Electronic Cigarette Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product (Modular, Rechargeable, Disposable), By Distribution Channel (Online, Retail [Specialty E-Cig Stores, Supermarkets/Hypermarkets, Convenience Stores]), By Battery Mode (Automatic, Manual), And Geography

2025-11-28

Consumer Products

Jaya Bundele (Research Analyst)

Description

Electronic Cigarette Market Overview

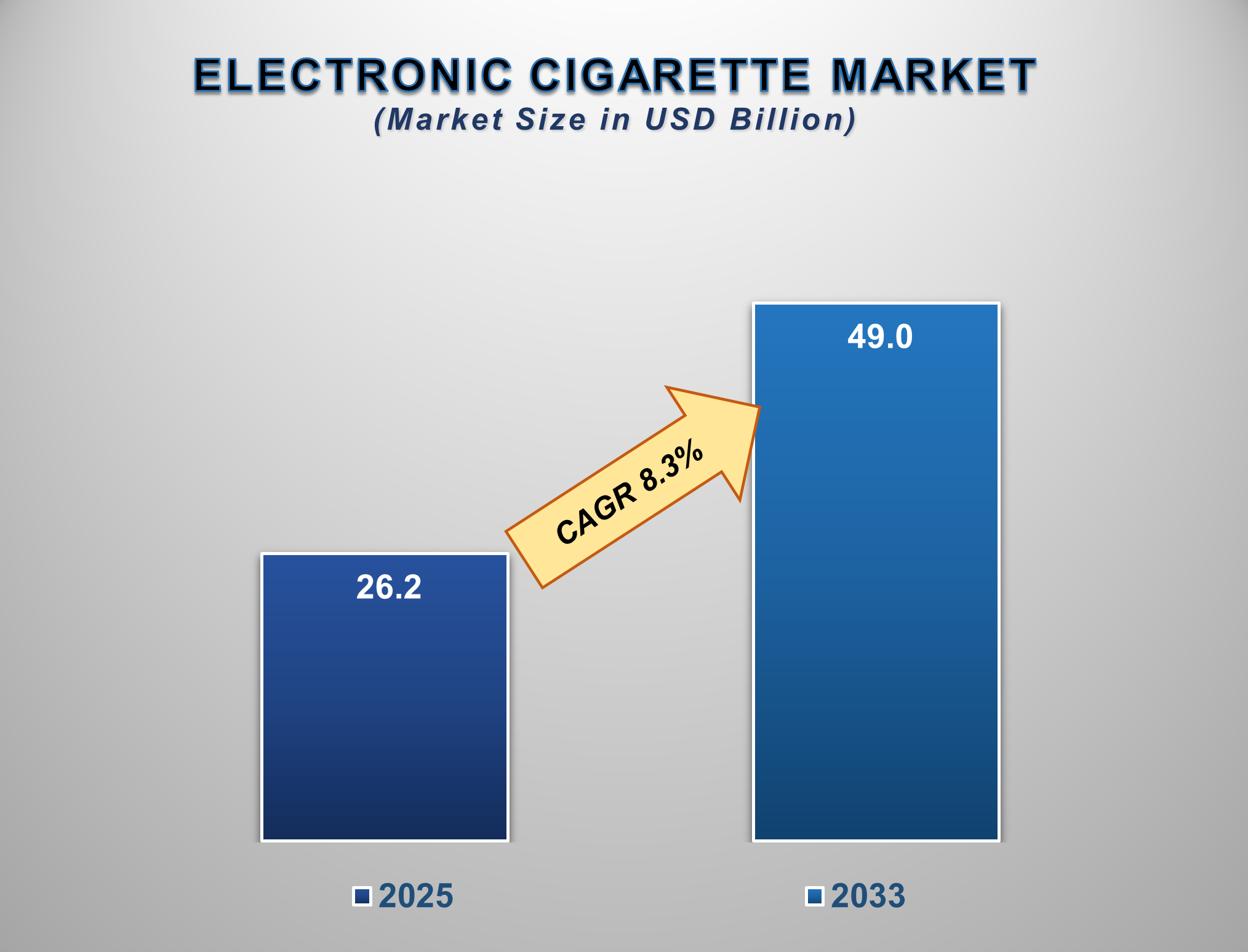

The Electronic Cigarette Market is poised for dynamic growth from 2025 to 2033, driven by the global shift away from traditional tobacco, continuous product innovation, and the perception of e-cigarettes as a less harmful alternative for adult smokers. The market is projected to be valued at approximately USD 26.2 billion in 2025 and is forecasted to reach nearly USD 49.0 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 8.3% during this period.

Electronic cigarettes, or e-cigarettes, are

battery-operated devices that heat a liquid (e-liquid) to create an aerosol,

which is inhaled by the user. The market's expansion is primarily fueled by

increasing health consciousness among smokers, supportive government

initiatives in some regions aimed at tobacco harm reduction, and the widespread

availability of a vast array of flavors and device types.

Technological advancements leading to improved

battery life, enhanced vapor production, and more efficient nicotine delivery

systems are also significant contributors. However, the market faces challenges

from stringent regulatory frameworks, increasing health concerns regarding

long-term use, and a ban on certain flavored products in key markets like the

United States. Despite this, North America and Europe currently hold

significant market shares, while the Asia-Pacific region is expected to witness

the fastest growth due to its massive smoking population and evolving

regulatory landscape.

Electronic

Cigarette Market Drivers and Opportunities

The Shift Towards Harm Reduction and Smoking

Cessation is the Primary Market Driver

The most powerful driver for the electronic

cigarette market is the growing global movement towards tobacco harm reduction.

As public awareness of the severe health risks associated with combustible

cigarettes intensifies, a substantial number of adult smokers are seeking

alternatives. E-cigarettes, which do not involve combustion and thus eliminate

tar and many of the carcinogens found in tobacco smoke, are widely perceived as

a less harmful option. This perception is bolstered by public health endorsements

in certain countries, such as the UK, where e-cigarettes are promoted as a

smoking cessation tool. The desire to reduce or quit traditional smoking,

coupled with the ability to control nicotine intake, creates a sustained and

powerful demand driver for the e-cigarette market.

Product Innovation and Flavor Diversity are

Driving Consumer Adoption

Continuous and rapid product innovation is a key

catalyst propelling the e-cigarette market. The evolution from early

cig-a-likes to advanced personal vaporizers (mods) and the recent explosion in

popularity of convenient, pre-filled disposable e-cigarettes have significantly

broadened the market's appeal. Manufacturers are constantly innovating in areas

of design, battery technology, and e-liquid formulations. The availability of

an extensive range of flavors, from traditional tobacco and menthol to fruits,

desserts, and beverages, plays a crucial role in attracting and retaining

users, particularly among younger demographics. This constant cycle of

innovation keeps the market dynamic and stimulates repeat purchases.

The Expansion into Emerging Markets and the

Development of Next-Generation Products Present

Significant Opportunities

The electronic cigarette market holds

substantial untapped potential, primarily in emerging economies across

Asia-Pacific, Latin America, and the Middle East. These regions have high

smoking prevalence and, in many cases, less restrictive regulatory environments,

offering fertile ground for market expansion.

Furthermore, significant opportunities lie in the development and

commercialization of next-generation products. This includes the advancement of

nicotine salt e-liquids for a smoother experience, temperature control devices

for improved safety, and the exploration of cannabis/CBD-infused vaping

products in regions where they are legal. For companies, investing in clinical

research to substantiate harm reduction claims, developing sustainable and

recyclable products to address environmental concerns, and leveraging digital

marketing and e-commerce channels are key strategies to capture future growth.

Electronic Cigarette

Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 26.2 Billion |

|

Market Forecast in 2033 |

USD 49.0 Billion |

|

CAGR % 2025-2033 |

8.3% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Product ●

By Distribution

Channel ●

By Battery Mode |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Electronic Cigarette

Market Report Segmentation Analysis

The global Electronic Cigarette

Market industry analysis is segmented by Product, by Distribution Channel, by

Battery Mode, and by Region.

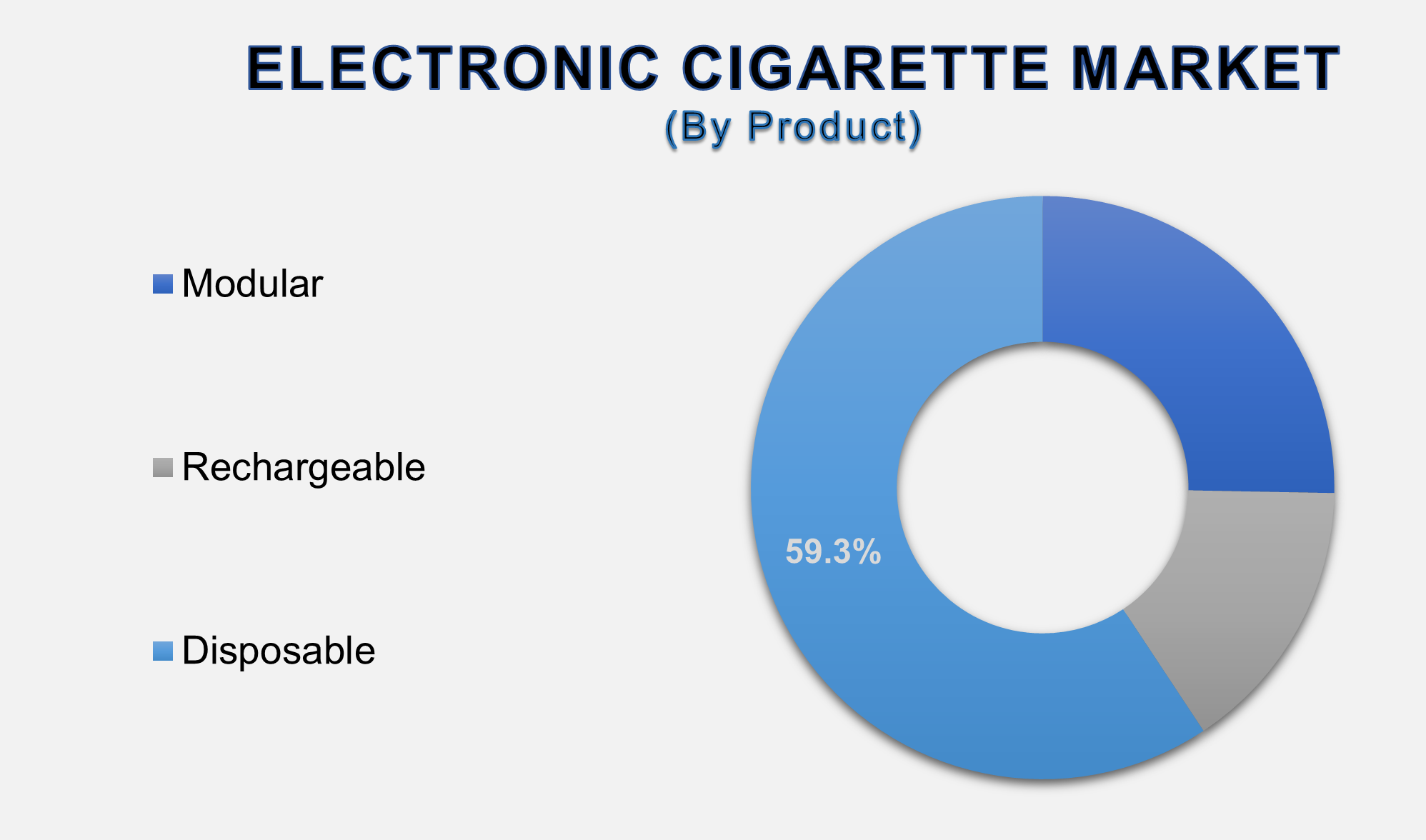

The Disposable product

segment is anticipated to command the largest market share in 2025

The Product segment is categorized

into Modular, Rechargeable, and Disposable. The dominance of the disposable

segment is attributed to its unparalleled convenience and user-friendliness.

Disposable e-cigarettes are pre-filled, pre-charged, and require no maintenance

or refilling, making them an ideal entry point for new users and a convenient

option for experienced vapers. Their compact design, wide availability in

numerous flavors, and affordable upfront cost have driven their explosive

growth, particularly through convenience stores and gas stations. This ease of

use has allowed disposable devices to capture a significant portion of the

market from more complex, modular, and rechargeable systems.

The Online distribution channel segment is

projected to grow at a significant CAGR.

The Distribution Channel segment includes Online

and Retail (Specialty E-Cig Stores, Supermarkets/Hypermarkets, Convenience

Stores). The online segment's projected high growth is driven by several key

advantages. E-commerce platforms offer a broader selection of products,

flavors, and accessories than most physical stores, along with competitive

pricing and discreet home delivery. They also serve as a vital channel for

information, with user reviews and detailed product specifications aiding the

purchase decision. While retail remains crucial for impulse buys, the

convenience, variety, and often lower prices available online are fueling this

channel's rapid expansion, especially among tech-savvy consumers.

The Retail end-use segment is projected to

witness the highest growth rate.

The Retail segment is divided into Specialty

E-Cig Stores, Supermarkets/Hypermarkets, and Convenience Stores. The

convenience store sub-segment, in particular, is witnessing the highest growth

rate due to its critical role in the distribution of disposable e-cigarettes.

These outlets offer immediate accessibility and impulse purchase opportunities,

capitalizing on high foot traffic. The placement of e-cigarettes alongside

traditional tobacco products makes them highly visible to the target

demographic of current smokers. The extensive, established distribution network

of convenience stores and gas stations is a primary driver of volume sales,

making this retail channel a powerhouse for market growth.

The following segments are part of an in-depth analysis of

the global Electronic Cigarette Market:

|

Market

Segments |

|

|

By

Product |

●

Modular ●

Rechargeable ●

Disposable |

|

By

Distribution Channel |

●

Online Channel ●

Retail Store |

|

By Battery Mode |

●

Automatic ●

Manual |

Electronic Cigarette

Market Share Analysis by Region

The North America region

is anticipated to hold the largest portion of the Electronic Cigarette Market

globally throughout the forecast period.

North America's dominance is anchored by the

United States, which has one of the most mature and sophisticated e-cigarette

markets in the world. High consumer spending power, early adoption of vaping

culture, and intense marketing and product innovation from major companies have

solidified the region's leading position. While stringent FDA regulations pose

challenges, the well-established retail and online distribution networks and a

large base of adult users seeking alternatives to smoking continue to drive the

market. The presence of industry giants like Juul Labs and RJ Reynolds Vapor

Company further cements North America's influence on global trends, product

development, and market size.

The U.S. is the epicenter of the e-cigarette

market within North America, characterized by a constant stream of product

launches, fierce brand competition, and a complex regulatory environment. The

market has seen a significant shift towards disposable devices following

federal restrictions on flavored cartridge-based pods. American consumers

demonstrate high brand awareness and are quick to adopt new technologies and

flavors. This dynamic, albeit challenging, environment makes the U.S. the most

significant single-country market, dictating global strategies for major

players and attracting substantial investment in marketing and regulatory

compliance.

Electronic Cigarette

Market Competition Landscape Analysis

The global electronic

cigarette market is highly competitive and consolidated, dominated by a few

large tobacco and vaping-focused companies. Competition is intense and revolves

around brand strength, product innovation, marketing reach, and distribution

network dominance. Key strategies include heavy investment in research and

development to create new devices and e-liquid formulations, strategic mergers

and acquisitions to gain market share and technology, and navigating the

complex global regulatory landscape to ensure product compliance. The market

also features a large number of smaller players and vape shops that compete on

customization, niche flavors, and community engagement.

Global Electronic

Cigarette Market Recent Developments News:

- In February 2025, Juul Labs announced the launch of

a new Bluetooth-enabled device in international markets, featuring

age-verification technology and usage controls.

- In December 2024, British American Tobacco (BAT)

unveiled a new line of "potentially reduced-risk" heated tobacco

products in Japan, diversifying its smoke-free portfolio beyond e-vapor.

- In October 2024, SMOK, a leading manufacturer of

advanced vaping devices, introduced a new pod system with adjustable

wattage and a leak-resistant design, targeting experienced vapers.

- In August 2024, the FDA issued

its first marketing granted orders for a set of tobacco-flavored e-liquid

products, signaling a potential pathway for legal sales of certain vape

products in the U.S.

The Global Electronic

Cigarette Market Is Dominated by a Few Large Companies, such as

●

Juul Labs, Inc.

●

British American

Tobacco PLC (BAT)

●

Imperial Brands PLC

●

Japan Tobacco

International (JTI)

●

Altria Group, Inc.

●

(SMOK)

●

Vaporesso

●

Geekvape

●

Fontem Ventures (blu)

●

Logic Technology

●

NJOY

●

Shenzhen Eigate

Technology Co., Ltd (VOOPOO)

●

Suorin

●

RELX Technology

●

Philip Morris

International (IQOS)

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Electronic

Cigarette Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Electronic Cigarette Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Electronic

Cigarette Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product of Global Electronic

Cigarette Market

1.3.2.Distribution Channel of

Global Electronic Cigarette Market

1.3.3.Battery Mode of Global Electronic

Cigarette Market

1.3.4.Region of Global Electronic

Cigarette Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Pricing

Analysis

2.6.

Key

Developments

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Electronic Cigarette Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Electronic Cigarette Market Estimates

& Forecast Trend Analysis, by Product

4.1.

Global

Electronic Cigarette Market Revenue (US$ Bn) Estimates and Forecasts, by Product,

2020 - 2033

4.1.1.Modular

4.1.2.Rechargeable

4.1.3.Disposable

5. Global

Electronic Cigarette Market Estimates

& Forecast Trend Analysis, by Distribution Channel

5.1.

Global

Electronic Cigarette Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution

Channel, 2020 - 2033

5.1.1.Online Channel

5.1.2.Retail Store

6. Global

Electronic Cigarette Market Estimates

& Forecast Trend Analysis, by Battery Mode

6.1.

Global

Electronic Cigarette Market Revenue (US$ Bn) Estimates and Forecasts, by Battery

Mode 2020 - 2033

6.1.1.Automatic

6.1.2.Manual

7. Global

Electronic Cigarette Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Electronic Cigarette Market Revenue (US$ Bn) Estimates and Forecasts, by region,

2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Electronic

Cigarette Market: Estimates &

Forecast Trend Analysis

8.1. North America Electronic

Cigarette Market Assessments & Key Findings

8.1.1.North America Electronic

Cigarette Market Introduction

8.1.2.North America Electronic

Cigarette Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Product

8.1.2.2.

By Distribution Channel

8.1.2.3.

By Battery Mode

8.1.2.4. By Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Electronic

Cigarette Market: Estimates &

Forecast Trend Analysis

9.1. Europe Electronic

Cigarette Market Assessments & Key Findings

9.1.1.Europe Electronic

Cigarette Market Introduction

9.1.2.Europe Electronic

Cigarette Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Product

9.1.2.2.

By Distribution Channel

9.1.2.3.

By Battery Mode

9.1.2.4. By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Electronic

Cigarette Market: Estimates &

Forecast Trend Analysis

10.1. Asia Pacific Market

Assessments & Key Findings

10.1.1.

Asia

Pacific Electronic Cigarette Market Introduction

10.1.2.

Asia

Pacific Electronic Cigarette Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

10.1.2.1.

By Product

10.1.2.2.

By Distribution Channel

10.1.2.3.

By Battery Mode

10.1.2.4. By Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Electronic

Cigarette Market: Estimates &

Forecast Trend Analysis

11.1. Middle East & Africa

Market Assessments & Key Findings

11.1.1. Middle

East & Africa

Electronic Cigarette Market Introduction

11.1.2. Middle

East & Africa

Electronic Cigarette Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Product

11.1.2.2.

By Distribution Channel

11.1.2.3.

By Battery Mode

11.1.2.4. By Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Electronic Cigarette Market: Estimates

& Forecast Trend Analysis

12.1. Latin America Market

Assessments & Key Findings

12.1.1. Latin America Electronic

Cigarette Market Introduction

12.1.2. Latin America Electronic

Cigarette Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Product

12.1.2.2.

By Distribution Channel

12.1.2.3.

By Battery Mode

12.1.2.4. By Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13.

Country

Wise Market: Introduction

14.

Competition

Landscape

14.1. Global Electronic

Cigarette Market Product Mapping

14.2. Global Electronic

Cigarette Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3. Global Electronic

Cigarette Market Tier Structure Analysis

14.4. Global Electronic

Cigarette Market Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

Juul Labs, Inc.

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2.

British American Tobacco PLC (BAT)

15.3.

Imperial Brands PLC

15.4.

Japan Tobacco International (JTI)

15.5.

Altria Group, Inc.

15.6.

(SMOK)

15.7.

Vaporesso

15.8.

Geekvape

15.9.

Fontem Ventures (blu)

15.10.

Logic Technology

15.11.

NJOY

15.12.

Shenzhen Eigate Technology Co., Ltd (VOOPOO)

15.13.

Suorin

15.14.

RELX Technology

15.15.

Philip Morris International (IQOS)

15.16.

Other Prominent Players

16. Research

Methodology

16.1. External Transportations /

Databases

16.2. Internal Proprietary

Database

16.3. Primary Research

16.4. Secondary Research

16.5. Assumptions

16.6. Limitations

16.7. Report FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables