Erectile Dysfunction Drugs Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Drug Type (PDE5 Inhibitors, Hormonal Therapy, Others); By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies); By Route of Administration (Oral, Topical, Injectables); and Geography

2025-11-04

Healthcare

Swetal (Research Analyst)

Description

Erectile Dysfunction Drugs Market Overview

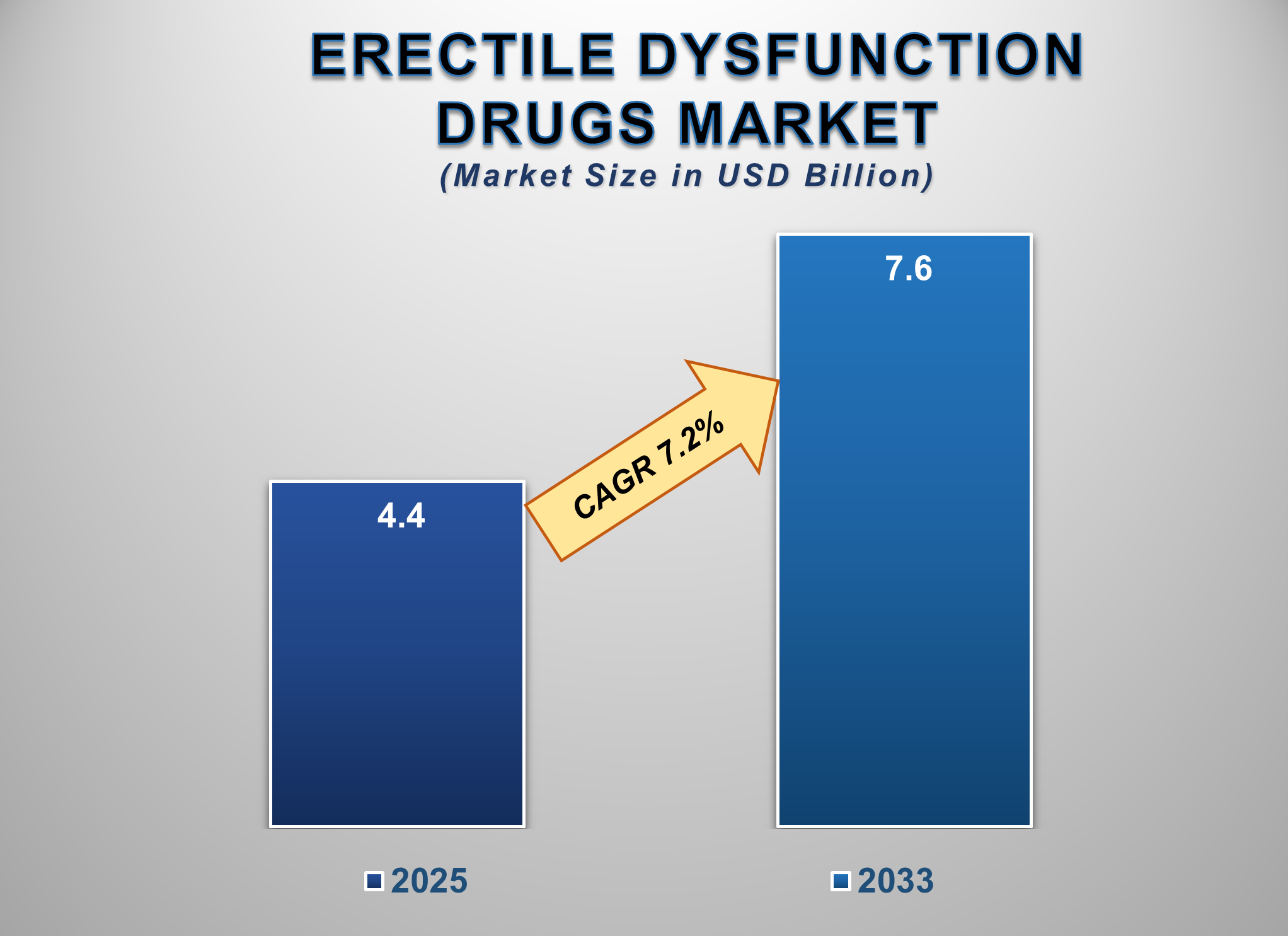

The Erectile Dysfunction Drugs market size is projected to witness steady growth from 2025 to 2033, driven by the rising global prevalence of erectile dysfunction (ED), growing awareness and destigmatization of men's health issues, and the introduction of novel therapeutic formulations. Valued at approximately USD 4.4 billion in 2025, the market is expected to reach USD 7.6 billion by 2033, reflecting a compound annual growth rate (CAGR) of 7.2% over the forecast period.

The erectile dysfunction drugs

market is a well-established yet evolving sector within the pharmaceutical

industry, primarily dominated by Phosphodiesterase type 5 (PDE5) inhibitors.

The market is experiencing a paradigm shift from being solely focused on

treatment to encompassing overall male sexual wellness and preventive health.

The high efficacy and strong brand recognition of drugs like sildenafil

(Viagra), tadalafil (Cialis), and vardenafil (Levitra) continue to form the

bedrock of market revenue. A key growth driver is the expanding patient pool,

which is strongly correlated with the increasing incidence of underlying

conditions such as diabetes, cardiovascular diseases, and obesity, all of which

are major risk factors for ED. The growing aging male population globally,

which is more susceptible to ED, further propels market expansion.

The market is also benefiting

from the increasing ease of access to these medications through online

pharmacies and telemedicine platforms, which offer discretion and convenience.

Furthermore, ongoing research and development are focused on creating faster-acting

formulations, new drug combinations, and therapies for sub-populations

non-responsive to current treatments. The impending patent expiries of major

brands are paving the way for robust generic competition, which is expected to

increase affordability and market penetration, particularly in cost-sensitive

regions. North America remains the dominant market due to high awareness and

healthcare spending, while the Asia-Pacific region is anticipated to exhibit

the fastest growth, fueled by a large untapped patient base and improving

healthcare access.

Erectile Dysfunction

Drugs Market Drivers and Opportunities

Rising Prevalence of Erectile Dysfunction and Associated

Comorbidities

The increasing global incidence of erectile

dysfunction is the fundamental driver for this market. This rise is

intrinsically linked to the growing prevalence of chronic conditions such as

diabetes, hypertension, and hormonal imbalances, which can impair vascular and

neurological functions critical for erectile performance. Furthermore,

lifestyle factors, including smoking, alcohol consumption, and psychological stress, contribute significantly to the condition. As global

health burdens from these risk factors increase, the patient pool for ED

expands correspondingly. Growing awareness campaigns and a gradual reduction in

the social stigma associated with ED are encouraging more men to seek diagnosis

and treatment, thereby driving demand for pharmaceutical interventions.

The United States is facing a significant and

growing challenge with erectile dysfunction, a condition that affects a

substantial portion of the male population and has broad implications for

quality of life and mental health. Studies estimate that ED affects

approximately 30 million men in the U.S., with prevalence increasing markedly

with age. However, it is not an inevitable consequence of aging alone; it is

often a barometer for overall cardiovascular and metabolic health. The economic

impact is considerable, encompassing direct costs of medications and doctor

visits, as well as indirect costs related to relationship stress and reduced

psychological well-being.

This high prevalence is driven by a confluence of

powerful demographic and health factors. Primarily, the aging of the population

is a key driver, as the risk of ED rises significantly in men over 40.

Concurrently, the high and rising rates of obesity, metabolic syndrome, and type 2

diabetes are major contributors, as these conditions damage blood vessels and

nerves. Furthermore, the prevalence of cardiovascular disease, a leading cause

of ED, remains high. Modern sedentary lifestyles and psychological factors like

stress and anxiety also play a significant role. Increased public health focus

on men's health is leading to more open discussions and higher diagnosis rates,

further illuminating the scale of this issue.

Shift Towards Telemedicine and Online Pharmacies

The overarching trend in healthcare towards

digitalization and convenience is a significant driver for the ED drugs market.

The rise of telemedicine platforms and direct-to-consumer online pharmacies has

dramatically improved access to treatment. These channels offer discreet

consultations, easy prescription renewals, and home delivery, which helps

overcome barriers related to embarrassment and privacy concerns that often

prevent men from seeking help. This shift is expanding the market reach beyond

traditional brick-and-mortar pharmacies, capturing a broader demographic of

patients who prefer the convenience and anonymity of digital health solutions.

Opportunity for the Erectile Dysfunction Drugs Market

Expansion

in Emerging Markets and Development of Next-Generation Therapies

A significant opportunity lies in the vast

untapped potential of emerging economies in the Asia-Pacific, Latin America,

and the Middle East. Rising disposable incomes, improving healthcare

infrastructure, and growing awareness of men's health issues in these regions

are creating new growth frontiers. Companies that can implement effective educational

campaigns and offer affordable generic versions or competitively priced branded

drugs are poised to capture a substantial market share. Furthermore, a major opportunity

exists in the development of next-generation therapies, including new molecular

entities beyond PDE5 inhibitors, faster-dissolving oral formulations, and

effective topical creams or gels that could offer a non-invasive alternative to

pills and injections, thereby appealing to a wider patient base.

Erectile Dysfunction

Drugs Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 4.4 Billion |

|

Market Forecast in 2033 |

USD 7.6 Billion |

|

CAGR % 2025-2033 |

7.2% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, Company Share, Company Heatmap, Company

Production, Service Type, Growth Factors, and more |

|

Segments Covered |

●

By Drug Type ●

By Application ●

By End-user |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Netherlands 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19)

Egypt 20) South Africa |

Erectile Dysfunction

Drugs Market Report Segmentation Analysis

The global Erectile Dysfunction

Drugs Market industry analysis is segmented by Drug Type, by Application, and

by End-user.

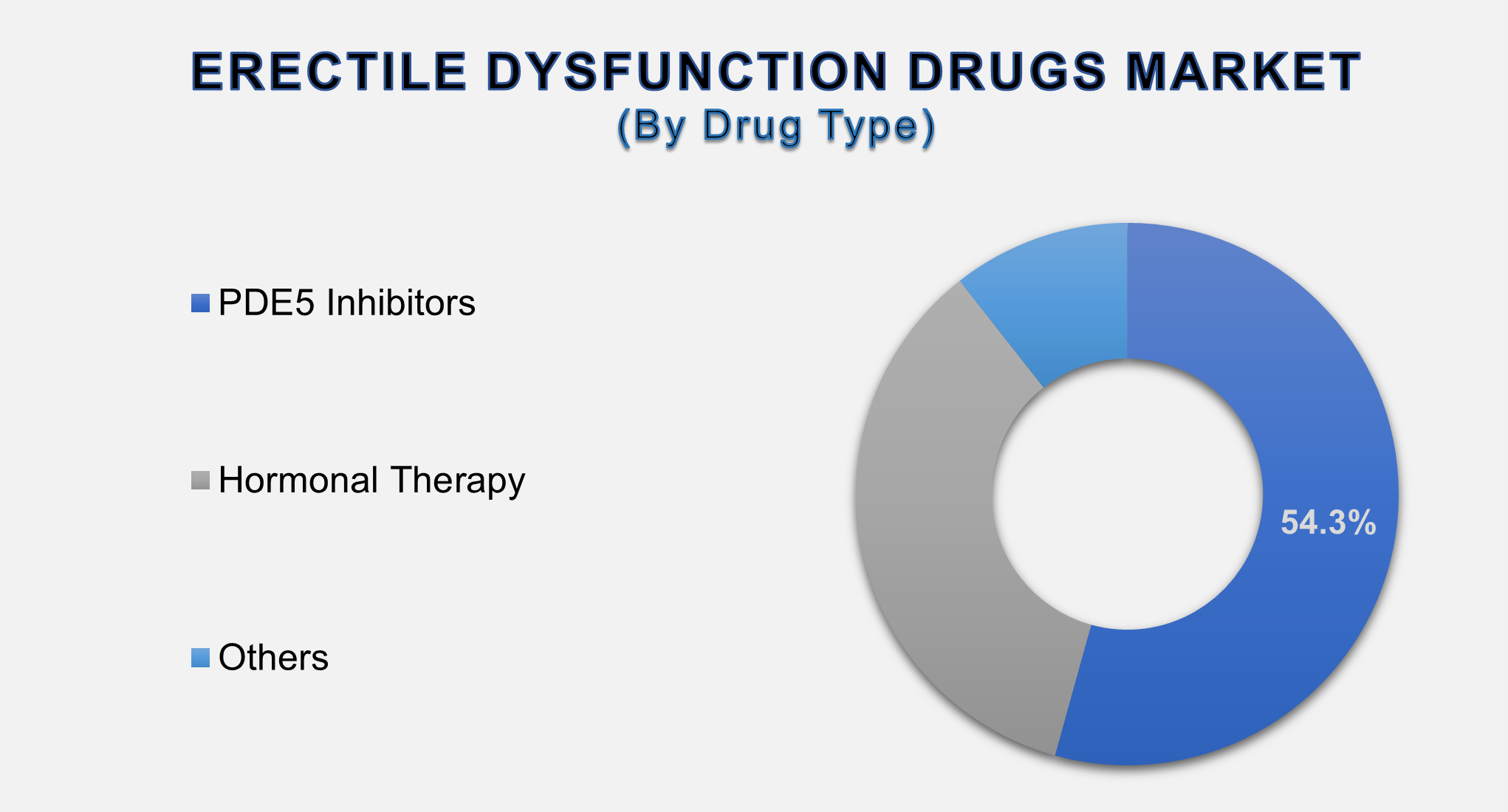

The Dominance of the PDE5 Inhibitors Drug Type Segment

The PDE5 inhibitors segment is the undisputed

revenue leader and cornerstone of the erectile dysfunction drugs market. This

dominance is secured by their position as the first-line pharmacological

therapy for ED, backed by decades of proven efficacy, safety, and a vast body

of clinical evidence. Drugs like sildenafil, tadalafil, and vardenafil have

achieved immense brand recognition and patient trust, making them the default

choice for both prescribers and patients. Their mechanism of action, which enhances

blood flow to the penis, is effective for a broad majority of ED cases. The

availability of both branded and a wide array of generic versions ensures

competitive pricing and widespread accessibility, cementing the segment's

continued dominance in terms of prescription volume and overall market share.

The Leadership of the Retail Pharmacies Distribution Channel

The Retail Pharmacies distribution channel is the

largest and most traditional point of sale for ED drugs. This dominance is a

direct result of convenience, immediate product availability, and the

established practice of patients obtaining prescribed medications from their

local pharmacy. Retail pharmacies offer the advantage of direct interaction

with pharmacists for immediate consultation, which is valued by many patients.

Furthermore, the extensive networks of retail pharmacy chains, along with their

partnerships with insurance providers and pharmacy benefit managers (PBMs),

make them the most accessible and reimbursed channel for a large portion of the

population. While online pharmacies are growing rapidly, retail pharmacies

remain the primary distribution channel due to their deep market penetration

and integration within the standard healthcare workflow.

The Oral Route of Administration commands a major share of

the market

The Oral Route of Administration commands a

dominant market share because it represents the most patient-friendly,

non-invasive, and convenient method of drug delivery for ED. Oral PDE5

inhibitors are easy to administer, do not require any medical training for use,

and are highly portable and discreet. The high efficacy and predictable onset

of action of oral tablets align perfectly with patient preferences for

simplicity and normalcy in their treatment regimen. Compared to alternatives

like intracavernosal injections or topical creams, which can be perceived as

intimidating, messy, or less reliable, oral pills offer a superior user

experience. This overwhelming patient and prescriber preference for the oral

route ensures its continued and commanding leadership in the market.

The following segments are part of an in-depth analysis of the global

Erectile Dysfunction Drugs Market:

|

Market Segments |

|

|

By Drug Type |

●

PDE5 Inhibitors ●

Hormonal Therapy ●

Others |

|

By Route of Administration |

●

Oral ●

Topical ●

Injectables |

|

By Distribution Channel |

●

Hospital Pharmacies ●

Retail Pharmacies ●

Online Pharmacies |

Erectile Dysfunction

Drugs Market Share Analysis by Region

The North America region is expected to

dominate the Global Erectile Dysfunction Drugs Market during the forecast

period.

North America is anticipated to be the

leader in the global Erectile Dysfunction Drugs Market. This dominance is

anchored by the region's high healthcare expenditure, early and widespread

adoption of leading branded pharmaceuticals, and a well-established

reimbursement structure that covers prescription medications for ED. The

presence of a large patient population, high awareness levels driven by

direct-to-consumer advertising, and a robust healthcare infrastructure in the

U.S. and Canada create a highly conducive environment for market growth.

Furthermore, the region is a hub for major pharmaceutical companies and

significant R&D activities, securing North America's leading position.

Erectile Dysfunction (ED) represents a

significant and widespread public health challenge in the United States,

affecting a substantial portion of the male population. Current estimates

suggest that ED impacts approximately 30 million American men, with its

prevalence strongly correlated with age. While the condition is relatively

uncommon in younger men, its incidence rises markedly, affecting about 40% of

men by age 40 and nearly 70% of those by age 70. However, ED is not an

inevitable consequence of aging alone; it often serves as a critical barometer

for underlying health issues.

The high prevalence is driven by a

confluence of powerful factors, primarily the increasing rates of comorbidities

such as cardiovascular disease, diabetes, hypertension, and metabolic syndrome,

all of which can impair vascular and neurological functions essential for

erectile performance. Furthermore, modern lifestyle factors, including obesity,

sedentary habits, smoking, and psychological stressors like anxiety and

depression, contribute significantly to the

problem. The economic and quality-of-life burden is considerable, encompassing

direct medical costs and profound impacts on mental well-being, self-esteem,

and intimate relationships. Increased public health focus and destigmatization

are leading to more open discussions and higher diagnosis rates, further

illuminating the true scale of this condition.

Global Erectile

Dysfunction Drugs Market Recent Developments News:

- In January 2025, Viatris Inc. launched an

authorized generic version of Cialis (tadalafil) in the U.S. market,

increasing affordable access to the long-acting PDE5 inhibitor.

- In February 2025, Pfizer Inc. entered a strategic

partnership with a digital health company to integrate its ED medication,

Viagra (sildenafil), with a companion app for tracking treatment outcomes

and patient support.

- In March 2025, Metuchen Pharmaceuticals LLC

received FDA approval for a novel sublingual film formulation of a PDE5

inhibitor, aiming to provide a faster onset of action compared to

traditional oral tablets.

- In April 2025, Dare Bioscience, Inc. announced

positive Phase IIb results for its topical intravaginal gel for female

sexual arousal disorder, highlighting crossover

interest in adjacent sexual health markets that could influence the ED

landscape.

The Global Erectile

Dysfunction Drugs Market is dominated by a few large companies, such as

●

Pfizer Inc.

●

Eli Lilly and Company

●

Bayer AG

●

Viatris Inc.

●

Teva Pharmaceutical

Industries Ltd.

●

Aurobindo Pharma Ltd.

●

Sun Pharmaceutical

Industries Ltd.

●

Cipla Inc.

●

AbbVie Inc.

●

Endo International plc

●

Metuchen

Pharmaceuticals LLC

●

Dare Bioscience, Inc.

●

Petros

Pharmaceuticals, Inc.

●

Cumberland

Pharmaceuticals Inc.

●

Futura Medical plc

●

Other Prominent

Players

FAQs

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global Erectile

Dysfunction Drugs Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Erectile Dysfunction Drugs Market Scope and Market Estimation

1.2.1.Global Erectile

Dysfunction Drugs Market Overall Market Size (US$ Bn), Market CAGR (%), Market

forecast (2025 - 2033)

1.2.2.Global Erectile

Dysfunction Drugs Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Drug Type of Global Erectile

Dysfunction Drugs Market

1.3.2.Route of Administration of

Global Erectile Dysfunction Drugs Market

1.3.3.Distribution Channel of

Global Erectile Dysfunction Drugs Market

1.3.4.Region of Global Erectile

Dysfunction Drugs Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Erectile Dysfunction Drugs Market

2.8.

Number

of Spinal Surgery Performed per year, by key countries

2.9.

Key

Products/Brand Analysis

2.10.

Pricing

Analysis

2.11.

Porter’s

Five Forces Analysis

2.12.

PEST

Analysis

2.13.

Key

Regulation

3. Global

Erectile Dysfunction Drugs Market

Estimates & Historical Trend Analysis (2020 - 2024)

4.

Global Erectile

Dysfunction Drugs Market Estimates

& Forecast Trend Analysis, by Drug Type

4.1.

Global

Erectile Dysfunction Drugs Market Revenue (US$ Bn) Estimates and Forecasts, by Drug

Type, 2020 - 2033

4.1.1.PDE5 Inhibitors

4.1.2.Hormonal Therapy

4.1.3.Others

5.

Global Erectile

Dysfunction Drugs Market Estimates

& Forecast Trend Analysis, by Route of Administration

5.1.

Global

Erectile Dysfunction Drugs Market Revenue (US$ Bn) Estimates and Forecasts, by Route

of Administration, 2020 - 2033

5.1.1.Oral

5.1.2.Topical

5.1.3.Injectables

6.

Global Erectile

Dysfunction Drugs Market Estimates

& Forecast Trend Analysis, by Distribution Channel

6.1.

Global

Erectile Dysfunction Drugs Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution

Channel, 2020 - 2033

6.1.1.Hospital Pharmacies

6.1.2.Retail Pharmacies

6.1.3.Online Pharmacies

7. Global

Erectile Dysfunction Drugs Market

Estimates & Forecast Trend Analysis, by region

1.1.

Global

Erectile Dysfunction Drugs Market Revenue (US$ Bn) Estimates and Forecasts, by

region, 2020 - 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East & Africa

1.1.5.Latin America

8. North America Erectile

Dysfunction Drugs Market: Estimates

& Forecast Trend Analysis

8.1. North America Erectile

Dysfunction Drugs Market Assessments & Key Findings

8.1.1.North America Erectile

Dysfunction Drugs Market Introduction

8.1.2.North America Erectile

Dysfunction Drugs Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Drug Type

8.1.2.2. By Route of

Administration

8.1.2.3. By Distribution

Channel

8.1.2.4.

By

Country

8.1.2.4.1.

The

U.S.

8.1.2.4.2.

Canada

9. Europe Erectile

Dysfunction Drugs Market: Estimates

& Forecast Trend Analysis

9.1.

Europe

Erectile Dysfunction Drugs Market Assessments & Key Findings

9.1.1.Europe Erectile

Dysfunction Drugs Market Introduction

9.1.2.Europe Erectile

Dysfunction Drugs Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Drug Type

9.1.2.2. By Route of

Administration

9.1.2.3. By Distribution

Channel

9.1.2.4.

By

Country

9.1.2.4.1. Germany

9.1.2.4.2. Italy

9.1.2.4.3. U.K.

9.1.2.4.4. France

9.1.2.4.5. Spain

9.1.2.4.6. Netherland

9.1.2.4.7.

Rest of Europe

10. Asia Pacific Erectile

Dysfunction Drugs Market: Estimates

& Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Erectile Dysfunction Drugs Market Introduction

10.1.2.

Asia

Pacific Erectile Dysfunction Drugs Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1. By Drug Type

10.1.2.2. By Route of

Administration

10.1.2.3. By Distribution

Channel

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6.

Rest

of Asia Pacific

11. Middle East & Africa Erectile

Dysfunction Drugs Market: Estimates

& Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Erectile Dysfunction Drugs Market

Introduction

11.1.2.

Middle East & Africa Erectile Dysfunction Drugs Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Drug Type

11.1.2.2. By Route of

Administration

11.1.2.3. By Distribution

Channel

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4.

Rest of MEA

12. Latin America

Erectile Dysfunction Drugs Market:

Estimates & Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Erectile Dysfunction Drugs Market Introduction

12.1.2.

Latin

America Erectile Dysfunction Drugs Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

12.1.2.1. By Drug Type

12.1.2.2. By Route of

Administration

12.1.2.3. By Distribution

Channel

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Mexico

12.1.2.4.3. Argentina

12.1.2.4.4.

Rest of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Erectile Dysfunction Drugs Market Product Mapping

14.2.

Global

Erectile Dysfunction Drugs Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3.

Global

Erectile Dysfunction Drugs Market Tier Structure Analysis

14.4.

Global

Erectile Dysfunction Drugs Market Concentration & Company Market Shares (%)

Analysis, 2024

15.

Company

Profiles

15.1. Pfizer Inc.

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all

the players mentioned below

15.2. Eli Lilly and

Company

15.3. Bayer AG

15.4. Viatris Inc.

15.5. Teva

Pharmaceutical Industries Ltd.

15.6. Apricus

Biosciences, Inc.

15.7. Meda

Pharmaceuticals (a Viatris Company)

15.8. Cristalia

Produtos Químicos Farmacêuticos Ltda.

15.9. Dong-A ST

Co., Ltd.

15.10. Seoul Pharma

Co., Ltd.

15.11. Other

Prominent Players

16. Research

Methodology

16.1.

External

Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables