Fishing Vessel Market Size and Forecast (2025–2033), Global and Regional Share, Trends, and Industry Analysis Report Coverage: By Deck Type (Large Decks, Medium Decks, Small Decks), By Trawlers (Freezer Trawlers, Wet-Fish Trawlers, Side Trawlers, Outrigger Trawlers, Factory Trawlers, Stern Trawlers), By Engine Capacity (<200 HP, 200–300 HP, >300 HP), and Geography

2026-01-30

Aerospace & Defense

Ekta Chaurasia (Team Lead)

Description

Fishing Vessel Market Overview

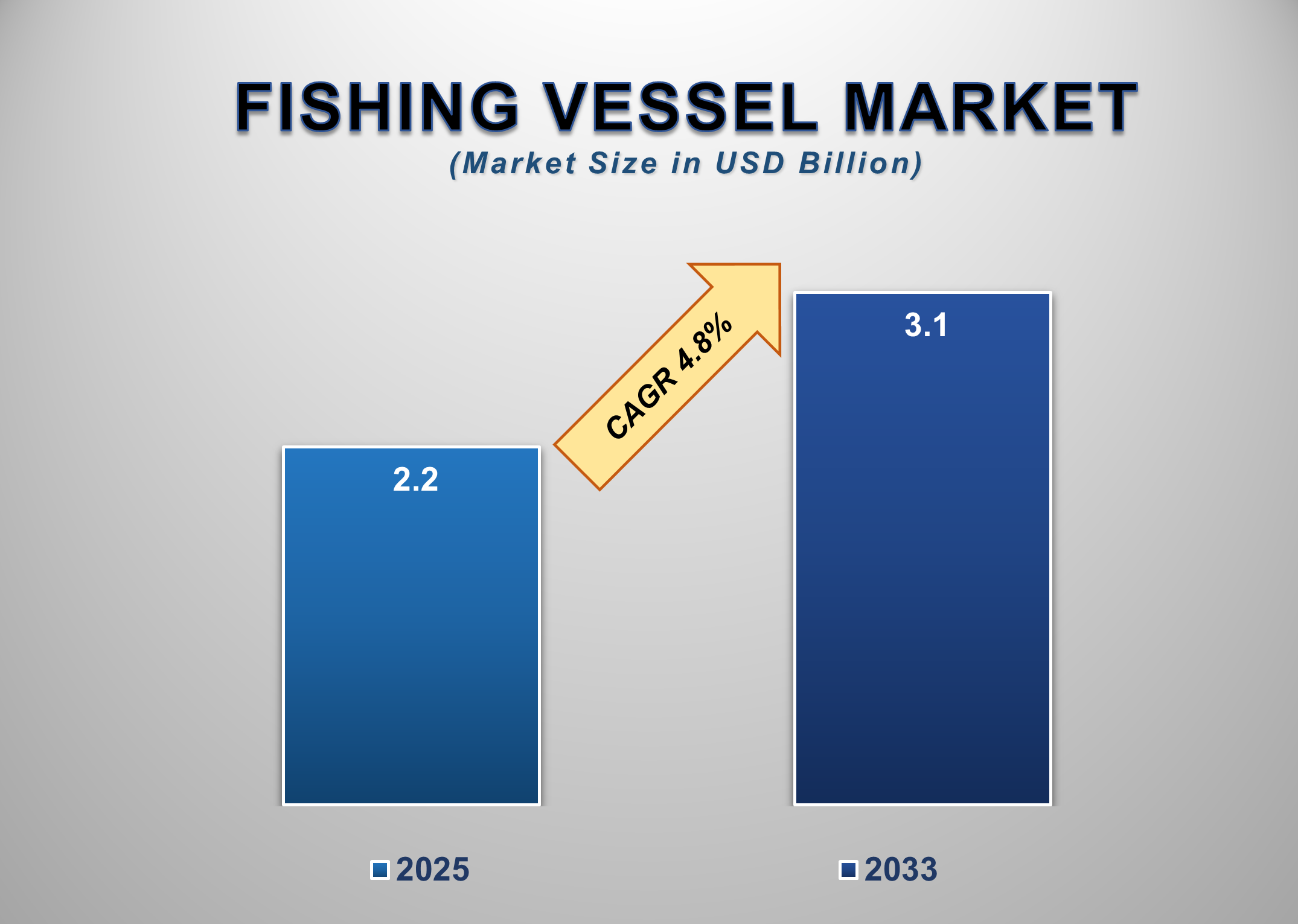

The global Fishing Vessel Market is a vital component of the commercial fishing and seafood supply chain, supporting large-scale harvesting, processing, and transportation of marine resources. Valued at USD 2.2 billion in 2025, the market is expected to reach USD 3.1 billion by 2033, registering a CAGR of 4.8% during the forecast period. Fishing vessels range from small coastal boats to large industrial trawlers equipped with advanced navigation, refrigeration, and fish processing systems.

Market growth is driven by rising

global seafood consumption, increasing demand for protein-rich diets, and

expanding commercial fishing activities in offshore and deep-sea waters.

Governments and private operators are investing in modern vessels to improve

fuel efficiency, catch optimization, crew safety, and regulatory compliance.

Technological advancements such as GPS navigation, sonar systems, automated

trawling equipment, and onboard freezing facilities are transforming vessel

productivity and operational efficiency.

Fishing Vessel Market

Drivers and Opportunities

Rising

Global Seafood Demand Is Driving Investment in Modern Fishing Vessels

The growing global demand for seafood is a primary driver of the

Fishing Vessel Market. Fish and seafood are increasingly recognized as

essential sources of high-quality protein, omega-3 fatty acids, and other

nutrients, driving consumption across developed and emerging economies. This

rising demand is encouraging commercial fishing operators to expand and

modernize their fleets to improve catch volumes and operational efficiency.

Large-scale fishing companies are investing in freezer trawlers and factory trawlers

capable of processing and preserving fish onboard, allowing longer voyages and

reduced post-harvest losses. Additionally, population growth, urbanization, and

changing dietary preferences are boosting seafood consumption, particularly in

the Asia-Pacific and coastal regions. Governments are also supporting fleet

upgrades through subsidies, financing programs, and fisheries development

initiatives. As demand for consistent and high-quality seafood supplies

increases, the need for reliable, efficient, and technologically advanced

fishing vessels continues to rise, directly supporting market growth.

Technological Advancements and Fleet Modernization Are

Enhancing Vessel Efficiency

Technological advancements in vessel design, propulsion systems,

and onboard equipment are significantly influencing the Fishing Vessel Market.

Modern fishing vessels are increasingly equipped with advanced navigation

systems, fish-finding sonar, automated hauling equipment, and energy-efficient

engines. These technologies enhance catch accuracy, reduce fuel consumption,

and improve crew safety. Fleet modernization programs in several countries aim

to replace aging vessels with newer models that comply with environmental

regulations and safety standards. Improved hull designs, lightweight materials,

and hybrid propulsion systems are being adopted to reduce emissions and

operating costs. Onboard refrigeration and freezing technologies also enable

longer fishing trips and better preservation of catch quality. As regulatory

bodies enforce stricter sustainability and safety requirements, vessel owners

are compelled to invest in modern fishing vessels, accelerating market demand

over the forecast period.

Expansion of Offshore and Deep-Sea Fishing Creates Long-Term

Market Opportunities

The expansion of offshore and deep-sea fishing activities presents a significant growth opportunity for the Fishing Vessel Market. Declining nearshore fish stocks and stricter coastal fishing regulations are pushing operators toward deeper waters, requiring larger, more capable vessels. These vessels must be equipped with high-capacity engines, advanced navigation systems, and onboard processing facilities. Emerging fishing zones in the Indian Ocean, Pacific Ocean, and parts of the Atlantic are attracting investments in freezer trawlers and factory vessels. Additionally, the growth of aquaculture support services and fishery research activities is increasing demand for specialized vessels. As global fisheries evolve toward offshore operations, demand for high-performance fishing vessels with greater endurance and capacity is expected to rise, creating sustained opportunities for shipbuilders and equipment manufacturers

Fishing Vessel Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 2.2 Billion |

|

Market Forecast in 2033 |

USD 3.1 Billion |

|

CAGR % 2025-2033 |

4.8% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factor,

and more. |

|

Segments Covered |

●

By Deck Type, By

Trawlers, By Engine Capacity |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Fishing Vessel Market

Report Segmentation Analysis

The Global Fishing Vessel Market

Industry Analysis is segmented by Deck Type, by Trawlers, by Engine Capacity,

and by Region.

The

Large Decks Segment Accounted for the Largest Market

Share in the Global Fishing Vessel Market

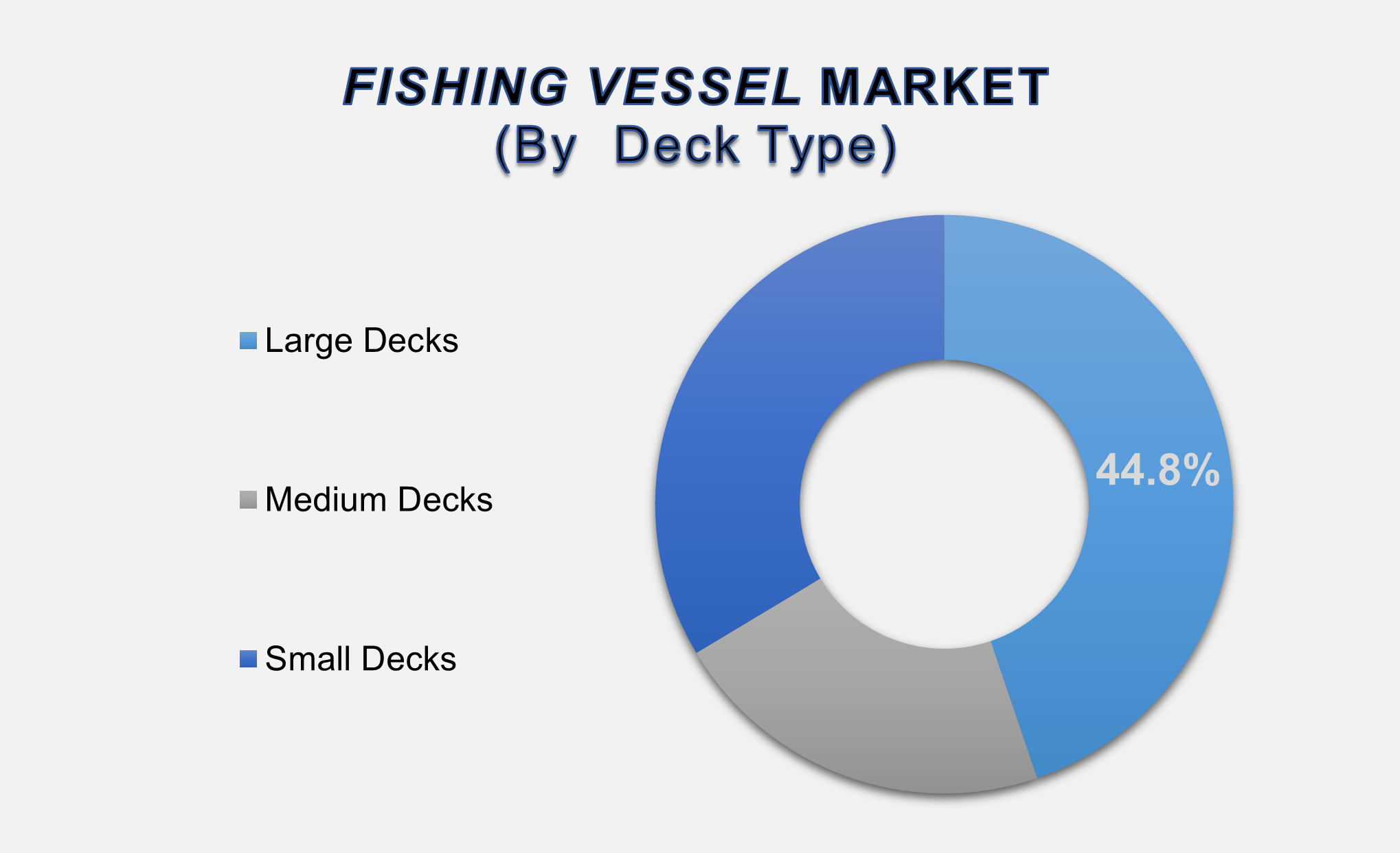

The large decks segment accounted for the largest market share at 44.8%, driven by the increasing demand for vessels capable of supporting long-duration fishing operations and onboard processing. Large-deck vessels offer higher stability, greater storage capacity, and the ability to accommodate advanced equipment such as freezing units, processing lines, and heavy-duty trawling systems. These vessels are widely used in offshore and deep-sea fishing, where extended voyages and higher catch volumes are required. Large deck configurations also improve crew safety and operational efficiency, making them the preferred choice for industrial fishing operators. As commercial fishing continues to scale up, the dominance of large deck vessels is expected to persist.

Freezer

Trawlers Segment Leads Due to Onboard Processing Capabilities

The

freezer trawlers segment holds a significant share of the market, as these

vessels enable immediate freezing and preservation of catch onboard. This

capability reduces spoilage, extends fishing duration, and improves product

quality, making freezer trawlers essential for long-distance and deep-sea

operations. Freezer trawlers are particularly popular among operators targeting

export markets, where maintaining freshness and quality is critical. The

growing demand for frozen seafood products further supports the adoption of this vessel type.

<200

HP Engine Capacity Segment Remains Prominent in Coastal Operations

The

<200 HP engine capacity segment remains widely adopted, especially for small

to medium-scale fishing operations and coastal fisheries. These vessels offer

lower operating costs, reduced fuel consumption, and easier maintenance, making

them suitable for regional fishing activities. While higher-capacity engines

are gaining traction in offshore fishing, smaller engine vessels continue to

play an important role in supporting local fisheries and sustainable fishing

practices.

The following segments are

part of an in-depth analysis of the global Fishing Vessel market:

|

Market Segments |

|

|

By Deck

Type |

●

Large Decks ●

Medium Decks ●

Small Decks |

|

By

Trawlers |

●

Freezer Trawlers ●

Wet-Fish Trawlers ●

Side Trawlers ●

Outrigger Trawlers ●

Factory Trawlers ●

Stern Trawlers |

|

By

Engine Capacity |

●

<200 HP ●

200-300 HP ●

>300 HP |

Fishing Vessel Market

Share Analysis by Region

Asia Pacific is

anticipated to hold the biggest portion of the Fishing Vessel Market globally

throughout the forecast period.

Asia-Pacific dominates the global

Fishing Vessel Market with a 41.9% share, driven by large fishing fleets,

strong seafood demand, and government-led fisheries development programs in

countries such as China, Japan, India, and Indonesia. The region’s extensive

coastline and fishing tradition further reinforce market leadership.

North America is expected to grow

at the fastest CAGR, supported by fleet renewal initiatives, sustainability

regulations, and the adoption of advanced vessel technologies. Europe maintains

a steady demand due to the modernization of fishing fleets and strict

regulatory compliance.

Fishing Vessel Market

Competition Landscape Analysis

The Fishing Vessel Market is

moderately competitive, with shipbuilders focusing on advanced vessel design,

fuel efficiency, and regulatory compliance. Companies are investing in R&D,

strategic partnerships, and customization to meet diverse fishing requirements

across regions.

Global Fishing Vessel

Market Recent Developments News:

- In September 2024,

the Ministry of Agriculture, Fisheries, and Blue and Green Economy in

Dominica signed agreements under the Dominica Emergency Agricultural

Livelihoods and Climate Resilience Project (DEALCRP) for the construction

of fifty fishing boats and the refurbishment of landing sites in Mahaut,

Bioche, and Dublanc. The initiatives aim to boost fisheries production,

enhance climate resilience, and improve livelihoods for local fishers.

- In November 2024,

an agreement was secured to

manufacture four ARESA 2500 S RWS semi-industrial purse seine fishing vessels, funded by Deutsche

Bank, destined for Angola. The vessels feature advanced suction fishing

systems and RWS Chilled Water Systems for on-board fish preservation.

- In December 2024,

Namibia deposited its instrument of accession to the 2012 Cape Town

Agreement at the International Maritime Organization (IMO), becoming the

23rd country to ratify the treaty. This move underscores Namibia's

commitment to enhancing the safety of fishing vessels and protecting crew

welfare in its maritime sector.

The Global Fishing Vessel Market

Is Dominated by a Few Large Companies, such as

●

Karstensen Skibsværft

●

Kleven Maritime

●

VARD

●

Armon Shipyards

●

Astilleros Gondán

●

Damen Shipyards Group

●

Fincantieri

●

Hakodate Dock

●

Mitsubishi Heavy

Industries

●

Tsuneishi Holdings

●

Jiangsu Jinling

Shipyard

●

China State

Shipbuilding Corporation

●

Hyundai Heavy

Industries

●

Daewoo Shipbuilding

& Marine Engineering

●

Samsung Heavy

Industries

●

STX Offshore &

Shipbuilding

●

Meyer Werft

●

Ulstein Group

●

Westcon Yards

●

Fjellstrand

● Others

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Fishing Vessel

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Fishing Vessel Market Scope and Market Estimation

1.2.1.Global Fishing Vessel Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Fishing Vessel

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Deck Type of Global Fishing

Vessel Market

1.3.2.Trawlers of Global Fishing

Vessel Market

1.3.3.Engine Capacity of Global Fishing

Vessel Market

1.3.4.Region of Global Fishing

Vessel Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Fishing Vessel Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Fishing Vessel Market Estimates

& Forecast Trend Analysis, by Deck Type

4.1.

Global

Fishing Vessel Market Revenue (US$ Bn) Estimates and Forecasts, by Deck Type, 2020

- 2033

4.1.1.Large Decks

4.1.2.Medium Decks

4.1.3.Small Decks

5. Global

Fishing Vessel Market Estimates

& Forecast Trend Analysis, by Trawlers Form

5.1.

Global

Fishing Vessel Market Revenue (US$ Bn) Estimates and Forecasts, by Trawlers

Form, 2020 - 2033

5.1.1.Freezer Trawlers

5.1.2.Wet-Fish Trawlers

5.1.3.Side Trawlers

5.1.4.Outrigger Trawlers

5.1.5.Factory Trawlers

5.1.6.Stern Trawlers

6. Global

Fishing Vessel Market Estimates

& Forecast Trend Analysis, by Engine Capacity

6.1.

Global

Fishing Vessel Market Revenue (US$ Bn) Estimates and Forecasts, by Engine

Capacity, 2020 - 2033

6.1.1.<200 HP

6.1.2.200-300 HP

6.1.3.>300 HP

7. Global

Fishing Vessel Market Estimates

& Forecast Trend Analysis, by Region

7.1.

Global

Fishing Vessel Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020

- 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Fishing

Vessel Market: Estimates & Forecast

Trend Analysis

8.1.

North

America Fishing Vessel Market Assessments & Key Findings

8.1.1.North America Fishing

Vessel Market Introduction

8.1.2.North America Fishing

Vessel Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Deck Type

8.1.2.2. By Trawlers

8.1.2.3. By Engine

Capacity

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Fishing

Vessel Market: Estimates & Forecast

Trend Analysis

9.1.

Europe

Fishing Vessel Market Assessments & Key Findings

9.1.1.Europe Fishing Vessel

Market Introduction

9.1.2.Europe Fishing Vessel

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Deck Type

9.1.2.2. By Trawlers

9.1.2.3. By Engine

Capacity

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Fishing

Vessel Market: Estimates & Forecast

Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Fishing Vessel Market Introduction

10.1.2.

Asia

Pacific Fishing Vessel Market Size Estimates and Forecast (US$ Billion) (2020 -

2033)

10.1.2.1. By Deck Type

10.1.2.2. By Trawlers

10.1.2.3. By Engine

Capacity

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Fishing

Vessel Market: Estimates & Forecast

Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Fishing Vessel Market Introduction

11.1.2.

Middle East & Africa Fishing Vessel Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Deck Type

11.1.2.2. By Trawlers

11.1.2.3. By Engine

Capacity

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Fishing Vessel Market: Estimates &

Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Fishing Vessel Market Introduction

12.1.2.

Latin

America Fishing Vessel Market Size Estimates and Forecast (US$ Billion) (2020 -

2033)

12.1.2.1. By Deck Type

12.1.2.2. By Trawlers

12.1.2.3. By Engine

Capacity

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Fishing Vessel Market Product Mapping

14.2.

Global

Fishing Vessel Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3.

Global

Fishing Vessel Market Tier Structure Analysis

14.4.

Global

Fishing Vessel Market Concentration & Company Market Shares (%) Analysis,

2024

15.

Company

Profiles

15.1.

Karstensen Skibsværft

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. Kleven

Maritime

15.3. VARD

15.4. Armon

Shipyards

15.5. Astilleros

Gondán

15.6. Damen

Shipyards Group

15.7. Fincantieri

15.8. Hakodate

Dock

15.9. Mitsubishi

Heavy Industries

15.10. Tsuneishi

Holdings

15.11. Jiangsu

Jinling Shipyard

15.12. China

State Shipbuilding Corporation

15.13. Hyundai

Heavy Industries

15.14. Daewoo

Shipbuilding & Marine Engineering

15.15. Samsung

Heavy Industries

15.16. STX

Offshore & Shipbuilding

15.17. Meyer

Werft

15.18. Ulstein

Group

15.19. Westcon

Yards

15.20. Fjellstrand

15.21. Others

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables