Embedded Insurance Market Size and Forecast (2025–2033), Global and Regional Share, Trends, and Industry Analysis Report Coverage: By Insurance Type (Property, Health, Auto, Travel, Cyber, Others), By Distribution Channel (E-commerce & Online Platforms, Telecommunications & Digital Service Providers, Retail & Physical Stores, Financial Institutions & Banks, Others), By End User (Individual Customers, SMEs, Large Enterprises), and Geography

2026-01-30

Business & Financial Services

Ekta Chaurasia (Team Lead)

Description

Embedded Insurance Market Overview

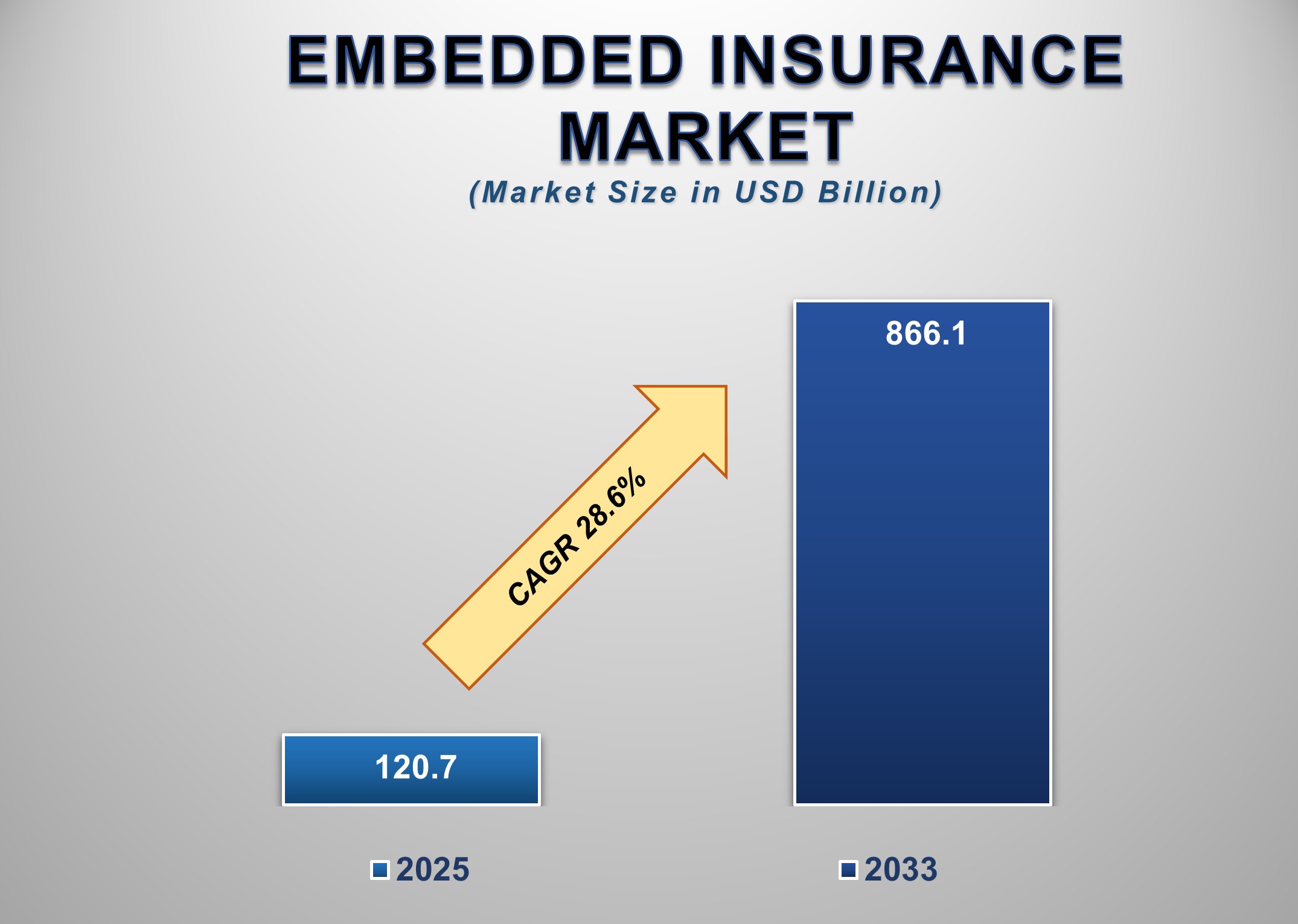

The global Embedded Insurance Market is undergoing a rapid transformation as insurance products are increasingly integrated directly into the purchase journeys of non-insurance products and services. Valued at USD 120.7 billion in 2025, the market is projected to reach an impressive USD 866.1 billion by 2033, expanding at a robust CAGR of 28.6% during the forecast period. Embedded insurance enables seamless, contextual coverage offerings at the point of sale, eliminating traditional friction associated with policy purchase and underwriting.

This model has gained significant

traction across digital commerce, mobility services, travel platforms, fintech

ecosystems, and real estate transactions. By embedding insurance into customer

journeys, such as property protection during home purchases, device insurance

at checkout, or travel insurance during ticket booking, providers can improve

conversion rates, enhance the customer experience, and unlock new revenue

streams. The rise of APIs, cloud-based insurance platforms, and real-time data

analytics has made it easier for insurers and insurtech firms to partner with

distributors and digital platforms.

Embedded Insurance Market Drivers and

Opportunities

Digital

Commerce Expansion and Platform-Based Distribution Are Driving Market Growth

The rapid expansion of digital commerce and platform-based ecosystems is a primary driver of the Embedded Insurance Market. E-commerce platforms, mobility providers, fintech applications, and online travel agencies are increasingly integrating insurance offerings directly into their user journeys. This approach allows customers to purchase relevant insurance coverage instantly, without navigating separate insurance platforms or lengthy application processes. Embedded insurance significantly improves customer convenience and conversion rates by offering protection at the moment of highest relevance. For example, consumers purchasing electronics are more likely to opt for device protection when offered during checkout, while travelers readily accept trip insurance when booking flights or accommodations. This contextual relevance has proven far more effective than traditional insurance marketing channels. From the insurer’s perspective, embedded distribution lowers customer acquisition costs and provides access to large, pre-qualified customer bases. Digital platforms benefit by enhancing customer trust, increasing average transaction values, and differentiating their offerings. As global e-commerce penetration continues to rise and super-app ecosystems expand, embedded insurance is expected to become a default feature across many digital consumer experiences.

Advancements in API-Based Insurance Infrastructure Are

Accelerating Adoption

Technological advancements, particularly the development of

API-driven insurance platforms, are playing a critical role in accelerating

embedded insurance adoption. Modern insurance APIs enable seamless integration

of underwriting, pricing, policy issuance, and claims management into

third-party platforms. This technological flexibility allows insurers and

insurtech firms to rapidly customize insurance products for specific use cases,

industries, and customer segments. Cloud computing, artificial intelligence,

and real-time data analytics further enhance embedded insurance capabilities by

enabling dynamic pricing, automated risk assessment, and instant policy

activation. These technologies allow insurers to offer personalized coverage

based on user behavior, transaction data, and contextual risk factors. As a

result, embedded insurance solutions are becoming more scalable, efficient, and

profitable. Additionally, regulatory advancements in open insurance and digital

financial services are encouraging innovation and collaboration across the

insurance value chain. As API ecosystems mature and standardization improves,

barriers to entry continue to decline, allowing new players to participate in

the embedded insurance landscape. This technology-driven evolution is expected

to sustain strong market growth over the forecast period.

Rising Demand for Contextual and On-Demand Coverage Creates

Major Opportunities

The growing consumer preference for contextual, flexible, and on-demand insurance solutions presents a significant opportunity for the Embedded Insurance Market. Modern consumers increasingly favor insurance coverage that aligns with specific activities, durations, or assets rather than traditional long-term policies. Embedded insurance perfectly addresses this demand by offering coverage precisely when and where it is needed. Opportunities are expanding rapidly across sectors such as mobility, gig economy services, property rentals, digital health, and cyber protection. For instance, ride-sharing drivers can access usage-based auto insurance, renters can obtain property coverage instantly, and SMEs can secure cyber insurance bundled with digital services. Emerging markets also offer substantial potential due to rising digital adoption and limited access to traditional insurance channels. As awareness of insurance benefits grows and digital literacy improves globally, embedded insurance providers can leverage partnerships, data-driven personalization, and innovative pricing models to unlock new customer segments. This shift toward contextual protection positions embedded insurance as a critical growth engine for the global insurance industry

Embedded Insurance Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 120.7 Billion |

|

Market Forecast in 2033 |

USD 866.1 Billion |

|

CAGR % 2025-2033 |

28.6% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors

and more |

|

Segments Covered |

●

By Insurance Type, By Distribution Channel,

By End User |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Embedded Insurance Market

Report Segmentation Analysis

The Global Embedded Insurance

Market Industry Analysis Is Segmented By Insurance Type, By Distribution

Channel, By End User, and By Region.

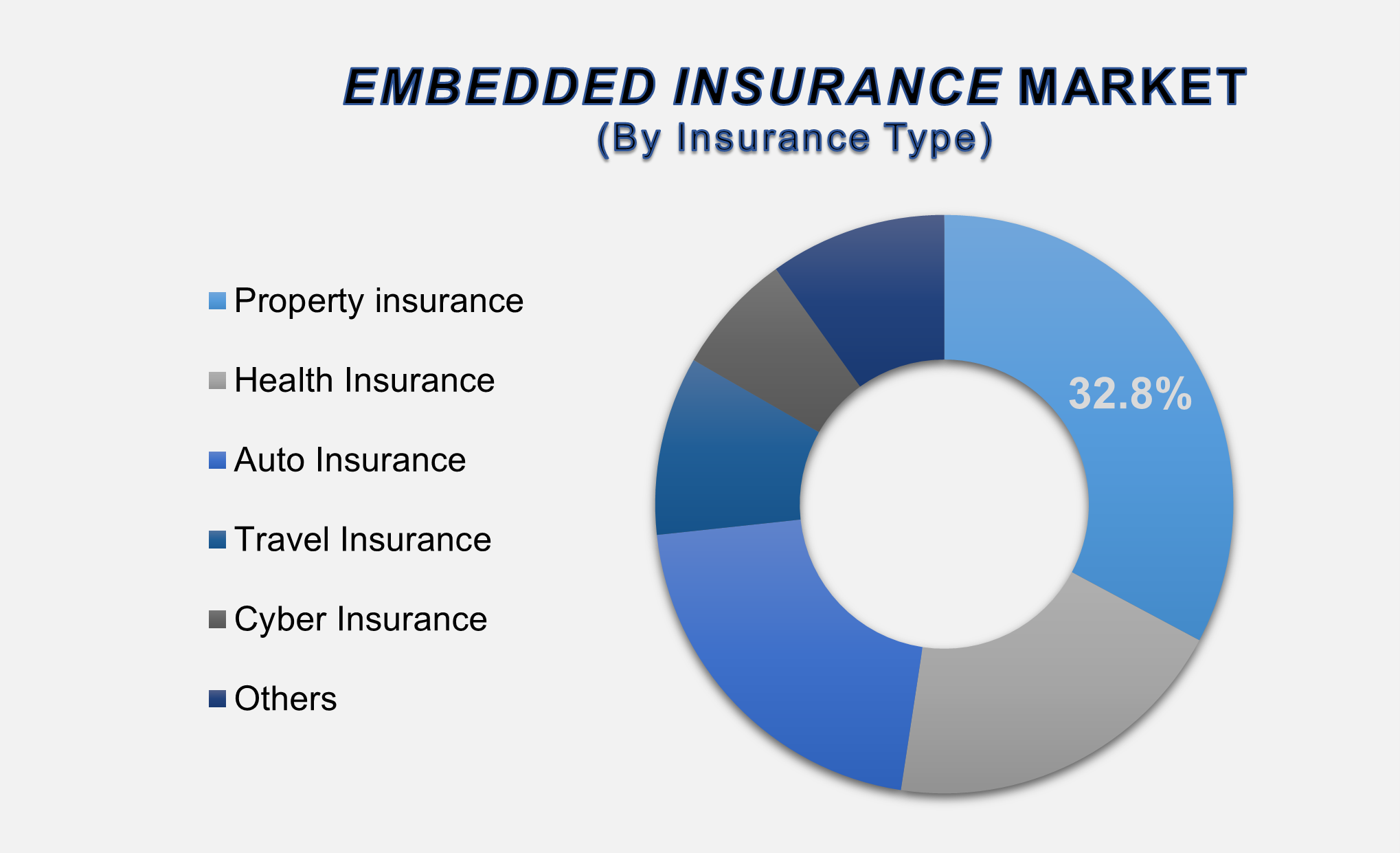

Property

Insurance Segment Accounted for the Largest Market Share in the Global Embedded

Insurance Market

The property insurance segment accounted for the largest market share, holding 32.8% of the global Embedded Insurance Market, driven by strong demand for embedded protection in real estate transactions, rental platforms, mortgage services, and home-related e-commerce purchases. Property insurance is frequently embedded into digital home-buying platforms, landlord-tenant ecosystems, and smart home services, offering instant coverage at critical transaction points. The rising adoption of digital property marketplaces and increasing awareness of asset protection have strengthened demand for embedded property insurance. Insurers benefit from predictable risk profiles and scalable distribution, while platforms gain enhanced customer trust. This segment is expected to maintain its leading position as digital property ecosystems continue to expand globally.

E-commerce and Online

Platforms Lead Distribution Due to High Digital Engagement

The e-commerce and online

platforms segment dominates the distribution channel landscape, supported by

widespread digital adoption and high transaction volumes. Online platforms

provide an ideal environment for embedding insurance due to real-time customer

data, automated workflows, and seamless payment integration. Consumers

purchasing goods, travel, or services online are more inclined to opt for

embedded coverage when presented transparently during checkout. This channel

significantly improves policy uptake rates compared to traditional insurance

sales methods. As digital commerce ecosystems grow, online platforms will

remain the primary driver of embedded insurance distribution.

Individual Customers Segment

Holds the Largest Share Due to Rising Digital Insurance Awareness

The individual customer segment

accounts for the largest share of the Embedded Insurance Market, driven by

increasing consumer familiarity with digital financial services and a

preference for convenience-based insurance solutions. Embedded insurance simplifies

the purchasing process for individuals by eliminating paperwork and enabling

instant coverage activation. Use cases such as device insurance, travel

insurance, health coverage add-ons, and personal cyber protection have

significantly boosted adoption among individual customers. As digital-native

generations increasingly enter the workforce, demand for embedded insurance

among individual users is expected to remain strong.

The following segments are

part of an in-depth analysis of the global Embedded Insurance market:

|

Market Segments |

|

|

By Insurance Type |

●

Property

insurance ●

Health

Insurance ●

Auto

Insurance ●

Travel

Insurance ●

Cyber

Insurance ●

Others |

|

By Distribution Channel |

●

E-commerce

& Online Platforms ●

Telecommunications

& Digital Service Providers ●

Retail

& Physical Stores ●

Financial

Institutions & Banks ●

Others |

|

By End User |

●

Individual

Customers ●

SMEs ●

Large

Enterprises |

Embedded Insurance Market

Share Analysis by Region

North America is

anticipated to hold the biggest portion of the Embedded Insurance Market

globally throughout the forecast period.

North America leads the global

Embedded Insurance Market with 39.8% share, supported by advanced digital

infrastructure, strong insurtech ecosystems, and high consumer acceptance of

embedded financial services. The presence of major insurtech firms, technology

platforms, and regulatory support for innovation further strengthens regional

dominance.

Asia-Pacific is projected to grow

at the highest CAGR, driven by rapid digitalization, expanding e-commerce

ecosystems, and rising demand for micro and on-demand insurance solutions.

Countries such as China, India, and Southeast Asian nations are witnessing

strong growth due to increasing smartphone penetration and financial inclusion

initiatives.

Embedded Insurance Market

Competition Landscape Analysis

The Embedded Insurance Market is

highly competitive and innovation-driven, characterized by the presence of

insurtech startups, global insurers, and technology-enabled insurance

platforms. Companies focus on API development, strategic partnerships, product

customization, and geographic expansion. Speed-to-market, scalability, and

platform integration capabilities are key competitive differentiators.

Global Embedded Insurance

Market Recent Developments News:

- In

May 2025, Bolttech and Sumitomo Corporation formed a joint venture to

deliver technology-driven embedded insurance and protection solutions to

distribution partners across Asian markets.

- In

March 2025, Smartpay Corporation partnered with Chubb Insurance Japan

to launch embedded insurance products in Japan, offering integrated

coverage within buy-now-pay-later (BNPL) and other digital transactions to

modernize the local insurance market.

- In

January 2025, Accenture acquired AOX, a German provider of embedded

software for automotive suppliers and manufacturers. The acquisition

strengthens Accenture’s ability to help automotive clients transition to

software-defined vehicles (SDVs) and manage complex embedded system

challenges.

The Global Embedded Insurance Market

Is Dominated by a Few Large Companies, such as

●

Cover Genius

●

Trov

●

Slice Labs

●

Qover

●

Bought By Many

●

Oscar Health

●

Hippo

●

Lemonade

●

Root Insurance

●

Metromile

●

Huckleberry

●

Zego

●

Cuvva

●

Sure

●

Hokodo

●

Bima

●

MicroEnsure

●

Chubb

●

AXA

●

Allianz

● Others

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

Embedded Insurance Market

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables