Epoxy Curing Agents Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; Curing Agent (Amine-based curing agents, Anhydride-based Curing Agents, and Others), Application (Paints and Coatings, Adhesives, Composites, Electronic encapsulation, and Others), End User (Building and construction, Transportation, General Industrial, Wind Power, Aerospace, Marine, and Others), Raw Material (Organic Compounds and Inorganic Compounds) and Geography

2026-02-04

Chemicals & Materials

Jaya Bundele (Research Analyst)

Description

Epoxy Curing

Agents Market Overview

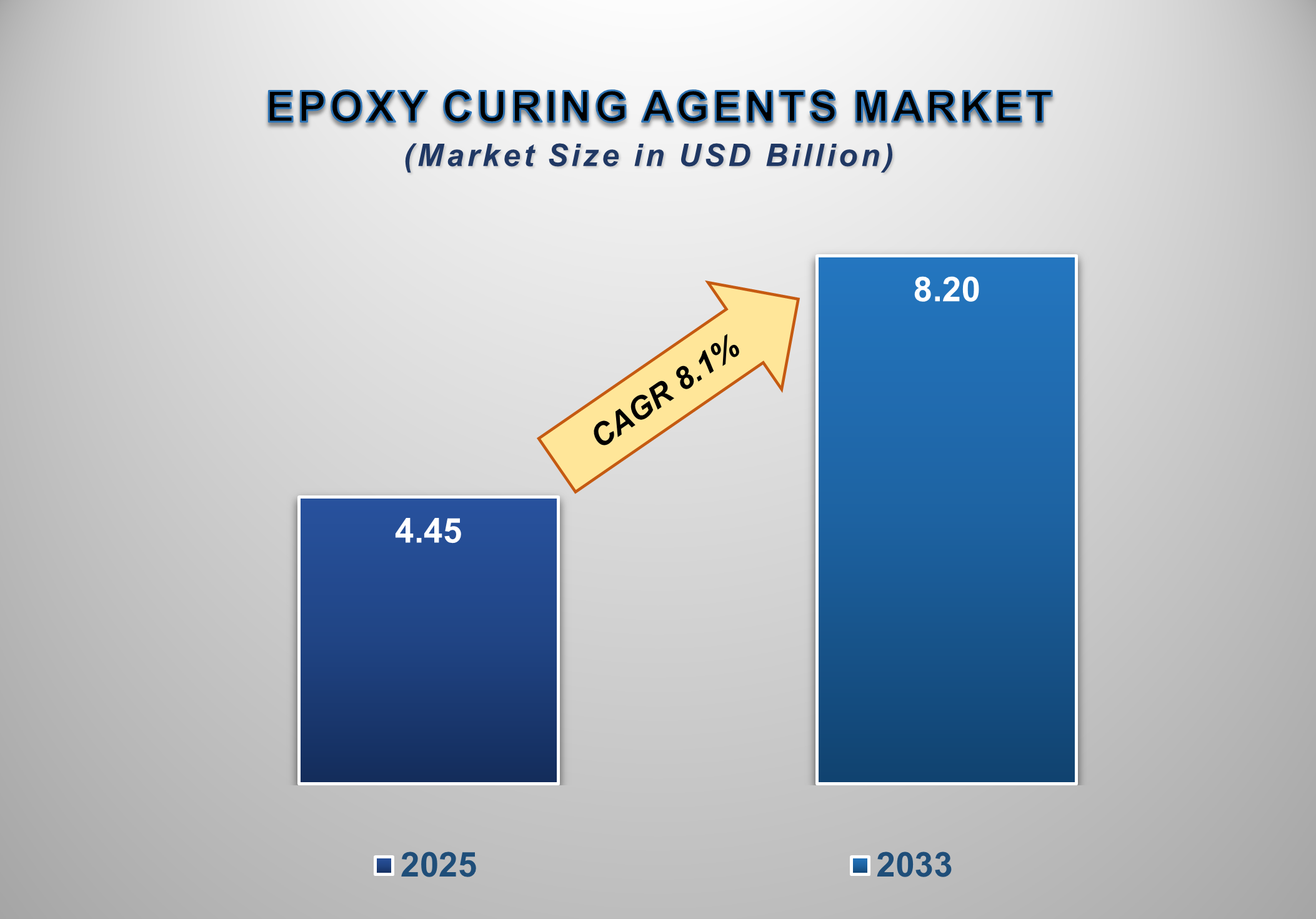

The Global Epoxy Curing Agents Market is experiencing strong growth, driven by the expanding use of epoxy resins across construction, automotive, aerospace, electronics, wind energy, and industrial coatings. Valued at USD 4.45 billion in 2025, the market is projected to reach USD 8.20 billion by 2033, growing at a CAGR of 8.1% during the forecast period.

Epoxy resin use in construction, coatings, adhesives,

composites, and electrical and electronics applications is steadily increasing,

propelling the market for epoxy curing agents. The demand for epoxy-based

protective coatings and flooring systems is rising due to rapid urbanization

and infrastructure development, especially in the Asia-Pacific and the Middle

East. This directly supports the need for curing agents. Demand is further

increased by the expansion of wind energy, automotive lightweighting, and aerospace

composites, as epoxy systems are frequently used to produce strong,

long-lasting composite materials.

The versatility of epoxy curing agents, particularly

amine-based systems, which provide fast curing, robust mechanical qualities,

and compatibility with a variety of epoxy resins, is a major factor driving

demand. Because of their superior thermal and dielectric qualities,

anhydride-based curing agents are still in steady demand in high-temperature

and electrical insulation applications. In addition, specialist curing agents

like polyamides, phenolics, and bio-based solutions are becoming more popular in

performance-driven and specialized applications.

The availability and cost of raw materials, including

amines, petrochemical derivatives, and bio-based feedstocks, have an impact on

the market on the supply side. Production costs and profits may be impacted by

disruptions to the supply chain and fluctuations in the price of crude oil. Top

producers concentrate on backward integration, long-term supplier agreements,

and regional industrial growth to reduce these risks.

Market dynamics are being shaped by regulatory and environmental constraints.

Innovation in low-toxicity, low-VOC, and sustainable curing agents is being

driven by stricter laws on volatile organic compounds (VOCs), toxic amines, and

workplace exposure. This includes increasing R&D spending on bio-based

substitutes made from renewable resources, latent curing agents, and

water-borne systems.

Large, international chemical corporations and local experts

coexist amid competitive dynamics. Pricing, customization, application support,

and product performance are the main factors that drive competition. Strategic

alliances with manufacturers of epoxy resin and end-use formulators are

becoming more crucial for preserving market share. Thus, industrialization,

infrastructure development, and continuous innovation in high-performance and

sustainable curing technologies are likely to support the market's steady

growth for epoxy curing agents.

Epoxy Curing

Agents Market Drivers and Opportunities

Growing Demand from

Construction and Infrastructure

The market for epoxy curing agents

is mostly driven by the building and infrastructure industries. Epoxy systems'

exceptional mechanical strength, chemical resistance, and longevity make them useful in flooring, adhesives, repair mortars, and protective

coatings. The need for curing agents is being driven by the rapid urbanization,

extensive infrastructure projects, and rehabilitation activities, particularly

in emerging nations, which are increasing the consumption of epoxy-based

materials.

Expansion of Coatings and Industrial Applications

Epoxy curing agents are widely

used in protective and industrial coatings. The market is expanding due to the

growing need for corrosion-resistant coatings in the oil and gas, marine, power

generation, and industrial manufacturing sectors. Curing agents based on amines

and polyamides are especially preferred because of their high adhesive

qualities and rapid curing times, which facilitate effective industrial

processes.

Growth in Composites and Lightweight Materials

Another significant growth driver

is the growing application of epoxy composites in wind energy, automotive,

aerospace, and sporting goods. High-performance composites with superior

strength-to-weight ratios and thermal stability are made possible by epoxy

curing agents. Epoxy curing agents are still in high demand due to the

expansion of renewable energy, especially wind turbine installations.

Development of Sustainable and Bio-Based Curing Agents

Sustainability objectives present

strong potential for innovation and environmental regulations. Bio-based,

low-toxicity, and low-VOC curing agents made from renewable feedstocks are

being invested in by manufacturers. These products are being used more and more

in environmentally friendly industrial applications, green structures, and

eco-friendly coatings.

Advancements in Specialty and High-Performance Systems

Specialty curing agents with

improved qualities, like rapid cure times, greater thermal resistance, and

better electrical performance, are in greater demand. Latent curing agents,

anhydride systems for electronics, and specialized formulations for advanced

composites and electrical insulation are all areas with potential.

Emerging Markets and Regional Expansion

Emerging economies in Latin

America, the Middle East, and the Asia-Pacific

present substantial development prospects due to growing manufacturing bases

and infrastructural investments. Strategic alliances, local manufacturing, and

customized product offers can all help suppliers take advantage of these

rapidly expanding markets.

Epoxy Curing Agents Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 4.45 Billion |

|

Market Forecast in 2033 |

USD 8.20 Billion |

|

CAGR % 2025-2033 |

8.1% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Comprehensive global Epoxy

Curing Agents Market size and forecast analysis, product type and

distribution channel assessment, end-user consumption trends, industrial and

direct sales performance evaluation, regional and country-level market

insights, competitive landscape and market share analysis, technological

advancements in curing chemistries and formulations, digital transformation

and e-procurement impact, growth drivers, challenges, opportunities, and

strategic insights for epoxy resin manufacturers, formulators, distributors,

and investors. |

|

Segments Covered |

●

By Curing Agent ●

By Application ●

By End User ●

By Raw Material |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Switzerland 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19)

South Africa |

Epoxy Curing Agents

Market Report Segmentation Analysis

The global Epoxy Curing Agents

Market analysis is segmented by Curing Agent, Application, End User, Raw

Material, and Region.

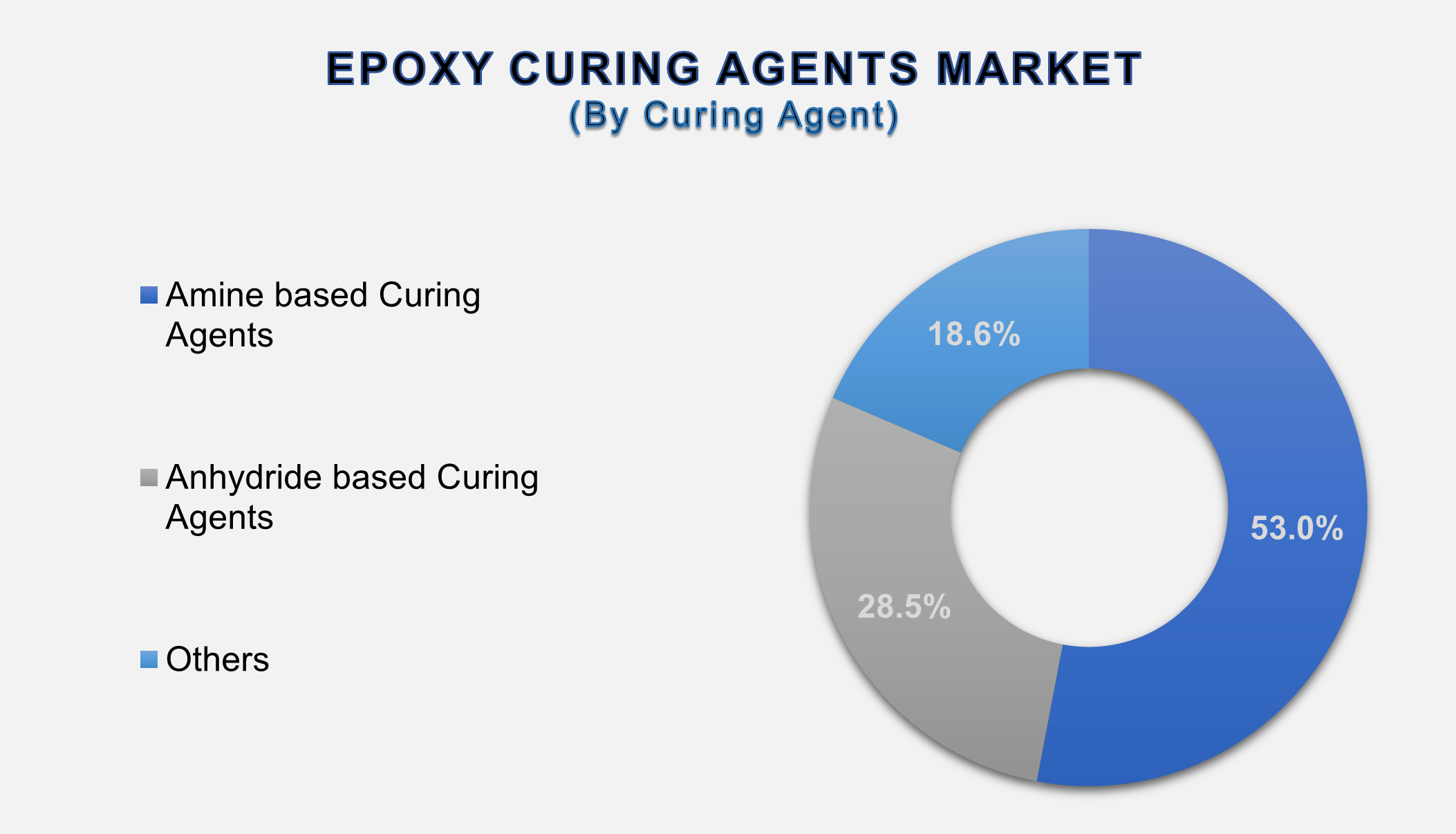

The Amine based Curing

Agents segment dominated the market in 2025 and is projected to grow at the

highest CAGR during the forecast period.

By curing agent, the Epoxy Curing

Agents Market is segmented into amine-based curing agents, anhydride-based

curing agents, and others. The amine-based curing agents segment accounts for

the largest share of the global Epoxy Curing Agents Market. Amine-based curing

agents represent the largest and most widely used category. They are prized for

their extensive compatibility with epoxy resins, superior mechanical strength,

high adhesion, and quick cure rates. Coatings, adhesives, flooring,

construction, maritime, and composite applications all frequently employ amine

curing agents. Formulators can customize performance attributes, including cure

speed, chemical resistance, and temperature tolerance, by using variants like

aliphatic, cycloaliphatic, and aromatic amines. Low-toxicity, low-VOC, and

modified amine systems are the main areas of ongoing innovation to satisfy

sustainability and legal criteria.

The paints and coatings

segment holds the highest share of the Application Segment over the forecast

period

Based

on application, the market is bifurcated into paints and coatings, adhesives,

composites, electronic encapsulation, and others. The paints and coatings

segment accounts for the largest share of the market. Epoxy curing agents are

widely used in paints and coatings due to the demand for high-performance,

long-lasting protective surfaces. Epoxy systems' superior adhesion, chemical

resistance, corrosion protection, and mechanical strength make them popular in

industrial, marine, automotive, and protective coatings. In order to determine

coating characteristics like hardness, cure time, and environmental resistance,

curing agents are essential. Curing agents based on amines and polyamides are

frequently chosen because of their adaptability and quick curing. The market is

still expanding due to increased infrastructure development and the need for

corrosion-resistant coatings.

Building and construction hold the highest share of the end-user

segment over the forecast period

Based on the end user, the market

is bifurcated into building & construction, transportation, general

industrial, wind power, aerospace, marine & others. The building and

construction segment accounts for the largest share of the market. A

significant end-use market for epoxy curing agents is building and

construction, which is motivated by the demand for materials that are strong,

long-lasting, and durable. Epoxy solutions are frequently utilized in grouts,

protective coatings, structural adhesives, flooring, and concrete restoration.

Crucial performance attributes, including durability, chemical resistance,

load-bearing strength, and curing speed, are all determined by curing

chemicals. Amine-based curing agents are widely employed because of their

excellent adherence to steel and concrete and their adaptability. Globally, the

need for epoxy curing agents in construction applications is being driven by

increased urbanization, infrastructure development, and renovation operations.

The Organic Compounds Segment will

probably dominate the market during the forecast period

In terms of raw material, the

Epoxy Curing Agents Market is segmented into organic compounds and inorganic

compounds. The organic compounds segment holds the largest share of the Epoxy

Curing Agents Market. Since the majority of curing systems are produced from

organic amines, anhydrides, polyamides, and similar chemistries, organic

compounds serve as the chemical basis for epoxy curing agents. The regulated

crosslinking of epoxy resins made possible by these organic compounds produces

materials with excellent mechanical strength, chemical resistance, and thermal

stability. Their molecular structure can be modified to change their

performance, flexibility, and rate of cure under different environmental

circumstances. For epoxy formulations to achieve application-specific qualities

in coatings, adhesives, construction, and composite materials, organic

chemicals are crucial. Safer, less toxic, and bio-based organic curative

chemicals are the subject of ongoing innovation.

The following segments are

part of an in-depth analysis of the global Epoxy Curing Agents Market:

|

Market

Segments |

|

|

By Curing

Agent |

●

Amine-based curing

agents ▪

Aliphatic Amines ▪

Cycloaliphatic

Amines ▪

Aromatic Amines ▪

Polyamides ▪

Others ●

Anhydride-based

Curing Agents ●

Others |

|

By Application |

●

Paints and Coatings ●

Adhesives ●

Composites ●

Electronic

encapsulation ●

Others |

|

By End User |

●

Building and

construction ●

Transportation ●

General Industrial ●

Wind Power ●

Aerospace ●

Marine ●

Others |

|

By Raw

Material |

●

Organic Compounds ●

Inorganic

Compounds |

Epoxy Curing Agents Market Share Analysis by

Region

The Asia-Pacific region

is projected to hold the largest share of the global Epoxy Curing Agents Market

over the forecast period.

The

Asia-Pacific region is projected to hold the largest share of the global Epoxy

Curing Agents Market over the forecast period and is also expected to be the

fastest-growing region. Rapid urbanization, industrialization, and

infrastructure development are the main drivers of market expansion. Market

expansion is supported by robust demand from the automotive, wind energy,

construction, coatings, and electronics sectors. Nations like South Korea,

China, India, and Japan are important contributors due to their significant

manufacturing bases and rising investments in infrastructure and industrial

projects. Asia-Pacific is a crucial growth hub for market players due to its

cost-effective production, growing capacity for epoxy resin, and increasing use

of sustainable and high-performance curing agents.

Global Epoxy

Curing Agents Market Recent Developments News:

●

In March 2025,

Baxxodur® EC 151, a novel amine-based epoxy curing agent with low volatile

organic compound emissions and improved performance, was introduced

commercially by BASF and Sika for use in environmentally friendly flooring

applications.

●

In June 2025, Aditya

Birla Group stated that it had acquired a

specialty chemical manufacturing facility in Dalton, Georgia, USA, in order to

greatly increase its yearly capacity for producing innovative materials and

epoxy curing agents.

●

In July 2025, Evonik

Industries AG advanced sustainability activities by converting its global epoxy

curing agent production plants in Germany, the UK, Japan, the US, and Singapore

to run entirely on renewable electricity.

The Global

Epoxy Curing Agents Market is dominated by a few large companies, such as

●

Huntsman Corporation

●

Hexion Inc.

●

BASF SE

●

Evonik Industries AG

●

Olin Corporation

●

Cardolite Corporation

●

Atul Ltd.

●

Aditya Birla Chemicals

●

KUKDO Chemical Co.,

Ltd.

●

Mitsubishi Chemical

Corporation

●

Gabriel Performance

Products

●

Air Products and

Chemicals, Inc.

●

DIC Corporation

●

Shandong Deyuan Epoxy

Resin Co., Ltd.

●

Toray Industries, Inc.

●

Kumho P&B

Chemicals Inc.

●

Momentive Specialty

Chemicals, Inc.

●

Grasim Industries Ltd.

●

RAMPF Group

● Cargill Incorporated

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1.

Global Epoxy Curing Agents Market Introduction and Market Overview

1.1.

Objectives of the Study

1.2.

Global Epoxy Curing Agents Market Scope and Market Estimation

1.2.1.Global Epoxy

Curing Agents Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Epoxy

Curing Agents Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market Segmentation

1.3.1.Curing Agent

of Global Epoxy Curing Agents Market

1.3.2.Application

of Global Epoxy Curing Agents Market

1.3.3.End User of

Global Epoxy Curing Agents Market

1.3.4.Raw Material of

Global Epoxy Curing Agents Market

1.3.5.Region of

Global Epoxy Curing Agents Market

2.

Executive

Summary

2.1.

Demand Side Trends

2.2.

Key Market Trends

2.3.

Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand and Opportunity Assessment

2.5.

Market Dynamics

2.5.1.Drivers

2.5.2.Limitations

2.5.3.Opportunities

2.5.4.Impact

Analysis of Drivers and Restraints

2.6.

Porter’s Five Forces Analysis

2.7.

PEST Analysis

2.8.

Key Regulation

2.9.

Key Developments

2.10. Value

Chain / Ecosystem Analysis

3.

Global

Epoxy Curing Agents Market Estimates & Historical Trend Analysis (2020 - 2024)

4. Global Epoxy Curing Agents Market Estimates & Forecast Trend Analysis, by Curing Agent

4.1.

Global Epoxy Curing Agents Market Revenue (US$ Bn) Estimates and

Forecasts, by Curing Agent, 2020 - 2033

4.1.1.Amine based

curing agents

4.1.1.1.

Aliphatic Amines

4.1.1.2.

Cycloaliphatic Amines

4.1.1.3.

Aromatic Amines

4.1.1.4.

Polyamides

4.1.1.5.

Others

4.1.2.Anhydride

based Curing Agents

4.1.3.Others

5. Global Epoxy Curing Agents Market Estimates & Forecast Trend Analysis, by Application

5.1.

Global Epoxy Curing Agents Market Revenue (US$ Bn) Estimates and

Forecasts, by Application, 2020 - 2033

5.1.1.Paints and

Coating

5.1.2.Adhesives

5.1.3.Composites

5.1.4.Electronic

encapsulation

5.1.5.Others

6. Global Epoxy Curing Agents Market Estimates & Forecast Trend Analysis, by End User

6.1.

Global Epoxy Curing Agents Market Revenue (US$ Bn) Estimates and

Forecasts, by End User, 2020 - 2033

6.1.1.Building and

construction

6.1.2.Transportation

6.1.3.General

Industrial

6.1.4.Wind Power

6.1.5.Aerospace

6.1.6.Marine

6.1.7.Others

7. Global Epoxy Curing Agents Market Estimates & Forecast Trend Analysis, by Raw Material

7.1.

Global Epoxy Curing Agents Market Revenue (US$ Bn) Estimates and

Forecasts, by Raw Material, 2020 - 2033

7.1.1.Organic

Compounds

7.1.2.Inorganic

Compounds

8.

Global

Epoxy Curing Agents Market Estimates & Forecast Trend Analysis, by Region

8.1.

Global Epoxy Curing Agents Market Revenue (US$ Bn) Estimates and

Forecasts, by Region, 2020 - 2033

8.1.1.North America

8.1.2.Europe

8.1.3.Asia Pacific

8.1.4.Middle East

& Africa

8.1.5.Latin America

9.

North America Epoxy

Curing Agents Market: Estimates &

Forecast Trend Analysis

9.1.

North America Epoxy Curing Agents Market Assessments & Key

Findings

9.1.1.North America

Epoxy Curing Agents Market Introduction

9.1.2.North America

Epoxy Curing Agents Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Curing Agent

9.1.2.2. By Application

9.1.2.3. By End User

9.1.2.4. By Raw Material

9.1.2.5.

By Country

9.1.2.5.1.

The U.S.

9.1.2.5.2.

Canada

10.

Europe Epoxy

Curing Agents Market: Estimates &

Forecast Trend Analysis

10.1. Europe

Epoxy Curing Agents Market Assessments & Key Findings

10.1.1.

Europe Epoxy Curing Agents Market Introduction

10.1.2.

Europe Epoxy Curing Agents Market Size Estimates and Forecast (US$

Billion) (2020 - 2033)

10.1.2.1. By Curing Agent

10.1.2.2. By Application

10.1.2.3. By End User

10.1.2.4. By Raw Material

10.1.2.5. By

Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Russia

10.1.2.5.7. Rest of Europe

11.

Asia Pacific Epoxy

Curing Agents Market: Estimates &

Forecast Trend Analysis

11.1. Asia

Pacific Epoxy Curing Agents Market Assessments & Key Findings

11.1.1.

Asia Pacific Epoxy Curing Agents Market Introduction

11.1.2.

Asia Pacific Epoxy Curing Agents Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

11.1.2.1. By Curing Agent

11.1.2.2. By Application

11.1.2.3. By End User

11.1.2.4. By Raw Material

11.1.2.5.

By Country

11.1.2.5.1.

China

11.1.2.5.2.

Japan

11.1.2.5.3.

India

11.1.2.5.4.

Australia

11.1.2.5.5.

South Korea

11.1.2.5.6. Rest

of Asia Pacific

12.

Middle East & Africa Epoxy Curing Agents Market:

Estimates & Forecast Trend Analysis

12.1. Middle

East & Africa Epoxy Curing Agents Market Assessments & Key Findings

12.1.1.

Middle East & Africa Epoxy

Curing Agents Market Introduction

12.1.2.

Middle East & Africa Epoxy

Curing Agents Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1. By Curing Agent

12.1.2.2. By Application

12.1.2.3. By End User

12.1.2.4. By Raw Material

12.1.2.5.

By Country

12.1.2.5.1.

UAE

12.1.2.5.2.

Saudi Arabia

12.1.2.5.3.

South Africa

12.1.2.5.4. Rest of MEA

13.

Latin America Epoxy

Curing Agents Market: Estimates &

Forecast Trend Analysis

13.1. Latin

America Event Industry Assessments & Key Findings

13.1.1.

Latin America Epoxy Curing Agents Market Introduction

13.1.2.

Latin America Epoxy Curing Agents Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

13.1.2.1. By Curing Agent

13.1.2.2. By Application

13.1.2.3. By End User

13.1.2.4. By Raw Material

13.1.2.5.

By Country

13.1.2.5.1.

Brazil

13.1.2.5.2.

Mexico

13.1.2.5.3.

Argentina

13.1.2.5.4. Rest of LATAM

14.

Country Wise Market: Introduction

15. Competition

Landscape

15.1. Global

Epoxy Curing Agents Market Product Mapping

15.2. Global

Epoxy Curing Agents Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

15.3. Global

Epoxy Curing Agents Market Tier Structure Analysis

15.4. Global

Epoxy Curing Agents Market Concentration & Company Market Shares (%)

Analysis, 2024

16. Company

Profiles

16.1.

Huntsman Corporation

16.1.1.

Company Overview & Key Stats

16.1.2.

Financial Performance & KPIs

16.1.3.

Product Portfolio

16.1.4.

SWOT Analysis

16.1.5.

Business Strategy & Recent Developments

*

Similar details would be provided for all the players mentioned below

16.2.

Hexion Inc.

16.3.

BASF SE

16.4.

Evonik Industries AG

16.5.

Olin Corporation

16.6.

Cardolite Corporation

16.7.

Atul Ltd.

16.8.

Aditya Birla Chemicals

16.9.

KUKDO Chemical Co., Ltd.

16.10.

Mitsubishi Chemical Corporation

16.11.

Gabriel Performance Products

16.12.

Air Products and Chemicals, Inc.

16.13.

DIC Corporation

16.14.

Shandong Deyuan Epoxy Resin Co., Ltd.

16.15.

Toray Industries, Inc.

16.16.

Kumho P&B Chemicals Inc.

16.17.

Momentive Specialty Chemicals, Inc.

16.18.

Grasim Industries Ltd.

16.19.

RAMPF Group

16.20.

Other Prominent Players

17.

Research

Methodology

17.1. External

Transportations / Databases

17.2. Internal

Proprietary Database

17.3. Primary

Research

17.4. Secondary

Research

17.5. Assumptions

17.6. Limitations

17.7. Report

FAQs

18.

Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables