Energy Storage as a Service (ESaaS) Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Service Type (Battery Storage, Thermal Storage, Mechanical Storage, Hybrid Systems); By Application (Grid Storage, Commercial & Industrial, Residential, Utility-Scale); By Technology (Lithium-ion, Flow Batteries, Compressed Air, Pumped Hydro); By Contract Duration (Short-term (<5 years), Medium-term (5–10 years), Long-term (>10 years)); and Geography

2025-08-12

Energy & Power

Ekta Chaurasia (Team Lead)

Description

Energy Storage As-a-Service Market Overview

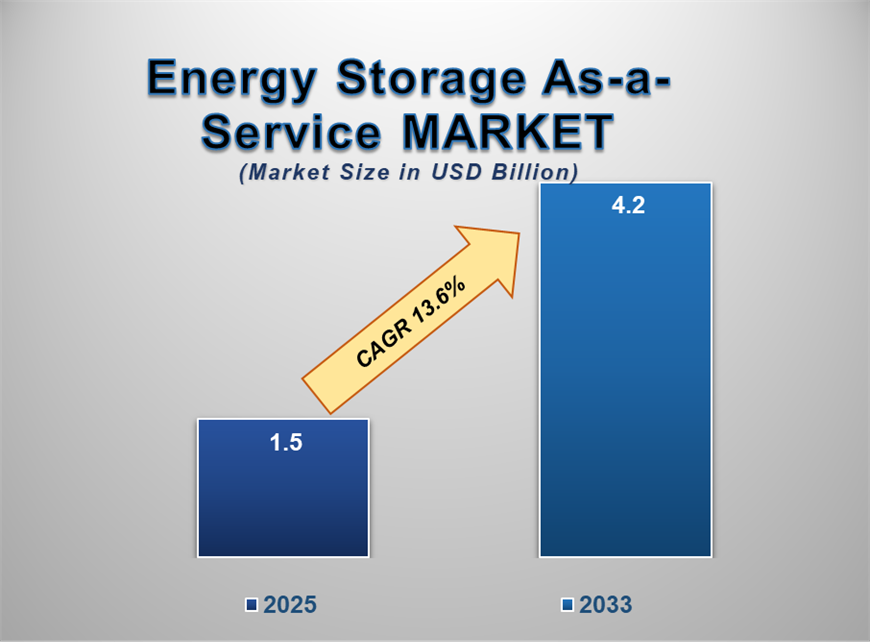

The energy storage as a service (ESaaS) market is anticipated to experience robust growth from 2025 to 2033, with increasing adoption of renewable energy sources and the integration of distributed energy systems serving as key drivers for market expansion. With an estimated valuation of approximately USD 1.39 billion in 2025, the market is expected to reach USD 4.2 billion by 2033, registering a strong compound annual growth rate (CAGR) of 13.6% over the forecast period. This upward trajectory is further propelled by advancements in battery technologies, favorable regulatory policies, and growing emphasis on sustainable energy solutions to support the global energy transition.

The energy storage as a service

(ESaaS) market has emerged as a pivotal enabler in the transition to a more

resilient, flexible, and decarbonized energy landscape. ESaaS providers deliver

comprehensive energy storage solutions, spanning battery systems, control

software, and performance management, via service-based models, allowing

end-users to access advanced storage capabilities without direct capital

investment or technical complexity. These solutions are instrumental in

balancing grid fluctuations, facilitating renewable energy integration,

performing peak shaving, and enhancing overall grid reliability. Modern ESaaS

offerings integrate cutting-edge lithium-ion, flow, and hybrid battery

chemistries within modular containerized systems, engineered for rapid

deployment and adaptable scalability.

Material innovations emphasize

durability, high energy density, efficient thermal management, and fire

resistance, reflecting the sector’s commitment to safety and operational

longevity. As global grids adapt to rising shares of intermittent renewables, ESaaS

providers are increasingly tasked with meeting stringent regulatory standards

around grid compatibility, system uptime, cybersecurity, and environmental

compliance. The ability to deliver robust, cloud-based monitoring, predictive

maintenance, and real-time performance optimization is a defining feature of

leading ESaaS models.

Moreover, evolving business needs,

ranging from cost avoidance and power quality enhancement to regulatory

compliance and decarbonization, drive continuous innovation in multi-use,

modular storage architectures and service contracts. Looking ahead, the sector’s

direction is shaped by ongoing advances in battery technology, the emergence of

solid-state and second-life solutions, and increased collaboration between

utilities, commercial & industrial players, and technology providers.

Positioned as a critical component of the future energy value chain, the ESaaS

market is expected to expand rapidly, enabling accessible, secure, and

high-performing energy storage for grid stakeholders worldwide.

Energy Storage As-a-Service Market Drivers and Opportunities

Surging Adoption of Intermittent Renewable Energy Increasing Demand for

ESaaS

The sharp increase in the deployment

of solar and wind generation has amplified the need for flexible and reliable

energy storage. As renewable sources are highly intermittent—only producing

when the sun shines or the wind blows—energy storage as a service enables grid

operators and businesses to absorb surplus generation and dispatch it when

demand peaks or renewable output falters. For instance, major projects in

California have leveraged ESaaS solutions to balance large solar installations,

storing excess energy midday for evening release, directly supporting grid

stability and renewable integration

Regulatory Push for Grid Modernization and Carbon Emissions Reduction

Tightening regulations around carbon

reduction and grid resiliency are propelling utilities and industry to seek out

storage solutions without major capital investment. Energy storage as a service

allows organizations to rapidly deploy battery assets, complying with

decarbonization mandates and power quality regulations. In the UK, National

Grid ESO partnered with multiple ESaaS providers for fast frequency response

and emissions compliance, accelerating the transition to a cleaner, more

reliable electricity network.

Opportunity for the Energy Storage As-a-Service Market

Integration of Artificial Intelligence for Smart Energy Storage

Optimization

The convergence of AI with ESaaS is

opening new frontiers in predictive maintenance, real-time optimization, and

dynamic load balancing. By leveraging smart algorithms, ESaaS providers can

enhance battery life, forecast demand, and reduce operational costs for

clients. A recent example is STEM Inc., which has integrated AI tools with its

ESaaS offerings, enabling commercial customers across North America to minimize

peak charges and intelligently manage their distributed energy resources

Expansion of Utility-Scale and Hybrid Renewable and Storage Projects

Hybrid projects combining large-scale

batteries, solar, and wind are becoming a cornerstone for reliable,

round-the-clock clean energy supply. ESaaS providers are capitalizing on this

trend by offering turnkey solutions for utility-scale installations. In India,

Avaada is pioneering hybrid renewable-plus-storage projects using the ESaaS

model, allowing utilities to maximize grid flexibility and renewable energy

utilization while minimizing curtailment and infrastructure costs

Energy Storage As-a-Service Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 1.39 Billion |

|

Market Forecast in

2033 |

USD

4.2 Billion |

|

CAGR % 2025-2033 |

13.6% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company

share, company heatmap, company production Capacity, growth factors and more |

|

Segments Covered |

· By Service Type · By Application · By Technology · By Contract Duration |

|

Regional Scope |

·

North America ·

Europe ·

APAC ·

Latin America ·

Middle East and Africa |

|

Country Scope |

1) U.S. 2) Canada 3) U.K. 4) Germany 5) France 6) Italy 7) Spain 8) Netherland 9) China 10) India 11) Japan 12) South Korea 13) Australia 14) Mexico 15) Brazil 16) Argentina 17) Saudi Arabia 18) UAE 19) South Africa |

Energy

Storage As-a-Service Market Report

Segmentation Analysis

The global Energy Storage As-a-Service

Market industry analysis is segmented into by Service Type, by Application, by

Technology, by Contract Duration, and by Region.

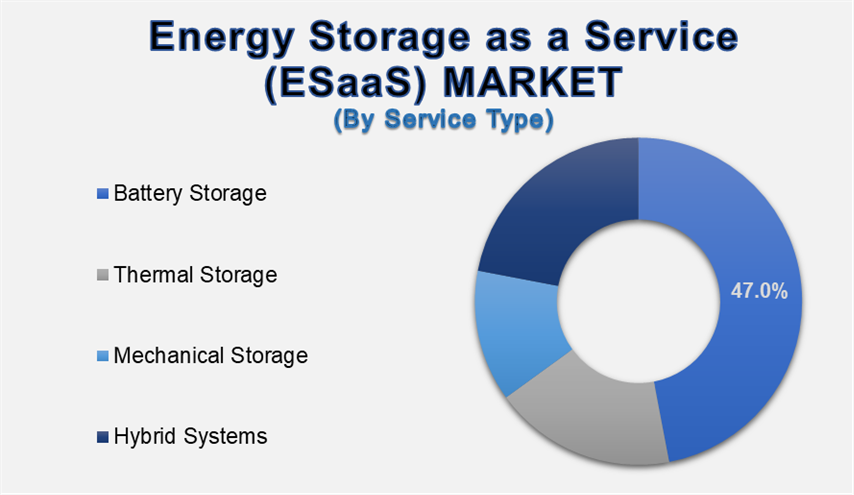

Battery Storage Segment Holds the Largest Share in the Energy Storage

As-a-Service Market

The battery storage segment dominates

the Energy Storage As-a-Service (ESaaS) market, fueled by its versatility,

scalability, and cost-efficiency in a broad array of applications including

grid balancing, renewable integration, and backup power. Battery systems,

chiefly lithium-ion technology, account for nearly half of the market share due

to their rapid response, high energy density, and proven

reliability. These systems enable peak shaving, load shifting, and

frequency regulation, which are crucial for both utilities and commercial

customers seeking operational flexibility without upfront capital investments.

For example, large-scale ESaaS deployments in California and the UK leverage

battery storage to provide critical grid services and renewable energy

smoothing, underpinning the widespread preference for battery-based solutions

across global markets.

Utility Application Segment Holds the Largest Share in the Energy Storage As-a-Service Market.

The utility application segment dominates the Energy

Storage As-a-Service (ESaaS) Market and is projected to exhibit the highest

growth potential over the forecast period. Utilities are leading adopters of

ESaaS due to the crucial need for large-scale grid stabilization and efficient

integration of intermittent renewables like solar and wind. Regulatory mandates

for improved grid reliability, decarbonization, and peak demand management are

driving utilities to implement flexible energy storage solutions without major

capital expenditures. A recent example is the deployment of ESaaS battery

systems by National Grid ESO in the UK, delivering fast frequency response and

ensuring resilient grid operations as renewable penetration accelerates.

Lithium-Ion Technology Segment Expected to Register Significant CAGR in ESaaS Market.

The lithium-ion technology segment is witnessing the fastest growth in the ESaaS industry, underpinned by its high energy density, rapid deployment capability, and proven scalability. Lithium-ion batteries have become the preferred choice for storage assets across ESaaS deployments, enabling reliable short- and medium-duration storage vital for both grid and behind-the-meter applications. Ongoing technological improvements and cost declines are further accelerating their adoption. For instance, Stem Inc., a leading ESaaS provider, has expanded its North American project pipeline with advanced, AI-optimized lithium-ion battery storage systems now supporting hundreds of commercial and utility sites.

Short-Term Contract Duration Segment Sees Increased Adoption by Commercial and Industrial Users

Short-term (<5 years) contract

duration is emerging as a high-growth segment, particularly among commercial

and industrial clients seeking flexible, rapid deployment of energy storage

solutions to manage peak demand charges and respond to market pricing

volatility. ESaaS offerings enable these clients to access storage capacity

without long-term commitments or capital outlay, allowing faster adaptation to

evolving operational and regulatory contexts. In the United States, a growing

number of small and mid-sized enterprises are entering short-term ESaaS

agreements for localized grid support, as seen in recent contracts between

C&I facilities and regional ESaaS service providers

The following segments are part of an

in-depth analysis of the global Energy Storage As-a-Service Market:

|

Market

Segments |

|

|

By

Service

Type |

·

Battery Storage ·

Thermal Storage ·

Mechanical Storage ·

Hybrid Systems |

|

By Application |

·

Grid Storage ·

Commercial & Industrial ·

Residential ·

Utility-Scale |

|

By Technology |

·

Lithium-ion ·

Flow Batteries ·

Compressed Air ·

Pumped Hydro |

|

By

Contract Duration |

·

Short-term (<5 years) ·

Medium-term (5-10 years) ·

Long-term (>10 years) |

Asia-Pacific Region Poised for the Fastest Growth in ESaaS Market

The Asia-Pacific region is anticipated

to experience the strongest growth in the ESaaS market, driven by rapid

urbanization, government-led renewable energy initiatives, and accelerated

infrastructure investments across emerging economies. Countries such as China,

India, and Japan are witnessing a surge in ESaaS deployments, with national

policies actively supporting large-scale grid modernization and renewable

integration. For example, in India, Avaada has launched hybrid

renewable-plus-storage projects utilizing the ESaaS model, supporting the grid

and enabling higher utilization of variable clean energy resources.

Energy Storage As-a-Service Market Competition Landscape Analysis

The market

is competitive, with several established players and new entrants offering a

range of energy storage as a service (ESaaS) products. Some of the

key players Fluence Energy, Ambri, Stem, Inc., Swell Energy, Sunrun, Sonnen,

Generac Power Systems, Engie Storage, Eos Energy Storage, Powin Energy,

NantEnergy, Nidec ASI, Nuvve, Pivot Power, Quidnet Energy, Redflow, Renault,

and Siemens Gamesa Renewable Energy and others

Global Energy Storage As-a-Service Market Recent Developments News:

o On June

12, 2025, Avaada, a major renewable energy firm in India, announced the

conceptualization and development of large-scale, integrated

renewable-plus-storage projects utilizing the ESaaS model. These projects

target grid reliability enhancement and provide 24/7 clean power supply by

colocating utility-scale battery plants with solar and wind farms, underscoring

the expanding role of hybrid ESaaS solutions in Asia’s energy transition.

o In Q1

2025, the U.S. energy storage market achieved a historic milestone, adding over

2 GW of new capacity across all ESaaS segments—the highest quarterly addition

on record. This reflects robust demand for flexible, third-party energy storage

deployment driven by policy incentives and greater renewable grid integration,

further solidifying ESaaS as a preferred industry model.

o In early

2025, the UK’s National Grid ESO expanded its fast frequency response

initiatives by contracting multiple ESaaS providers for large-scale battery

deployments. These projects aim to stabilize the grid and mitigate the

intermittency of growing wind and solar assets, exemplifying increased ESaaS

adoption in mature energy markets.

o On March

7, 2025, a global industry report highlighted that vehicle-to-grid (V2G)

technologies are gaining traction as a transformative opportunity for ESaaS

operators, allowing EVs to serve as distributed storage assets. This trend

supports both grid flexibility and new business models for energy storage

service providers, especially in the U.S. and Europe

The Global Energy Storage As-a-Service Market is dominated by a few

large companies, such as

·

Fluence Energy

·

Ambri

·

Stem, Inc.

·

Swell Energy

·

Sunrun

·

Sonnen

·

Generac Power Systems

·

Engie Storage

·

Eos Energy Storage

·

Powin Energy

·

NantEnergy

·

Nidec ASI

·

Nuvve

·

Pivot Power

·

Quidnet Energy

·

Redflow

·

Renault

·

Siemens Gamesa Renewable Energy

· Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

- Global Energy Storage as a Service (ESaaS) Market Introduction and Market Overview

- Objectives of the Study

- Global Energy Storage as a Service (ESaaS) Market Scope and Market Estimation

- Global Energy Storage as a Service (ESaaS) Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Energy Storage as a Service (ESaaS) Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

- Market Segmentation

- Service Type of Global Energy Storage as a Service (ESaaS) Market

- Application of Global Energy Storage as a Service (ESaaS) Market

- Technology of Global Energy Storage as a Service (ESaaS) Market

- Contract Duration of Global Energy Storage as a Service (ESaaS) Market

- Region of Global Energy Storage as a Service (ESaaS) Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Energy Storage as a Service (ESaaS) Market

- Technological Advancements

- Porter’s Five Forces Analysis

- Bargaining Power of Suppliers

- Bargaining Power of Buyers

- Threat of Substitutes

- Threat of New Entrants

- Competitive Rivalry

- PEST Analysis

- Political Factors

- Economic Factors

- Social Factors

- Technology Factors

- Global Energy Storage as a Service (ESaaS) Market Estimates & Historical Trend Analysis (2020 - 2024)

- Global Energy Storage as a Service (ESaaS) Market Estimates & Forecast Trend Analysis, by Service Type

- Global Energy Storage as a Service (ESaaS) Market Revenue (US$ Bn) Estimates and Forecasts, by Service Type, 2020 - 2033

- Battery Storage

- Thermal Storage

- Mechanical Storage

- Hybrid Systems

- Global Energy Storage as a Service (ESaaS) Market Revenue (US$ Bn) Estimates and Forecasts, by Service Type, 2020 - 2033

- Global Energy Storage as a Service (ESaaS) Market Estimates & Forecast Trend Analysis, by Application

- Global Energy Storage as a Service (ESaaS) Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- Grid Storage

- Commercial & Industrial

- Residential

- Utility-Scale

- Global Energy Storage as a Service (ESaaS) Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- Global Energy Storage as a Service (ESaaS) Market Estimates & Forecast Trend Analysis, by Technology

- Global Energy Storage as a Service (ESaaS) Market Revenue (US$ Bn) Estimates and Forecasts, by Technology, 2020 - 2033

- Lithium-ion

- Flow Batteries

- Compressed Air

- Pumped Hydro

- Global Energy Storage as a Service (ESaaS) Market Revenue (US$ Bn) Estimates and Forecasts, by Technology, 2020 - 2033

- Global Energy Storage as a Service (ESaaS) Market Estimates & Forecast Trend Analysis, by Contract Duration

- Global Energy Storage as a Service (ESaaS) Market Revenue (US$ Bn) Estimates and Forecasts, by Contract Duration, 2020 - 2033

- Short-term (<5 years)

- Medium-term (5-10 years)

- Long-term (>10 years)

- Global Energy Storage as a Service (ESaaS) Market Revenue (US$ Bn) Estimates and Forecasts, by Contract Duration, 2020 - 2033

- Global Energy Storage as a Service (ESaaS) Market Estimates & Forecast Trend Analysis, by region

- Global Energy Storage as a Service (ESaaS) Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Energy Storage as a Service (ESaaS) Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020 - 2033

- North America Energy Storage as a Service (ESaaS) Market: Estimates & Forecast Trend Analysis

- North America Energy Storage as a Service (ESaaS) Market Assessments & Key Findings

- North America Energy Storage as a Service (ESaaS) Market Introduction

- North America Energy Storage as a Service (ESaaS) Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Service Type

- By Application

- By Technology

- By Contract Duration

- By Country

- The U.S.

- Canada

- North America Energy Storage as a Service (ESaaS) Market Assessments & Key Findings

- Europe Energy Storage as a Service (ESaaS) Market: Estimates & Forecast Trend Analysis

- Europe Energy Storage as a Service (ESaaS) Market Assessments & Key Findings

- Europe Energy Storage as a Service (ESaaS) Market Introduction

- Europe Energy Storage as a Service (ESaaS) Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Service Type

- By Application

- By Technology

- By Contract Duration

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Netherland

- Rest of Europe

- Europe Energy Storage as a Service (ESaaS) Market Assessments & Key Findings

- Asia Pacific Energy Storage as a Service (ESaaS) Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Energy Storage as a Service (ESaaS) Market Introduction

- Asia Pacific Energy Storage as a Service (ESaaS) Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Service Type

- By Application

- By Technology

- By Contract Duration

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Energy Storage as a Service (ESaaS) Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Energy Storage as a Service (ESaaS) Market Introduction

- Middle East & Africa Energy Storage as a Service (ESaaS) Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Service Type

- By Application

- By Technology

- By Contract Duration

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Energy Storage as a Service (ESaaS) Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Energy Storage as a Service (ESaaS) Market Introduction

- Latin America Energy Storage as a Service (ESaaS) Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Service Type

- By Application

- By Technology

- By Contract Duration

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Energy Storage as a Service (ESaaS) Market Product Mapping

- Global Energy Storage as a Service (ESaaS) Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Energy Storage as a Service (ESaaS) Market Tier Structure Analysis

- Global Energy Storage as a Service (ESaaS) Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

- Fluence Energy

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Fluence Energy

* Similar details would be provided for all the players mentioned below

- ENGIE SA

- Honeywell International Inc.

- NRStor Inc.

- Siemens AG

- Eaton Corporation

- Convergent Energy + Power

- Stem, Inc.

- Aggreko Ltd.

- Enel X (Enel Group)

- Tesla, Inc.

- EDF Renewables

- AES Corporation

- Customized Energy Solutions (CES)

- Powin Energy

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables