Electric Bus Market Size And Forecast (2020 - 2033), Global And Regional Growth, Trend, Share And Industry Analysis Report Coverage: By Propulsion Type (Battery Electric Vehicle (BEV), Plug-In Hybrid Electric Vehicle (PHEV), Fuel Cell Electric Vehicle (FCEV), By Battery Type (Lithium Nickel Manganese Cobalt Oxide, Lithium Iron Phosphate), By Application (Intercity, Intracity) By End Use (Public, Private) And Geography

2025-10-31

Automotive & Transportation (Mobility)

Ekta Chaurasia (Team Lead)

Description

Electric Bus Market Overview

The global Electric Bus Market Size is projected to grow significantly from 2025 to 2033, driven by the ongoing shift toward sustainable urban mobility and stringent government policies aimed at reducing vehicular emissions. By 2025, the market is expected to reach approximately USD 31.4 billion, expanding further to about USD 88.8 billion by 2033, reflecting a CAGR of 14.3% over the forecast period.

Electric buses serve as a

cornerstone of eco-friendly public transportation by offering zero emissions

and lower operational costs. Rising environmental concerns over traditional

fossil-fueled vehicles are a primary growth driver, with governments worldwide

providing subsidies, tax incentives, and regulatory mandates to accelerate the adoption

of electric buses. Additionally, escalating fuel costs and the need for

energy-efficient transit solutions are motivating agencies to replace

conventional buses with electric alternatives. Advancements in charging

infrastructure, battery swapping systems, and fast-charging technologies are

further fueling market expansion.

Electric Bus Market

Drivers and Opportunities

Growing urbanization and public transit demand are

anticipated to lift the electric bus market during the forecast period

The fast pace of global

urbanization has substantially raised the stakes for efficient and sustainable

public transportation networks. Cities are witnessing an unprecedented growth

in population density, which is resulting in higher traffic congestion,

increased pollution, and increased burden on existing transport infrastructure.

Electric buses provide an eco-friendly, noiseless, and cost-effective mode of

addressing urban mobility needs. As the number of people flowing into the

cities is on the rise, municipalities are adopting smart transport networks to

manage increasing commuter traffic, and electric buses are becoming an

essential element of these networks. These buses not only cut operational cost

because of reduced fuel and maintenance expenditure but are also in line with

the environmental aspirations of the city. Moreover, city planning is becoming

increasingly oriented toward enhancing public transit to decrease the

dependency on private transport, and the role of electric buses is at the forefront

of these endeavors. The flexibility and scalability of the range of electric

buses are well-suited to different route lengths and city structures.

Furthermore, real-time data monitoring and management features are enhancing

the performance of services, which is further adding to the prospects of

adoption. As populations in the city are anticipated to grow extensively in the

decades to come, the demand for the role of electric buses in future-proofed

city transit networks is expected to rise, positioning urbanization as an

important growth catalyst.

Government policies and emission regulations are vital

drivers for influencing the growth of the global electric bus market

Government regulations and

emission standards are crucial drivers for the growth of the global market for

electric buses. Across the globe, governments and local governments are

implementing strict standards on emissions as an effort to reduce increasing

levels of air pollution and fulfill environmental obligations under global

treaties such as the Paris Climate Agreement. The regulations are forcing the

replacement of diesel buses with electric versions, which emit zero tailpipe

pollutants. For example, China’s New Energy Vehicle (NEV) policy and the Clean

Vehicles Directive in Europe strongly accelerated the demand for electric

buses. Moreover, financial subsidies, which are in the form of cash subsidies,

discounts on registration fees, and tax relief, are motivating public transport

providers to switch fleets. Besides environmental requirements, governments are

providing the industry with low-interest loans and investment in the expansion

of infrastructure, mainly the establishment of charging points for electric

vehicles (EVs). Cities with poor air quality are also implementing requirements

where the operating public transit fleets need to include a proportion of

transit vehicles as electric, thereby giving rise to a strong demand. These

policies are not only increasing demand but also driving innovation as Original

Equipment Manufacturers (OEMs) are trying to achieve compliance with changing

standards. As governments continue to impose tightening standards, the market

is poised to witness sustained growth, with public policy being an integral

driver in the anticipated market growth.

Public-Private Partnerships (PPPs) for fleet electrification are

poised to create significant opportunities in the global electric bus market

The growth of public-private

partnerships (PPPs) is opening opportunities for large-scale growth in the

global market for electric buses. As governments seek to green public transit

fleets to reach environmental needs, scant public funds and technical capacity

frequently become an impediment. PPPs provide municipal and regional

governments with the ability to partner with private sector firms to

co-develop, finance, and operate networks of electric buses. These arrangements

can extend to the procurement of vehicles, infrastructure rollout, maintenance

services, and energy supply management. For instance, private sector firms

specializing in fleet management or green energy are partnering with transit

agencies to deliver integrated packages that guarantee low-carbon operation.

These collaborations also de-risk investment by spreading responsibility and

ensuring that ventures take advantage of private sector innovation and prowess

for efficiency. In addition, these arrangements can spur market take-up by

lowering the upfront capital burden on transport agencies. PPP models are being

increasingly backed by climate funds and international development banks,

further underpinning the trend. As global cities implement climate action

plans, PPPs will play the key role in transitioning to large-scale populations

of electric buses and related infrastructure. The success of these

collaborations in pilot areas is acting as a template for replication and is

therefore one of the key growth opportunities in the forecasted market.

Electric Bus Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 31.4 Billion |

|

Market Forecast in 2033 |

USD 88.8 Billion |

|

CAGR % 2025-2033 |

14.3% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production capacity, growth factors and more |

|

Segments Covered |

●

By Propulsion Type ●

By Battery Type ●

By Application ●

By End Use |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Russia 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19) South Africa |

Electric Bus Market Report Segmentation Analysis

The Global Electric Bus Market

industry analysis is segmented by Propulsion Type, by Battery Type, by

Application, by End Use, and by Region.

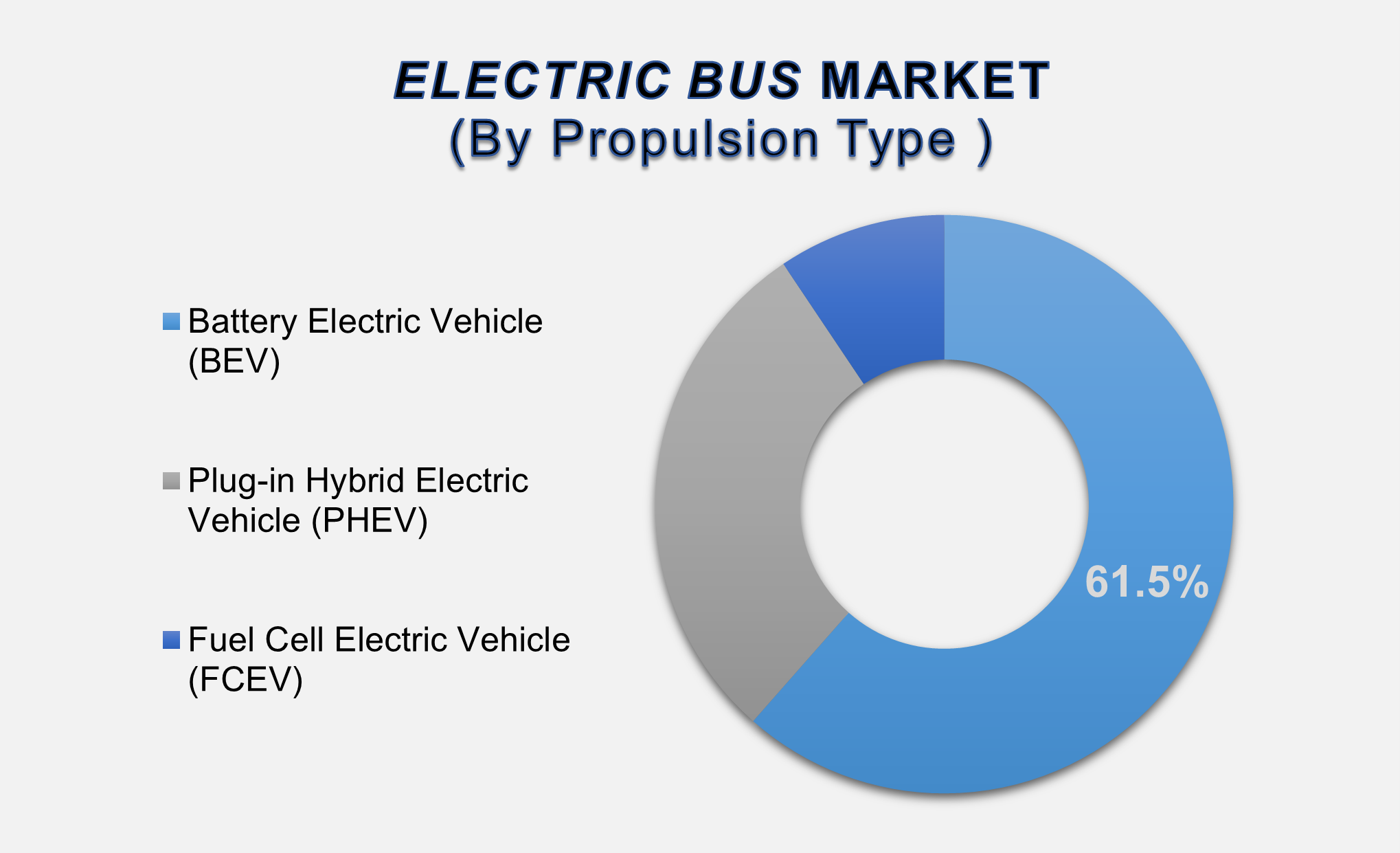

The Battery Electric Vehicle (BEV) segment is anticipated to

hold the highest share of the global electric bus market during the projected

timeframe

Based on the Propulsion Type market is segmented into Battery Electric Vehicle (BEV), Plug-in Hybrid Electric Vehicle (PHEV), and Fuel Cell Electric Vehicle (FCEV). The market is led by the Battery Electric Vehicle (BEV) during the forecast period. BEVs are powered by electricity alone and do not emit tailpipe exhaust, fitting well within global sustainability agendas and city clean-air programs. BEV acquisition is heavily subsidized by governments in various regions through cash incentives, tax credits, and subsidies, particularly for public transit. BEVs also enjoy the benefit of an existing charging network and lower maintenance costs compared to PHEVs and FCEVs. BEVs are most in demand for metropolitan applications because of the quiet operation, improved energy economy, and enhanced battery technologies that provide greater ranges and better charging rates.

The Lithium Iron Phosphate segment dominated the market in

2024 and is predicted to grow at the highest CAGR over the forecast period

By battery type, the market is

categorized into Lithium Nickel Manganese Cobalt Oxide (NMC) and Lithium Iron

Phosphate (LFP). The LFP battery segment in 2024 became the top pick and is set

to advance at the highest CAGR during the forecast period. The LFP batteries

are most commonly known for excellent thermal and chemical stability, long

lifespan, and safety features. These features render them highly suitable for

electric buses, whose frequent use demands high dependability and longevity.

The cost-effectiveness is also delivered through the absence of costly cobalt

and nickel metals, making them an affordable option for mass transit networks.

The concern for better fire safety and battery lifespan is further fueling the

growth of LFP through various global marketplaces.

The Intracity segment is predicted to grow at the highest

CAGR over the forecast period

Based on application, the global

electric bus market is segmented into Intercity and Intracity services. The

Intracity segment is anticipated to grow at the highest CAGR in the forecast

period, driven by the fast pace of electricalization of public transportation

networks within the city. Governments and municipal authorities are both

investing in fleets of electric buses to mitigate traffic-related emissions,

decongest the city, and align with climate requirements. Moreover, increasing

environmental consciousness among the public and government regulations on

clean city transport are further fueling the demand for electric intracity

buses.

The Public segment is expected to dominate the market during

the forecast period.

Based on end use, the market is

divided into the Public and Private sectors. The Public segment is expected to

dominate the market during the forecast period, accounting for the largest

share in terms of both volume and value. Public transportation authorities

across the globe are leading the transition from conventional diesel fleets to

electric alternatives to combat air pollution and reduce greenhouse gas

emissions. Governments are implementing regulatory mandates, offering funding

programs, and rolling out city-level initiatives that prioritize electric bus

deployment in public transit systems. Public agencies often operate large

fleets, which allows for economies of scale and greater impact in emission

reduction. Given the environmental urgency and public demand for cleaner

transportation options, the public end-use segment is set to drive major market

trends, contributing significantly to the forecasted expansion of the global

electric bus market.

The following segments are part of an in-depth analysis of the global

electric bus market:

|

Market Segments |

|

|

By Propulsion Type |

●

Battery Electric

Vehicle (BEV) ●

Plug-in Hybrid

Electric Vehicle (PHEV) ●

Fuel Cell Electric

Vehicle (FCEV) |

|

By Battery Type |

●

Lithium Nickel

Manganese Cobalt Oxide ●

Lithium Iron

Phosphate |

|

By Application |

●

Intercity ●

Intracity |

|

By End Use |

●

Public ●

Private |

Electric Bus Market Share

Analysis by Region

North America is

projected to hold the largest share of the global electric bus market over the

forecast period

North America led the global

market for electric buses in 2024 at an astonishing 47.2% market share and is

predicted to lead the market during the forecasting period. The massive market

is largely powered by extensive government subsidies, large-scale funding of

clean public transportation, and strict emission controls aimed at minimizing

carbon footprints in large metropolitan areas. The U.S. and Canadian

governments are actively using electric buses as part of green mobility

solutions, backed by incentives such as subsidies, tax credits, and grants

through the U.S. Bipartisan Infrastructure Law and the Canadian Zero Emission

Transit Fund. Moreover, the presence of global leading electric bus

manufacturers, rapid growth in the installation of advanced charging

facilities, as well as the increasing trend of fleet electrization in school

and public transit areas, are fuelling regional market growth. Public transit

agencies are collaborating with technology vendors and automotive titans to

increase rollout and enable cost-effective operation in metropolitan areas.

Further, the Asia Pacific is

expected to achieve the highest CAGR during the forecast period. The region's

accelerated urbanization, huge population base, and favorable government

policies, particularly in China and India, are driving demand. Aggressive

greenhouse gas reductions and city-wide transit electromobilization plans are

set to position Asia Pacific as the principal driver of future growth of the

electric bus market.

Electric Bus Market

Competition Landscape Analysis

The Global Electric Bus Market Is

Poised for Significant Growth, With Key Players Investing Heavily in Technology

and Infrastructure. These Companies Are Actively Engaged in Research and

Development, Strategic Partnerships, And Large-Scale Project Implementations to

Enhance Their Market Positions.

Global Electric Bus

Market Recent Developments News:

●

In March 2024, Volvo

Buses launched its BZR Electric electromobility platform, designed to support

urban, intercity, and commuter transport operations. The platform offers

multiple configurations to maximize profitability and sustainability for global

operators, aligning with the rising demand for electric mobility solutions.

Building on the success of Volvo’s low-floor electric buses—already in use

across more than 25 countries—the BZR Electric platform reinforces the

company’s commitment to advancing zero-emission public transportation. This

launch underscores Volvo Buses' leadership in delivering scalable, efficient,

and eco-friendly transit solutions for the future.

●

In May 2024, Yutong

achieved a milestone in China's electric vehicle export market by delivering 46

battery-electric apron buses to Spain. These zero-emission buses will serve 15

major Spanish airports, aligning with the country’s broader sustainability

objectives for airport infrastructure. Marking the largest order of its kind

for China, the deal underscores Yutong’s expanding footprint in Europe, where

its cutting-edge electric buses are already operational at over 70 airports,

including major hubs such as Madrid, Barcelona, and Rome.

The Global Electric Bus Market is dominated by a few large

companies, such as

●

BYD Company Limited

●

AB Volvo

●

Proterra

●

MAN

●

Nissan Motor Corporation

●

Ashok Leyland Limited

●

Daimler Truck AG

●

Zhengzhou Yutong Bus Co. Ltd.

●

TATA Motors Limited

●

Hyundai Motor Company

● Others

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1.

Global

Electric Bus Market Introduction and Market Overview

1.1. Objectives of the Study

1.2. Global Electric Bus Market Scope

and Market Estimation

1.2.1.Global Electric Bus Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Electric Bus Market

Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3. Market Segmentation

1.3.1.Propulsion Type of Global Electric

Bus Market

1.3.2.Battery Type of Global Electric

Bus Market

1.3.3.Application of Global Electric

Bus Market

1.3.4.End-use of Global Electric Bus

Market

1.3.5.Region of Global Electric Bus

Market

2.

Executive Summary

2.1. Demand Side Trends

2.2. Key Market Trends

2.3. Market Demand (US$ Bn) Analysis

2020 – 2024 and Forecast, 2025 – 2033

2.4. Demand and Opportunity

Assessment

2.5. Market Dynamics

2.5.1.Drivers

2.5.2.Limitations

2.5.3.Opportunities

2.5.4.Impact Analysis of Drivers and

Restraints

2.6. Key Product/Brand Analysis

2.7. Technological Advancements

2.8. Key Developments

2.9. Porter’s Five Forces Analysis

2.9.1.Bargaining Power of Suppliers

2.9.2.Bargaining Power of Buyers

2.9.3.Threat of Substitutes

2.9.4.Threat of New Entrants

2.9.5.Competitive Rivalry

2.10. PEST Analysis

2.10.1. Political Factors

2.10.2. Economic Factors

2.10.3. Social Factors

2.10.4. Technology Factors

2.11. Insights on Cost-effectiveness

of Electric Bus

2.12. Key Regulation

3.

Global Electric Bus Market Estimates & Historical Trend Analysis (2020 - 2024)

4.

Global Electric Bus Market Estimates & Forecast Trend Analysis, by

Propulsion Type

4.1. Global Electric Bus Market

Revenue (US$ Bn) Estimates and Forecasts, by Propulsion Type, 2020 - 2033

4.1.1.Battery Electric Vehicle (BEV)

4.1.2.Plug-in Hybrid Electric Vehicle

(PHEV)

4.1.3.Fuel Cell Electric Vehicle

(FCEV)

5.

Global Electric Bus Market Estimates & Forecast Trend Analysis, by

Battery Type

5.1. Global Electric Bus Market

Revenue (US$ Bn) Estimates and Forecasts, by Battery Type, 2020 - 2033

5.1.1.Lithium Nickel Manganese Cobalt

Oxide

5.1.2.Lithium Iron Phosphate

6.

Global Electric Bus Market Estimates & Forecast Trend Analysis, by

Application

6.1. Global Electric Bus Market

Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

6.1.1.Intercity

6.1.2.Intracity

7.

Global Electric Bus Market Estimates & Forecast Trend Analysis, by

End-use

7.1. Global Electric Bus Market

Revenue (US$ Bn) Estimates and Forecasts, by End-use, 2020 - 2033

7.1.1.Public

7.1.2.Private

8.

Global Electric Bus Market Estimates & Forecast Trend Analysis,

by Region

8.1. Global Electric Bus Market

Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

8.1.1.North America

8.1.2.Europe

8.1.3.Asia Pacific

8.1.4.Middle East & Africa

8.1.5.Latin America

9.

North

America Electric Bus Market: Estimates & Forecast Trend Analysis

9.1.

North

America Electric Bus Market Assessments & Key Findings

9.1.1.North America Electric Bus

Market Introduction

9.1.2.North America Electric Bus

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Propulsion Type

9.1.2.2. By Battery Type

9.1.2.3. By Application

9.1.2.4. By End-use

9.1.2.5. By Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Electric

Bus Market: Estimates & Forecast

Trend Analysis

10.1. Europe Electric Bus Market

Assessments & Key Findings

10.1.1. Europe Electric Bus Market

Introduction

10.1.2. Europe Electric Bus Market Size

Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Propulsion Type

10.1.2.2. By Battery Type

10.1.2.3. By Application

10.1.2.4. By End-use

10.1.2.5. By Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6. Rest

of Europe

11. Asia Pacific Electric

Bus Market: Estimates & Forecast

Trend Analysis

11.1. Asia Pacific Market Assessments

& Key Findings

11.1.1. Asia Pacific Electric Bus Market

Introduction

11.1.2. Asia Pacific Electric Bus Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Propulsion Type

11.1.2.2. By Battery Type

11.1.2.3. By Application

11.1.2.4. By End-use

11.1.2.5. By Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Electric

Bus Market: Estimates & Forecast

Trend Analysis

12.1. Middle East & Africa Market

Assessments & Key Findings

12.1.1. Middle

East & Africa Electric

Bus Market Introduction

12.1.2. Middle

East & Africa Electric

Bus Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1. By Propulsion Type

12.1.2.2. By Battery Type

12.1.2.3. By Application

12.1.2.4. By End-use

12.1.2.5. By Country

12.1.2.5.1. UAE

12.1.2.5.2. Saudi

Arabia

12.1.2.5.3. South

Africa

12.1.2.5.4. Rest of

MEA

13. Latin America

Electric Bus Market: Estimates &

Forecast Trend Analysis

13.1. Latin America Market Assessments

& Key Findings

13.1.1. Latin America Electric Bus

Market Introduction

13.1.2. Latin America Electric Bus

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

13.1.2.1. By Propulsion Type

13.1.2.2. By Battery Type

13.1.2.3. By Application

13.1.2.4. By End-use

13.1.2.5. By Country

13.1.2.5.1. Brazil

13.1.2.5.2. Argentina

13.1.2.5.3. Mexico

13.1.2.5.4. Rest of

LATAM

14. Country Wise Market:

Introduction

15. Competition Landscape

15.1. Global Electric Bus Market Product

Mapping

15.2. Global Electric Bus Market

Concentration Analysis, by Leading Players / Innovators / Emerging Players /

New Entrants

15.3. Global Electric Bus Market Tier

Structure Analysis

15.4. Global Electric Bus Market

Concentration & Company Market Shares (%) Analysis, 2024

16. Company Profiles

16.1.

BYD Company Limited

16.1.1. Company Overview & Key Stats

16.1.2. Financial Performance & KPIs

16.1.3. Product Portfolio

16.1.4. SWOT Analysis

16.1.5. Business Strategy & Recent

Developments

* Similar details would be provided

for all the players mentioned below

16.2. AB Volvo

16.3. Proterra

16.4. MAN

16.5. Nissan Motor

Corporation

16.6. Ashok Leyland

Limited

16.7. Daimler Truck

AG

16.8. Zhengzhou

Yutong Bus Co. Ltd.

16.9. TATA Motors

Limited

16.10. Hyundai Motor

Company

16.11. Others

17. Research

Methodology

17.1. External Transportations /

Databases

17.2. Internal Proprietary Database

17.3. Primary Research

17.4. Secondary Research

17.5. Assumptions

17.6. Limitations

17.7. Report FAQs

18. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables