft Azure, Google

Cloud, IBM, Cisco Systems, Dell Technologies, Hewlett Packard Enterprise (HPE),

Intel, NVIDIA, Huawei, Siemens, and Schneider Electric. These players are

investing heavily in AI-driven edge platforms, specialized hardware, and

5G-enabled solutions. Startups such as FogHorn Systems, ClearBlade, and Litmus

Automation are also contributing to innovation in niche areas like industrial

IoT and real-time analytics. Strategic collaborations between telecom providers

and edge solution vendors are expanding the global market footprint.

Global Edge Computing

Market Recent Developments News:

- In June 2025 – HPE and KDDI announced a

collaboration to launch the Osaka Sakai AI Data Center by early 2026. The

facility will deploy NVIDIA GB200 NVL72 rack-scale systems with HPE’s

hybrid cooling technology, supporting AI application development and large

language model (LLM) training. The center integrates sustainable

infrastructure with NVIDIA-accelerated services via KDDI’s WAKONX

platform, enabling advanced AI capabilities with reduced environmental

impact.

- In June 2025 – VAST Data and Cisco expanded their

strategic alliance, combining VAST’s AI Operating System with Cisco UCS

servers, Nexus switching, and HyperFabric AI to deliver a unified,

zero-trust infrastructure blueprint. This turnkey solution streamlines

data pipelines from edge to core to cloud, accelerates enterprise AI

deployment, and enhances real-time intelligent decision-making worldwide.

- In May 2025 – AWS activated a Wavelength Zone within Verizon’s 5G

network in Lenexa, Kansas, embedding EC2, EBS, VPC, and other AWS services

directly at the network edge. This deployment enables Midwest customers in

finance, healthcare, gaming, and the public sector to run

latency-sensitive workloads locally while meeting strict data-residency

and resiliency requirements.

The Global Edge Computing Market is dominated by a few large

companies, such as

●

Amazon Web Services

(AWS)

●

Microsoft Azure

●

Google Cloud

●

IBM

●

Cisco Systems

●

Dell Technologies

●

Hewlett-Packard

Enterprise (HPE)

●

Intel

●

NVIDIA

●

Huawei

●

Siemens

●

Schneider Electric

●

General Electric (GE)

●

Honeywell

●

Litmus Automation

●

FogHorn Systems

●

ClearBlade

●

ADLINK Technology

●

Moxa

●

SixSq

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

- Global Edge Computing Market Introduction and Market Overview

- Objectives of the Study

- Global Edge Computing Market Scope and Market Estimation

- Global Edge Computing Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Edge Computing Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

- Market Segmentation

- Component of Global Edge Computing Market

- Enterprise Type of Global Edge Computing Market

- Application of Global Edge Computing Market

- Industry of Global Edge Computing Market

- Region of Global Edge Computing Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Edge Computing Market

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Edge Computing Market Estimates & Historical Trend Analysis (2020 - 2024)

- Global Edge Computing Market Estimates & Forecast Trend Analysis, by Component

- Global Edge Computing Market Revenue (US$ Bn) Estimates and Forecasts, by Component, 2020 - 2033

- Hardware

- Application/Software

- Edge Cloud Infrastructure

- Services

- Network

- Global Edge Computing Market Revenue (US$ Bn) Estimates and Forecasts, by Component, 2020 - 2033

- Global Edge Computing Market Estimates & Forecast Trend Analysis, by Enterprise Type

- Global Edge Computing Market Revenue (US$ Bn) Estimates and Forecasts, by Enterprise Type, 2020 - 2033

- Small & Medium-sized Enterprises (SMEs)

- Large Enterprises

- Global Edge Computing Market Revenue (US$ Bn) Estimates and Forecasts, by Enterprise Type, 2020 - 2033

- Global Edge Computing Market Estimates & Forecast Trend Analysis, by Application

- Global Edge Computing Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- IoT Applications

- Robotics & Automation

- Predictive Maintenance

- Remote Monitoring

- Smart Cities

- Others

- Global Edge Computing Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- Global Edge Computing Market Estimates & Forecast Trend Analysis, by Industry

- Global Edge Computing Market Revenue (US$ Bn) Estimates and Forecasts, by Industry, 2020 - 2033

- Manufacturing

- Oil & Gas

- BFSI

- Healthcare

- Retail

- IT & Telecom

- Automotive

- Others

- Global Edge Computing Market Revenue (US$ Bn) Estimates and Forecasts, by Industry, 2020 - 2033

- Global Edge Computing Market Estimates & Forecast Trend Analysis, by region

- Global Edge Computing Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Edge Computing Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020 - 2033

- North America Edge Computing Market: Estimates & Forecast Trend Analysis

- North America Edge Computing Market Assessments & Key Findings

- North America Edge Computing Market Introduction

- North America Edge Computing Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Component

- By Enterprise Type

- By Application

- By Industry

- By Country

- The U.S.

- Canada

- North America Edge Computing Market Assessments & Key Findings

- Europe Edge Computing Market: Estimates & Forecast Trend Analysis

- Europe Edge Computing Market Assessments & Key Findings

- Europe Edge Computing Market Introduction

- Europe Edge Computing Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Component

- By Enterprise Type

- By Application

- By Industry

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Switzerland

- Rest of Europe

- Europe Edge Computing Market Assessments & Key Findings

- Asia Pacific Edge Computing Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Edge Computing Market Introduction

- Asia Pacific Edge Computing Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Component

- By Enterprise Type

- By Application

- By Industry

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Edge Computing Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Edge Computing Market Introduction

- Middle East & Africa Edge Computing Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Component

- By Enterprise Type

- By Application

- By Industry

- By Country

- South Africa

- UAE

- Saudi Arabia

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Edge Computing Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Edge Computing Market Introduction

- Latin America Edge Computing Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Component

- By Enterprise Type

- By Application

- By Industry

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Edge Computing Market Product Mapping

- Global Edge Computing Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Edge Computing Market Tier Structure Analysis

- Global Edge Computing Market Concentration & Company Market Shares (%) Analysis, 2023

- Company Profiles

- Amazon Web Services (AWS)

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Amazon Web Services (AWS)

* Similar details would be provided for all the players mentioned below

- Microsoft Azure

- Google Cloud

- IBM

- Cisco Systems

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Intel

- NVIDIA

- Huawei

- Siemens

- Schneider Electric

- General Electric (GE)

- Honeywell

- Litmus Automation

- FogHorn Systems

- ClearBlade

- ADLINK Technology

- Moxa

- SixSq

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables