Eyewear Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: Product Type (Prescription Glasses/Spectacles, Sunglasses, and Contact Lenses), End User (Men and Women), Mode of Sale (Retail Stores and Online Stores), and Geography

2026-02-04

Consumer Products

Jaya Bundele (Research Analyst)

Description

Eyewear

Market Overview

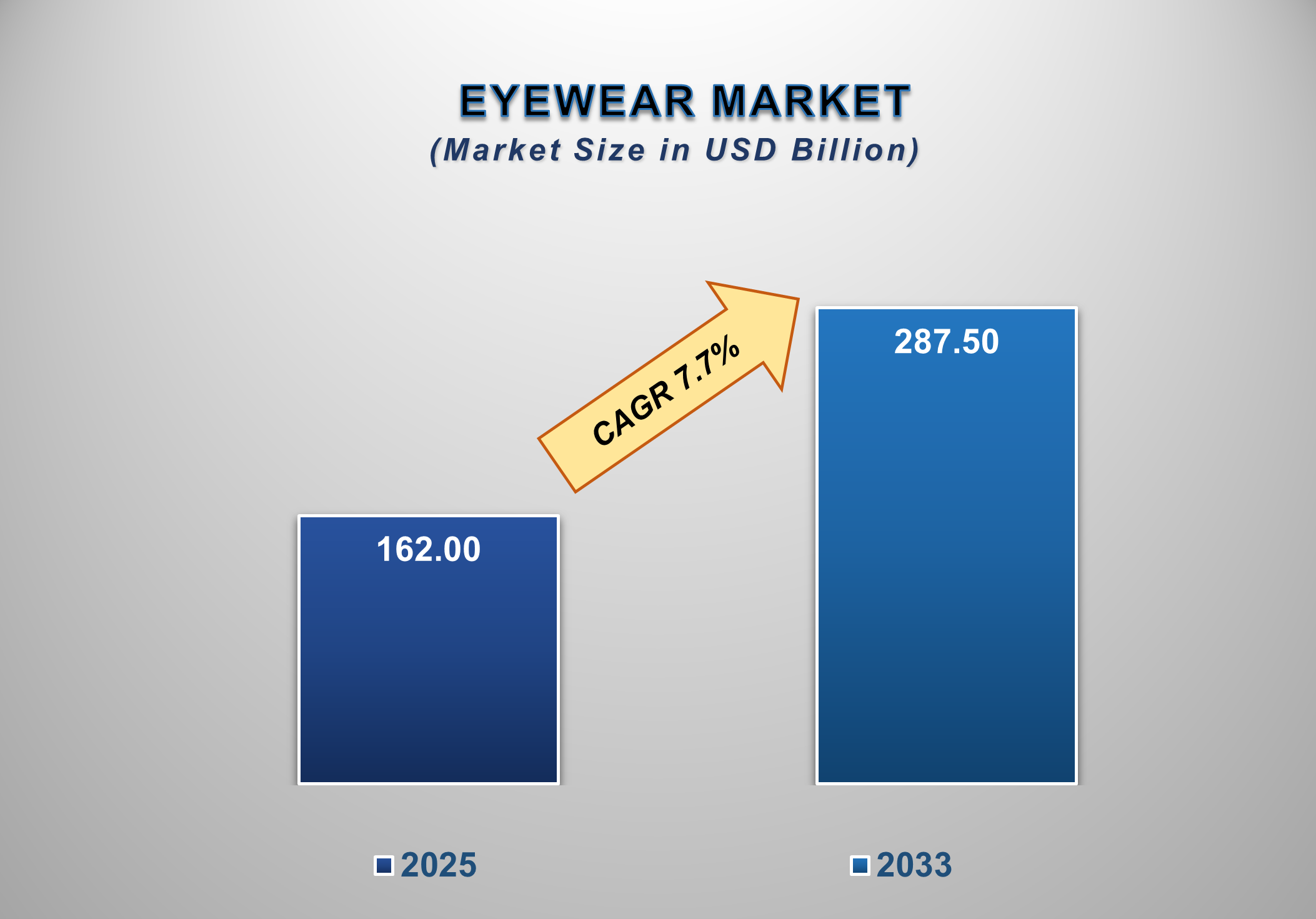

The global Eyewear

Market is experiencing strong growth, driven by a surge in eye defects and visual

impairments. Valued at USD 162.0 billion in 2025, the market is

projected to reach USD 287.5 billion by 2033, growing at a CAGR of 7.7% during

the forecast period.

The global eyewear market, which includes

fashion-forward products, eye protection, and vision correction solutions, is a

well-established yet rapidly expanding segment of the consumer goods and

healthcare industries. Sunglasses, contact lenses, and prescription

glasses/spectacles are key examples of eyewear products. These items are

essential for correcting refractive errors, protecting the eyes from harmful

radiation, and enhancing personal style. In addition to steady demand driven by

medical necessity, the industry also benefits from discretionary spending

influenced by evolving fashion trends and lifestyle preferences.

The eyewear market has changed significantly

over the past decade. Products that were once regarded primarily as medical

necessities have evolved into fashionable and technologically advanced

accessories. Aesthetics, lightweight materials, premium lenses, and

customization options have become increasingly important to brands.

Furthermore, the expansion of online eyewear platforms and the adoption of

omnichannel retail strategies have reshaped consumer purchasing behavior,

making eyewear more accessible to a broader global population.

In the wake of the COVID-19 pandemic, the

eyewear market has recovered strongly. Demand for prescription eyewear

increased due to a rise in eye strain and myopia associated with remote

working, online education, and prolonged digital device usage. At the same

time, increased outdoor activities and the recovery of tourism have supported

the resurgence of the sunglasses segment.

Eyewear

Market Drivers and Opportunities

Rising Prevalence of

Vision Disorders

The increasing prevalence of vision

impairments such as myopia, hyperopia, presbyopia, and astigmatism is one of

the key factors driving the growth of the global eyewear market. Global health

studies indicate that a significant proportion of the world’s population

requires some form of vision correction, with children and young adults

experiencing a sharp rise in myopia due to prolonged screen exposure.

Prescription glasses and contact lenses remain the most widely adopted and

cost-effective vision correction solutions, sustaining strong demand across

both developed and developing economies.

Increasing Screen Time and Digital Eye Strain

Digital eye strain has become more prevalent

due to the widespread use of laptops, tablets, smartphones, and digital work

environments. Increased screen exposure associated with remote work models,

online learning platforms, and digital entertainment has resulted in symptoms

such as headaches, blurred vision, and dry eyes. Consequently, demand for

prescription eyewear featuring anti-reflective coatings and

blue-light-filtering lenses has increased, creating new growth opportunities

for eyewear manufacturers and lens technology providers.

Growing Fashion Consciousness and Lifestyle Adoption

Eyewear has increasingly gained popularity as

a fashion accessory, particularly among younger consumers and urban

populations. Sunglasses, in particular, are often purchased as style statements

in addition to providing UV protection. Collaborations between eyewear brands

and fashion designers, celebrity endorsements, and social media influence have

elevated eyewear into a premium lifestyle category. As a result, consumers now

own multiple pairs of eyewear for different outfits, occasions, and activities,

driving higher replacement rates and overall market value.

Expansion of Online and Direct-to-Consumer Channels

The rapid growth of e-commerce and

direct-to-consumer (DTC) eyewear brands presents a significant opportunity for

market expansion. Online platforms offer competitive pricing, home delivery, a

wide product range, and digital tools such as virtual try-ons and online eye

examinations. These platforms have attracted younger, tech-savvy consumers and

improved accessibility, particularly in regions with limited physical optical

retail presence.

Aging Population and Rising Demand for Vision Correction

The global eyewear market is significantly driven

by the aging population, as vision impairment tends to increase with age.

Conditions such as presbyopia, cataracts, and age-related macular degeneration

become more prevalent among individuals aged 40 and above, leading to sustained

demand for prescription glasses and specialized lenses. As global life

expectancy continues to rise, particularly in developed regions such as North

America, Europe, and parts of Asia-Pacific, the number of people requiring routine

vision correction continues to grow. Older consumers often prefer premium,

comfortable, and high-quality eyewear solutions, including progressive lenses,

anti-glare coatings, and lightweight frames, contributing to higher average

selling prices. Increased health awareness and more frequent eye examinations

further support long-term, stable demand for eyewear products across global

markets.

Eyewear Market Scope

|

Report Attributes |

Description |

|

Market Size in

2025 |

USD 162.0

Billion |

|

Market Forecast

in 2033 |

USD 287.5

Billion |

|

CAGR % 2025-2033 |

7.7% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Comprehensive

global eyewear market size and forecast analysis, product type and

distribution channel assessment, end-user consumption trends, retail and

online sales performance evaluation, regional and country-level market

insights, competitive landscape and market share analysis, technological

advancements in lenses and frames, digital transformation and e-commerce

impact, growth drivers, challenges, opportunities, and strategic insights for

eyewear manufacturers, retailers, and investors. |

|

Segments Covered |

●

By

Product Type ●

By End

User ●

By Mode

of Sale |

|

Regional Scope |

●

North

America ●

Europe ●

APAC ●

Latin

America ●

Middle

East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada

3)

U.K. 4)

Germany

5)

France

6)

Italy 7)

Spain 8)

Switzerland

9)

China

10)

India

11)

Japan 12)

South

Korea 13)

Australia 14)

Mexico

15)

Brazil

16)

Argentina

17)

Saudi

Arabia 18)

UAE 19)

South

Africa |

Eyewear Market

Report Segmentation Analysis

The global Eyewear

Market analysis is segmented by Product Type, End User, Mode of Sale, and

Region.

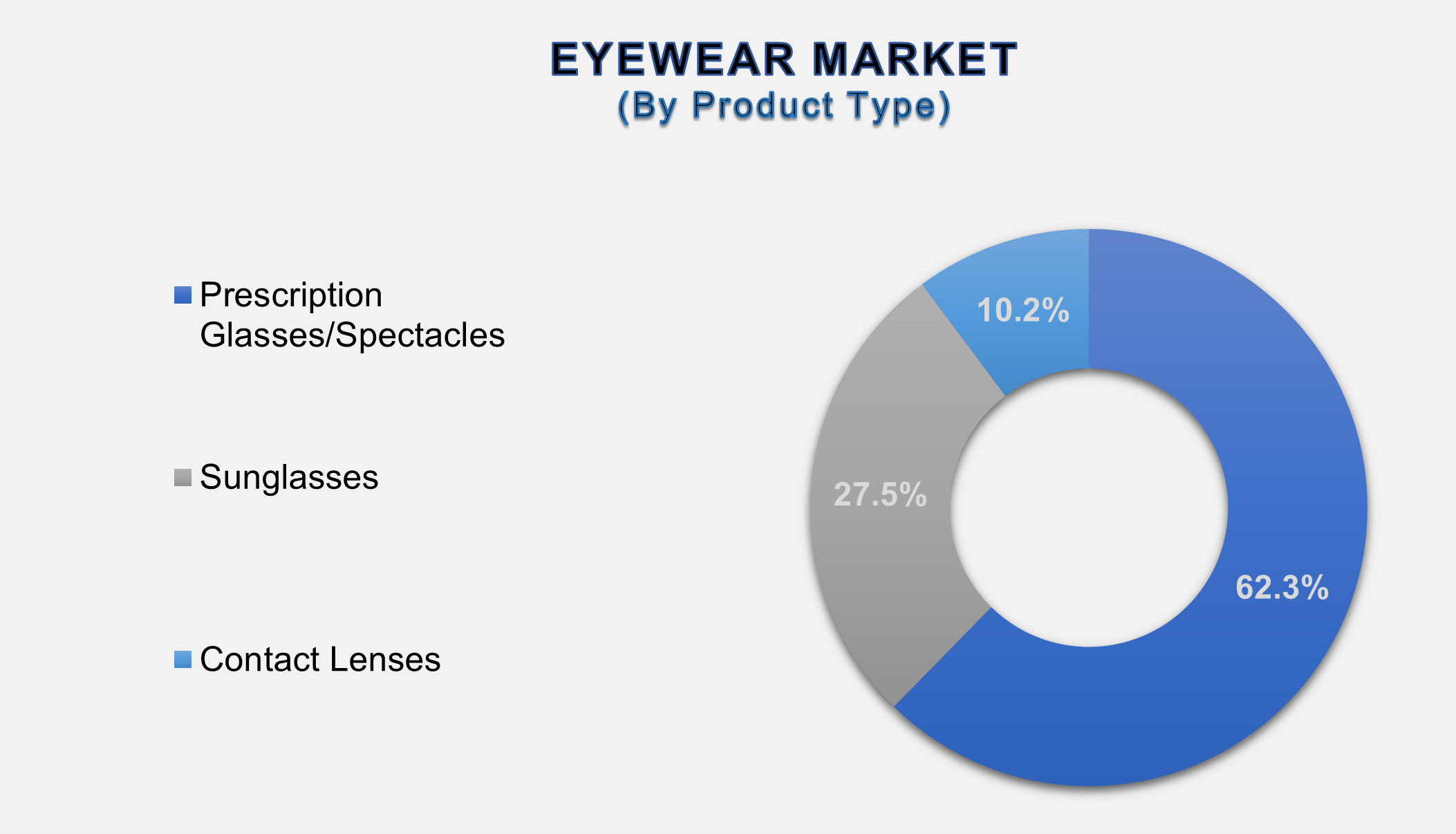

The prescription

glasses/spectacles segment dominated the market in 2025 and is projected to

grow at the highest CAGR during the forecast period.

By Product Type,

the Eyewear Market is segmented into prescription glasses/spectacles,

sunglasses, and contact lenses. The prescription glasses/spectacles segment

accounts for the largest share of the global eyewear market, primarily due to

the essential need for vision correction and the rising incidence of refractive

errors across all age groups. Technological advancements such as blue-light

blocking lenses, progressive lenses, and photochromic lenses have enhanced

product value and increased adoption rates. However, the contact lenses segment

is expected to grow at a higher CAGR during the forecast period. Innovations in

lens materials, including silicone hydrogel and daily disposable lenses, have

significantly improved comfort and safety, encouraging greater adoption among

young adults and working professionals seeking alternatives to traditional

spectacles.

Men hold the

highest share of the End User Segment over the forecast period

Based on end users, the market is bifurcated into men and women. The men's

segment accounts for the largest share of the market due to steady demand for

prescription glasses, sunglasses, and contact lenses for daily, professional,

and recreational use. Men frequently require vision correction because of

age-related vision issues and prolonged screen exposure at work, supporting

consistent demand for prescription eyewear. Sunglasses are widely used by men

for driving, sports, and outdoor activities, with an increasing preference for

durable and polarized frames. Additionally, growing fashion awareness and wider

acceptance of eyewear as a style accessory are encouraging men to purchase

multiple eyewear products, thereby increasing replacement rates and contributing

to overall market growth.

The Retail

Stores Segment will probably dominate the market during the forecast period

In terms of mode of

sale, the Eyewear Market is segmented into retail stores and online stores. The

retail stores segment holds the largest share of the eyewear market, as

consumers strongly prefer in-person purchasing for vision testing, frame

fitting, and professional consultation. Optical retail outlets, specialty

eyewear stores, and hospital-based optical centers play a critical role,

particularly for prescription glasses and contact lenses, where accuracy and

comfort are essential. Retail stores enhance customer trust and satisfaction by

offering personalized services, post-purchase support, and immediate product

availability. Moreover, many retail outlets stock a wide range of branded and

premium eyewear, attracting quality-conscious consumers. Despite growing

competition from online channels, physical retail remains the dominant sales

mode due to its reliability and service-oriented customer experience.

The following

segments are part of an in-depth analysis of the global Eyewear Market:

|

Market Segments |

|

|

By

Product Type |

●

Prescription

glasses/spectacles ●

Sunglasses ●

Contact

lenses |

|

By End

User |

●

Men ●

Women |

|

By

Mode of Sale |

●

Retail

stores ●

Online

stores |

Eyewear Market Share Analysis by Region

The Asia-Pacific

region is projected to hold the largest share of the global Eyewear Market over

the forecast period.

The

Asia-Pacific region is projected to hold the largest share of the global

eyewear market over the forecast period and is also expected to be the

fastest-growing region. The presence of a large consumer base, rising

prevalence of vision disorders, and increasing disposable incomes are the

primary factors driving market expansion. In countries such as China, India,

Japan, and South Korea, cases of myopia have increased significantly due to

rapid urbanization, expanding middle-class populations, and increased exposure

to digital devices, particularly among children and young adults. Growing

awareness of eye health and improved access to optical care services are

further supporting market growth. In addition, high smartphone penetration and

widespread adoption of e-commerce platforms are contributing to strong growth

in online eyewear sales. Affordable pricing strategies and omnichannel

distribution models are enabling both local manufacturers and global brands to

strengthen their market presence. Government initiatives focused on vision

screening and healthcare infrastructure development are also supporting

sustained growth across the Asia-Pacific region.

Global

Eyewear Market Recent Developments News:

●

In January

2025, Innovative Eyewear, Inc. announced its participation in major industry

events, including Vision Expo West and the Vision Council Executive Summit, to

showcase advancements in smart eyewear technology.

●

In April 2025,

Warby Parker raised USD 120 million in Series F funding to expand its retail

footprint and enhance technology platforms supporting omnichannel growth.

●

In May 2025, the European Commission approved the merger

of EssilorLuxottica and GrandVision, creating a global eyewear leader with an

estimated market share of approximately 70%.

●

In August

2024, the U.S. Federal Communications Commission (FCC) approved Luxottica’s

Ray-Ban Meta Smart Glasses 2.0, featuring improved battery life and enhanced

augmented reality capabilities.

The

Global Eyewear Market is dominated by a few large companies, such as

●

EssilorLuxottica

SA

●

Johnson &

Johnson Vision Care

●

Bausch + Lomb

●

CooperVision

(The Cooper Companies)

●

Alcon

●

Carl Zeiss AG

●

Safilo Group

●

HOYA

Corporation

●

Marcolin

S.p.A.

●

De Rigo Vision

●

Marchon

Eyewear

●

Fielmann AG

●

Warby Parker

●

Zenni Optical

●

JINS Inc.

●

Silhouette

International

●

Kering Eyewear

●

Prada Group

(Eyewear)

●

Lenskart

● GrandVision

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1.

Global Eyewear Market Introduction and Market Overview

1.1.

Objectives of the Study

1.2.

Global Eyewear Market Scope and Market Estimation

1.2.1.Global Eyewear

Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Eyewear

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market Segmentation

1.3.1.Product Type

of Global Eyewear Market

1.3.2.End User of

Global Eyewear Market

1.3.3.Mode of Sale of

Global Eyewear Market

1.3.4.Region of

Global Eyewear Market

2.

Executive

Summary

2.1.

Demand Side Trends

2.2.

Key Market Trends

2.3.

Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand and Opportunity Assessment

2.5.

Market Dynamics

2.5.1.Drivers

2.5.2.Limitations

2.5.3.Opportunities

2.5.4.Impact

Analysis of Drivers and Restraints

2.6.

Porter’s Five Forces Analysis

2.7.

PEST Analysis

2.8.

Key Regulation

2.9.

Key Developments

2.10. Value

Chain / Ecosystem Analysis

3.

Global

Eyewear Market Estimates & Historical Trend Analysis (2020 - 2024)

4. Global Eyewear Market Estimates & Forecast Trend Analysis, by Product Type

4.1.

Global Eyewear Market Revenue (US$ Bn) Estimates and Forecasts, by

Product Type, 2020 - 2033

4.1.1.Prescription

Glasses/Spectacles

4.1.2.Sunglasses

4.1.3.Contact

Lenses

5. Global Eyewear Market Estimates & Forecast Trend Analysis, by End User

5.1.

Global Eyewear Market Revenue (US$ Bn) Estimates and Forecasts, by

End User, 2020 - 2033

5.1.1.Men

5.1.2.Women

6. Global Eyewear Market Estimates & Forecast Trend Analysis, by Mode of Sale

6.1.

Global Eyewear Market Revenue (US$ Bn) Estimates and Forecasts, by

Mode of Sale, 2020 - 2033

6.1.1.Retail

Stores

6.1.2.Online

Stores

7.

Global

Eyewear Market Estimates & Forecast Trend Analysis, by Region

7.1.

Global Eyewear Market Revenue (US$ Bn) Estimates and Forecasts, by

Region, 2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East

& Africa

7.1.5.Latin America

8.

North America Eyewear

Market: Estimates & Forecast Trend

Analysis

8.1.

North America Eyewear Market Assessments & Key Findings

8.1.1.North America

Eyewear Market Introduction

8.1.2.North America

Eyewear Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Product Type

8.1.2.2. By End User

8.1.2.3. By Mode of Sale

8.1.2.4.

By Country

8.1.2.4.1.

The U.S.

8.1.2.4.2.

Canada

9.

Europe Eyewear

Market: Estimates & Forecast Trend

Analysis

9.1.

Europe Eyewear Market Assessments & Key Findings

9.1.1.Europe Eyewear

Market Introduction

9.1.2.Europe Eyewear

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product Type

9.1.2.2. By End User

9.1.2.3. By Mode of Sale

9.1.2.4. By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Russia

9.1.2.4.7.

Rest

of Europe

10.

Asia Pacific Eyewear

Market: Estimates & Forecast Trend

Analysis

10.1. Asia

Pacific Eyewear Market Assessments & Key Findings

10.1.1.

Asia Pacific Eyewear Market Introduction

10.1.2.

Asia Pacific Eyewear Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1. By Product Type

10.1.2.2. By End User

10.1.2.3. By Mode of Sale

10.1.2.4.

By Country

10.1.2.4.1.

China

10.1.2.4.2.

Japan

10.1.2.4.3.

India

10.1.2.4.4.

Australia

10.1.2.4.5.

South Korea

10.1.2.4.6. Rest

of Asia Pacific

11.

Middle East & Africa Eyewear Market: Estimates

& Forecast Trend Analysis

11.1. Middle

East & Africa Eyewear Market Assessments & Key Findings

11.1.1.

Middle East & Africa Eyewear

Market Introduction

11.1.2.

Middle East & Africa Eyewear

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Product Type

11.1.2.2. By End User

11.1.2.3. By Mode of Sale

11.1.2.4.

By Country

11.1.2.4.1.

UAE

11.1.2.4.2.

Saudi Arabia

11.1.2.4.3.

South Africa

11.1.2.4.4. Rest of MEA

12.

Latin America Eyewear

Market: Estimates & Forecast Trend

Analysis

12.1. Latin

America Event Industry Assessments & Key Findings

12.1.1.

Latin America Eyewear Market Introduction

12.1.2.

Latin America Eyewear Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

12.1.2.1. By Product Type

12.1.2.2. By End User

12.1.2.3. By Mode of Sale

12.1.2.4.

By Country

12.1.2.4.1.

Brazil

12.1.2.4.2.

Mexico

12.1.2.4.3.

Argentina

12.1.2.4.4. Rest of LATAM

13.

Country Wise Market: Introduction

14. Competition

Landscape

14.1. Global

Eyewear Market Product Mapping

14.2. Global

Eyewear Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3. Global

Eyewear Market Tier Structure Analysis

14.4. Global

Eyewear Market Concentration & Company Market Shares (%) Analysis, 2024

15. Company

Profiles

15.1.

EssilorLuxottica SA

15.1.1.

Company Overview & Key Stats

15.1.2.

Financial Performance & KPIs

15.1.3.

Product Portfolio

15.1.4.

SWOT Analysis

15.1.5.

Business Strategy & Recent Developments

*

Similar details would be provided for all the players mentioned below

15.2.

Johnson & Johnson Vision Care

15.3.

Bausch + Lomb

15.4.

CooperVision (The Cooper Companies)

15.5.

Alcon

15.6.

Carl Zeiss AG

15.7.

Safilo Group

15.8.

HOYA Corporation

15.9.

Marcolin S.p.A.

15.10.

De Rigo Vision

15.11.

Marchon Eyewear

15.12.

Fielmann AG

15.13.

Warby Parker

15.14.

Zenni Optical

15.15.

JINS Inc.

15.16.

Silhouette International

15.17.

Kering Eyewear

15.18.

Prada Group (Eyewear)

15.19.

Lenskart

15.20.

GrandVision

15.21.

Other Prominent Players

16.

Research

Methodology

16.1. External

Transportations / Databases

16.2. Internal

Proprietary Database

16.3. Primary

Research

16.4. Secondary

Research

16.5. Assumptions

16.6. Limitations

16.7. Report

FAQs

17.

Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables