Flexible Display Market Size and Forecast (2026–2034), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage; Technology (OLED, LCD, E-Paper, Others), Substrate Material (Plastic, Glass, Metal Foil), Application (Smartphones & Tablets, Wearables, Television & Digital Signage, Automotive Displays, Others), and Geography

2026-03-11

Semiconductor and Electronics

Ekta Chaurasia (Team Lead)

Description

Flexible Display Market Overview

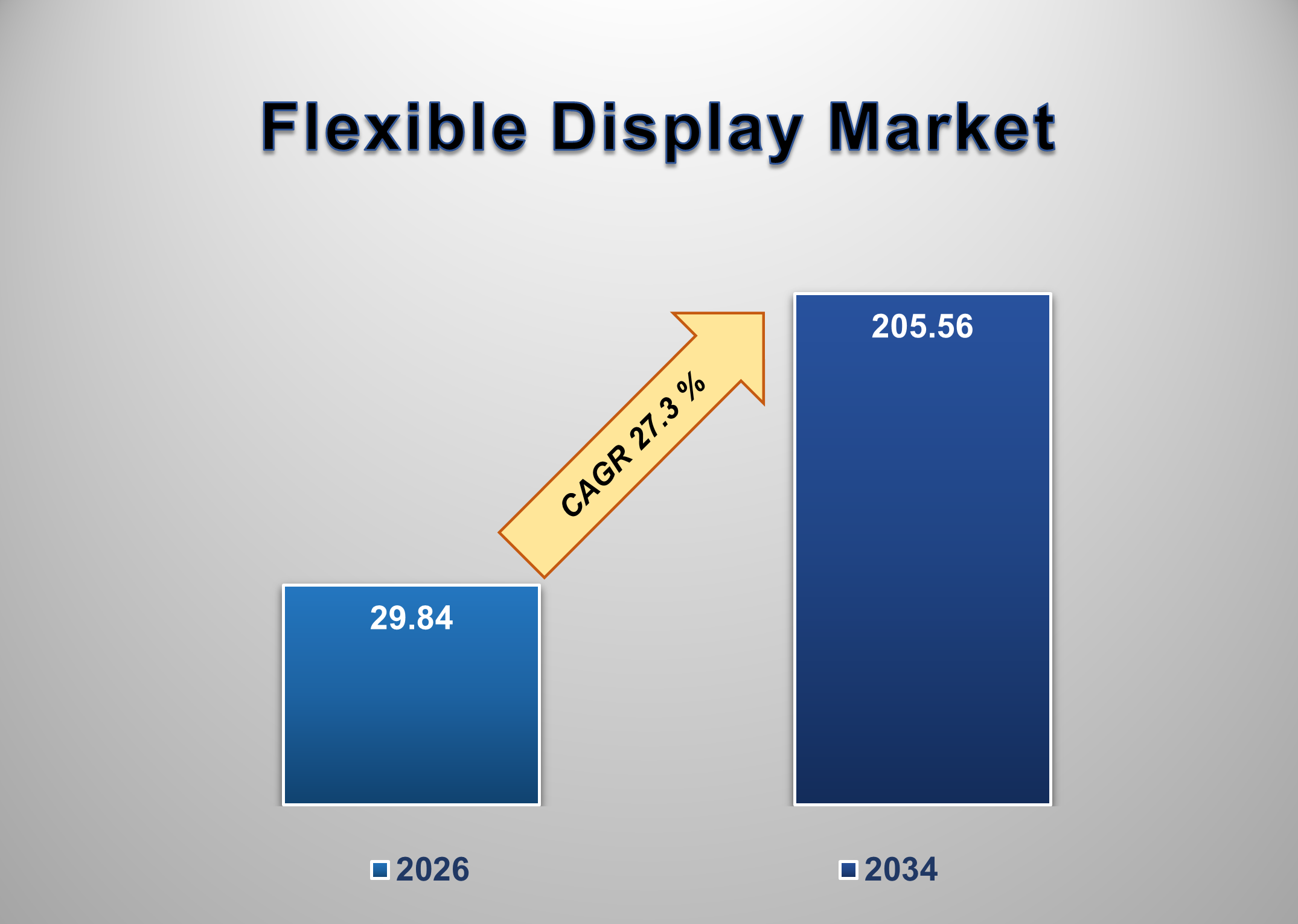

The global flexible display market is experiencing rapid growth, driven by increasing adoption of foldable consumer electronics, advancements in organic light-emitting diode (OLED) technology, and rising demand for lightweight, durable, and energy-efficient display solutions. Valued at USD 29.84 billion in 2026, the market is projected to reach USD 205.56 billion by 2034, expanding at a CAGR of 27.3% during the forecast period.

Flexible displays are electronic visual interfaces built on bendable substrates such as plastic or thin metal foils, allowing them to curve, fold, or roll without compromising performance. Unlike conventional rigid glass-based displays, flexible displays provide enhanced design versatility, reduced weight, and improved durability. The majority of commercially deployed flexible displays utilize OLED technology due to its thin form factor, high contrast ratio, and self-emissive properties.

The proliferation of foldable smartphones has significantly accelerated market adoption. Leading consumer electronics manufacturers are incorporating flexible OLED panels into premium devices to differentiate product offerings and enhance user experience. Beyond smartphones, flexible displays are gaining traction in wearable devices, automotive infotainment systems, augmented reality (AR) headsets, and digital signage.

Technological advancements in thin-film encapsulation, substrate materials, and low-temperature polycrystalline oxide (LTPO) backplane technologies have improved durability, brightness, and power efficiency. Manufacturing scale improvements and yield optimization are gradually reducing production costs, making flexible displays more commercially viable across mid-range product categories.

Despite strong growth prospects, the market faces challenges such as high production costs, complex manufacturing processes, durability concerns related to repeated folding, and supply chain concentration among a limited number of panel manufacturers. However, continued innovation and capacity expansion are expected to mitigate these constraints over time.

As consumer demand for innovative form factors and immersive visual experiences continues to grow, flexible displays are poised to become a transformative technology within the global electronics ecosystem.

Flexible Display Market Drivers and Opportunities

Rising Adoption of Foldable and Next-Generation Consumer Electronics

The increasing commercialization of foldable smartphones and dual-screen devices is a primary driver of the flexible display market. Consumers are seeking larger screen experiences without compromising portability, prompting manufacturers to adopt flexible OLED panels capable of withstanding repeated bending cycles. These displays enable clamshell and book-style folding mechanisms, offering expanded screen real estate while maintaining compact device profiles.

In addition to smartphones, flexible displays are being integrated into smartwatches, fitness trackers, and AR/VR devices, where curved or wraparound screens enhance ergonomics and user interaction. The premium positioning of foldable devices has allowed manufacturers to justify higher price points, driving revenue growth for flexible display suppliers.

Advancements in OLED Manufacturing and Material Science

Technological advancements in OLED fabrication and substrate engineering are significantly contributing to market expansion. The development of ultra-thin plastic substrates and advanced thin-film encapsulation techniques has enhanced flexibility while maintaining structural integrity. Improvements in LTPO backplane technology have also increased power efficiency and refresh rate adaptability, critical for mobile and wearable devices.

Large-scale investments in next-generation fabrication plants have improved production yields and reduced defect rates. As panel manufacturers refine roll-to-roll processing and deposition technologies, economies of scale are gradually lowering per-unit production costs. These advancements strengthen the commercial feasibility of flexible displays across broader application segments.

Expansion into Automotive and Large-Format Display Applications

A significant opportunity for market growth lies in the adoption of flexible displays within automotive interiors and large-format commercial displays. Modern vehicles increasingly incorporate curved and pillar-to-pillar digital dashboards, central infotainment screens, and heads-up displays. Flexible OLED panels allow seamless integration into curved surfaces, enhancing aesthetics and improving driver interaction.

In addition, rollable and bendable displays are being explored for large-scale digital signage and smart retail applications. Rollable television prototypes demonstrate the potential for space-saving home entertainment systems. As manufacturing capabilities mature and durability standards improve, flexible display adoption is expected to expand beyond consumer electronics into automotive, smart home, and commercial sectors.

Flexible Display Market Scope

Flexible Display Market Report Segmentation Analysis

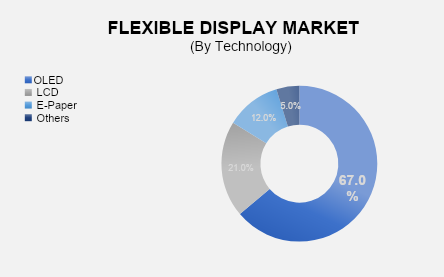

The global flexible display market analysis is segmented by Technology, Substrate Material, Application, and Region. The OLED segment dominated the market in 2025 and is projected to register the highest CAGR during the forecast period.

By technology, the market includes OLED, LCD, E-Paper, and others. OLED accounts for the largest share due to its superior flexibility, high contrast ratio, lightweight design, and self-emissive characteristics that eliminate the need for backlighting. Flexible OLED panels are thinner and more energy-efficient than traditional LCDs, making them ideal for foldable smartphones and wearable devices. Continuous improvements in pixel density, brightness levels, and durability further strengthen OLED’s dominance in the flexible display market.

Application Segment Analysis

The Smartphones & Tablets segment holds the highest share of the application segment over the forecast period.

Smartphone manufacturers are the largest adopters of flexible display technology, primarily for foldable and edge-curved premium devices. Flexible displays enable innovative product designs while improving portability and visual immersion. Increasing consumer demand for multitasking capabilities and enhanced entertainment experiences has accelerated the production of foldable smartphones. As manufacturing efficiencies improve and device prices decline, adoption is expected to expand into mid-range smartphone segments, further driving market growth.

Flexible Display Market Share Analysis by Region

Asia-Pacific is projected to hold the largest share of the global flexible display market over the forecast period.

The region’s dominance is attributed to the presence of major display panel manufacturers and strong consumer electronics production ecosystems in countries such as South Korea, China, and Japan. Significant investments in OLED fabrication facilities, coupled with high demand for premium smartphones, drive regional growth. Additionally, supportive government policies and advanced semiconductor supply chains further reinforce the Asia-Pacific’s leadership in flexible display manufacturing and innovation.

Flexible Display Market Recent Developments News

In January 2025, Samsung Display announced the expansion of its flexible OLED production capacity to support increasing demand for foldable smartphones.

In May 2025, LG Display introduced a next-generation rollable OLED panel designed for large-format television applications.

In September 2025, BOE Technology Group unveiled an ultra-thin flexible display optimized for automotive dashboard integration.

Competitive Landscape

The Global Flexible Display Market is dominated by a few large companies, such as

Samsung Display Co., Ltd.

LG Display Co., Ltd.

BOE Technology Group Co., Ltd.

Japan Display Inc.

AU Optronics Corp.

Tianma Microelectronics Co., Ltd.

Visionox Technology Inc.

Royole Corporation

Innolux Corporation

Sharp Corporation

E Ink Holdings Inc.

Sony Group Corporation

CSOT (China Star Optoelectronics Technology)

Panasonic Holdings Corporation

Koninklijke Philips N.V.

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

Flexible Display Market

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables