Electrosurgical Devices Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Product Type (Radiofrequency Electrosurgical Devices, Electrosurgical Generators, Electrocautery Devices and Electrosurgical Accessories); By Application (General Surgery, Dermatological Surgery, Cardiac Surgery, Orthopaedic Surgery, Gastrointestinal Surgery and Others); By End-user (Hospitals, Specialty Clinics, Ambulatory Surgical Centers and Others) and Geography

2025-08-06

Healthcare

Swetal (Research Analyst)

Description

Electrosurgical Devices Market Overview

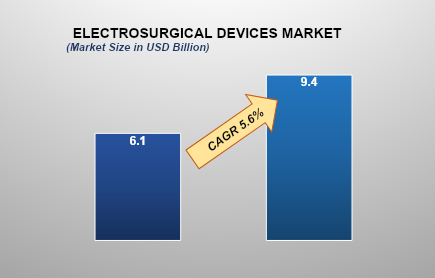

The Electrosurgical Devices Market size is anticipated to experience substantial growth from 2025 to 2033, driven primarily by an Increase in the number of minimally invasive surgeries. This is one of the key factors fueling the global electrosurgical devices market growth. With an estimated valuation of approximately USD 6.1 billion in 2025, the market is expected to reach USD 9.4 billion by 2033, registering a robust compound annual growth rate (CAGR) of 5.6% over the decade.

Electrosurgical devices are medical instruments used to cut tissue, coagulate blood, or achieve hemostasis during surgical procedures by applying high-frequency electrical currents. These devices are widely used across various surgical specialties, including general surgery, gynecology, urology, and dermatology. Electrosurgery operates in two primary modes: monopolar and bipolar. In monopolar electrosurgery, the electrical current passes from the active electrode through the patient’s body to a return electrode, whereas in bipolar electrosurgery, the current flows between two tips of a forceps-like instrument, providing more localized energy delivery.

These devices allow for precise tissue dissection with minimal blood loss, reducing operative time and improving visibility in the surgical field. Modern electrosurgical units offer adjustable power settings, safety features, and compatibility with different surgical tools. Despite their advantages, electrosurgical devices require careful handling due to potential risks such as burns, unintended tissue damage, or interference with implanted electronic devices. Proper training and adherence to safety protocols are essential to minimize complications. With advancements in technology, newer systems have incorporated feedback-controlled energy delivery and integration with minimally invasive techniques, enhancing their precision and safety. Electrosurgery remains a cornerstone of modern operative methods, balancing efficiency and effectiveness in surgical interventions.

Electrosurgical Devices Market Drivers and Opportunities

Rising Demand for Minimally Invasive Surgeries is anticipated to lift the Electrosurgical Devices Market during the forecast period

One of the primary drivers of the electrosurgical devices market is the increasing global demand for minimally invasive surgical procedures. Patients and healthcare providers prefer these techniques due to their advantages, such as reduced blood loss, smaller incisions, shorter hospital stays, quicker recovery, and lower post-operative complications. Electrosurgical devices are integral to these procedures, offering precision and efficiency in cutting and coagulating tissues. The growing prevalence of chronic conditions like cancer, cardiovascular disorders, and obesity, which often require surgical intervention, further boosts demand. Moreover, advancements in laparoscopic and robotic surgeries have widened the scope of electrosurgery across multiple specialties. As surgical technology evolves, healthcare systems are increasingly adopting these devices to improve outcomes and reduce surgical costs, fueling market growth.

Technological Advancements in Electrosurgical Devices drive the global Electrosurgical Devices Market

Technological innovations are significantly propelling the electrosurgical devices market trends The introduction of advanced energy-based instruments with improved safety features, real-time feedback control, and compatibility with robotic-assisted systems enhances procedural precision and patient safety. Smart electrosurgical units that automatically adjust energy output based on tissue resistance minimize collateral damage and improve clinical efficiency. Innovations like plasma-based devices, argon beam coagulators, and hybrid systems that combine cutting and coagulation functions have expanded the scope of electrosurgery in complex procedures. Moreover, integration with digital operating rooms and data-driven systems improves workflow and documentation. These continuous technological upgrades not only increase the adoption of electrosurgical equipment in modern operating rooms but also enable manufacturers to differentiate their products, strengthening their market presence.

Opportunity for the Electrosurgical Devices Market

Emerging Markets in Asia-Pacific and Latin America offer significant opportunities in the global Electrosurgical Devices Market

Emerging economies in regions such as Asia-Pacific and Latin America present significant growth opportunities for the electrosurgical devices market. Rapidly expanding healthcare infrastructure, increasing investments in medical technology, and growing awareness about advanced surgical procedures are key factors driving demand in these regions. Additionally, a rising middle-class population, increasing health insurance coverage, and government initiatives to improve access to quality care are fueling the adoption of modern surgical tools. Countries like China, India, Brazil, and Mexico are witnessing a surge in both public and private healthcare facilities, which are equipping themselves with technologically advanced surgical devices to enhance service offerings. Moreover, medical tourism is thriving in many of these regions due to cost-effective treatments, further boosting demand for efficient surgical equipment like electrosurgical devices. Manufacturers tapping into these markets through partnerships, localized production, and customized offerings can leverage substantial untapped potential.

Electrosurgical Devices Market Scope

Electrosurgical Devices Market Analysis - Report Segmentation

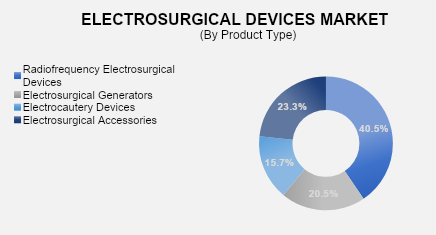

The global Electrosurgical Devices Market industry analysis is segmented by product type, by application, by end-user, and by region.

The Radiofrequency Electrosurgical Devices segment is leading the Electrosurgical Devices Market

Radiofrequency (RF) electrosurgical devices are leading the electrosurgical devices market due to their widespread clinical applications, precision, and safety. These devices use alternating electrical current in the radiofrequency range to generate heat, enabling precise tissue cutting and coagulation with minimal damage to surrounding areas. RF technology is favored in various surgical specialties, including dermatology, cardiology, ENT, and oncology, for procedures like tumor ablation, lesion removal, and cardiac arrhythmia treatment. The increasing preference for minimally invasive and non-invasive techniques has further driven the adoption of RF-based systems. Additionally, modern RF electrosurgical units incorporate advanced features such as temperature control, impedance monitoring, and feedback systems, enhancing safety and clinical outcomes. Their versatility, cost-effectiveness, and reduced recovery time for patients make them a preferred choice among surgeons and healthcare institutions. As technology continues to evolve, RF electrosurgical devices are expected to maintain their dominance in the market, especially in outpatient and day-care surgical centers.

The General Surgery application segment holds the largest electrosurgical devices market share

The general surgery segment holds the largest share in the electrosurgical devices market due to the broad range of procedures it encompasses and the critical role electrosurgery plays in them. General surgery includes operations on the digestive tract, abdomen, breast, skin, and soft tissues, where electrosurgical devices are essential for effective tissue dissection, hemostasis, and minimizing blood loss. The growing number of surgeries related to gallbladder removal, hernia repair, appendectomies, and gastrointestinal interventions has contributed to the high usage of electrosurgical instruments in this segment. These procedures benefit greatly from electrosurgical technologies, which enable surgeons to operate more efficiently, reduce operative time, and improve patient recovery outcomes. Additionally, the growing elderly population, increasing prevalence of lifestyle-related disorders, and rising surgical admissions further support this trend. Hospitals and ambulatory surgical centers are increasingly relying on electrosurgical tools for general surgery, solidifying this segment’s dominance in the global market.

Hospitals' End-user segment dominating in electrosurgical devices market

Hospitals represent the dominant end-user segment in the electrosurgical devices market, driven by their high surgical volumes, advanced infrastructure, and access to a wide range of surgical specialties. These healthcare facilities are equipped with operating rooms that support complex and high-risk procedures, where electrosurgical devices are extensively used for their efficiency in cutting and coagulating tissue. Hospitals are also more likely to adopt technologically advanced devices, thanks to larger capital budgets and integration with digital health systems. Moreover, the presence of trained surgical professionals and anesthesiologists in hospital settings supports the safe and effective use of electrosurgical equipment. Hospitals often serve as referral centers for both emergency and elective surgeries, further increasing the demand for reliable and high-performance electrosurgical units. As surgical caseloads continue to rise due to aging populations and an increase in chronic disease-related interventions, hospitals are expected to remain the largest consumers of electrosurgical devices globally.

The following segments are part of an in-depth analysis of the global electrosurgical devices market:

Electrosurgical Devices Market Share Analysis by Region

The North America region is projected to hold the largest share of the global Electrosurgical Devices Market over the forecast period.

North America is expected to maintain the largest share of the global electrosurgical devices market over the forecast period, primarily due to its well-established healthcare infrastructure, high healthcare expenditure, and early adoption of advanced medical technologies. The region, particularly the United States, has a high volume of surgical procedures driven by the prevalence of chronic diseases, an aging population, and a growing demand for minimally invasive surgeries. In addition, the presence of leading medical device manufacturers and continuous investment in research and development contribute significantly to market growth. Favourable regulatory policies and reimbursement frameworks also support the adoption of electrosurgical devices across hospitals and outpatient surgical centers. Moreover, the region benefits from a skilled healthcare workforce and increasing awareness about surgical innovations among both providers and patients. As a result, North America remains at the forefront of technological advancement and usage of electrosurgical devices, reinforcing its dominant market position in the foreseeable future.

Electrosurgical Devices Market Analysis - Competition Landscape Overview

The market is competitive, with several established players and new entrants offering a range of electrosurgical device products. Some of the key players are Medtronic plc, Johnson & Johnson (Ethicon), B. Braun Melsungen AG, Olympus Corporation, CONMED Corporation, Boston Scientific Corporation, Smith & Nephew plc, Erbe Elektromedizin GmbH, and others.

Global Electrosurgical Devices Market Recent Developments News:

In June 2023, Olympus launched the ESG-410 electrosurgical generator, designed for treating non-muscle-invasive bladder cancer (NMIBC) and benign prostatic hyperplasia (BPH). Compared to its predecessor, the ESG-400, the ESG-410 features larger capacitors, enhancing plasma stability during ignition.

In March 2025, Johnson & Johnson MedTech announced the launch of its FDA-cleared Dualto energy system, a surgical solution that integrates multiple energy modalities into a single platform for use in open and minimally invasive surgery. This launch expanded Johnson & Johnson’s surgical energy portfolio and reinforced its leadership in advanced surgical technologies.

In April 2025, Erbe Elektromedizin GmbH expanded its VIO 3 family by introducing a new generation of electrosurgical generators, designed to meet the needs of various medical specialties and procedures. The portfolio was further strengthened with the addition of the VIO seal, the first VIO generator dedicated entirely to bipolar applications.

The Global Electrosurgical Devices Market is dominated by a few large companies, such as

Medtronic plc

Johnson & Johnson (Ethicon)

B. Braun Melsungen AG

Olympus Corporation

CONMED Corporation

Boston Scientific Corporation

Smith & Nephew plc

Erbe Elektromedizin GmbH

KLS Martin Group

Bovie Medical Corporation

BOWA-electronic GmbH & Co. KG

Stryker Corporation

Zimmer Biomet Holdings, Inc.

Applied Medical Resources Corporation

Aesculap, Inc.

Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

- Global Electrosurgical Devices Market Introduction and Market Overview

- Objectives of the Study

- Global Electrosurgical Devices Market Scope and Market Estimation

- Global Electrosurgical Devices Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Electrosurgical Devices Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2033

- Market Segmentation

- Product Type of Global Electrosurgical Devices Market

- Application of Global Medical Devices Coating Market

- End-user of Global Electrosurgical Devices Market

- Region of Global Electrosurgical Devices Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Electrosurgical Devices Market

- Number of thoracic Surgery performed per year

- Key Product/Brand Analysis

- Porter’s Five Forces Analysis

- Bargaining Power of Suppliers

- Bargaining Power of Buyers

- Threat of Substitutes

- Threat of New Entrants

- Competitive Rivalry

- PEST Analysis

- Political Factors

- Economic Factors

- Social Factors

- Technology Factors

- Key Regulation

- Global Electrosurgical Devices Market Estimates & Historical Trend Analysis (2021 - 2024)

- Global Electrosurgical Devices Market Estimates & Forecast Trend Analysis, by Product Type

- Global Electrosurgical Devices Market Revenue (US$ Bn) Estimates and Forecasts, by Product Type, 2021 - 2033

- Radiofrequency Electrosurgical Devices

- Electrosurgical Generators

- Electrocautery Devices

- Electrosurgical Accessories

- Global Electrosurgical Devices Market Estimates & Forecast Trend Analysis, by Application

- Global Electrosurgical Devices Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2033

- General Surgery

- Dermatological Surgery

- Cardiac Surgery

- Orthopedic Surgery

- Gastrointestinal Surgery

- Others

- Global Electrosurgical Devices Market Estimates & Forecast Trend Analysis, by End-user

- Global Electrosurgical Devices Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2021 - 2033

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Others

- Global Electrosurgical Devices Market Estimates & Forecast Trend Analysis, by region

- Global Electrosurgical Devices Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- North America Electrosurgical Devices Market: Estimates & Forecast Trend Analysis

- North America Electrosurgical Devices Market Assessments & Key Findings

- North America Electrosurgical Devices Market Introduction

- North America Electrosurgical Devices Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product Type

- By Application

- By End-user

- By Country

- The U.S.

- Canada

- Western Europe Electrosurgical Devices Market: Estimates & Forecast Trend Analysis

- Western Europe Electrosurgical Devices Market Assessments & Key Findings

- Western Europe Electrosurgical Devices Market Introduction

- Western Europe Electrosurgical Devices Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product Type

- By Application

- By End-user

- By Country

- Germany

- Italy

- U.K.

- France

- Spain

- Netherland

- Rest of W. Europe

- Asia Pacific Electrosurgical Devices Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Electrosurgical Devices Market Introduction

- Asia Pacific Electrosurgical Devices Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product Type

- By Application

- By End-user

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East & Africa Electrosurgical Devices Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Electrosurgical Devices Market Introduction

- Middle East & Africa Electrosurgical Devices Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product Type

- By Application

- By End-user

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Latin America Electrosurgical Devices Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Electrosurgical Devices Market Introduction

- Latin America Electrosurgical Devices Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product Type

- By Application

- By End-user

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Country Wise Market: Introduction

- Competition Landscape

- Global Electrosurgical Devices Market Product Mapping

- Global Electrosurgical Devices Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Electrosurgical Devices Market Tier Structure Analysis

- Global Electrosurgical Devices Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

- Medtronic plc

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

* Similar details would be provided for all the players mentioned below

- Johnson & Johnson (Ethicon)

- B. Braun Melsungen AG

- Olympus Corporation

- CONMED Corporation

- Boston Scientific Corporatio

- Smith & Nephew plc

- Erbe Elektromedizin GmbH

- KLS Martin Group

- Bovie Medical Corporation

- BOWA-electronic GmbH & Co. KG

- Stryker Corporation

- Zimmer Biomet Holdings, Inc.

- Applied Medical Resources Corporation

- Aesculap, Inc.

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables