Events Industry Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; Type (Music Concert, Festivals, Sports, Exhibitions and Conferences, Corporate Events and Seminar, and Others), Revenue Source (Ticket Sale, Sponsorship, Food and Beverage, Advertising, Merchandise Sales, Membership Fees, Participation Fees, Media and Licensing Revenue, and Others), Organizer (Corporate, Sports, Education, Entertainment, and Others); Age Group (Below 20 Years, 21-40 Years, and Above 40 Years); Origin of Attendees (National, Continental, and Transcontinental); Event Location (Tier 1 Cities, Tier 2 Cities, and Tier 3 Cities); and Geography

2026-02-05

Consumer Products

Jaya Bundele (Research Analyst)

Description

Events

Industry Overview

The global events

industry is experiencing strong growth, driven by rapid digital transformation and

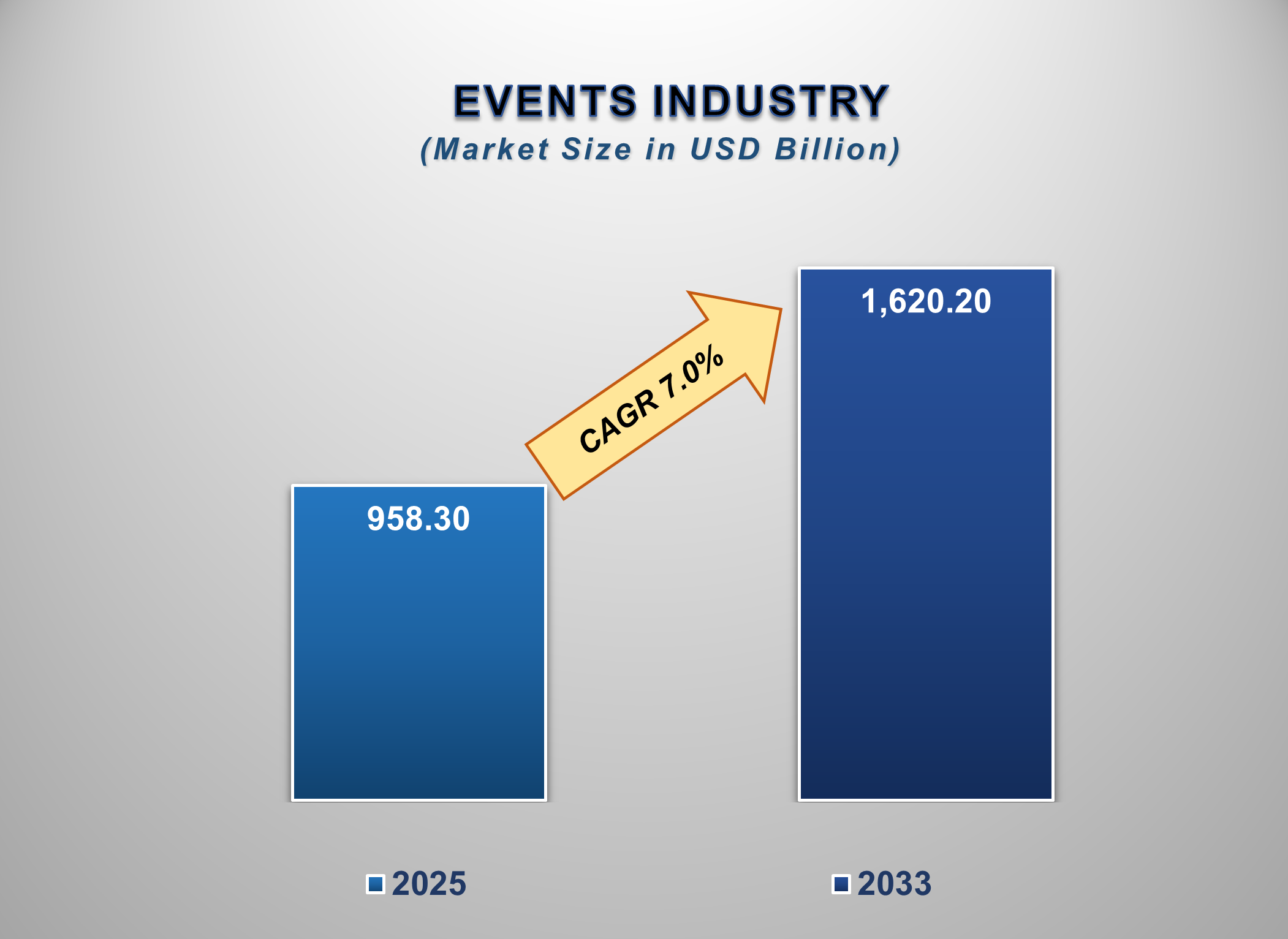

advancements in technology. Valued at USD 958.30 billion in 2025, the

market is projected to reach USD 1,620.20 billion by 2033, growing at a CAGR of

7.0% during the forecast period.

The planning,

organization, execution, and management of a broad range of events, including

corporate meetings, conferences, exhibitions, trade shows, concerts, festivals,

sporting events, weddings, and social gatherings, are all included in the

dynamic and diverse global events industry. Event planners, venue operators,

logistics companies, audiovisual firms, catering services, and digital event

technology platforms are among the many service providers that the sector

combines. The events industry has evolved significantly over the past decade,

moving from traditional in-person forms to hybrid and virtual models that make

use of modern digital technologies.

Following the

disruption caused by the COVID-19 pandemic, the industry has witnessed a strong

recovery. Growing demand for in-person contacts, brand experiences, and

large-scale events sped up industry expansion when limitations loosened. Events

are becoming more and more recognized by organizations as essential instruments

for revenue development, staff cooperation, customer engagement, and brand

growth. Growing corporate marketing and promotion expenditures, an increase in

business travel, and increased consumer spending on live events and

entertainment all contribute to the industry.

The global events

industry is projected to be worth several hundred billion dollars in 2025 and

is projected to develop at a robust compound annual growth rate through 2033.

Technology integration, corporate globalization, rising sponsorship

expenditures, and the spread of experiential marketing techniques across

sectors like technology, healthcare, education, sports, and entertainment are

the main drivers of growth.

Physical venues are

no longer the only option for the events sector. With their scalability, global

reach, cost efficiency, and data-driven insights, virtual and hybrid events

have become a crucial component of the market. Artificial intelligence (AI),

augmented reality (AR), virtual reality (VR), live streaming, and event

management software platforms are examples of innovative technologies that are

changing the way events are planned and executed. This allows event planners to

improve attendee engagement and more accurately assess return on investment.

Events

Industry Drivers and Opportunities

Growing Demand

for Corporate Events and Experiential Marketing

The growing need for corporate events and

experiential marketing campaigns is one of the main factors propelling

expansion in the global events sector. Companies across industries are making

significant investments in conferences, product launches, trade fairs,

exhibitions, and internal meetings in order to improve employee engagement,

build client relationships, and promote brand presence. Organizations see

events as high-impact venues to convey brand values, promote innovation, and

produce memorable consumer experiences in an increasingly competitive business

climate. Experiential marketing has become a major strategic concern,

especially in consumer-oriented industries like fast-moving consumer goods,

retail, automotive, and technology. Budgets for immersive, interactive events

that enable direct interaction with target audiences are replacing traditional

advertising. Experiential roadshows, pop-up events, and live brand activations

are becoming more popular because they can foster strong emotional bonds and

enduring brand loyalty. This trend is expected to sustain the high demand for

expert event management services around the world.

Expansion of Business

Travel and MICE Tourism

Another important aspect driving the events

industry is the rapid expansion of Meetings, Incentives, Conferences, and

Exhibitions (MICE) tourism. By making investments in large convention halls,

exhibition spaces, lodging, and transportation infrastructure, governments and

tourism boards around the globe are aggressively marketing their locations as

international event hubs. Major cities in Europe, the Middle East, and the Asia-Pacific

are establishing themselves as the go-to locations for international

exhibitions and conferences. International conferences and trade exhibitions

are becoming more frequent due to growing globalization and cross-border

economic activities. As businesses use travel-based incentives to boost

employee motivation and improve partner relationships, incentive travel

programs are likewise becoming more and more popular. The general growth

trajectory of the events industry is being reinforced by these trends, which

are producing significant revenue for venue operators, hospitality providers,

event organizers, and local economies.

Digital Transformation

and Technology Adoption

The events industry is changing as a result of

technological advancements that make planning, execution, and engagement more

effective. These days, end-to-end solutions for registration, ticketing,

attendee analytics, marketing automation, and post-event reporting are

available on event management software platforms. Artificial intelligence is

being utilized to enhance event scheduling, suggest networking possibilities,

and customize attendee experiences. By eliminating geographical restrictions

and lowering travel and venue rental expenses, the use of virtual and hybrid

event formats has opened up new growth prospects. Organizers looking to enhance

reach while preserving physical involvement are especially drawn to hybrid

events, which combine in-person and virtual components. Live streaming, virtual

exhibition booths, AR/VR experiences, and interactive polling tools are

examples of technologies that are becoming commonplace and opening up new

revenue sources for both technology companies and event planners.

Events Industry Scope

|

Report Attributes |

Description |

|

Market Size in

2025 |

USD 958.30

Billion |

|

Market Forecast

in 2033 |

USD 1,620.20

Billion |

|

CAGR % 2025-2033 |

7.0% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Global events

industry market size and forecast analysis, event type and service-based

revenue assessment, corporate, MICE, and entertainment event insights,

virtual, hybrid and in-person event coverage, regional and country-level

market evaluation, competitive landscape and market share analysis,

sponsorship, ticketing and revenue stream assessment, event technology and

digital platform adoption trends, experiential marketing and brand activation

analysis, sustainability and green event practices, growth drivers,

challenges and opportunity mapping, strategic insights for event organizers

and industry stakeholders |

|

Segments Covered |

●

By Type ●

By

Revenue Source ●

By

Organizer ●

By Age

Group ●

By Origin

of Attendees ●

By Event

Location |

|

Regional Scope |

●

North

America ●

Europe ●

APAC ●

Latin

America ●

Middle

East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada

3)

U.K. 4)

Germany

5)

France

6)

Italy 7)

Spain 8)

Switzerland

9)

China

10)

India

11)

Japan 12)

South

Korea 13)

Australia 14)

Mexico

15)

Brazil

16)

Argentina

17)

Saudi

Arabia 18)

UAE 19)

South

Africa |

Events Industry

Report Segmentation Analysis

The global events

industry analysis is segmented by Type, Revenue Source, Organizer, Age Group,

Origin of Attendees, Event Location, and Region.

The corporate

events and seminars segment dominated the market in 2025 and is projected to

grow at the highest CAGR during the forecast period.

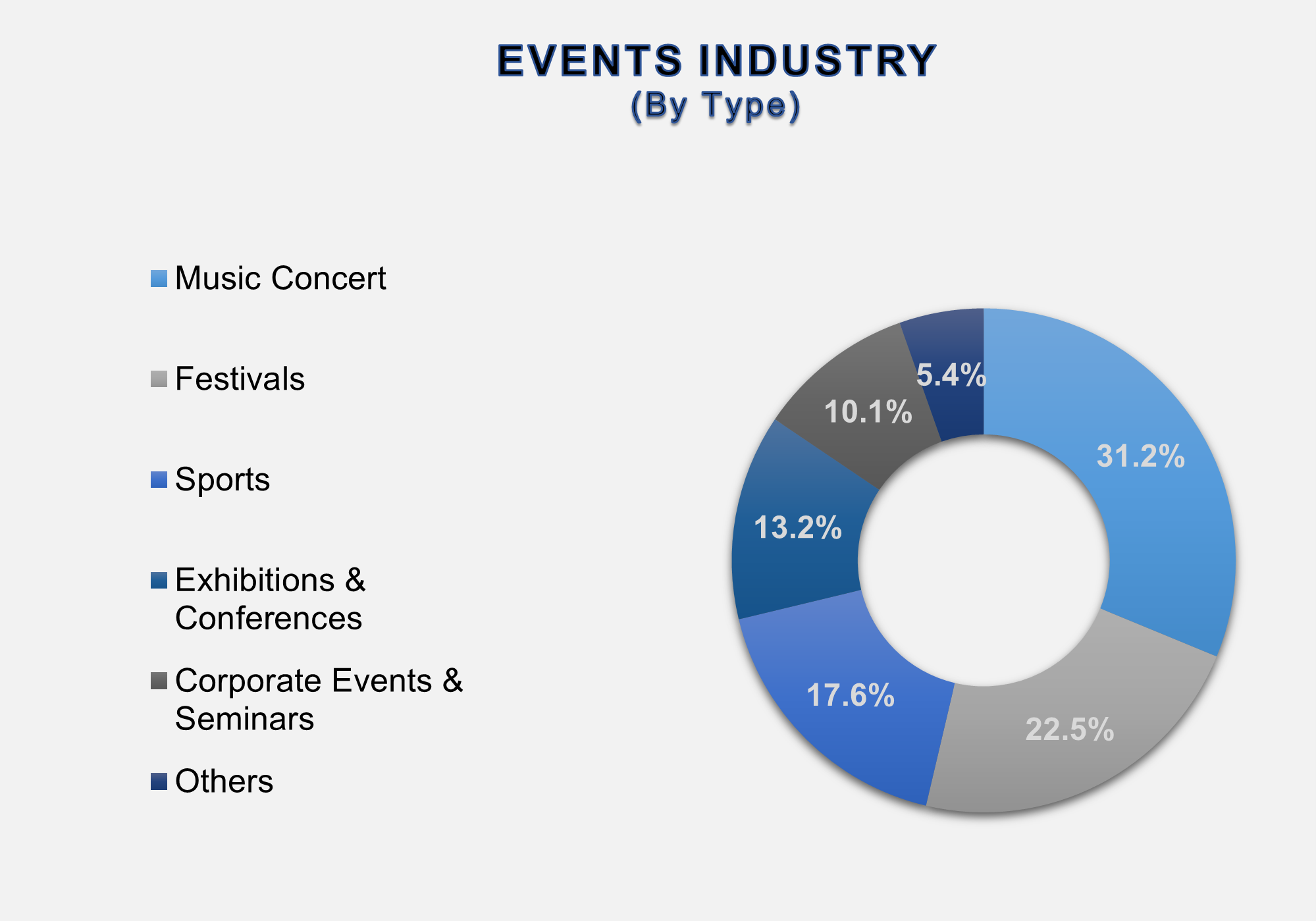

By Type, the Events

Industry is segmented into music concerts, festivals, sports, exhibitions &

conferences, corporate events & seminars, and others. Corporate events and

seminars account for the largest market share in the events industry due to

high spending by businesses and sponsors. Conferences, meetings, product

launches, exhibitions, and incentive programs are examples of corporate events

that encourage business networking, increase stakeholder engagement, boost

brand visibility, and advance marketing, training, and sales goals globally.

However, sports events are expected to grow at a higher CAGR during the

forecast period. Professional and amateur competitions, tournaments, leagues,

and championships are all included in sports events. These events attract huge

crowds, make money from ticket sales and sponsorships, improve fan interaction,

and advance travel, media attention, and community development on a global

scale.

Sponsorship holds

the highest share of the Revenue Source Segment over the forecast period

Based on revenue source, the market is bifurcated into Ticket Sales,

Sponsorship, Food and Beverage, Advertising, Merchandise Sales, Membership

Fees, Participation Fees, Media and Licensing Revenue, and Others. The

sponsorship segment accounts for the largest share of the market. The term

"sponsorship" describes strategic alliances in which companies

provide material or financial assistance for events in return for brand

association, audience participation, and marketing exposure. It is essential

for generating income since it allows event planners to improve event size,

quality, and reach while providing sponsors with quantifiable promotional

value.

The entertainment segment will probably dominate the market during the forecast

period

In terms of organizers,

the events industry is segmented into Corporate, Sports, Education,

Entertainment, and Others. The entertainment segment holds the largest share in

the events industry. Concerts, music festivals, cultural performances, and live

performances are examples of entertainment events that provide immersive

experiences, draw sizable crowds, make money from ticket sales and

sponsorships, and promote travel, media attention, and cultural involvement on

a worldwide scale.

21-40 Years hold the highest share of the Age Group

Segment over the forecast period

Based on age group,

the market is bifurcated into below 20 years, 21 to 40 years, and above 40 years.

The 21–40 years age group holds the highest share in the market. A significant

audience segment for the events industry, the 21–40 age group is distinguished

by high levels of social engagement, digital connectivity, and a strong

preference for brand-driven experiences, live entertainment, networking events,

and experiential activities. These traits are strengthened by rising disposable

incomes and active participation in corporate, cultural, and sporting events.

The national segment will probably dominate the market during the forecast

period

In terms of the origin

of attendees, the events industry is segmented into National, Continental, and

Transcontinental. The national segment holds the largest share in the events

industry. The geographic and cultural background of guests, both local and

foreign, refers to the geographic and cultural background of attendees. In

addition to having a significant impact on tourism, cross-border networking,

and global audience involvement, this element also affects event scalability,

content modification, language needs, marketing methods, and revenue potential.

Tier 1 Cities hold the highest share of the Event

Location Segment over the forecast period

Based on event

location, the market is bifurcated into Tier 1 Cities, Tier 2 Cities, and Tier

3 Cities. Tier 1 cities are significant urban centers with sophisticated

infrastructure, dense populations, and robust economies. Large-scale corporate,

entertainment, and international events are hosted by the events industry

because of their excellent venues, connections, hospitality capacity, trained

staff, and greater potential for sponsorship and audience spending.

The following

segments are part of an in-depth analysis of the global events industry:

|

Market Segments |

|

|

By

Type |

●

Music

Concert ●

Festivals ●

Sports ●

Exhibitions

and Conferences ●

Corporate

Events and Seminars ●

Others |

|

By

Revenue Source |

●

Ticket

Sale ●

Sponsorship ●

Food and

Beverage ●

Advertising ●

Merchandise

Sales ●

Membership

Fees ●

Participation

Fees ●

Media and

Licensing Revenue ●

Others |

|

By

Organizer |

●

Corporate ●

Sports ●

Education ●

Entertainment ●

Others |

|

By Age

Group |

●

Below 20

Years ●

21 to 40

Years ●

Above 40

Years |

|

By

Origin of Attendees |

●

National ●

Continental ●

Transcontinental |

|

By

Event Location |

●

Tier 1

Cities ●

Tier 2

Cities ●

Tier 3

Cities |

Events Industry Share Analysis by Region

The Europe region

is projected to hold the largest share of the global events industry over the

forecast period.

Europe leads the

global events industry and is also expected to be the fastest-growing region

throughout the forecast period. The Europe region is a mature and

well-established market within the global events industry with a robust

corporate presence, innovative facilities, and a diverse cultural backdrop.

Every year, a large number of international conferences, exhibits, trade shows,

cultural festivals, and athletic events are held in nations including Germany,

the UK, France, Italy, and Spain. Europe leads the world in the MICE industry

due to corporate travel, international trade, and government backing for

tourism and event promotion. Additionally, the region shows a high uptake of

digital ticketing, hybrid event forms, and sustainable practices. The quality,

scope, and international appeal of events throughout the area are further

improved by Europe's rich sponsorship economy, varied cultural legacy, and

legislative emphasis on environmental and safety requirements.

Global Events Industry Recent Developments

News:

●

In December

2025, Bending Spoons agreed to acquire Eventbrite for approximately $500

million, aiming to revitalize the ticketing and events platform under its

technology portfolio.

●

In June 2025,

Zoho announced a strategic partnership with Whova to integrate CRM with

event-management solutions, enhancing attendee data insights and engagement

tools.

●

In May 2025,

Cvent acquired PlanHero to strengthen its event-planning workflow and

hybrid-event capabilities, enhancing its software portfolio for global event

management.

●

In January

2025, DRPG Group accelerated its North American expansion by acquiring The

Special Event Company and UK agency OWB, broadening creative production

capabilities.

The

Global Events industry is dominated by a few large companies, such as

●

Live Nation

Entertainment

●

Freeman

●

Informa PLC

●

Reed

Exhibitions (Reed Elsevier Group)

●

Messe

Frankfurt

●

Tarsus Group

●

GL Events

●

The

Experiential Marketing Firm (EMF)

●

MCI Group

●

Cvent

●

Hubb

●

Eventbrite

●

ASM Global

●

SMG (now

merged under ASM Global)

●

Lagardère

Sports and Entertainment

●

SXM (Social

Experience Management)

●

BCD Meetings

& Events

●

GES (Global

Experience Specialists)

●

Comexposium

● UBM (now part of Informa Group)

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1.

Global Events Industry Introduction and Market Overview

1.1.

Objectives of the Study

1.2.

Global Events Industry Scope and Market Estimation

1.2.1.Global Events

Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Events

Industry Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market Segmentation

1.3.1.Type of

Global Events industry

1.3.2.Revenue

Source of Global Events Industry

1.3.3.Organizer of

Global Events Industry

1.3.4.Age Group of

Global Events Industry

1.3.5.Origin of

Attendees of Global Events Industry

1.3.6.Event

Location of Global Events Industry

1.3.7.Region of

Global Events Industry

2.

Executive

Summary

2.1.

Demand Side Trends

2.2.

Key Market Trends

2.3.

Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand and Opportunity Assessment

2.5.

Market Dynamics

2.5.1.Drivers

2.5.2.Limitations

2.5.3.Opportunities

2.5.4.Impact

Analysis of Drivers and Restraints

2.6.

Porter’s Five Forces Analysis

2.7.

PEST Analysis

2.8.

Key Regulation

2.9.

Key Developments

2.10. Value

Chain / Ecosystem Analysis

3.

Global

Events Industry Estimates & Historical Trend Analysis (2020 - 2024)

4. Global Events Industry Estimates & Forecast Trend Analysis, by Type

4.1.

Global Events Industry Revenue (US$ Bn) Estimates and Forecasts,

by Type, 2020 - 2033

4.1.1.Music

concerts

4.1.2.Festivals

4.1.3.Sports

4.1.4.Exhibitions

& conferences

4.1.5.Corporate

events & seminars

4.1.6.Others

5. Global Events Industry Estimates & Forecast Trend Analysis, by Revenue Source

5.1.

Global Events Industry Revenue (US$ Bn) Estimates and Forecasts,

by Revenue Source, 2020 - 2033

5.1.1.Ticket

Sale

5.1.2.Sponsorship

5.1.3.Food and

Beverage

5.1.4.Advertising

5.1.5.Merchandise

Sales

5.1.6.Membership

Fees

5.1.7.Participation

Fees

5.1.8.Media and

Licensing Revenue

5.1.9.Others

6. Global Events Industry Estimates & Forecast Trend Analysis, by Organizer

6.1.

Global Events Industry Revenue (US$ Bn) Estimates and Forecasts,

by Organizer, 2020 - 2033

6.1.1.Corporate

6.1.2.Sports

6.1.3.Education

6.1.4.Entertainment

6.1.5.Others

7. Global Events Industry Estimates & Forecast Trend Analysis, by Age Group

7.1.

Global Events Industry Revenue (US$ Bn) Estimates and Forecasts,

by Age Group, 2020 - 2033

7.1.1.Below 20

Years

7.1.2.21-40

Years

7.1.3.Above 40

Years

8. Global Events Industry Estimates & Forecast Trend Analysis, by Origin of Attendee

8.1.

Global Events Industry Revenue (US$ Bn) Estimates and Forecasts,

by Origin of Attendee, 2020 - 2033

8.1.1.National

8.1.2.Continental

8.1.3.Transcontinental

9. Global Events Industry Estimates & Forecast Trend Analysis, by Event Location

9.1.

Global Events Industry Revenue (US$ Bn) Estimates and Forecasts,

by Event Location, 2020 - 2033

9.1.1.Tier 1

Cities

9.1.2.Tier 2

Cities

9.1.3.Tier 3

Cities

10.

Global

Events Industry Estimates & Forecast Trend Analysis, by Region

1.1.

Global Events Industry Revenue (US$ Bn) Estimates and Forecasts,

by Region, 2020 - 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East

& Africa

1.1.5.Latin America

11.

North America Events

Industry: Estimates & Forecast

Trend Analysis

11.1.

North America Events Industry Assessments & Key Findings

11.1.1.

North America Events Industry Introduction

11.1.2.

North America Events Industry Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

11.1.2.1. By Type

11.1.2.2. By Revenue Source

11.1.2.3. By Organizer

11.1.2.4. By Age Group

11.1.2.5. By Origin of Attendees

11.1.2.6. By Event Location

11.1.2.7.

By Country

11.1.2.7.1. The

U.S.

11.1.2.7.2. Canada

12.

Europe Events

Industry: Estimates & Forecast

Trend Analysis

12.1. Europe

Events Industry Assessments & Key Findings

12.1.1.

Europe Events Industry Introduction

12.1.2.

Europe Events Industry Size Estimates and Forecast (US$ Billion) (2020

- 2033)

12.1.2.1. By Type

12.1.2.2. By Revenue Source

12.1.2.3. By Organizer

12.1.2.4. By Age Group

12.1.2.5. By Origin of Attendees

12.1.2.6. By Event Location

12.1.2.7.

By Country

12.1.2.7.1.

Germany

12.1.2.7.2.

Italy

12.1.2.7.3.

U.K.

12.1.2.7.4.

France

12.1.2.7.5.

Spain

12.1.2.7.6.

Russia

12.1.2.7.7. Rest of Europe

13.

Asia Pacific Events

industry: Estimates & Forecast

Trend Analysis

13.1. Asia

Pacific Events Industry Assessments & Key Findings

13.1.1.

Asia Pacific Events Industry Introduction

13.1.2.

Asia Pacific Events Industry Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

13.1.2.1. By Type

13.1.2.2. By Revenue Source

13.1.2.3. By Organizer

13.1.2.4. By Age Group

13.1.2.5. By Origin of Attendees

13.1.2.6. By Event Location

13.1.2.7.

By Country

13.1.2.7.1.

China

13.1.2.7.2.

Japan

13.1.2.7.3.

India

13.1.2.7.4.

Australia

13.1.2.7.5.

South Korea

13.1.2.7.6. Rest

of Asia Pacific

14.

Middle East & Africa Events Industry: Estimates

& Forecast Trend Analysis

14.1. Middle

East & Africa Events Industry Assessments & Key Findings

14.1.1.

Middle East & Africa Events

Industry Introduction

14.1.2.

Middle East & Africa Events

Industry Size Estimates and Forecast (US$ Billion) (2020 - 2033)

14.1.2.1. By Type

14.1.2.2. By Revenue Source

14.1.2.3. By Organizer

14.1.2.4. By Age Group

14.1.2.5. By Origin of Attendees

14.1.2.6. By Event Location

14.1.2.7.

By Country

14.1.2.7.1.

UAE

14.1.2.7.2.

Saudi Arabia

14.1.2.7.3.

South Africa

14.1.2.7.4. Rest of MEA

15.

Latin America Events

Industry: Estimates & Forecast

Trend Analysis

15.1. Latin

America Event Industry Assessments & Key Findings

15.1.1.

Latin America Events Industry Introduction

15.1.2.

Latin America Events Industry Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

15.1.2.1. By Type

15.1.2.2. By Revenue Source

15.1.2.3. By Organizer

15.1.2.4. By Age Group

15.1.2.5. By Origin of Attendees

15.1.2.6. By Event Location

15.1.2.7.

By Country

15.1.2.7.1.

Brazil

15.1.2.7.2.

Mexico

15.1.2.7.3.

Argentina

15.1.2.7.4. Rest of LATAM

16.

Country Wise Market: Introduction

17. Competition

Landscape

17.1. Global

Events Industry Product Mapping

17.2. Global

Events Industry Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

17.3. Global

Events Industry Tier Structure Analysis

17.4. Global

Events Industry Concentration & Company Market Shares (%) Analysis, 2024

18. Company

Profiles

18.1. Live

Nation Entertainment

18.1.1.

Company Overview & Key Stats

18.1.2.

Financial Performance & KPIs

18.1.3.

Product Portfolio

18.1.4.

SWOT Analysis

18.1.5.

Business Strategy & Recent Developments

*

Similar details would be provided for all the players mentioned below

18.2.

Freeman

18.3.

Informa PLC

18.4.

Reed Exhibitions (Reed Elsevier Group)

18.5.

Messe Frankfurt

18.6.

Tarsus Group

18.7.

GL Events

18.8.

The Experiential Marketing Firm (EMF)

18.9.

MCI Group

18.10.

Cvent

18.11.

Hubb

18.12.

Eventbrite

18.13.

ASM Global

18.14.

SMG (now merged under ASM Global)

18.15.

Lagardère Sports and Entertainment

18.16.

SXM (Social Experience Management)

18.17.

BCD Meetings & Events

18.18.

GES (Global Experience Specialists)

18.19.

Comexposium

18.20.

UBM (now part of Informa Group)

18.21.

Other Prominent Players

19.

Research

Methodology

19.1. External

Transportations / Databases

19.2. Internal

Proprietary Database

19.3. Primary

Research

19.4. Secondary

Research

19.5. Assumptions

19.6. Limitations

19.7. Report

FAQs

20.

Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables